Automotive Engineering Services Outsourcing Market Size 2024-2028

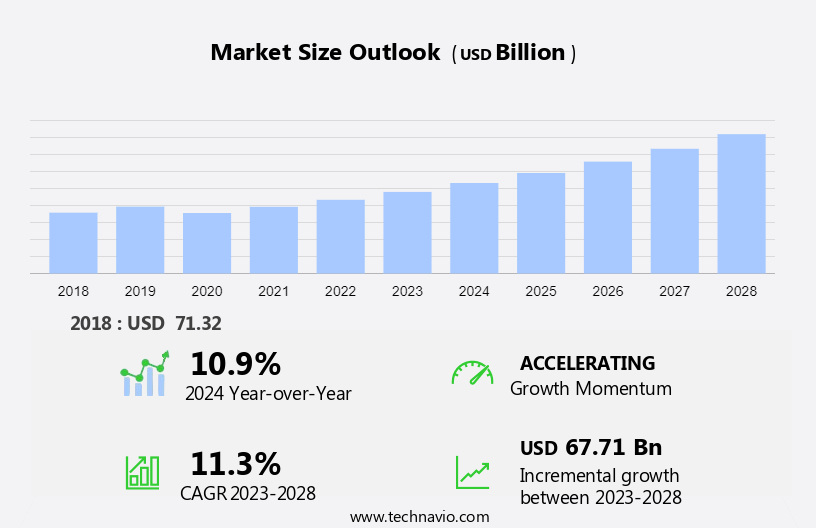

The automotive engineering services outsourcing market size is forecast to increase by USD 67.71 billion at a CAGR of 11.3% between 2023 and 2028.

- The market is witnessing significant growth due to the cost-effective solution that comes with outsourcing. Mathematical models and formulae are increasingly being outsourced to optimize design and development processes. The implementation of advanced information technology and the electrification of powertrains are key trends driving the market. However, there are challenges such as ensuring data security and privacy in the supply chain. As the industry shifts from internal combustion engines to petroleum-free alternatives like gasoline and electric vehicles, outsourcing partners must adapt to these technological advancements to remain competitive. In the aftermarket support segment, outsourcing engineering services can help automotive companies reduce costs and improve efficiency.

What will the Automotive Engineering Services Outsourcing Market Size be during the forecast period?

- The market is witnessing significant growth due to the increasing demand for advanced connectivity solutions, smart infotainment systems, and passenger safety features in automobiles. This market caters to the needs of automotive manufacturers producing various types of vehicles, including automobiles, trucks, and motorcycles. Connectivity solutions play a crucial role in enhancing the driving experience and improving vehicle efficiency. These solutions include navigation systems, remote diagnostics, and vehicle positioning. With the rise in electric vehicle sales, there is an increasing focus on virtual battery development and hydrogen fuel cell technology, leading to a higher demand for engineering services in these areas.

- Product innovation is another key driver of the market. Electrification, hybridization, methane combustion, and lightweight vehicle development are some of the major areas of focus for automotive manufacturers. Engineering subsystems, such as mechanical, electrical, electronic, software, and safety engineering, are essential to bring these innovations to life. Automotive manufacturers require engineering services to develop and integrate various systems in their vehicles. For instance, electrical engineering is essential for designing and implementing electrical systems in electric vehicles. Software engineering is necessary for developing the software that powers advanced driver assistance systems (ADAS) and infotainment systems.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Location

- Onshore

- Offshore

- Vehicle Type

- Passenger vehicle

- Commercial vehicle

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- Italy

- North America

- US

- South America

- Middle East and Africa

- APAC

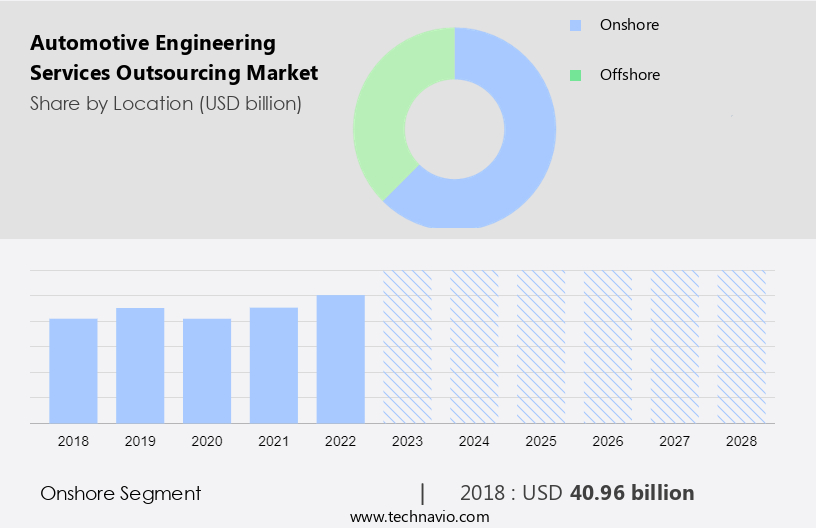

By Location Insights

- The onshore segment is estimated to witness significant growth during the forecast period.

