Applied AI In Energy And Utilities Market Size 2025-2029

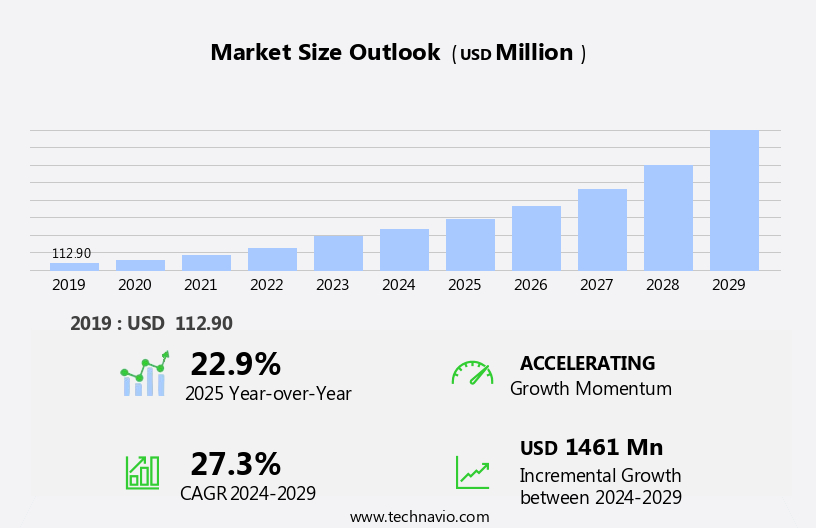

The applied AI in energy and utilities market size is forecast to increase by USD 1.46 billion, at a CAGR of 27.3% between 2024 and 2029.

- The market is witnessing significant growth, driven by the critical imperative for grid modernization and resilience. Advanced technologies, including Generative AI, are revolutionizing the energy sector by enabling predictive maintenance and advanced operational simulation. This innovation allows companies to optimize energy production, reduce downtime, and enhance overall efficiency. However, the market's expansion is not without challenges. As AI systems process increasingly large volumes of sensitive data, ensuring data protection and compliance becomes essential.

- Companies must invest in robust cybersecurity measures and adhere to regulatory frameworks to mitigate risks and maintain customer trust. These challenges, while daunting, present opportunities for market participants to differentiate themselves by offering secure and compliant AI solutions. By addressing these complexities, companies can capitalize on the market's potential and contribute to a more efficient, reliable, and sustainable energy future. Navigating data security, privacy, and governance complexities poses a significant hurdle.

What will be the Size of the Applied AI In Energy And Utilities Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The energy and utilities market continues to evolve, with artificial intelligence (AI) playing an increasingly significant role in optimizing operations and enhancing efficiency across various sectors. AI-powered asset management, for instance, enables utilities to predict maintenance needs, reducing downtime and extending asset life. Deep learning energy analysis, leveraging neural networks, improves energy production and distribution efficiency. Computer vision energy solutions analyze satellite and drone imagery for geospatial energy analytics, optimizing renewable energy generation and distribution. Energy efficiency AI and operational efficiency AI streamline processes, reducing costs and improving overall performance. AI-driven resource allocation and IOT energy integration enable real-time monitoring and response to energy demand.

Utility data visualization and advanced metering infrastructure provide insights into energy consumption patterns, enabling demand-side management and customer energy profiling. AI-driven grid optimization and outage prediction improve grid stability and reliability. Distributed generation AI optimizes energy storage and enhances the integration of renewable energy sources. Utility workforce optimization, proactive grid management, and grid stability algorithms ensure efficient workforce deployment and grid maintenance. Renewable energy forecasting and real-time energy monitoring enable accurate predictions and responsive adjustments. Load forecasting algorithms and predictive maintenance AI prevent potential issues before they become major problems.

According to a recent industry report, the global AI in energy market is expected to grow by over 20% annually in the coming years, underscoring the market's continuous dynamism and the growing importance of AI in the energy and utilities sector. For example, one utility company implemented an AI-powered predictive maintenance solution, resulting in a 30% reduction in maintenance costs and a 15% increase in asset availability.

How is this Applied AI In Energy And Utilities Industry segmented?

