Automated Material Handling (Amh) Market Size 2024-2028

The automated material handling (amh) market size is valued to increase USD 46.5 billion, at a CAGR of 13.61% from 2023 to 2028. Growing e-commerce industry will drive the automated material handling (amh) market.

Major Market Trends & Insights

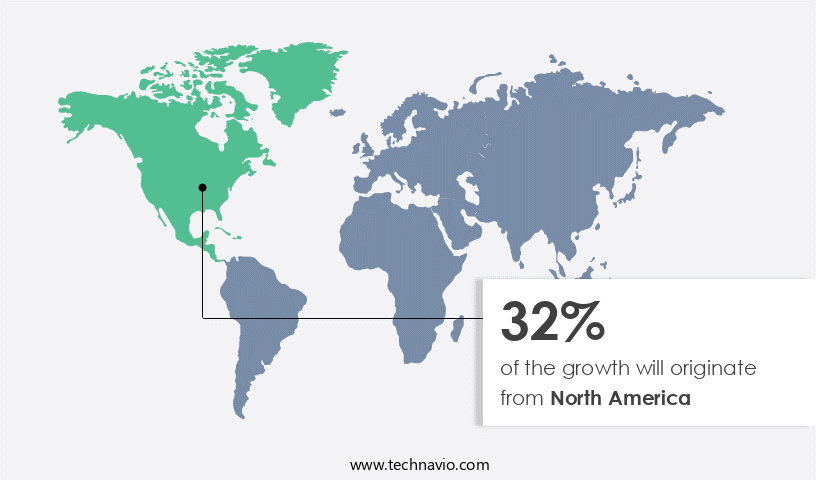

- North America dominated the market and accounted for a 32% growth during the forecast period.

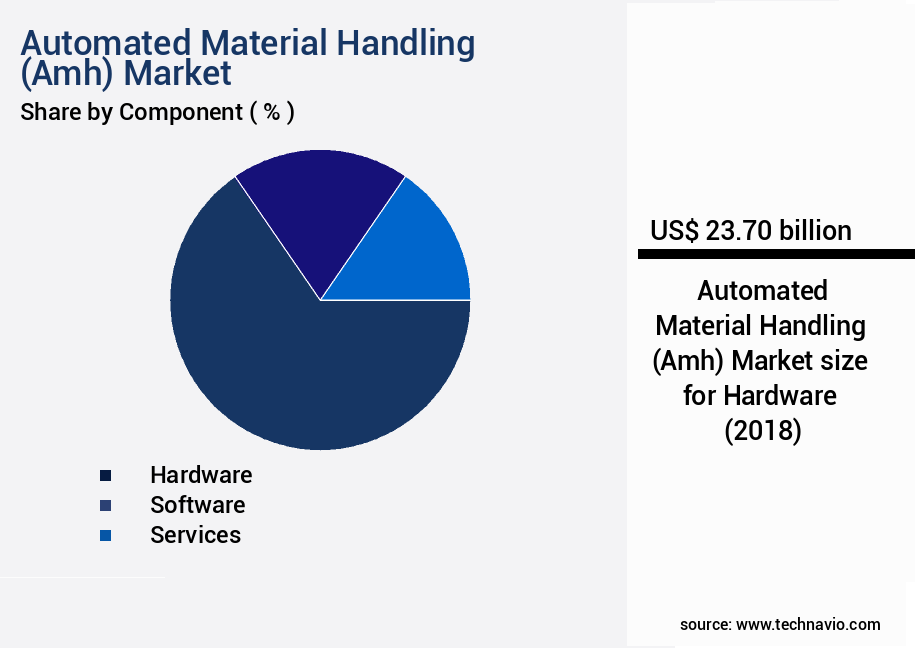

- By Component - Hardware segment was valued at USD 23.70 billion in 2022

- By End-user - Automotive segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 176.19 billion

- Market Future Opportunities: USD 46.50 billion

- CAGR from 2023 to 2028 : 13.61%

Market Summary

- In the realm of industrial production, the market has emerged as a critical catalyst for enhancing operational efficiency and productivity. With the e-commerce sector's relentless expansion, there is a surging demand for swift, precise, and uninterrupted material handling processes. This need has given rise to significant technological advances, enabling the integration of automation in various industrial applications. Despite the substantial upfront investments required for acquiring AMH equipment, businesses are recognizing the long-term benefits. These benefits include increased productivity, reduced labor costs, and improved product quality. The global AMH market is expected to reach a value of USD225 billion by 2025, underscoring its growing importance in the industrial landscape.

