Automotive Chassis Market Size 2025-2029

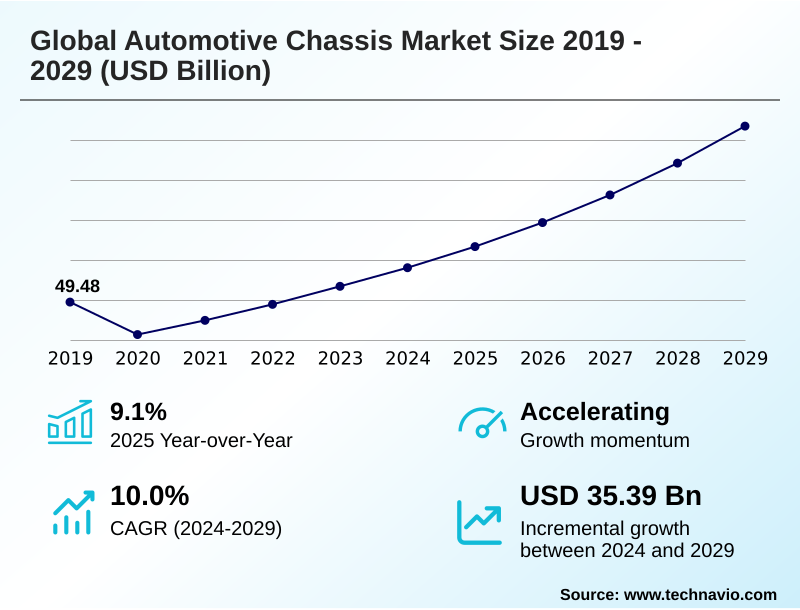

The automotive chassis market size is valued to increase by USD 35.39 billion, at a CAGR of 10% from 2024 to 2029. Increasing adoption of advanced chassis design leads to the reduced weight of vehicles will drive the automotive chassis market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 54.2% growth during the forecast period.