The applied AI in energy and utilities industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Application

- Renewables management

- Demand forecasting

- Grid management

- Energy management and optimization

- Others

- Technology

- Machine learning

- Predictive analytics

- Deep learning

- Computer vision

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Deployment Insights

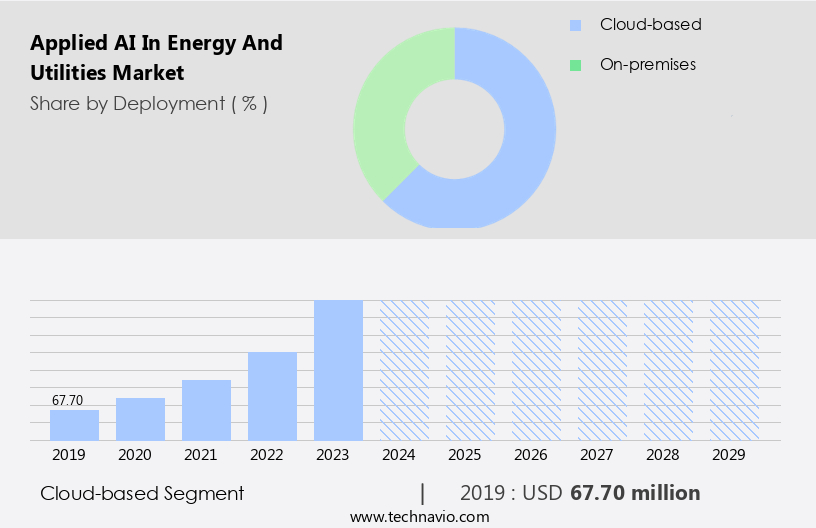

The Cloud-based segment is estimated to witness significant growth during the forecast period. The market is experiencing significant growth, with cloud-based solutions leading the charge. Hosting AI applications and processing data on third-party cloud services like Amazon Web Services, Microsoft Azure, and Google Cloud is becoming the preferred choice for utilities due to its scalability, cost efficiency, and access to advanced analytical tools. For instance, long-term electricity demand forecasting, which requires petabytes of data and immense processing power to account for weather patterns, economic indicators, and the rise of electric vehicles, is made feasible by cloud-based solutions. AI-powered asset management, deep learning energy, computer vision energy, geospatial energy analytics, energy efficiency AI, operational efficiency AI, and AI-driven resource allocation are some of the applications transforming the energy sector.

Moreover, IoT energy integration, utility data visualization, advanced metering infrastructure, AI-driven grid optimization, AI-powered outage prediction, distributed generation AI, utility workforce optimization, grid stability algorithms, demand-side management AI, energy storage optimization, condition-based maintenance, proactive grid management, renewable energy forecasting, real-time energy monitoring, load forecasting algorithms, customer energy profiling, predictive maintenance AI, energy consumption patterns, smart grid cybersecurity, and AI-based anomaly detection are all integral components of this dynamic market. According to recent estimates, the market is projected to grow by over 20% annually, underscoring its transformative potential. Smart grid cybersecurity and AI-based anomaly detection ensure the security and reliability of the energy infrastructure.

The Cloud-based segment was valued at USD 67.70 billion in 2019 and showed a gradual increase during the forecast period.

The Applied AI in Energy and Utilities Market is rapidly transforming with technologies like energy system modeling and power grid automation, enabling efficient grid operations. Smart city energy management and AI in utility operations enhance urban sustainability. Tools for risk assessment AI and energy infrastructure AI ensure system reliability. Innovations such as autonomous grid control and microgrid control systems support localized energy networks. Demand response optimization and energy conservation strategies reduce operational costs. Solar panel performance is improved through real-time monitoring. Smart meter data analytics and machine learning power grid enable predictive maintenance. Power system simulation AI and natural language processing energy aid planning. Additionally, AI in energy trading and digital twin energy systems drive operational intelligence.

