Automotive Drivetrain Market Size 2024-2028

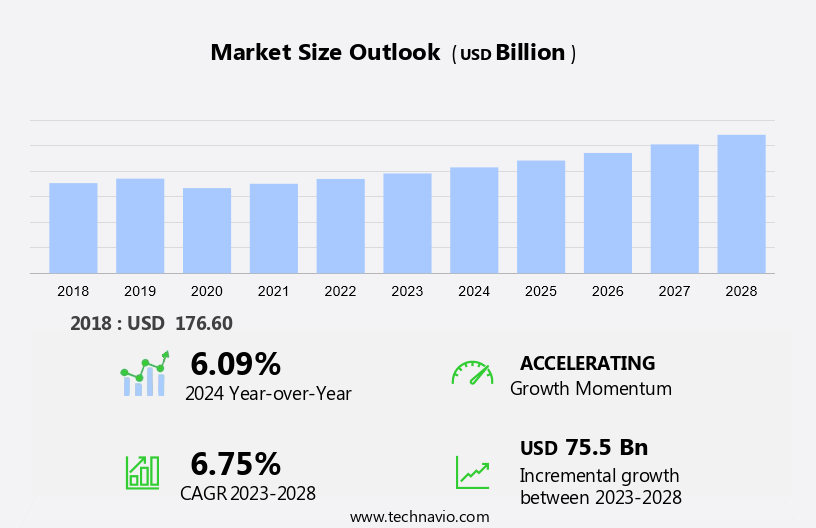

The automotive drivetrain market size is forecast to increase by USD 75.5 billion at a CAGR of 6.75% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing demand for commercial vehicles and luxury cars. With the rise of e-commerce and logistics industries, commercial vehicles are becoming increasingly essential, leading to a growth in demand for strong drivetrain systems. Similarly, the luxury vehicle segment is witnessing a resurgence, fueled by consumer preferences for comfort and performance. However, the automotive industry faces uncertainty due to various factors, including regulatory changes and evolving consumer preferences. Drive shafts, axles, CV joints, and U joints continue to be critical components of drivetrain systems, ensuring the efficient transfer of power from the engine to the wheels. These components must be able to withstand the demands of both commercial and luxury vehicles, making innovation and durability key factors In their development.

What will be the Size of the Automotive Drivetrain Market During the Forecast Period?

- The market is witnessing significant advancements in technology, particularly in electric drive systems, automated transmissions, and power distribution components. Electric vehicles (EVs) and hybrid vehicles (HEVs) are leading the charge, with their reliance on synchronous motors and advanced battery systems. In traditional automobiles, the drivetrain system comprises engine location, transmission, drive shafts, axles, CV joints, U joints, wheels, power, and torque distribution. The internal combustion engine (ICE) plays a crucial role in delivering power to the wheels via the transmission. However, the future lies in electric drive systems, where power is directly delivered to the wheels, eliminating the need for a traditional transmission. Rear-wheel drive and all-wheel drive configurations are common in both ICE and electric vehicles.

- Additionally, automated transmissions offer improved fuel efficiency and smoother shifting, while electric vehicles and hybrid vehicles leverage regenerative braking to recover energy during deceleration. The towing capacity of heavy commercial vehicles is a critical consideration in drivetrain design, necessitating strong axles and CV joints. Technology advancements in drivetrain systems include traction control systems, engine combustion control, and advanced materials for improved durability and efficiency. The market is poised for growth, driven by the increasing adoption of electric and hybrid vehicles and the continuous pursuit of improved vehicle performance and efficiency.

How is this Automotive Drivetrain Industry segmented and which is the largest segment?

