Automotive Aftermarket E-retailing Market Size 2026-2030

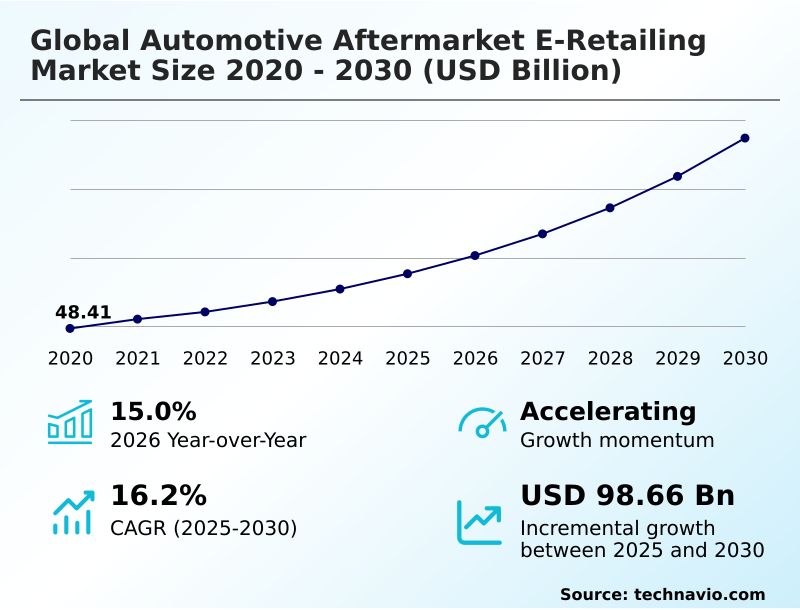

The automotive aftermarket e-retailing market size is valued to increase by USD 98.66 billion, at a CAGR of 16.2% from 2025 to 2030. Increasing average age of vehicles and extended ownership cycles will drive the automotive aftermarket e-retailing market.

Major Market Trends & Insights

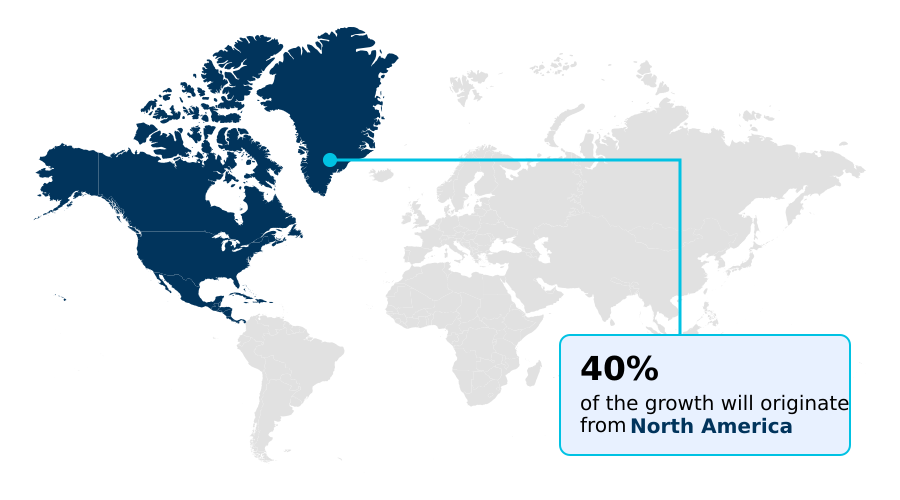

- North America dominated the market and accounted for a 39.9% growth during the forecast period.