Regional Analysis

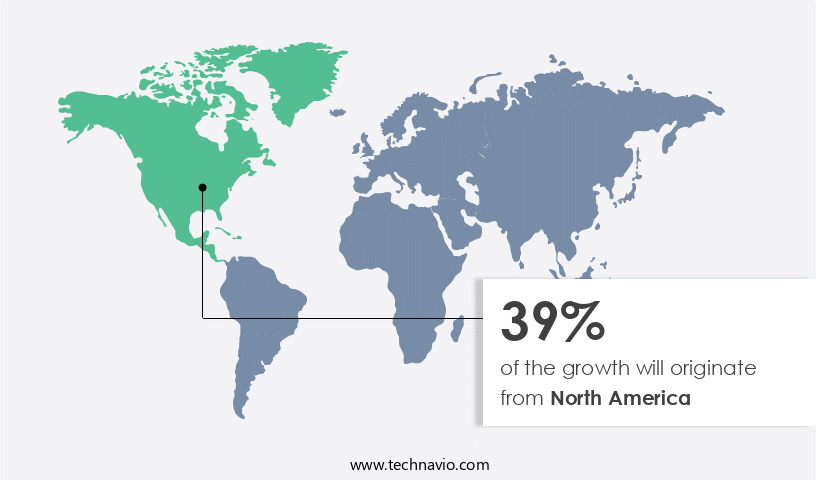

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

Artificial intelligence (AI) is transforming the energy and utilities sector in North America, with the region leading the global adoption due to several compelling drivers. Grid modernization is a pressing requirement to replace aging infrastructure, and AI technologies such as deep learning energy and computer vision are at the forefront of this transition. Geospatial energy analytics and IoT energy integration enable real-time monitoring and predictive maintenance, improving operational efficiency and grid stability. AI-driven resource allocation and demand-side management optimize energy consumption patterns, reducing overall energy waste. Advanced metering infrastructure and AI-powered outage prediction enhance customer experience and grid reliability.

Renewable energy forecasting and smart grid cybersecurity are essential components of the transition to clean energy sources, while AI-based anomaly detection ensures grid security. The energy storage optimization and condition-based maintenance further boost grid resilience. The United States, with its innovative technology ecosystem, is a hub for AI startups and established tech giants, fostering a competitive landscape. According to recent research, the North American AI in energy and utilities market is expected to grow by 15% annually, underscoring the sector's potential for significant growth. For instance, a leading utility company in the US implemented an AI-powered predictive maintenance system, resulting in a 20% reduction in unplanned downtime and a 15% increase in operational efficiency.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The market is experiencing significant growth as companies seek to leverage advanced technologies to optimize energy production, distribution, and consumption. AI algorithms for grid stability are being used to maintain power system balance and improve grid reliability. Machine learning for energy trading is enabling more accurate price forecasting and efficient energy market participation. Deep learning applications in power systems are enhancing power system analysis and improving the integration of renewable energy sources. Predictive analytics for power generation is helping utilities optimize generation capacity and reduce downtime.

AI-powered optimization of renewable energy is improving the efficiency and effectiveness of renewable energy sources, while natural language processing in utility billing is streamlining customer interactions and reducing billing errors. Computer vision for infrastructure inspection is enabling early detection of infrastructure issues, reducing maintenance costs and improving safety. IoT sensor data for energy efficiency is providing real-time insights into energy usage patterns, enabling proactive energy management. Advanced metering infrastructure data analysis is enabling more accurate energy consumption forecasting and demand response programs. AI-driven solutions for grid modernization are improving grid flexibility and resilience, while machine learning models for load forecasting are helping utilities better manage energy demand.

Predictive maintenance of energy assets is reducing downtime and maintenance costs, while AI in optimizing energy storage systems is improving energy storage efficiency and reducing costs. Real-time anomaly detection in power grids is enabling faster response times to grid issues, and deep learning for energy consumption prediction is helping utilities better understand energy usage patterns and optimize energy distribution. AI-driven solutions for smart city energy are enabling more efficient energy management in urban areas, while geospatial analytics for energy infrastructure is providing valuable insights into energy infrastructure performance and potential upgrades. AI-powered customer energy management systems are enabling more personalized energy management, and data visualization tools for utility operations are improving operational efficiency and effectiveness.

Overall, the market is transforming the energy industry, enabling more efficient, effective, and sustainable energy production, distribution, and consumption.

What are the key market drivers leading to the rise in the adoption of Applied AI In Energy And Utilities Industry?

- The imperative need for grid modernization and resilience serves as the primary market driver. In today's world, ensuring a reliable and efficient power grid is not only critical but mandatory for meeting the increasing energy demands and mitigating the risks of power outages and other grid-related issues. Artificial intelligence offers a robust set of solutions to shift from a reactive to a proactive and predictive grid management approach. This outdated infrastructure is increasingly susceptible to failures amplified by extreme weather events instigated by climate change, including hurricanes, heatwaves, and wildfires.