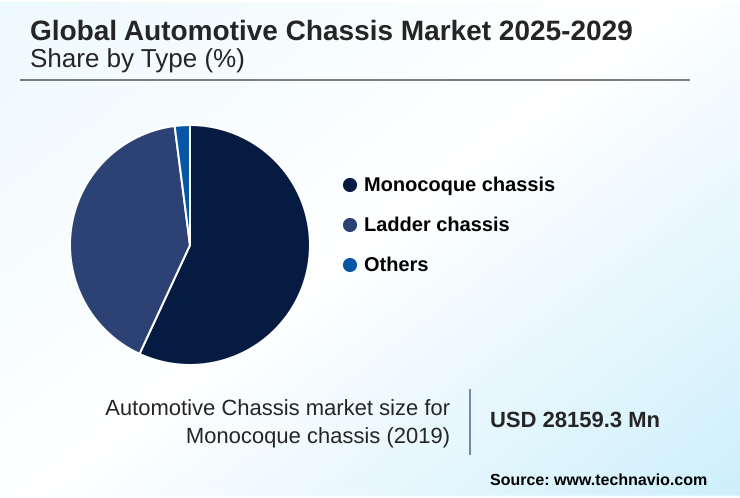

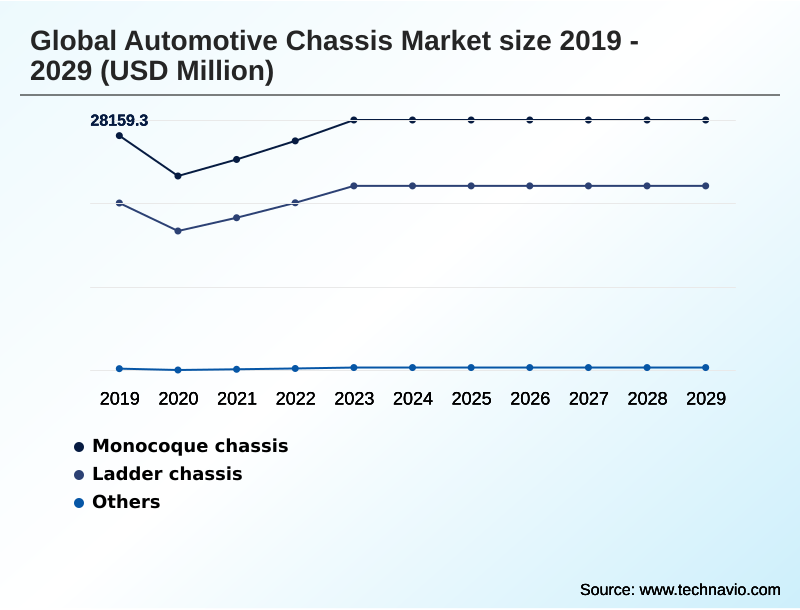

- By Type - Monocoque chassis segment was valued at USD 29.98 billion in 2023

- By Application - Passenger cars segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 43.99 billion

- Market Future Opportunities: USD 35.39 billion

- CAGR from 2024 to 2029 : 10%

Market Summary

- The automotive chassis market is undergoing a fundamental transformation, driven by the shift to electric mobility and stricter emissions regulations. The demand for vehicle lightweighting is pushing manufacturers away from traditional steel-only structures toward advanced solutions involving a backbone chassis or spaceframe chassis.

- This includes multi-material construction incorporating aluminum alloys and carbon fiber composites to improve the power-to-weight ratio without compromising torsional rigidity or crash energy absorption.

- A key business scenario involves optimizing the supply chain for these varied materials; for instance, a manufacturer must manage the logistics of sourcing advanced high-strength steel from one supplier and carbon fiber reinforced plastic from another for a single modular platform architecture.

- This complexity extends to manufacturing, where techniques like structural adhesive bonding and robotic spot welding must be adapted for different materials. The rise of skateboard chassis designs for electric vehicles further disrupts traditional body-on-frame concepts, integrating driveline components and EV battery enclosures into a single, scalable unit that redefines vehicle assembly and design possibilities.

What will be the Size of the Automotive Chassis Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Chassis Market Segmented?

The automotive chassis industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Monocoque chassis

- Ladder chassis

- Others

- Application

- Passenger cars

- Commercial vehicles

- Material

- Steel

- Aluminum

- Carbon fiber composites

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The monocoque chassis segment is estimated to witness significant growth during the forecast period.

The monocoque chassis segment is defined by its unitary construction, where the body-in-white (BIW) structure and frame are a single piece, enhancing structural integrity.

This design, formed from stamped steel panels joined by robotic spot welding, is fundamental to mass-market vehicle manufacturing. It facilitates efficient, high-volume production, with automated lines reducing assembly times by over 20% compared to traditional methods, enabling just-in-time (JIT) production.

While offering superior crash protection, the design also allows for improved ride comfort engineering.

The continuous push for efficiency is driving innovation in materials to enhance the power-to-weight ratio, although the core principles of this cost-effective manufacturing process remain dominant, impacting platform lifecycle management across the passenger car sector.

The Monocoque chassis segment was valued at USD 29.98 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 54.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Chassis Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by the APAC region, which accounts for over 54% of the market's incremental growth, driven by high vehicle adoption rates in China and India.

The region showcases a dual dynamic: high demand for traditional body-on-frame and ladder chassis designs for commercial vehicles and SUVs, alongside rapid adoption of advanced skateboard chassis for electric vehicles.

This transition to EVs in APAC is driving innovation in axle systems and the design of the EV battery enclosure.

In contrast, mature markets in Europe and North America focus on optimizing chassis system integration with features like advanced driver assistance integration and integrated braking solutions.

The strategic localization of manufacturing in APAC has enabled some OEMs to reduce supply chain costs by over 10%, highlighting the region's importance for both volume and operational efficiency.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic decisions facing automotive engineers today are increasingly complex, involving detailed analysis of monocoque versus ladder chassis for SUVs, where the trade-offs between on-road comfort and off-road ruggedness are critical. The cost-benefit of aluminum in chassis construction remains a key debate, balancing weight savings against material and fabrication expenses.

