Augmented Reality (AR) Gaming Market Size 2025-2029

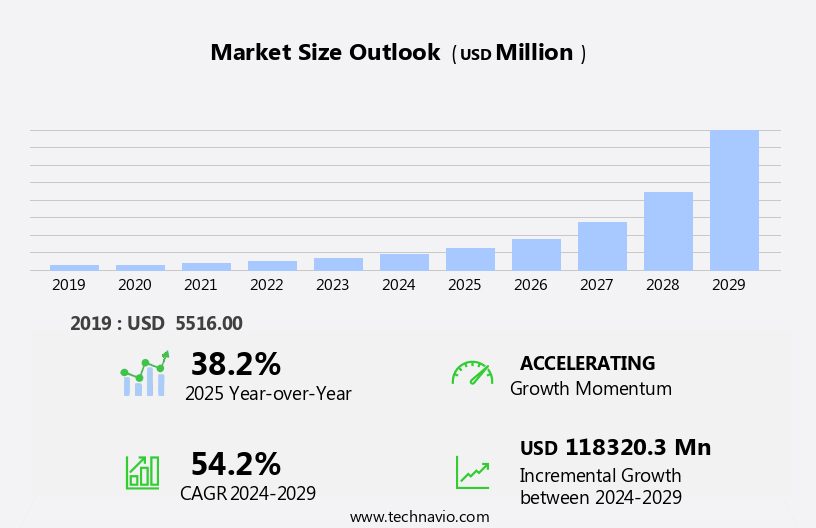

The augmented reality (ar) gaming market size is forecast to increase by USD 118.32 billion, at a CAGR of 54.2% between 2024 and 2029.

- The market is experiencing significant growth, driven by escalating investments in AR technology and the increasing popularity of AR games. The immersive nature of AR games, which overlays digital information onto the real world, is capturing the attention of consumers and driving demand. However, the high cost associated with developing and implementing AR gaming applications poses a significant challenge for market players.

- Companies must navigate this obstacle by exploring cost-effective solutions and partnerships to bring AR gaming experiences to a broader audience. To capitalize on this market's potential, businesses should focus on creating engaging and innovative AR gaming applications, while also addressing affordability concerns to ensure long-term success.

What will be the Size of the Augmented Reality (AR) Gaming Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in network infrastructure, frame rate, head-mounted displays (HMDs), and sensor fusion technology. These innovations enable more immersive experiences, enhancing player engagement across various sectors. Real-time rendering, game engines, and environmental mapping are crucial components, ensuring seamless integration of AR SDKs, spatial computing, computer vision, and data analytics. Haptic feedback, graphics rendering, and AR headsets offer new dimensions to gaming, merging digital and physical worlds. Motion tracking, cross-platform compatibility, and GPS integration broaden accessibility, while monetization strategies, such as subscription models, virtual currency, and in-app purchases, fuel market growth.

Security protocols, churn rate, and game development are essential aspects, with cloud computing and performance optimization playing a significant role in enhancing the overall user experience. Gesture recognition, depth sensing, and voice recognition add to the interactive nature of AR gaming, creating a dynamic and ever-evolving market landscape.

How is this Augmented Reality (AR) Gaming Industry segmented?

The augmented reality (ar) gaming industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

