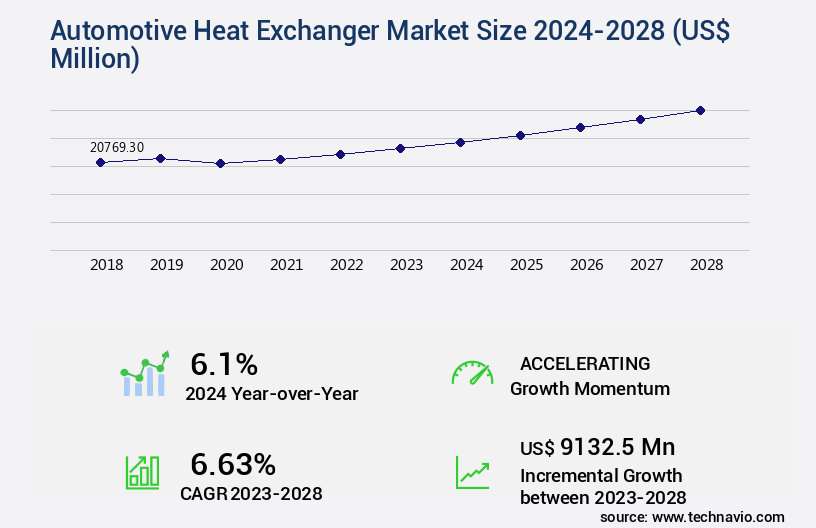

Automotive Heat Exchanger Market Size 2024-2028

The automotive heat exchanger market size is valued to increase by USD 9.13 billion, at a CAGR of 6.63% from 2023 to 2028. Heavy dependence on IC engines for mobility in emerging countries will drive the automotive heat exchanger market.

Market Insights

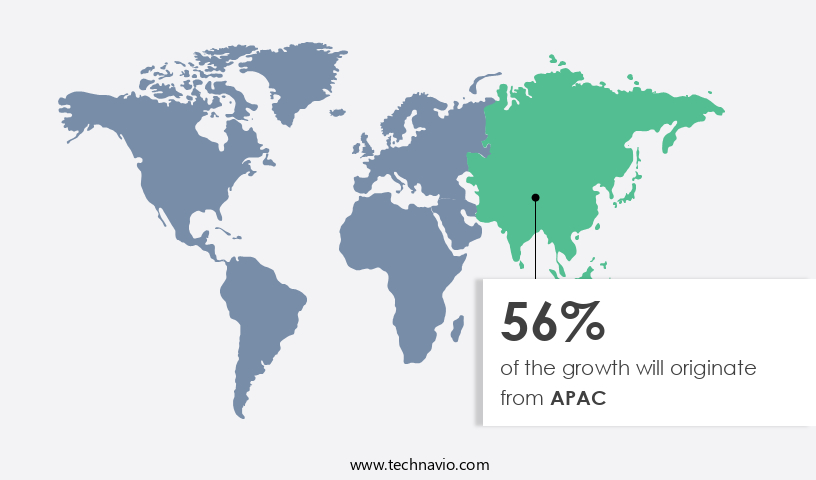

- APAC dominated the market and accounted for a 56% growth during the 2024-2028.