- This is particularly relevant when considering carbon fiber monocoque production challenges, which, despite offering superior performance, involve high costs and complex manufacturing cycles. The impact of skateboard chassis on EV interior design is profound, liberating space once occupied by traditional drivetrain components. This shift necessitates new joining techniques for multi-material chassis to effectively bond aluminum, steel, and composites.

- Concurrently, lightweighting strategies for commercial vehicles are being developed to improve fuel efficiency without sacrificing payload capacity, often involving advanced high-strength steel grade applications. Engineers focus on the role of subframes in noise vibration harshness reduction and enhancing torsional rigidity in performance cars.

- A primary concern is chassis design for battery protection in EVs, demanding high structural integrity of hydroformed rails. The robotic welding impact on chassis quality is a constant area of improvement. Material selection for axle systems is crucial for durability, while chassis optimization for active suspension is key for dynamic handling. Steer-by-wire implications for chassis design are reshaping front-end architecture.

- The shortened platform lifecycle impact on R&D costs, now representing over 5% more of a vehicle's total cost than a decade ago, puts pressure on development. Finally, the chassis material impact on crashworthiness and the body-on-frame vs unibody for towing debate remain central to vehicle engineering, as does optimizing power-to-weight ratio with composites for ultimate performance.

What are the key market drivers leading to the rise in the adoption of Automotive Chassis Industry?

- The increasing adoption of advanced chassis designs to achieve significant vehicle weight reduction is a primary driver of market growth.

- Key market drivers are stringent emissions regulations and the mass production efficiencies of modern chassis designs.

- The imperative for vehicle lightweighting is compelling the adoption of advanced high-strength steel (AHSS) and aluminum, which can reduce the weight of key structures like subframes and hydroformed components by up to 30% compared to conventional materials.

- Virtual simulation optimization is crucial in this process, allowing engineers to conduct fatigue life analysis digitally, accelerating development. Concurrently, the use of robotic manufacturing for monocoque designs has increased production throughput by over 20%, making advanced designs more cost-effective.

- This automation, combined with techniques like structural adhesive bonding, supports the complex mechatronic systems integration required for modern suspension modules.

What are the market trends shaping the Automotive Chassis Industry?

- The growing popularity of carbon monocoque chassis is emerging as a significant market trend. This is driven by demand for lightweight and structurally sound frames, particularly in high-performance vehicles.

- Emerging trends are centered on advanced materials and construction methods to enhance performance and efficiency. The development of multi-material chassis, which combines automotive-grade aluminum with carbon fiber composites, is gaining traction. This approach optimizes material placement, with some designs achieving a 15% increase in stiffness while simultaneously reducing weight.

- The growing popularity of carbon fiber composites, particularly in high-performance vehicles, is notable; their use in a backbone chassis or tubular frame design can reduce the chassis weight by up to 40% compared to steel.

- These innovations are coupled with the integration of electronic suspension systems featuring active damping technology, which improves vehicle dynamics control and allows for real-time adjustments to road conditions, creating a more responsive and refined driving experience.

What challenges does the Automotive Chassis Industry face during its growth?

- Rapid new product development, which consequently shortens the vehicle platform lifecycle, presents a significant challenge to industry profitability and investment planning.

- Significant market challenges stem from fluctuating raw material costs and rapid technological shifts. The price volatility of aluminum alloys, which can fluctuate by more than 10% quarterly, directly impacts the production cost of components like steering knuckles and cross-member designs. This uncertainty complicates budgeting for advanced structures like a spaceframe chassis.

- Another challenge is the shortened product development cycle, which reduces the time available for extensive component durability testing. This pressure can affect the long-term reliability of systems such as electronic stability control and brake-by-wire systems. Ensuring consistent crash energy absorption and torsional rigidity across rapidly evolving platforms requires significant R&D investment, straining profitability for many suppliers in the ecosystem.

Exclusive Technavio Analysis on Customer Landscape

The automotive chassis market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive chassis market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Chassis Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive chassis market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AISIN Corp. - Analysis indicates a focus on integrated automotive chassis technologies, encompassing electronic suspension, advanced braking controls, and driver assistance system integration for enhanced vehicle dynamics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN Corp.

- ALF Engineering Pvt. Ltd.

- American Axle and Manufacturing Inc.