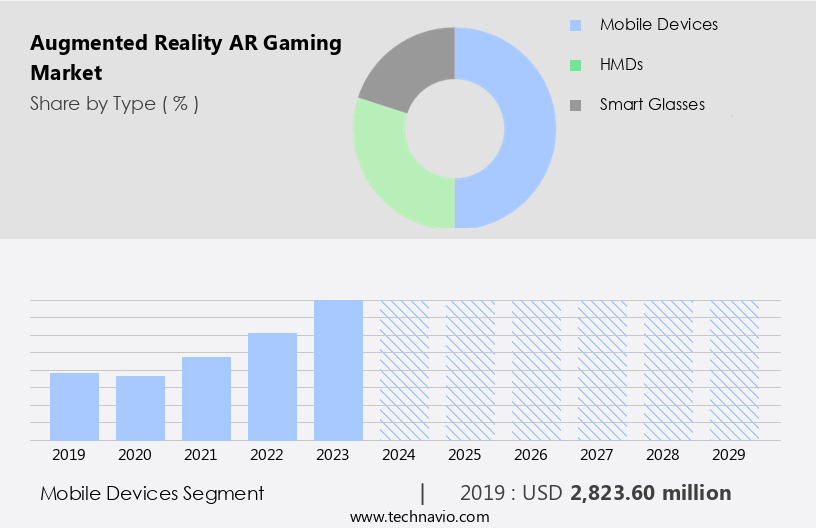

- Mobile devices

- HMDs

- Smart glasses

- Component

- Hardware

- Software

- Genre

- Adventure

- Shooter

- Puzzle

- Sports and fitness

- Business Segment

- Free-to-play

- Premium

- Subscription

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The mobile devices segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, with mobile devices leading the way. In 2024, mobile devices held the largest market share due to their convenience, reliability, and portability. AR gaming companies are increasingly investing in AR technology, making games available on mobile devices such as smartphones and laptops. The affordability and accessibility of these games are driving market growth. Subscription models and virtual currencies are popular monetization strategies in AR gaming. Player engagement is enhanced through motion tracking, cross-platform compatibility, environmental mapping, real-time rendering, and game engine technology. Data privacy and accessibility features are essential for maintaining user trust.

GPS integration, social features, and avatar customization add to the immersive gaming experience. Cloud computing, gesture recognition, performance optimization, and network infrastructure ensure seamless gameplay. Frame rate, head-mounted displays (HMDs), and PC integration offer improved graphics rendering and user experience. Security protocols and churn rate management are crucial for maintaining user retention. SLAM technology, augmented reality SDKs, and spatial computing enable advanced features like object recognition and level design. Multiplayer gaming, in-app purchases, and advertising revenue are essential revenue streams. Computer vision, data analytics, haptic feedback, and voice recognition enhance the overall gaming experience. AR headsets and overlays provide a more immersive experience.

Depth sensing and sensor fusion offer advanced motion tracking capabilities. Overall, the AR gaming market is evolving rapidly, with continuous innovation in technology and business models.

The Mobile devices segment was valued at USD 2.82 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

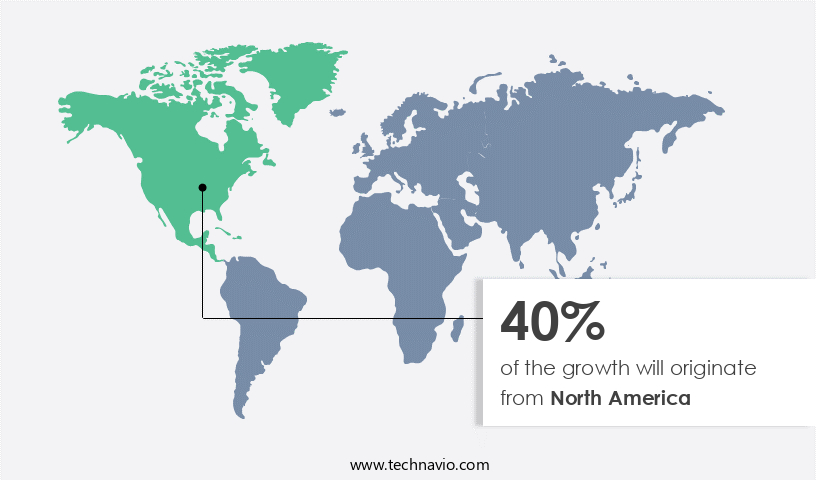

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is witnessing significant growth, with North America leading the way in 2024. Driven by the integration of advanced technologies such as the Internet of Things (IoT) and AR, mixed reality (MR), and virtual reality (VR), the market is experiencing a surge in innovation. AR technology, in particular, is gaining traction due to its immersive and harmonious nature. Companies like Qualcomm are heavily investing in AR technology, with a strong presence in the US market. For instance, Apple's Vision Pro, launched in February 2024, although marketed as a mixed reality headset, has opened new avenues for AR gaming experiences.

These include narrative-driven and spatially interactive formats. Subscriptions models are increasingly popular monetization strategies, offering players unlimited access to games and additional features. Virtual currencies and in-app purchases provide alternative revenue streams. Motion tracking and depth sensing technologies enhance player engagement, while cross-platform compatibility and real-time rendering ensure seamless gameplay. Environmental mapping and SLAM technology offer more immersive gaming experiences. Data privacy and security protocols are essential considerations, with companies implementing robust performance optimization and network infrastructure to maintain high frame rates and reduce churn. Social features, avatar customization, and multiplayer gaming foster community engagement. AR SDKs and game engines facilitate game development, while cloud computing and computer vision enable data analytics and image processing.