The automotive drivetrain industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Forward wheel drive

- Rear wheel drive

- All wheel drive

- Vehicle Type

- Passenger car

- Commercial vehicle

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- North America

- US

- South America

- Middle East and Africa

- APAC

By Application Insights

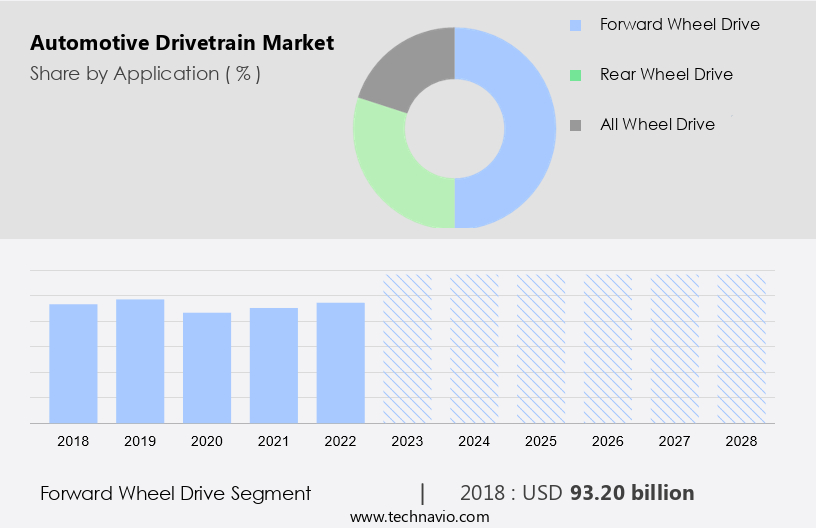

- The forward wheel drive segment is estimated to witness significant growth during the forecast period.

In the realm of automotive powertrains, forward wheel drive systems have gained significant traction due to their ability to efficiently transmit engine power to the front wheels. These systems are lighter than their counterparts, such as rear-wheel and four-wheel-drive systems, leading to improved fuel economy. The rising preference for sport utility vehicles (SUVs) and crossovers among consumers is driving the demand for forward wheel drive systems.

Moreover, many SUV manufacturers cater to the medium-size vehicle segment, equipping these vehicles with strong off-road capabilities and enhanced suspension for optimal comfort on challenging terrains. Medium-size SUVs offer unique off-road features that are not readily available in other vehicle classes. Automakers provide forward wheel drive as a standard or optional feature in SUVs and crossovers, with deployment varying among models, automakers, and geographical regions.

Get a glance at the Automotive Drivetrain Industry report of share of various segments Request Free Sample

The forward wheel drive segment was valued at USD 93.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

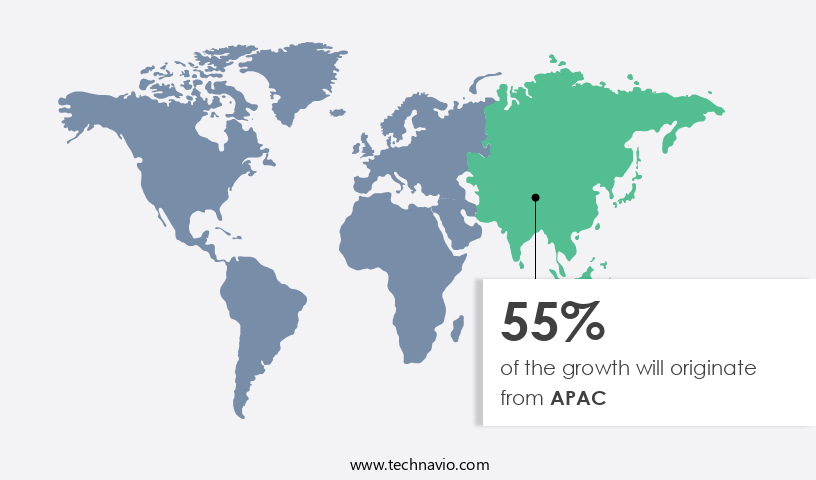

- APAC is estimated to contribute 55% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market In the Asia Pacific (APAC) region experiences significant growth due to the increasing demand for commercial vehicles in countries like China, Japan, South Korea, and India. These nations are key contributors to the market's expansion, as their economies rely heavily on manufacturing and logistics industries that require efficient land transport solutions. Moreover, developed markets such as Japan, South Korea, and Australia serve as prominent automotive export hubs in APAC. The production and sale of commercial vehicles and their associated drivetrain components are closely interconnected, with the former driving the demand for the latter. The region's automotive drivetrain industry also benefits from the increasing export-oriented production of automotive components to cater to global markets.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Automotive Drivetrain Industry?