- For instance, AI-driven predictive maintenance can reduce unplanned downtime by up to 20%, ensuring a reliable power supply and minimizing potential revenue losses for utility companies. According to industry reports, the market is projected to expand at a double-digit percentage rate in the coming years. The market is experiencing significant growth due to the pressing requirement to modernize antiquated electrical grids and fortify them against the escalating risks of climate change. Infrastructure in developed regions, such as North America and Europe, is often decades old and ill-equipped to handle the intricacies of the contemporary energy sector.

What are the market trends shaping the Applied AI In Energy And Utilities Industry?

- Generative AI serves as a catalyst for predictive maintenance and advanced operational simulation, emerging as the market trend in the industry. The energy and utilities sector is undergoing a significant transformation, transitioning from traditional machine learning applications to the adoption of Generative Artificial Intelligence (AI). This shift marks a significant evolution in how organizations manage their critical assets, anticipate operational challenges, and train the upcoming workforce. Unlike traditional predictive models that identify trends in historical data, generative AI generates new synthetic data and intricate simulations, providing unparalleled opportunities for enhancing operational resilience and efficiency.

- According to recent studies, the global generative AI market in the energy sector is projected to grow by 25% in the next three years, reflecting the immense potential of this technology. The integration of generative AI in energy and utilities is poised to revolutionize the industry, offering numerous benefits such as improved asset performance, reduced operational risks, and enhanced predictive maintenance capabilities. The primary catalyst for this trend is the escalating complexity of energy systems and the pressing need to extend asset life, minimize unplanned downtime, and optimize capital expenditures amidst increasing costs and stringent regulatory oversight.

What challenges does the Applied AI In Energy And Utilities Industry face during its growth?

- Navigating the intricate data security, privacy, and governance complexities is a significant challenge that can hinder industry growth. Professionals in this field must possess extensive knowledge and expertise to effectively address these issues and ensure regulatory compliance. Failure to do so can result in reputational damage, financial losses, and legal consequences. Therefore, prioritizing and effectively managing data security, privacy, and governance is essential for any organization seeking to succeed in today's digital landscape. Artificial intelligence (AI) adoption in the energy and utilities sector faces significant hurdles due to growing concerns over data security, privacy, and governance.

- Amidst these concerns, the energy and utilities sector is projected to witness a 20% growth in AI investments over the next five years, underscoring the industry's commitment to leveraging AI for enhanced operational efficiency and resilience. However, it is crucial that companies prioritize robust security measures to mitigate potential risks and safeguard their critical infrastructure. With the integration of AI systems into energy grids and utility networks, the amount of sensitive data from smart meters, sensors, and operational technology (OT) systems increases exponentially. This convergence of IT and OT networks introduces new vulnerabilities, as cyberattacks could lead to severe consequences such as power outages, energy market manipulation, or consumer data breaches. For instance, a successful cyberattack on an AI-driven system could result in a 30% increase in power outages, as reported in a recent industry study.

Exclusive Customer Landscape

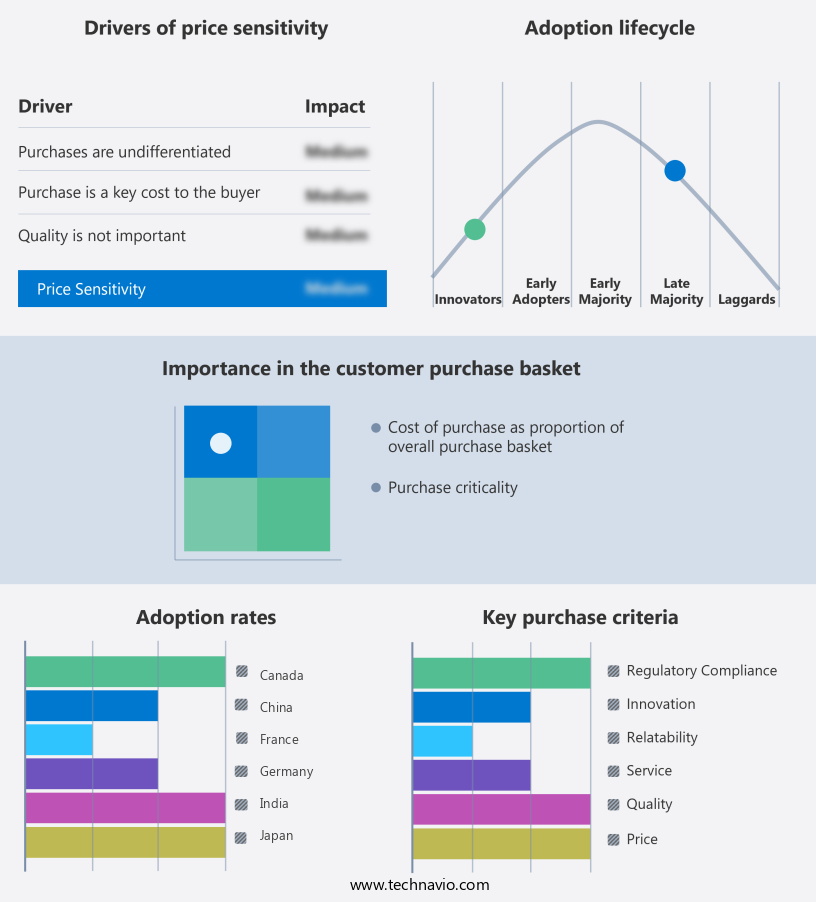

The applied AI in energy and utilities market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the applied AI in energy and utilities market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, applied AI in energy and utilities market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - The ABB Ability platform is a cutting-edge AI solution designed for energy facilities, delivering asset health monitoring, process optimization, and robotic automation capabilities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Amazon Web Services Inc.

- Arundo Analytics Inc.

- BIDGELY INC.

- C3.ai Inc.

- General Electric Co.

- Google LLC

- Honeywell International Inc.

- International Business Machines Corp.

- Landis Gyr AG

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Palantir Technologies Inc.

- SAP SE

- Schneider Electric SE

- Siemens AG

- SparkCognition Inc.

- Stem Inc.

- Verdigris Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Applied AI In Energy And Utilities Market

- In January 2024, IBM announced the launch of its new AI-powered energy management system, IBM Watson Energy and Water Insights, designed to optimize energy usage and grid management for utility companies. This solution uses machine learning algorithms to analyze real-time data and predict energy demand, thereby improving efficiency and reducing costs (IBM Press Release).

- In March 2024, Siemens Energy and Microsoft entered into a strategic partnership to integrate Microsoft Azure's AI capabilities into Siemens Energy's energy management systems. This collaboration aimed to enhance grid stability, optimize renewable energy production, and improve overall energy system performance (Microsoft News Center).

- In May 2024, Enel X, a leading energy services provider, raised USD 150 million in a funding round led by SoftBank's Vision Fund 2. The investment was earmarked for the expansion of Enel X's global energy management business, focusing on the deployment of AI and digital solutions for energy optimization and grid management (Enel X Press Release).

- In April 2025, the European Commission approved the merger of Siemens Energy and Siemens Gamesa Renewable Energy. The combined entity, Siemens New Energy, would leverage AI technologies to enhance renewable energy production, grid integration, and energy efficiency across Europe (European Commission Press Release).

Research Analyst Overview

The market for Artificial Intelligence (AI) in energy and utilities continues to evolve, with applications spanning various sectors. AI-powered fault detection and predictive asset management are transforming maintenance operations, reducing downtime and increasing efficiency. Energy blockchain technology and grid modernization AI are revolutionizing the power grid, enabling secure and decentralized energy transactions. Renewable integration AI and wind turbine maintenance optimize energy production from renewable sources, while thermal plant optimization ensures maximum efficiency. Data-driven energy systems and energy market simulation enable accurate forecasting and pricing, with renewable energy optimization and intelligent energy pricing leading to significant cost savings. Power quality monitoring and AI-driven fraud detection enhance grid security and reliability.

Hydropower plant AI and sensor data analysis optimize energy production and improve operational performance. The energy sector is expected to grow by over 12% annually, driven by the increasing adoption of AI and advanced technologies. For instance, a leading utility company achieved a 15% reduction in maintenance costs through AI-powered predictive asset management.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Applied AI In Energy And Utilities Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

255 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 27.3% |

|

Market growth 2025-2029 |

USD 1.46 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

22.9 |

|

Key countries |

US, China, Canada, India, Germany, UK, Mexico, Japan, France, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Applied AI In Energy And Utilities Market Research and Growth Report?

- CAGR of the Applied AI In Energy And Utilities industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the applied AI in energy and utilities market growth of industry companies

We can help! Our analysts can customize this applied AI in energy and utilities market research report to meet your requirements.

RIA -

RIA -