Haptic feedback and graphics rendering further enhance the overall gaming experience. GPS integration and voice recognition offer additional functionalities, while head-mounted displays (HMDs) and gaming console integration expand the reach of AR gaming. Gesture recognition and sensor fusion ensure intuitive user experiences. Retention rates remain a key focus, with companies implementing various strategies to keep players engaged. Advertising revenue and object recognition are emerging monetization opportunities.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The augmented reality gaming market is experiencing rapid growth, with immersive experiences captivating consumers worldwide. AR technology merges digital content with the real world, revolutionizing gaming. Players engage with interactive 3D models, virtual objects, and holograms, creating a captivating and engaging environment. AR gaming apps utilize advanced features like facial recognition, motion tracking, and location-based services to enhance gameplay. The market is driven by consumer demand for innovative gaming experiences, with applications extending beyond entertainment to education, healthcare, and retail. AR gaming offers a new dimension in social interaction, enabling multiplayer experiences and community building. The future of AR gaming is bright, with continued advancements in technology and increasing industry investment. Companies are exploring new revenue streams through in-app purchases, subscriptions, and advertising, making AR gaming a lucrative business opportunity. Gamers seek immersive experiences, and AR technology delivers, offering endless possibilities for creativity and engagement.

What are the key market drivers leading to the rise in the adoption of Augmented Reality (AR) Gaming Industry?

- As a professional virtual assistant, I'm here to help you with accurate and formal responses. Regarding your query, the market's growth is primarily attributed to the significant increase in investments dedicated to Augmented Reality (AR) technology.

- Augmented Reality (AR) gaming is an emerging technology gaining significant traction in various industries, including social media, retail, healthcare, and automotive. The integration of AR in gaming is expected to offer immersive experiences with social features, avatar customization, and 3D modeling. AR gaming platforms are also exploring gaming console integration, depth sensing, and gesture recognition for enhanced user experience. The market dynamics of AR gaming are driven by the increasing demand for cloud computing and performance optimization. With millions of users engaging in AR gaming daily, there is a need for robust security protocols to ensure user data privacy and churn rate reduction.

- Game developers are investing heavily in AR technology, leveraging the power of 3D modeling, depth sensing, and gesture recognition for creating innovative games. Investors recognize AR gaming as a high-potential frontier within the broader immersive tech ecosystem. The transfer of large amounts of data and massive processing power required for AR gaming necessitates significant investment. Companies are entering partnerships and acquisitions to expand their AR gaming offerings and stay competitive. In conclusion, the AR gaming market is poised for growth, with several market players and startups investing in innovation and collaboration to deliver immersive gaming experiences.

- The technology's potential applications extend beyond gaming, making it an exciting area for investment and innovation.

What are the market trends shaping the Augmented Reality (AR) Gaming Industry?

- The rising adoption of augmented reality (AR) games signifies a significant market trend. This emerging technology is poised to revolutionize the gaming industry, offering immersive experiences that blur the lines between the physical and digital worlds.

- Augmented Reality (AR) gaming represents an immersive and harmonious fusion of digital content and the physical world. The global market for AR gaming is experiencing significant growth, driven by the widespread adoption of smartphones and tablets, increasing network infrastructure, and the integration of AR technology into these devices. Moreover, the integration of AR gaming into Personal Computers (PC) is also propelling the market forward. Sensor fusion and Spatial Computing technologies are essential components of AR gaming, enabling real-time interaction between the virtual and real worlds. Computer vision and data analytics play a crucial role in enhancing the user experience, while haptic feedback provides a more immersive and engaging gaming experience.

- SLAM (Simultaneous Localization and Mapping) technology is another key enabler, allowing for accurate tracking of the user's position and environment. The AR gaming market is also witnessing the development and adoption of advanced technologies such as head-mounted displays (HMDs) and Augmented Reality Software Development Kits (SDKs). These technologies enable more immersive and interactive gaming experiences, increasing retention rates and user engagement. However, concerns around privacy, safety, and data usage remain, as AR games often require access to cameras, location data, and real-world mapping. It is essential for companies to address these concerns through robust data security measures and user-friendly privacy policies.

- In conclusion, the AR gaming market is experiencing significant growth, driven by the increasing adoption of AR technology and the integration of AR games into mobile devices and PCs. The use of advanced technologies such as sensor fusion, SLAM, and haptic feedback is enhancing the user experience, while the development of AR SDKs and HMDs is enabling more immersive and interactive gaming experiences. However, privacy and data security concerns remain a significant challenge, requiring robust solutions from companies to address these concerns and build user trust.