In the realm of automotive engineering services, onshore outsourcing refers to the practice of procuring engineering solutions from local providers. This approach enables companies to leverage domestic talent without expanding their in-house teams, thereby reducing overhead costs. The automotive sector is experiencing a period of significant expansion due to the integration of advanced technologies such as connectivity solutions, navigation, smart infotainment, passenger safety, remote diagnostics, and vehicle positioning. These innovations are transforming vehicles into connected automobiles, enhancing the driving experience, and promoting the adoption of green vehicles.

Furthermore, original Equipment Manufacturers (OEMs) are responding to these trends by producing new models, making onshore outsourcing an indispensable tool for cost savings and efficient fleet management. By partnering with local engineering service providers, OEMs can remain competitive, deliver high-quality products, and cater to the evolving needs of consumers.

Get a glance at the market report of share of various segments Request Free Sample

The onshore segment was valued at USD 40.96 billion in 2018 and showed a gradual increase during the forecast period.

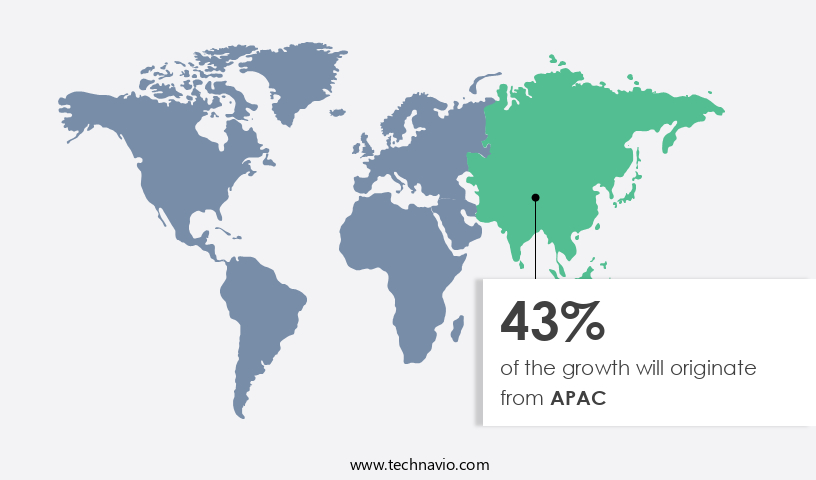

Regional Analysis

- APAC is estimated to contribute 43% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in APAC is experiencing significant growth due to the increasing demand from automotive companies in the region for improved customer service. With rising costs and the need to focus on core competencies, numerous enterprises from North America and Europe have opted to outsource their automotive engineering services to APAC. This trend is driven by several factors, including cost savings, access to local talent at competitive prices, excellent service delivery, multilingual proficiency, and strong infrastructure. The automotive industry's shift towards electrification, hydrogen, hybridization, methane combustion, and other alternative fuel sources is also fueling the demand for automotive engineering services outsourcing.

For instance, virtual battery development for electric vehicles and engineering services for heavy-duty trucks require specialized expertise and resources, which are readily available in APAC. Moreover, the aerospace engineering, naval architecture, and mechanical engineering sectors also contribute significantly to the market in APAC. The region's strong engineering capabilities and cost advantages make it an attractive destination for global enterprises seeking to outsource their engineering requirements.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Automotive Engineering Services Outsourcing Market?

Outsourcing engineering services being a cost-effective solution is the key driver of the market.

- Automotive engineering services outsourcing has become a cost-effective solution for automotive companies in the United States seeking to reduce expenses on in-house engineering. By partnering with external companies, such as Altair Engineering Inc., automotive manufacturers can eliminate the need for expensive facilities and equipment used for research projects. Outsourcing also allows companies to save on wages and training costs for research and development (R&D) engineers. Moreover, outsourcing R&D processes grants enterprises access to advanced technologies, ultimately saving on R&D costs, which can be reallocated towards operational enhancements. Electrical engineering, electronic engineering, software engineering, and safety engineering are essential engineering subsystems in the automotive industry.