- The market's evolution is characterized by the integration of advanced technologies such as robotics, artificial intelligence, and the Internet of Things (IoT). These innovations facilitate real-time monitoring, predictive maintenance, and optimized workflows, enhancing overall system performance. However, challenges persist, including the high cost of implementation and the need for extensive training to effectively utilize the technology. Despite these hurdles, the future direction of the AMH market is clear: automation is becoming an indispensable component of modern industrial operations.

What will be the Size of the Automated Material Handling (Amh) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Automated Material Handling (Amh) Market Segmented ?

The automated material handling (amh) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Component

- Hardware

- Software

- Services

- End-user

- Automotive

- E-commerce and 3PL

- Food and beverage

- Others

- Geography

- North America

- US

- Europe

- France

- Germany

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Component Insights

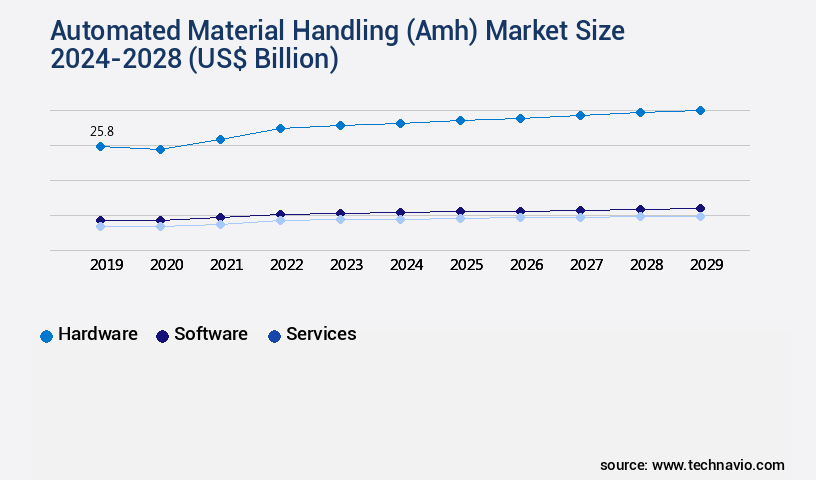

The hardware segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, integrating advanced technologies to streamline operations and enhance efficiency. Automated Guided Vehicles (AGVs) and warehouse control systems optimize labor productivity metrics, while cloud-based WMS and inventory management systems enable real-time data analytics. Safety compliance standards are upheld through robotics integration and energy efficiency measures. Human-machine interfaces (HMIs) ensure seamless order accuracy rates and error reduction strategies. Control system integration and data analytics dashboards facilitate process optimization and throughput optimization. In the realm of pallet handling, conveyor belt systems employ hydraulic, mechanical, and fully automated designs for sorting and distribution.

Lift truck systems and AGV navigation systems optimize warehouse layout design and logistics automation. Order fulfillment processes are further enhanced with real-time tracking systems and process optimization. Key statistics indicate that 64% of warehouses have already adopted some form of automation, underscoring the market's continuous growth and transformation.

The Hardware segment was valued at USD 23.70 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automated Material Handling (Amh) Market Demand is Rising in North America Request Free Sample

The market is witnessing significant growth, particularly in the Asia Pacific (APAC) region, which held the largest market share in 2023. The economic development in China and India is the primary driver of this growth. The e-commerce sector in these countries is expanding rapidly, leading to a surge in demand for efficient material handling solutions. Additionally, favorable government initiatives encouraging infrastructure development are propelling the growth of the construction industry in APAC, thereby increasing the demand for AMH equipment. Furthermore, the increasing adoption of AMH technology in the development of smart cities in APAC is expected to further fuel market growth during the forecast period.

The AMH market's expansion is a testament to its essential role in optimizing operations and enhancing productivity across various industries.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing demand for efficient and accurate warehouse operations. Advanced technologies such as automated guided vehicle navigation algorithms and warehouse control system software integration are driving innovation in the industry. These solutions enable seamless communication between different material handling systems, optimizing conveyor belt systems and improving overall warehouse performance. Robotics integration for order fulfillment is another key trend in the AMH market. By automating repetitive tasks, businesses can reduce labor costs and improve picking and packing system performance metrics. Material handling equipment maintenance strategies are also essential for ensuring the longevity and productivity of automated systems. Inventory management system data accuracy is crucial for optimizing supply chain operations using AI and ML. Automated storage and retrieval systems and design play a significant role in maximizing warehouse throughput. Real-time tracking systems for inventory control and predictive maintenance of automated equipment are essential for maintaining optimal warehouse performance. Error reduction strategies in automated systems are also critical for ensuring safety compliance standards are met. Warehouse layout design for maximum throughput is an essential consideration for businesses looking to implement a Warehouse Execution System (WES) or logistics automation system. Throughput optimization using lean manufacturing techniques and the implementation of RFID tagging strategies are also crucial for streamlining the order fulfillment process and improving overall supply chain efficiency. The benefits of order fulfillment process automation are numerous, including reduced lead times, increased accuracy, and improved customer satisfaction. ROI calculation is a critical factor for businesses considering investing in AMH solutions. By implementing these advanced technologies, businesses can reduce costs, increase productivity, and gain a competitive edge in their industries.

What are the key market drivers leading to the rise in the adoption of Automated Material Handling (Amh) Industry?

- The e-commerce industry's continued growth serves as the primary catalyst for market expansion.

- The market is experiencing significant growth and transformation, driven primarily by the burgeoning e-commerce sector. With the increasing number of online shoppers, businesses are under pressure to streamline their order processing and distribution capabilities. According to recent reports, the global e-commerce industry has seen a compound annual growth rate (CAGR) of approximately 20% over the past five years, with major markets including China, India, the US, and European nations. In the US, the e-commerce industry is expanding at a faster pace than traditional retail.

- To keep up with this demand, the number of warehouses and distribution centers has seen a substantial increase. AMH systems, such as conveyor belts, automated storage and retrieval systems, and robotic arms, are increasingly being adopted to optimize warehouse operations and enhance efficiency.

What are the market trends shaping the Automated Material Handling (Amh) Industry?

- The upcoming market trend mandates increasing technological advances in industrial operations. Technological progression is a requisite element in the evolving industrial landscape.

- The material handling market is undergoing a significant transformation, driven by the increasing demand for automation across various industries. This shift is part of the Fourth Industrial Revolution or Industry 4.0, which integrates advanced technologies such as the Internet of Things (IoT) and artificial intelligence (AI) into manufacturing and other sectors. The adoption of these technologies has led to the development of smart industries, where machine learning (ML) and big data analytics aid in autonomous decision-making in labor-intensive processes. Robotic systems, controlled remotely by computers integrated with ML, are increasingly used in industrial facilities to streamline workflows and minimize human intervention.

- According to recent estimates, the global material handling equipment market is expected to grow at a robust rate, with the market share of automated material handling systems projected to reach approximately 40% by 2025. The integration of advanced technologies in material handling is revolutionizing industries and enhancing operational efficiency.

What challenges does the Automated Material Handling (Amh) Industry face during its growth?