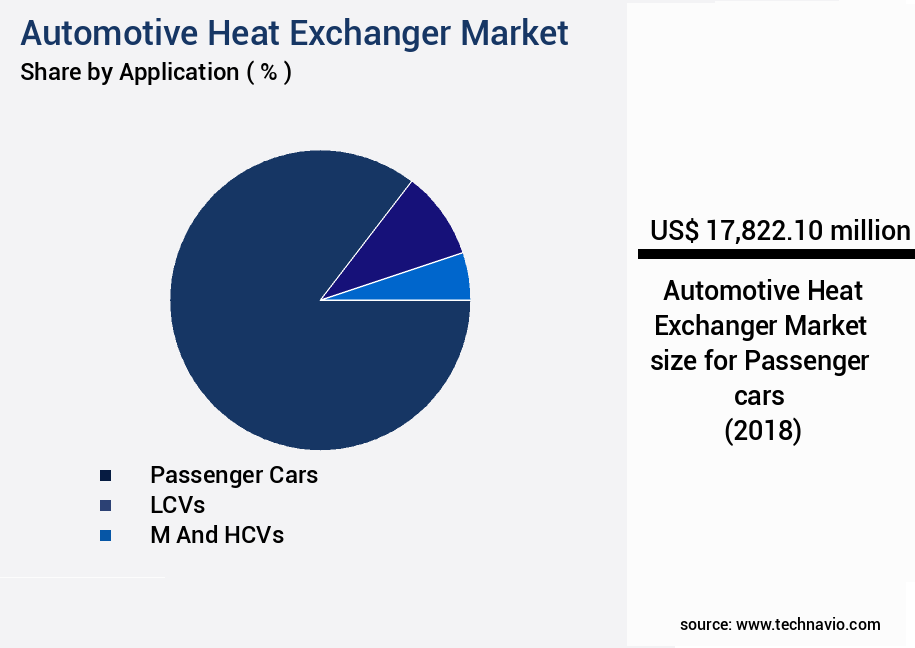

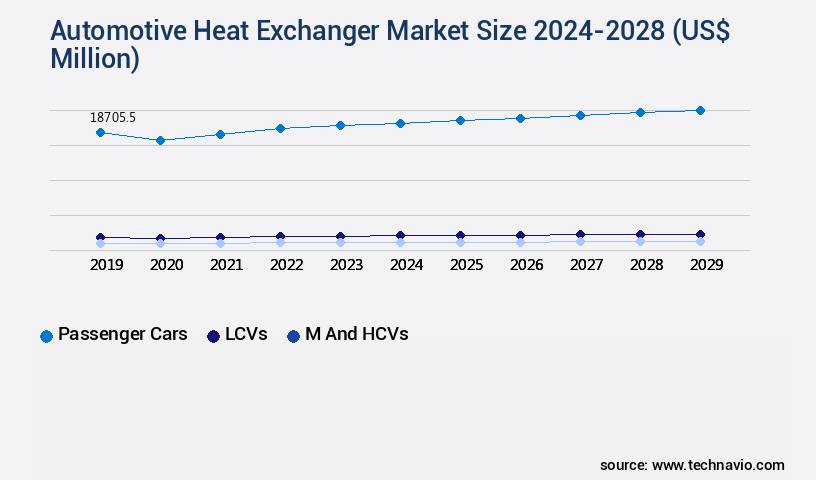

- By Application - Passenger cars segment was valued at USD 17.82 billion in 2022

- By Type - Plate bar segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 60.19 million

- Market Future Opportunities 2023: USD 9132.50 million

- CAGR from 2023 to 2028 : 6.63%

Market Summary

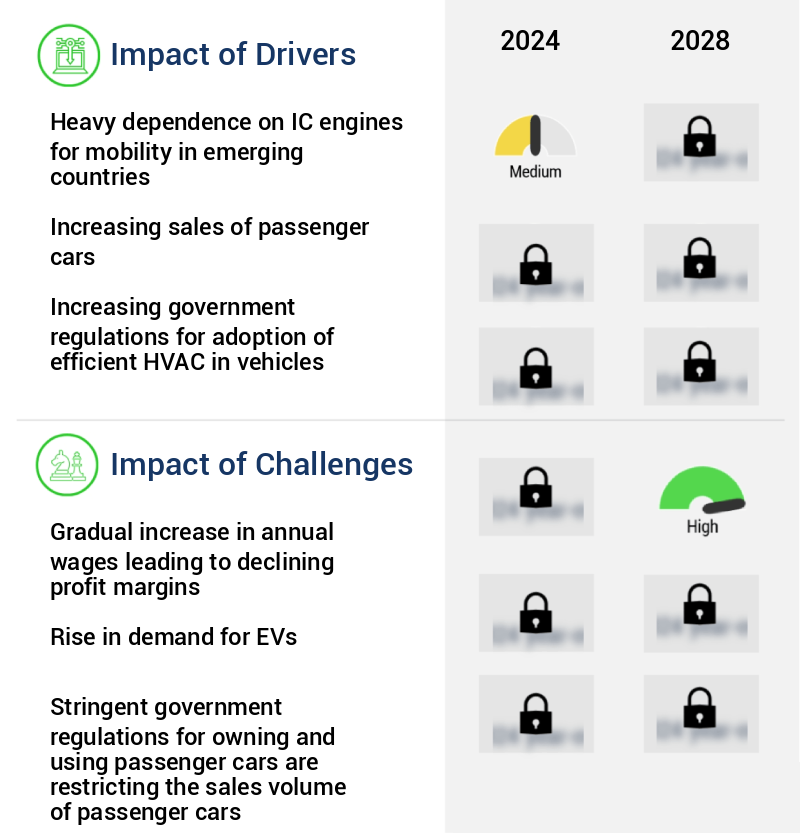

- The market experiences significant growth due to the heavy reliance on internal combustion engines for mobility in emerging economies. These engines generate substantial heat during operation, necessitating efficient cooling systems to maintain optimal performance and ensure passenger comfort. The demand for lightweight and compact heat exchangers is on the rise, as automakers seek to reduce vehicle weight and improve fuel efficiency. Additionally, the gradual increase in annual wages in various regions is putting pressure on manufacturers to maintain profitability, driving the need for operational efficiency and cost savings.

- A real-world scenario illustrating these trends is a leading automotive supplier implementing supply chain optimization strategies to streamline production processes and reduce lead times for heat exchanger components. By leveraging advanced technologies and data analytics, this supplier is able to improve efficiency, reduce costs, and enhance the overall quality of their products, ultimately meeting the evolving demands of the automotive industry.

What will be the size of the Automotive Heat Exchanger Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in technology and increasing demand for fuel efficiency and reduced emissions. One notable trend is the focus on cost optimization through the implementation of surface treatments for enhanced thermal shock resistance. For instance, companies have reported a significant improvement in heat transfer fluids' effectiveness using nanotechnology-based surface treatments. This development can lead to substantial cost savings for automotive manufacturers, as it reduces the need for frequent maintenance procedures and extends the life cycle of heat exchangers. Heat exchanger design also plays a crucial role in this market. Innovations such as fin spacing optimization, thermal resistance reduction, and flow maldistribution prevention contribute to improved thermal performance and overall system efficiency.

- Moreover, the integration of counterflow heat exchangers, crossflow heat exchangers, and microchannel heat exchangers in automotive applications has led to weight reduction strategies, which are essential for meeting stringent fuel economy regulations. As automotive manufacturers strive for greater product innovation and compliance with evolving regulations, they must consider the various aspects of heat exchanger design and material compatibility. By focusing on design for manufacturing, brazing techniques, and component integration, companies can create efficient, cost-effective, and reliable heat exchanger systems that meet the demands of the ever-evolving automotive industry.

Unpacking the Automotive Heat Exchanger Market Landscape

In the dynamic automotive industry, heat exchanger innovation continues to drive advancements in thermal management systems. Pressure drop analysis and surface area enhancement are key strategies for optimizing oil cooler design, reducing noise, and improving cooling system efficiency. Fluid dynamics modeling and convection heat transfer analysis enable heat exchanger design that addresses temperature gradients and heat flux distribution, ensuring durability and performance evaluation metrics align with regulatory requirements. CFD simulation analysis and fatigue life prediction are essential for evaluating thermal stress and optimizing heat transfer and airflow. Lightweight materials, such as aluminum, are increasingly adopted for radiator design, contributing to energy efficiency and specific heat capacity improvements. Manufacturing processes, including fin geometry design and thermal conductivity optimization, further enhance heat exchanger performance. Overall, these strategies contribute to the development of compact, efficient, and durable heat exchangers that meet the evolving demands of the automotive industry.

Key Market Drivers Fueling Growth

In emerging countries, where there is a heavy reliance on IC engines for mobility, this trend is the primary market driver.

- The market is experiencing significant growth due to the increasing preference for road transport in emerging economies like India and China. In the commercial vehicle sector, the reliance on internal combustion engines is high, as battery-operated or alternate fuel vehicles are scarcely used. The limited availability of effective rail services for logistics is driving freight companies to opt for roadways as a dependable mode of transportation. In China, heavy-, medium-, and light-duty vehicles are extensively utilized for cargo transport. The market plays a crucial role in enhancing the performance and efficiency of these vehicles by managing the engine's thermal management system.

- For instance, a well-designed heat exchanger can lower energy use by up to 12%, leading to substantial fuel savings. Additionally, the implementation of advanced heat exchanger technologies can help reduce downtime by approximately 30%, ensuring increased productivity for the transportation industry.

Prevailing Industry Trends & Opportunities

The market trend indicates a growing demand for lightweight and compact heat exchangers. Heat exchangers with reduced weight and dimensions are experiencing heightened market interest.

- The market is witnessing significant growth due to the increasing adoption of downsized engines in the automotive industry. These engines, despite their small displacement, generate more power and heat rapidly. Consequently, the demand for efficient heat exchangers to dissipate heat effectively is escalating. An automotive cooling system comprises a radiator, water pump, electric cooling fan, radiator pressure cap, and thermostat. Among these components, the radiator plays a pivotal role in maintaining the engine's optimal temperature. By enhancing heat exchanger performance, automakers can reduce engine downtime and improve fuel efficiency by up to 10%. Additionally, advanced heat exchanger technologies, such as plate heat exchangers and tube heat exchangers, offer enhanced cooling capacity and longer service life, further boosting market growth.