Increase in demand for commercial vehicles is the key driver of the market.

- The market is experiencing significant growth due to the escalating demand for commercial vehicles. In developed markets like North America, the popularity and sales of medium- and heavy-duty trucks, particularly for commercial applications, are on the rise. These vehicles play a pivotal role in various industries, including logistics, construction, mining, and manufacturing.

- In the developing and emerging economies of the Asia Pacific region, the demand for commercial vehicles is increasing, fueled by improving socio-economic conditions, infrastructure development, and employment opportunities. Key components of the drivetrain system, such as drive shafts, axles, CV joints, and U joints, are essential for the smooth functioning of these vehicles. The increasing demand for commercial vehicles is expected to continue driving the growth of the market.

What are the market trends shaping the Automotive Drivetrain Industry?

Increasing demand for luxury vehicles is the upcoming market trend.

- The market is anticipated to experience significant growth due to the increasing sales of high-performance luxury vehicles. Customers' preferences are evolving towards premium, comfortable vehicles with advanced onboard features. The demand for luxury SUVs, in particular, has been on the rise for the past few years and is projected to continue during the forecast period. SUVs are designed for off-roading and require strong drivetrain systems, including drive shafts, axles, CV joints, and U joints, to ensure optimal traction and performance on various terrains.

- Moreover, the growing popularity of luxury vehicles in emerging markets, such as China and India, is driven by stable economic conditions and rising disposable incomes. These factors are expected to fuel the demand for high-performance drivetrain systems In the automotive industry.

What challenges does the Automotive Drivetrain Industry face during its growth?

Uncertainty in automotive industry is a key challenge affecting the industry growth.

- The market experienced significant challenges due to the COVID-19 pandemic, particularly In the years 2020 and early 2021. Various countries, including India and the US, implemented nationwide lockdowns to curb the spread of the virus, leading to a disruption in cross-border trade activities. This, in turn, increased the cost of raw materials and components essential for manufacturing vehicles.

- Additionally, the absence of customers in automobile showrooms due to stringent lockdown measures resulted In the halt of automobile production units worldwide. Consequently, the adverse effects of the pandemic impeded the growth of the automotive industry during this period. Drive shafts, axles, CV joints, and U joints, which are integral components of the drivetrain system, were significantly impacted by these challenges.

Exclusive Customer Landscape

The automotive drivetrain market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive drivetrain market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive drivetrain market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry. The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Axle and Manufacturing Holdings Inc.

- BorgWarner Inc.

- Continental AG

- Dana Inc.

- JTEKT Corp.

- Magna International Inc.

- Melrose Industries Plc

- Mitsubishi Corp.

- Nidec Corp.

- Robert Bosch GmbH

- Schaeffler AG

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market caters to various vehicle types, including automobiles, electric vehicles (EVs), and heavy commercial vehicles. The market is witnessing significant growth due to advancements in technology, such as electric drive systems and automated transmissions. Electric vehicles utilize synchronous motors for propulsion, while hybrid vehicles combine internal combustion engines with electric motors. Rear-wheel drive and all-wheel drive (AWD) systems are common in automobiles, with engine location varying from front to rear. Transmission systems, including drive shafts, axles, CV joints, and U joints, transfer power from the engine to the wheels.

Thus, traction and towing capacity are essential considerations for heavy commercial vehicles. Government regulations aimed at reducing carbon dioxide emissions are driving the adoption of cleaner technologies, such as electric and hybrid drivetrains. The automotive drivetrain system market is influenced by factors like combustion control systems, turbochargers, disposable income, and consumer preferences for luxury cars, SUVs, and advanced electronics. Vehicle diagnostics using scanner vehicles and continuous improvements in AWD systems are core application areas for the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.75% |

|

Market growth 2024-2028 |

USD 75.5 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

6.09 |

|

Key countries |

China, US, Japan, Germany, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Drivetrain Market Research and Growth Report?

- CAGR of the Automotive Drivetrain industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive drivetrain market growth of industry companies

We can help! Our analysts can customize this automotive drivetrain market research report to meet your requirements.

RIA -

RIA -