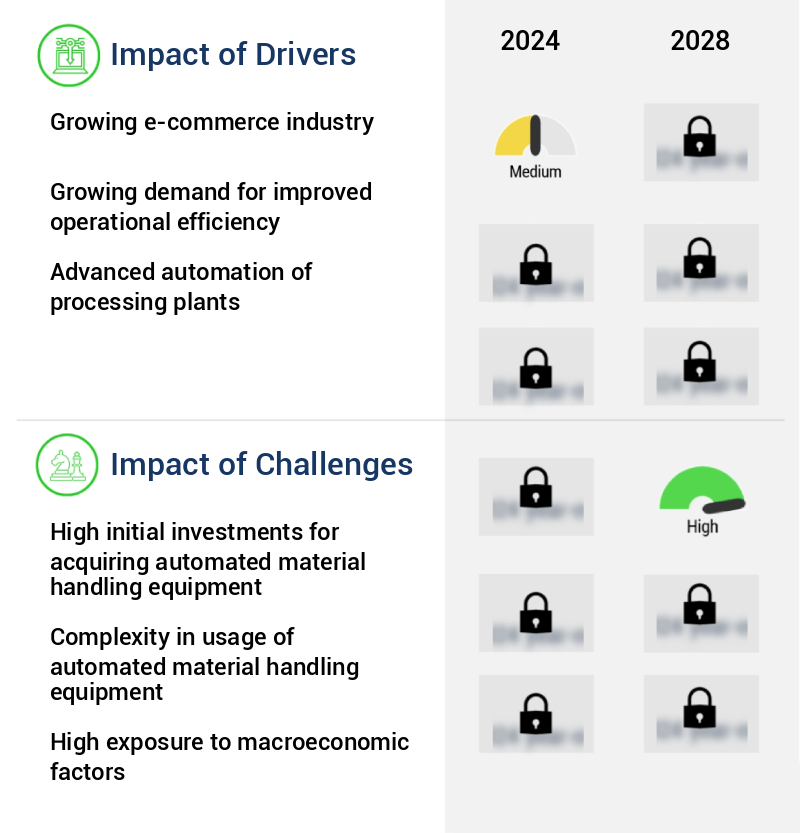

- The high initial investments required for acquiring automated material handling equipment poses a significant challenge to the industry's growth trajectory. This financial hurdle can limit the adoption rate of advanced technologies and hinder the expansion of businesses in this sector.

- The market growth is influenced by several factors, including the initial high capital expenditure required for procuring AMH equipment. This cost barrier primarily affects small- and medium-sized enterprises, who are hesitant to invest due to uncertainty regarding the return on investment (ROI). For instance, automated guided vehicles (AGVs) become cost-effective for warehouses managing over 40,000 pallets. Installation of AMH systems is another challenge, as it can disrupt revenue generation for an extended period.

- Despite these hurdles, the AMH market continues to evolve, with applications spanning various sectors, including manufacturing, logistics, and healthcare. The market's potential is underscored by the increasing demand for efficient and accurate material handling processes.

Exclusive Technavio Analysis on Customer Landscape

The automated material handling (amh) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automated material handling (amh) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automated Material Handling (Amh) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automated material handling (amh) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Addverb Technologies Pvt. Ltd. - The company specializes in automated material handling solutions, including the BG Sorter Compact CB. This innovative technology streamlines processes, enhancing operational efficiency and reducing labor costs for businesses. The BG Sorter Compact CB utilizes advanced sorting algorithms and sensors to optimize sorting accuracy and minimize errors. By automating repetitive tasks, companies can improve productivity and focus resources on core business functions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Addverb Technologies Pvt. Ltd.

- Beumer Group GmbH and Co. KG

- Daifuku Co. Ltd.

- FIVES SAS

- FlexLink Holding AB

- Hanwha Corp.

- Honeywell International Inc.

- John Bean Technologies Corp.

- Jungheinrich Group

- Kardex Holding AG

- KION GROUP AG

- KUKA AG

- Mecalux SA

- Murata Machinery Ltd.

- Robert Bosch GmbH

- Siemens AG

- SSI Schafer IT Solutions GmbH

- TGW LOGISTICS GROUP GmbH

- Toyota Industries Corp.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automated Material Handling (Amh) Market

- In January 2024, Swisslog, a leading provider of automated material handling solutions, announced the launch of its new Robotic Pallet Shuttle (RPS) system, which automates the storage and retrieval of palletized loads in warehouses (Swisslog press release, 2024). This innovation significantly enhances efficiency and flexibility in material handling operations.

- In March 2024, KION Group, a global supplier of industrial trucks and warehouse automation solutions, and Dematic, a leading automated material handling systems provider, announced their strategic partnership to combine their complementary offerings and create a global market leader in the automated material handling industry (KION Group press release, 2024).