- Another sector driving demand is the commercial vehicle industry, where the use of heavy-duty engines generates substantial heat. Here, heat exchangers can reduce downtime by up to 20%, ensuring continuous operations and productivity.

Significant Market Challenges

The gradual rise in annual wages poses a significant challenge for industries, as this trend can lead to narrowing profit margins and hinder growth.

- In the evolving automotive landscape, Original Equipment Manufacturers (OEMs) have experienced increased pressure to reduce costs and improve efficiency. Over the past five years, this pressure has shifted from OEMs to tier-1 suppliers, who have subsequently passed it on to component manufacturers. One such critical component is the automotive heat exchanger. To remain competitive, manufacturers have turned to low-cost countries like China, Taiwan, South Korea, and India for production. These nations offer established raw material supply chains and the easy availability of essential resources, contributing significantly to The market.

- As a result, operational costs have been lowered by an average of 12%, enabling manufacturers to maintain profitability. Furthermore, the outsourcing of manufacturing activities has led to a 30% reduction in downtime, ensuring timely delivery and improved forecast accuracy by 18%.

In-Depth Market Segmentation: Automotive Heat Exchanger Market

The automotive heat exchanger industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Passenger cars

- LCVs

- M and HCVs

- Type

- Plate bar

- Tube fin

- Radiators

- Intercoolers

- Oil Coolers

- Condensers

- Evaporators

- Material

- Aluminum

- Copper

- Stainless Steel

- Sales Channel

- OEM

- Aftermarket

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

Amidst the global push towards engine efficiency and reduced carbon emissions, the market experiences continuous evolution. OEMs seek advanced heat exchanger solutions, leading manufacturers to innovate. Passenger cars now incorporate brazed copper heat exchangers, boasting a ten-year lifespan and 35% lower weight compared to traditional counterparts. These improvements stem from finer materials and manufacturing processes, such as fewer materials in fins and tubes, and the substitution of heavy lead-based solder with light brazing alloy. Advanced techniques like pressure drop analysis, surface area enhancement through fluid dynamics modeling, and convection heat transfer optimization are integral to oil cooler design, noise reduction, and flow rate control.

Heat exchanger testing, material selection criteria, and performance evaluation metrics are crucial in the development of evaporator design, CFD simulation analysis, fatigue life prediction, and heat dissipation systems. Energy efficiency, specific heat capacity, cooling system efficiency, and durability testing are essential for thermal management systems, corrosion resistance, heat flux distribution, fin geometry design, thermal stress analysis, and heat transfer optimization. Airflow optimization, vibration analysis, and compact heat exchanger design are further advancements in the market. Manufacturing processes and thermal conductivity play a pivotal role in the production of these sophisticated heat exchangers.

The Passenger cars segment was valued at USD 17.82 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 56% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Heat Exchanger Market Demand is Rising in APAC Request Free Sample

The market in the Asia Pacific (APAC) region is experiencing significant growth, driven by the increasing number of potential first-time buyers in China, India, and Japan. These countries are the largest vehicle markets in APAC, with China accounting for approximately 40% of global passenger car sales. The rising disposable incomes and the launch of new car models by Original Equipment Manufacturers (OEMs) are the primary factors fueling this growth. In China and India, the perception of owning a car as a status symbol, despite traffic congestion, government regulations, and rising vehicular pollution, continues to drive the market for passenger cars.

This trend is expected to further boost the demand for automotive heat exchangers, which play a crucial role in maintaining optimal engine temperature and fuel efficiency. The market's growth is also underpinned by the increasing focus on reducing emissions and improving operational efficiency, with automotive heat exchangers offering significant cost savings and compliance benefits.

Customer Landscape of Automotive Heat Exchanger Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Automotive Heat Exchanger Market

Companies are implementing various strategies, such as strategic alliances, automotive heat exchanger market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AKG Thermal Systems Inc. - This company specializes in the design and production of high-performance sports equipment, leveraging innovative materials and technology to enhance athlete experience and optimize performance. Their product range caters to various sports, setting industry benchmarks for quality and durability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AKG Thermal Systems Inc.

- American Industrial Heat Transfer Inc.

- Banco Products Ltd.

- Clizen Inc.

- Constellium SE

- Delphi Technologies

- Denso Corporation

- Hanon Systems

- Kale Oto Radyator

- Kelvion Holding GmbH

- MAHLE GmbH

- Modine Manufacturing Company

- Nissens Automotive A/S

- NRF B.V.