What challenges does the Augmented Reality (AR) Gaming Industry face during its growth?

- The high cost of developing and implementing augmented reality (AR) gaming applications poses a significant challenge to the industry's growth. This financial barrier can hinder the expansion and mainstream adoption of AR technology in the gaming sector.

- The market offers immersive experiences by integrating digital graphics with real-world environments. AR headsets and mobile devices are the primary platforms for AR gaming. The market's growth is driven by advanced graphics rendering, image processing, and voice recognition technologies. Advertising revenue, multiplayer gaming, and in-app purchases are significant revenue streams. Level design and object recognition are essential components of AR gaming, ensuring a harmonious blend of virtual and real elements.

- The development process for AR gaming solutions varies in complexity and cost. Simple product visualizations have lower production costs than intricate, interactive standalone games. Realistic animations and intuitive user interfaces increase development time and expenses. AR gaming's potential is vast, offering limitless opportunities for innovation and growth.

Exclusive Customer Landscape

The augmented reality (ar) gaming market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the augmented reality (ar) gaming market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, augmented reality (ar) gaming market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Apple Inc. - The company showcases an innovative approach to augmented reality (AR) technology, integrating Apple's Vision Pro, ARKit, and RealityKit for immersive gaming experiences on iPhone and iPad. By leveraging these advanced tools, users can engage in interactive, 3D environments, blurring the lines between the physical and digital worlds. This cutting-edge technology offers limitless possibilities for entertainment, education, and productivity applications. By harnessing the power of AR, the company is at the forefront of transforming the way we interact with technology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apple Inc.

- Blippar Ltd.

- Hofli Ltd.

- Meta Platforms Inc.

- Milkroom Studios GmbH

- Netmarble Corp.

- Niantic Inc.

- OliveX Holdings Ltd.

- Qualcomm Inc.

- Resolution Games

- Rovio Entertainment Corp.

- Snap Inc.

- Unity Technologies Inc.

- Zappar Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Augmented Reality (AR) Gaming Market

- In January 2024, Niantic, a leading AR gaming company, launched its much-anticipated title, "Pokémon GO 2," which introduced new features like multiplayer mode and AR-enhanced location-based challenges (Niantic Press Release). In March 2024, Apple and Google strengthened their commitment to the AR gaming industry by announcing ARKit 4 and ARCore 1.11 updates, respectively, enhancing developer tools for creating immersive AR experiences (Apple Developer, Google Developers).

- In April 2024, Magic Leap, the AR headset manufacturer, secured a strategic partnership with Electronic Arts (EA) to develop exclusive AR games for their Magic Leap One headset, marking a significant step towards mainstream adoption of AR gaming (Magic Leap Press Release). In May 2025, Microsoft's Mojang Studios unveiled "Minecraft Earth," an AR version of their iconic game, at the Minecon Live event, attracting a massive fanbase and further expanding the reach of AR gaming (Mojang Studios Press Release).

Research Analyst Overview

- The market is experiencing significant growth, with innovative technologies such as 3D scanning, AR cloud, and location-based services driving engagement. Brands are leveraging marketing campaigns to promote immersive experiences, integrating AR markers and image targets for interactive gameplay. Game developers are utilizing advanced game mechanics, character design, and narrative design to create captivating content. AR glasses and depth cameras enable competitive gaming, while IMU sensors and game controllers offer enhanced user experiences. Fitness games and educational applications cater to diverse audiences, with beta testing and user feedback essential for game balancing and content creation.

- Game development frameworks facilitate the creation of location-based games, providing an analytics dashboard for tracking player behavior and optimizing game balancing. AR technology continues to revolutionize casual gaming, offering a new dimension to interactive storytelling and world building.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Augmented Reality (AR) Gaming Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

217 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 54.2% |

|

Market growth 2025-2029 |

USD 118320.3 million |

|

Market structure |

Concentrated |

|

YoY growth 2024-2025(%) |

38.2 |

|

Key countries |

US, China, Canada, Germany, UK, France, Japan, South Korea, Italy, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Augmented Reality (AR) Gaming Market Research and Growth Report?

- CAGR of the Augmented Reality (AR) Gaming industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the augmented reality (ar) gaming market growth of industry companies

We can help! Our analysts can customize this augmented reality (ar) gaming market research report to meet your requirements.

RIA -

RIA -