- In May 2024, Daifuku, a leading material handling solution provider, secured a USD100 million contract from a major e-commerce company to design and build an automated distribution center in the United States (Daifuku press release, 2024). This significant project underscores the growing demand for automated material handling systems in the e-commerce sector.

- In February 2025, Siemens AG, a technology powerhouse, received approval from the European Commission for its acquisition of Sensotec, a leading provider of sensors and automation solutions for material handling applications (European Commission press release, 2025). This acquisition strengthens Siemens' position in the automated material handling market by expanding its sensor technology offerings.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automated Material Handling (Amh) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.61% |

|

Market growth 2024-2028 |

USD 46.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

11.71 |

|

Key countries |

US, China, Germany, Japan, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in technology and the increasing demand for efficient and productive warehouse operations. Automated Guided Vehicles (AGVs) and Warehouse Control Systems (WCS) are at the forefront of this evolution, streamlining material flow and optimizing labor productivity metrics. Cloud-based Warehouse Management Systems (WMS) and lift truck systems are becoming increasingly popular, offering flexibility and scalability. Safety compliance standards remain a top priority, with robotics integration and energy efficiency measures playing crucial roles in ensuring safe and sustainable operations. Human-machine interfaces (HMIs) are essential for effective communication between operators and equipment, leading to improved order accuracy rates and error reduction strategies.

- Control system integration, data analytics dashboards, and pallet handling systems are other key components of AMH systems, enabling supply chain optimization and inventory management. Warehouse layout design, material handling equipment, and sorting and distribution systems are continually evolving to meet the demands of e-commerce and omnichannel retailing. Conveyor belt systems and throughput optimization are critical for high-volume operations, while real-time tracking systems and process optimization ensure efficient order fulfillment processes. For instance, a leading retailer reported a 20% increase in sales due to the implementation of an AGV system and a WCS, resulting in faster order processing and reduced picking errors.

- Industry growth in the AMH market is expected to reach 10% annually, as businesses continue to invest in automation to enhance their competitive edge.

What are the Key Data Covered in this Automated Material Handling (Amh) Market Research and Growth Report?

-

What is the expected growth of the Automated Material Handling (Amh) Market between 2024 and 2028?

-

USD 46.5 billion, at a CAGR of 13.61%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), End-user (Automotive, E-commerce and 3PL, Food and beverage, and Others), and Geography (APAC, North America, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing e-commerce industry, High initial investments for acquiring automated material handling equipment

-

-

Who are the major players in the Automated Material Handling (Amh) Market?

-

Addverb Technologies Pvt. Ltd., Beumer Group GmbH and Co. KG, Daifuku Co. Ltd., FIVES SAS, FlexLink Holding AB, Hanwha Corp., Honeywell International Inc., John Bean Technologies Corp., Jungheinrich Group, Kardex Holding AG, KION GROUP AG, KUKA AG, Mecalux SA, Murata Machinery Ltd., Robert Bosch GmbH, Siemens AG, SSI Schafer IT Solutions GmbH, TGW LOGISTICS GROUP GmbH, Toyota Industries Corp., and Wipro Ltd.

-

Market Research Insights

- The market for automated material handling (AMH) solutions continues to evolve, with a growing emphasis on enhancing space utilization and implementing safety protocols. Preventive maintenance and operational efficiency are key priorities, driving the adoption of mobile robots and process mapping to streamline order management and robotics programming. Inventory tracking and maintenance scheduling are essential components of AMH systems, contributing to cost reduction initiatives and throughput improvement. Automation consulting and system integration are increasingly in demand to ensure compliance with safety training and AGV fleet management. Ergonomic design and performance monitoring are also critical factors, as companies seek to optimize material flow and improve capacity planning.

- Logistics software, system upgrades, and equipment selection are ongoing considerations for businesses looking to stay competitive in the industry. According to recent reports, the AMH market is expected to grow by over 10% annually, reflecting the continuous demand for more efficient and effective material handling solutions. An example of this trend can be seen in a leading manufacturing company, which reported a 15% increase in sales following the implementation of an AMH system that included inventory tracking, real-time data analysis, and supply chain visibility.

We can help! Our analysts can customize this automated material handling (amh) market research report to meet your requirements.

RIA -

RIA -