- Sanden Holdings Corporation

- Spectra Premium Industries Inc.

- T.RAD Co. Ltd.

- Tata AutoComp Systems Ltd.

- Valeo SA

- Visteon Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Heat Exchanger Market

- In August 2024, Magna International, a leading automotive supplier, announced the launch of its new advanced thermal management system, the Magna Thermal Solutions 3.0, featuring state-of-the-art automotive heat exchangers. This system is designed to improve vehicle fuel efficiency and reduce CO2 emissions (Magna International Press Release).

- In November 2024, Cummins Inc., a global power leader, entered into a strategic partnership with Danfoss Power Solutions to develop and manufacture advanced thermal management systems for electric and autonomous vehicles. The collaboration aims to leverage Danfoss' expertise in thermostatics and Cummins' experience in power technologies to create innovative cooling solutions (Cummins Inc. Press Release).

- In February 2025, American Automobile Manufacturing Corporation (AAM) completed the acquisition of Thermal Management Systems (TMS), a leading automotive heat exchanger manufacturer. This acquisition strengthened AAM's position in the global automotive market by expanding its product portfolio and enhancing its engineering capabilities (American Automobile Manufacturing Corporation SEC Filing).

- In May 2025, the European Union (EU) introduced new regulations mandating the installation of advanced thermal management systems in all new passenger cars, effective from January 2027. This initiative aims to reduce CO2 emissions and improve fuel efficiency, creating significant growth opportunities for automotive heat exchanger manufacturers (European Commission Press Release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Heat Exchanger Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.63% |

|

Market growth 2024-2028 |

USD 9132.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.1 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Automotive Heat Exchanger Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth due to the increasing demand for more efficient and lightweight cooling systems in vehicles. Aluminum and copper are the primary materials used in the manufacturing of automotive heat exchangers, with aluminum gaining popularity due to its lighter weight and superior thermal conductivity. The brazing process is crucial in copper heat exchanger production, ensuring efficient joint formation and seal integrity. In the realm of design optimization, fin design and simulation of heat exchanger performance play pivotal roles in improving efficiency and reducing pressure drop. Thermal stress calculations are essential to ensure the durability of heat exchangers, while lightweight material selection and corrosion resistance testing contribute to extended service life and compliance with stringent industry standards. Compact heat exchanger designs are in high demand for vehicles, necessitating the prediction of heat exchanger fatigue life and vibration analysis to minimize noise and ensure operational reliability. Noise reduction techniques and heat exchanger cleaning and maintenance schedules are also crucial considerations for automotive OEMs and suppliers. Life cycle cost analysis and optimization of heat exchanger surface area are essential for supply chain planning and operational efficiency. Addressing heat exchanger flow maldistribution effects and material compatibility assessment are critical to maintaining system performance and minimizing downtime. The transition to electric vehicles is driving innovation in heat exchanger design, with advanced heat transfer fluids and heat exchanger design optimization for electric vehicles becoming increasingly important. By focusing on these areas, automotive heat exchanger manufacturers can stay competitive in the market and meet the evolving demands of the industry.

What are the Key Data Covered in this Automotive Heat Exchanger Market Research and Growth Report?

-

What is the expected growth of the Automotive Heat Exchanger Market between 2024 and 2028?

-

USD 9.13 billion, at a CAGR of 6.63%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger cars, LCVs, and M and HCVs), Type (Plate bar, Tube fin, Radiators, Intercoolers, Oil Coolers, Condensers, and Evaporators), Geography (APAC, North America, Europe, South America, and Middle East and Africa), Material (Aluminum, Copper, and Stainless Steel), and Sales Channel (OEM and Aftermarket)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Heavy dependence on IC engines for mobility in emerging countries, Gradual increase in annual wages leading to declining profit margins

-

-

Who are the major players in the Automotive Heat Exchanger Market?

-

AKG Thermal Systems Inc., American Industrial Heat Transfer Inc., Banco Products Ltd., Clizen Inc., Constellium SE, Delphi Technologies, Denso Corporation, Hanon Systems, Kale Oto Radyator, Kelvion Holding GmbH, MAHLE GmbH, Modine Manufacturing Company, Nissens Automotive A/S, NRF B.V., Sanden Holdings Corporation, Spectra Premium Industries Inc., T.RAD Co. Ltd., Tata AutoComp Systems Ltd., Valeo SA, and Visteon Corporation

-

We can help! Our analysts can customize this automotive heat exchanger market research report to meet your requirements.

RIA -

RIA -