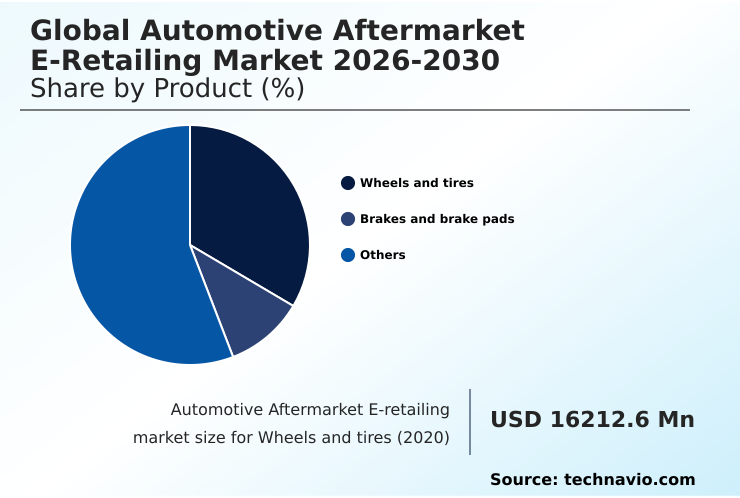

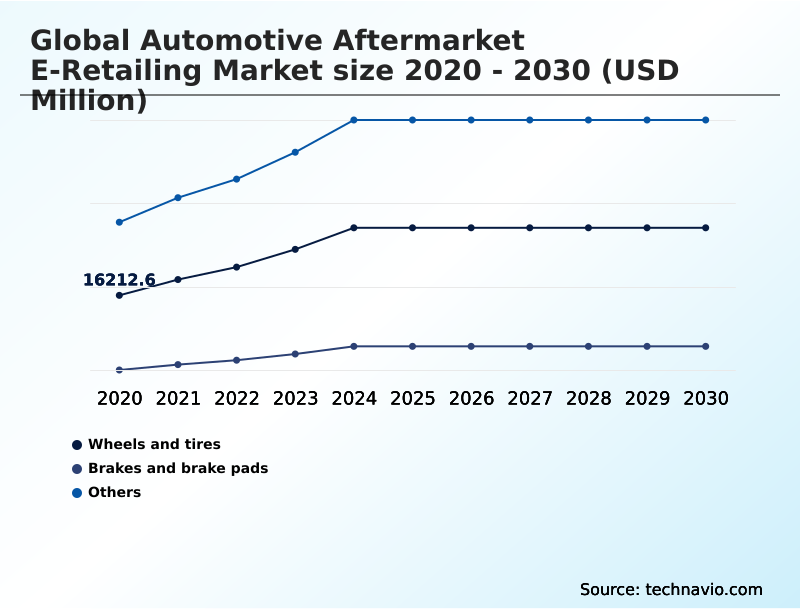

- By Product - Wheels and tires segment was valued at USD 26.21 billion in 2024

- By Customer Type - DIY customers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 138.44 billion

- Market Future Opportunities: USD 98.66 billion

- CAGR from 2025 to 2030 : 16.2%

Market Summary

- The automotive aftermarket e-retailing market is undergoing a significant transformation, driven by shifts in consumer purchasing behavior and technological advancements. The migration from traditional channels to digital platforms is fueled by demands for convenience, price transparency, and extensive selection. This digital shift empowers both the do-it-yourself consumer and professional installers, who leverage online resources for informed decision-making.

- Technology is a critical enabler, with innovations like VIN lookup tools, AI-powered diagnostic tool, and adherence to ACES and PIES standards improving part-to-vehicle compatibility and reducing transaction friction. For instance, a B2B procurement platform integrating a digital parts catalog management system allows independent garages to reduce part sourcing time by up to 40%, directly boosting technician productivity.

- However, this evolution brings challenges, including intense competition that puts pressure on margins and the logistical complexities of managing reverse logistics costs. The proliferation of the electric vehicle aftermarket introduces new component categories, requiring specialized knowledge and supply chains to meet emerging demands effectively. This dynamic environment necessitates continuous investment in technology and operational efficiency.

What will be the Size of the Automotive Aftermarket E-retailing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Aftermarket E-retailing Market Segmented?

The automotive aftermarket e-retailing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Wheels and tires

- Brakes and brake pads

- Others

- Customer type

- DIY customers

- Professional customers

- Vehicle type

- Passenger cars

- Light commercial vehicles

- Heavy commercial vehicles

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Product Insights

The wheels and tires segment is estimated to witness significant growth during the forecast period.

The wheels and tires segment constitutes a foundational, high-volume category within the automotive aftermarket e-retailing market. Growth is driven by non-discretionary replacement needs and consumer demand for vehicle personalization, which is addressed through an expansive online parts catalog.

Digital channels provide enhanced price transparency and product information, disrupting traditional purchasing funnels. A critical enabler is the ship-to-installer model, which resolves logistical challenges for consumers by delivering products directly to heavy-duty repair facilities or local garages.

Ensuring part-to-vehicle compatibility remains a key focus, as platforms using a fitment intelligence suite have demonstrated a 40% reduction in costly returns.

This focus on accurate parts compatibility check, supported by robust digital parts catalog management, is essential for maintaining customer trust and operational efficiency in online tire and wheel sales and for brake system components online.

The Wheels and tires segment was valued at USD 26.21 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Aftermarket E-retailing Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is characterized by diverse maturity levels and growth drivers. North America leads, contributing nearly 39.9% of incremental growth, supported by a mature DIY culture and sophisticated B2B e-commerce solutions.

Here, the ship-to-installer business model is well-established for both light commercial vehicles and heavy commercial vehicles. In contrast, APAC is the fastest-growing region, where a mobile-first, DIFM-centric approach prevails, fostering innovative online-to-offline business model and B2B2C segments.

Europe's fragmented market is heavily influenced by regulatory pressures like right to repair legislation, which promotes competition and transparency.

The success of online parts marketplace platforms in emerging economies is increasingly tied to providing a professional installer network, catering to a customer base that prioritizes service over DIY.

This regional variation requires adaptable strategies, from offering high-performance accessories in affluent markets to ensuring parts availability through a robust automotive aftermarket supply chain globally.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The digital transformation of automotive repair is intensifying competition and margins in online parts sales, compelling companies to refine their go-to-market strategies. A successful omnichannel strategy for auto parts retailers is now essential, blending digital convenience with physical accessibility to enhance the overall customer experience in aftermarket e-retailing.

- Central to this is the use of AI for accurate vehicle fitment, a critical tool for managing high return rates in e-retailing and ensuring data accuracy for correct part fitment. Platforms that guarantee part compatibility through advanced VIN lookup for guaranteed part compatibility report return rates up to 40% lower than competitors.

- This technological focus extends to B2B e-commerce for professional installers, with a clear trend toward integrating e-retailing with service networks to create a seamless workflow. The future of EV parts in e-retailing is a significant growth frontier, demanding specialized e-retailing for electric vehicles as the parc evolves.

- The underlying supply chain for online auto parts must adapt to handle both traditional components and new EV technologies. Furthermore, the role of marketplaces in auto e-retailing continues to expand, facilitating cross-border trade in aftermarket parts and driving the growth of private label parts online, which is increasingly influenced by mobile commerce for automotive aftermarket.

- Predictive analytics for parts demand is becoming crucial for inventory management.

What are the key market drivers leading to the rise in the adoption of Automotive Aftermarket E-retailing Industry?

- The increasing average age of vehicles and extended ownership cycles are key drivers for the market's growth.

- Market expansion is propelled by technological enablement and evolving consumer habits. The broad adoption of aftermarket parts data standards, including ACES and PIES standards, alongside robust VIN lookup tools that use the vehicle identification number, has dramatically improved order accuracy.

- E-commerce platform integration within omni-channel strategies allows traditional retailers to compete effectively in automotive digital retail, with some achieving a 20% lift in sales through unified online and in-store experiences.

- The do-it-yourself consumer is better supported than ever with extensive DIY auto repair resources. For recurring purchases, the subscription model for parts is gaining traction, increasing customer retention by up to 18%.

- This digital shift, facilitated by secure online payment gateways and the availability of remanufactured parts, makes the market more accessible and efficient for all participants.

What are the market trends shaping the Automotive Aftermarket E-retailing Industry?

- The proliferation of AI-driven fitment and vehicle personalization platforms represents a significant upcoming market trend. These technologies are set to redefine the customer experience by ensuring accuracy and tailoring product recommendations.

- Key trends are reshaping the market by enhancing precision and service integration. The deployment of an AI-powered diagnostic tool and predictive maintenance alerts is transforming reactive repairs into proactive service, with platforms reporting a 25% reduction in unplanned vehicle downtime for users.

- These AI-driven parts recommendation systems, coupled with visual search technologies, improve customer fitment guarantee and enrich the user experience. The expansion of the electric vehicle aftermarket is creating a new ecosystem for EV-specific components and specialized diagnostic tools.

- Simultaneously, the integration of do-it-for-me service networks directly into e-commerce platforms is capturing a new customer segment, boosting order values by an average of 40% when a service is bundled. The use of augmented reality applications for DIY assistance further reduces friction, empowering a wider consumer base with accessible automotive repair data.

What challenges does the Automotive Aftermarket E-retailing Industry face during its growth?

- Extreme logistical complexity and high product return rates represent a key challenge affecting the industry's growth.

- Significant operational challenges persist, primarily centered on logistics and intense competition. The complexity of the aftermarket logistics network makes supply chain optimization a continuous priority, as reverse logistics costs associated with high online auto parts return rates can erode profitability by over 15%. The necessity for rapid fulfillment drives investment in last-mile delivery solutions, yet this increases operational overhead.

- Concurrently, intense price competition, amplified by the growth of private-label parts and the ease of cross-border e-commerce, puts constant pressure on margins. The customer acquisition cost in e-commerce continues to rise, making retention critical.

- For B2B players, effective fleet maintenance procurement requires flawless execution in automotive e-commerce logistics to meet the stringent uptime demands of commercial clients, where any delay directly impacts revenue.

Exclusive Technavio Analysis on Customer Landscape

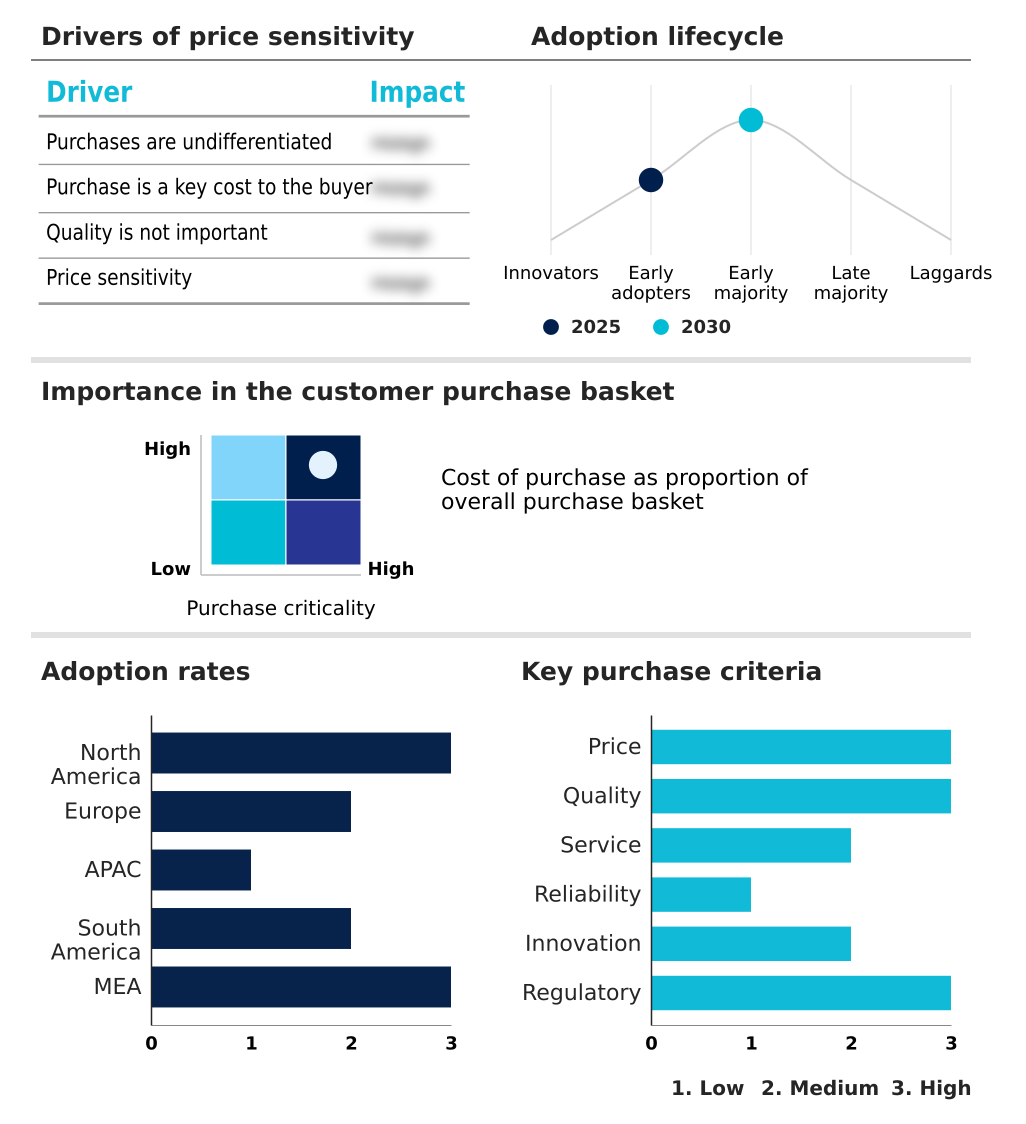

The automotive aftermarket e-retailing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive aftermarket e-retailing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Aftermarket E-retailing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive aftermarket e-retailing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

1A Auto Inc. - Delivering broad vehicle coverage through an affordable and extensive catalog of both OEM and aftermarket components.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 1A Auto Inc.

- Advance Auto Parts Inc.

- Amazon.com Inc.

- AutoZone Inc.

- Buy Auto Parts

- CarParts.com Inc.

- Delticom AG

- DENSO Corp.

- DHL International GmbH

- eBay Inc.

- Flipkart Internet Pvt. Ltd.

- General Motors Co.

- Genuine Parts Co.

- Icahn Automotive Group LLC

- ID Auto Inc.

- Keystone Automotive Inc.

- RockAuto LLC

- Sana Commerce

- Tekion Corp.

- Tire Rack

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive aftermarket e-retailing market

- In April 2025, Amazon.com expanded its automotive services by partnering with the Bosch Car Service network in Europe, enabling customers to bundle parts purchases with installation appointments.

- In August 2024, a global e-commerce marketplace integrated a new AI-powered diagnostic tool, allowing users to input vehicle symptoms to receive probable causes and a curated list of necessary replacement parts.

- In October 2024, a major international automotive data standards organization released a comprehensive update to its vehicle classification system to better accommodate electric vehicle configurations, requiring e-retailers to undertake significant data validation projects.

- In May 2025, Daimler Truck AG enhanced its Service-Connect platform with a Predictive Parts module that uses AI to anticipate component failures and automatically pre-order replacement parts to the nearest service center.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Aftermarket E-retailing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16.2% |

| Market growth 2026-2030 | USD 98658.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is driven by the sophisticated integration of digital technologies to address longstanding industry challenges. Ensuring part-to-vehicle compatibility, a primary hurdle, is now being systematically addressed by deploying VIN lookup tools and adhering to ACES and PIES standards, managed through advanced B2B e-commerce solutions.

- The rise of the electric vehicle aftermarket is compelling a strategic pivot, necessitating investment in specialized diagnostic tools and new supply chain optimization models, a decision now central to boardroom strategy. Omni-channel strategies are becoming the competitive baseline, combining digital procurement platforms with physical logistics like click-and-collect services.

- This integration allows for a 35% improvement in inventory turnover for retailers leveraging predictive maintenance alerts. The market is bifurcated, serving the do-it-yourself consumer with visual search technologies and augmented reality applications, while supporting professional heavy-duty repair facilities with tools that guarantee a parts compatibility check.

- From mobile mechanic services to the growth of remanufactured parts and private-label parts, technology is the core enabler.

What are the Key Data Covered in this Automotive Aftermarket E-retailing Market Research and Growth Report?

-

What is the expected growth of the Automotive Aftermarket E-retailing Market between 2026 and 2030?

-

USD 98.66 billion, at a CAGR of 16.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Wheels and tires, Brakes and brake pads, and Others), Customer Type (DIY customers, and Professional customers), Vehicle Type (Passenger cars, Light commercial vehicles, and Heavy commercial vehicles) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing average age of vehicles and extended ownership cycles, Extreme logistical complexity and high product return rates

-

-

Who are the major players in the Automotive Aftermarket E-retailing Market?

-

1A Auto Inc., Advance Auto Parts Inc., Amazon.com Inc., AutoZone Inc., Buy Auto Parts, CarParts.com Inc., Delticom AG, DENSO Corp., DHL International GmbH, eBay Inc., Flipkart Internet Pvt. Ltd., General Motors Co., Genuine Parts Co., Icahn Automotive Group LLC, ID Auto Inc., Keystone Automotive Inc., RockAuto LLC, Sana Commerce, Tekion Corp. and Tire Rack

-

Market Research Insights

- The market is shaped by a fundamental shift in consumer behavior toward digital channels, with over half of vehicle owners now initiating parts searches online. This digital-first approach, supported by robust automotive repair data and advanced e-commerce platform integration, caters to both DIY enthusiasts and professional installers.

- The use of a vehicle identification number for lookups has become standard, enhancing accuracy in digital parts catalog management. Innovations in AI-driven parts recommendation engines have improved order accuracy by up to 25%, significantly reducing returns. Concurrently, integrated B2B parts procurement platforms are streamlining operations for service centers, increasing technician productivity by over 15% by providing real-time inventory visibility.

- This convergence of technology and consumer expectation drives the evolution of parts and accessories e-retailing.

We can help! Our analysts can customize this automotive aftermarket e-retailing market research report to meet your requirements.

RIA -

RIA -