- Autokiniton US Holdings Inc.

- Benteler International AG

- BWI Group

- CIE Automotive SA

- Continental AG

- DuPont de Nemours Inc.

- FEV Group GmbH

- Hyundai Motor Co.

- KLT Automotive and Tubular Products Ltd.

- Magna International Inc.

- Rausch and Pausch SE

- Schaeffler AG

- Surin Automotive P Ltd.

- Tenneco Inc.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive chassis market

- In September 2024, Agratas announced an investment of over USD 5.37 billion to construct a 40 GWh gigafactory in Somerset, aimed at supplying batteries for electric vehicle chassis manufacturing.

- In November 2024, Hyundai Motors announced a substantial investment to expand its electric vehicle range and enhance its current vehicle platforms in India, focusing on localizing chassis development.

- In January 2025, Stellantis detailed its STLA Large platform, a global, flexible BEV architecture designed to standardize modules and chassis components for upcoming full-size electric vehicles.

- In May 2025, Jetour committed USD 123 million to establish a new vehicle assembly facility in Egypt, supporting the government's strategy to localize the automotive industry and chassis production.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Chassis Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10% |

| Market growth 2025-2029 | USD 35393.0 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 9.1% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive chassis market is undergoing a significant architectural shift, moving beyond traditional stamped steel panels and body-on-frame construction. The rise of electric vehicles is popularizing the skateboard chassis, which integrates driveline components and requires new approaches to achieve high torsional rigidity and structural integrity. For boardroom consideration, the choice of materials presents a strategic dilemma.

- Continuing with advanced high-strength steel (AHSS) for subframes and hydroformed components minimizes capital expenditure on retooling. However, investing in manufacturing capabilities for aluminum alloys and carbon fiber composites is essential for future competitiveness in vehicle lightweighting and achieving a superior power-to-weight ratio.

- Carbon fiber composites, for instance, offer a stiffness-to-weight ratio that is over five times that of steel, directly enhancing performance. This decision impacts everything from suspension modules and axle systems to steering knuckles.

- Whether developing a monocoque chassis, ladder chassis, spaceframe chassis, or a specialized backbone chassis, the focus is on optimizing crash energy absorption and integrating electronic suspension systems and integrated braking solutions through advanced manufacturing like robotic spot welding.

What are the Key Data Covered in this Automotive Chassis Market Research and Growth Report?

-

What is the expected growth of the Automotive Chassis Market between 2025 and 2029?

-

USD 35.39 billion, at a CAGR of 10%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Monocoque chassis, Ladder chassis, and Others), Application (Passenger cars, and Commercial vehicles), Material (Steel, Aluminum, and Carbon fiber composites) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing adoption of advanced chassis design leads to the reduced weight of vehicles, New product development leading to a reduction in the platform lifecycle

-

-

Who are the major players in the Automotive Chassis Market?

-

AISIN Corp., ALF Engineering Pvt. Ltd., American Axle and Manufacturing Inc., Autokiniton US Holdings Inc., Benteler International AG, BWI Group, CIE Automotive SA, Continental AG, DuPont de Nemours Inc., FEV Group GmbH, Hyundai Motor Co., KLT Automotive and Tubular Products Ltd., Magna International Inc., Rausch and Pausch SE, Schaeffler AG, Surin Automotive P Ltd., Tenneco Inc. and ZF Friedrichshafen AG

-

Market Research Insights

- Market dynamics are shaped by a push for higher efficiency and performance, compelling a shift toward advanced modular platform architecture. This strategic move allows for greater flexibility, with some automakers reporting a 20% reduction in development time for new models.

- The integration of mechatronic systems is central to this evolution, enabling technologies like active damping technology and active roll control for superior vehicle dynamics control. For instance, platforms incorporating these systems have demonstrated a 15% improvement in handling metrics during component durability testing. Furthermore, steer-by-wire systems are becoming more prevalent, creating new possibilities for chassis design and interior packaging.

- These innovations reflect a market where chassis system integration is critical for delivering the safety and performance features that consumers demand.

We can help! Our analysts can customize this automotive chassis market research report to meet your requirements.

RIA -

RIA -