- Motorcycle, automobile, and truck manufacturers rely on these engineering disciplines to design and develop vehicle customizations and manufacturing domain car parts. Outsourcing these engineering services enables enterprises to focus on their core competencies while leveraging the expertise of specialized companies. Automotive engineering services outsourcing encompasses various engineering domains, including electrical, electronic, software, and safety engineering. Motorcycle, automobile, and truck manufacturers require these engineering subsystems for vehicle customization and manufacturing car parts. By outsourcing these services, enterprises can concentrate on their core competencies while benefiting from the expertise of specialized companies. This collaboration results in cost savings, improved efficiency, and access to advanced technologies.

What are the market trends shaping the Automotive Engineering Services Outsourcing Market?

Implementation of new technologies and systems is the upcoming trend in the market.

- The global automotive engineering services market is witnessing significant growth due to increasing investments from Original Equipment Manufacturers (OEMs) in reducing carbon emissions and integrating advanced technologies such as autonomous driving/Advanced Driver-Assistance Systems (ADAS), sensors including LIDAR, GPS, Radar, and Inertial Measurement Units (IMUs). These technologies are transforming the automotive industry, with vehicles increasingly incorporating Internet of Things (IoT) devices for connectivity and voice command functionality.

- Prototyping plays a crucial role in the automotive sector, enabling companies to create replicas of finished components before implementing new technologies and systems in vehicles. Testing centers are essential for assessing the performance of these components and ensuring compliance with safety regulations. The automotive engineering services market is expected to grow substantially during the forecast period, driven by the continuous development of innovative technologies and systems.

What challenges does the Automotive Engineering Services Outsourcing Market face during its growth?

Threat to data security and privacy is a key challenge affecting the market growth.

- In the realm of automotive engineering, outsourcing has become a common practice for businesses seeking to reduce costs and focus on core competencies. However, this approach comes with its own set of challenges, particularly in the area of data security. When entrusting engineering tasks to third parties, companies grant companies access to confidential data, relinquishing control over their internal processes, policies, and IT systems. This lack of visibility increases the risk of data breaches and privacy violations, which can be costly and damaging to a company's reputation. Moreover, the digitization of the automotive industry is leading to an exponential increase in business data.

- While this data can provide valuable insights and drive innovation, it also makes companies more vulnerable to cyber threats. Mathematical models, formulae, and other sensitive information related to automotive engineering, including those concerning internal combustion engines, electrification of powertrains, and supply chain management, are prime targets for cybercriminals. To mitigate these risks, enterprises must conduct thorough due diligence on potential companies and implement strong security protocols. Information technology plays a key role in securing data, and companies must ensure that their companies have the latest security measures in place, such as encryption, firewalls, and intrusion detection systems.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adecco Group AG

- Altair Engineering Inc.

- Alten SA

- AVL List GmbH

- Belcan LLC

- Bertrandt AG

- Capgemini Service SAS

- DesignTech Systems

- EDAG Group

- FEV Group GmbH

- HCL Technologies Ltd.

- HORIBA Ltd.

- Larsen and Toubro Ltd.

- Mahindra and Mahindra Ltd.

- P3 group GmbH

- Ricardo Plc

- RLE INTERNATIONAL Group

- Samsung Electronics Co. Ltd.

- T NET Japan Co. Ltd.

- Volkswagen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The automotive engineering services outsourcing industry caters to the needs of automotive manufacturers by providing innovative engineering solutions in various domains. These services include connectivity solutions for smart infotainment and navigation systems, passenger safety, remote diagnostics, and vehicle positioning for connected automobiles. The industry leverages advanced technologies such as artificial intelligence (AI) and information technology (IT) to develop guidance systems for electric, hybrid, and lightweight vehicles. The infotainment & connectivity segment is a significant contributor to the industry's growth, with the integration of Bluetooth, cloud, edge computing, and advanced sensory information in vehicles. The engineering services cover body & chassis, prototyping, testing, designing, and manufacturing domains.

3D printing technology and mathematical models are used for vehicle customization and engineering subsystems. The outsourcing industry offers aftermarket support, IT services for the electrification of powertrains, and supply chain solutions. The on-shore and off-shore segments cater to the manufacturing domain, including car parts, motorcycles, automobiles, trucks, and engineering subsystems. The industry's focus is on energy-efficient automobiles, self-driving vehicles, and emerging technologies like hydrogen, methane combustion, and autonomous driving/ADAS. The automotive engineering services industry also serves aerospace engineering, naval architecture, and various engineering disciplines like mechanical, electrical, electronic, software, and safety engineering. The industry's growth is driven by vehicle sales, manufacturing sites, and the increasing demand for electric vehicles, vehicle customization, and vehicle sales. The industry's environmental impact is significant, with a focus on reducing carbon emissions and the development of green vehicles.

|

Automotive Engineering Services Outsourcing Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.3% |

|

Market growth 2024-2028 |

USD 67.71 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.9 |

|

Key countries |

US, China, Japan, Germany, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -