Aviation Cyber Security Market Size 2024-2028

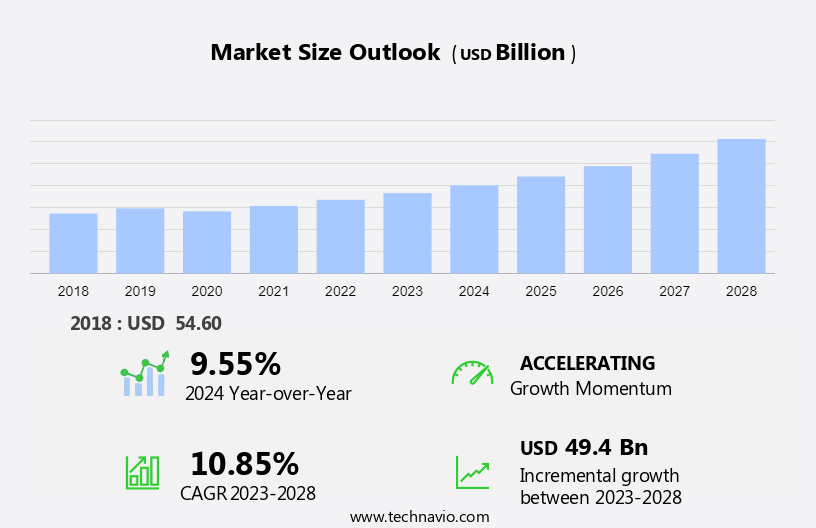

The aviation cyber security market size is forecast to increase by USD 49.4 billion at a CAGR of 10.85% between 2023 and 2028. The aviation industry's increasing reliance on technology for airline management, air cargo management, and airport management has led to a heightened focus on cyber security. Two primary models, cloud-based and on-premises, are being adopted to address this need. The hybrid model, combining both approaches, is gaining traction due to its flexibility and cost-effectiveness. Cloud-based services are increasingly popular due to their scalability and ease of implementation. However, the high cost of deploying cyber security solutions remains a challenge. Key trends in aviation cyber security include the adoption of cloud-based services, the integration of connectivity for improved customer service and flight efficiency, and the need for strong cyber security to enhance passenger experience.

The aviation industry's increasing reliance on internet-connected systems for ground and flight operations has brought about new cyber vulnerabilities. Airline companies are recognizing the importance of securing their in-flight entertainment, connectivity systems, cabin crew devices, application airline management, and customer service platforms from malicious malware activities and cyber attacks. Cyber security threats pose a significant risk to various aspects of the aviation sector. Ground operations, including check-in systems and flight ticketing, are increasingly digitized, making them susceptible to cyber intrusions. Flight operations, such as navigation and communication systems, are also at risk, which could impact flight efficiency and passenger experience.

The aviation cyber security market is growing rapidly as the industry faces increasing threats to in-flight entertainment systems, e-enabled ground systems, and flight ticketing platforms. To protect sensitive data and operations, aviation companies are investing in strong cyber security software and implementing comprehensive cyber security programs. Identity and Access Management (IAM) solutions are critical for safeguarding passenger and flight data across new airports and aviation platforms. With evolving standards and regulations, the market is also seeing increased demand for threat intelligence and response solutions to counter emerging cyber risks. As aviation infrastructure becomes more connected, the need for secure and resilient systems to protect computers, networks, and passenger information remains a top priority for the industry.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Network security

- Wireless security

- Cloud security

- Content and application security

- Deployment

- On-premise

- Cloud-based

- Geography

- North America

- US

- APAC

- China

- India

- Japan

- Europe

- Germany

- Middle East and Africa

- South America

- North America

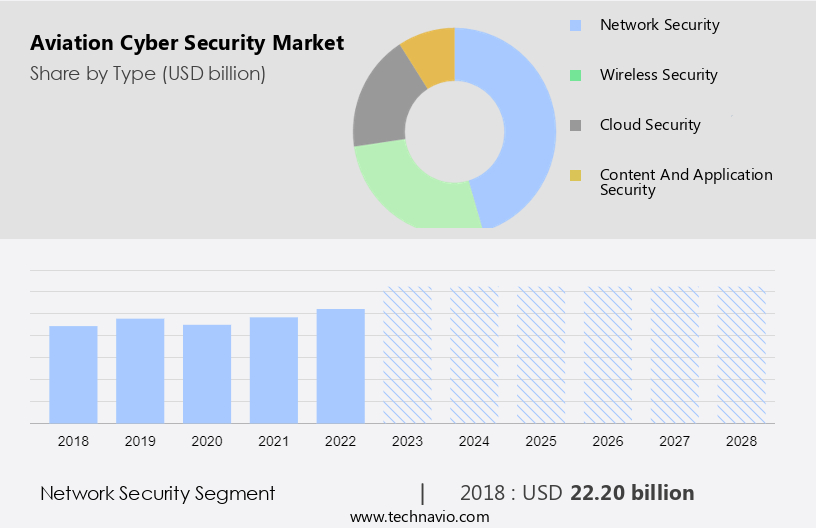

By Type Insights

The network security segment is estimated to witness significant growth during the forecast period. Network security is an essential aspect of the aviation industry, ensuring the protection of sensitive data and maintaining the usability and integrity of computer networks. With the increasing reliance on aviation technologies, such as real-time information systems for flight schedules and passenger services, the risk of data breaches becomes more significant. Air travel passengers and commercial flight airports are prime targets for cyber-attacks, which can lead to financial losses, reputational damage, and potential harm. Civil aviation authorities recognize the importance of advanced security capabilities to safeguard against these threats. Network security measures include detection systems, encryption, firewalls, and access control. Further, cybersecurity threats are a constant concern for the aviation industry, and implementing vigorous security measures is essential to mitigate these risks.

Get a glance at the market share of various segments Request Free Sample

The network security segment accounted for USD 22.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

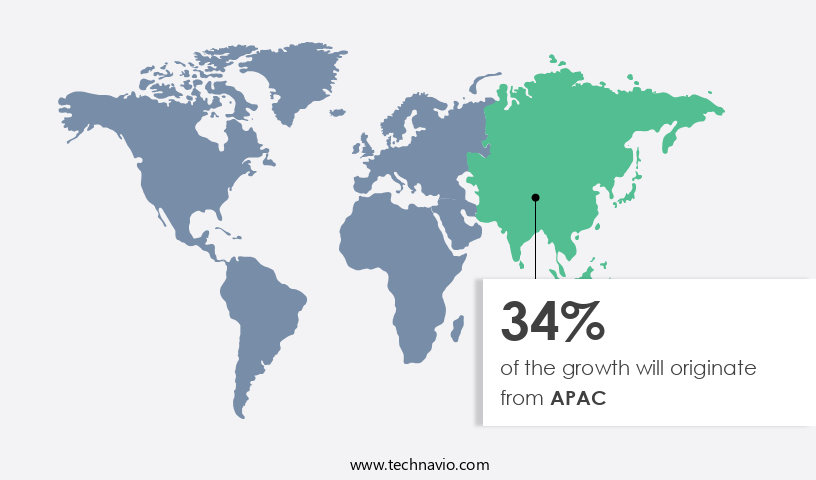

APAC is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The North American region dominates the market and is projected to maintain its leading position throughout the forecast period. The US is the primary market in North America, driven by several factors. These include the expanding use of aviation cyber security technologies such as firewalls, intrusion detection systems, and intrusion prevention systems to safeguard network users and critical infrastructure from cyber threats. Additionally, the shift towards advanced biometric technologies like identity recognition through facial recognition systems for secure biometric computer applications is gaining momentum. The growing number of suspected criminals and jaywalkers, along with increased government initiatives and the presence of numerous IT companies and startups, further fuel the market growth in North America.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The adoption of hybrid model in the aviation industry is the key driver of the market. The aviation industry's reliance on internet-connected systems for ground and flight operations has increased cyber vulnerabilities. Airline companies must secure in-flight entertainment, connectivity systems, cabin crew devices, onboard systems, electronic flight bags, and cargo handling. Traditional deployment models for aviation cyber security solutions were on-premises and cloud-based. While on-premises models offered more control, they required significant investment. Cloud-based models were cost-effective but lacked customization. To address these concerns, hybrid deployment models have emerged. These models offer the benefits of both on-premises and cloud-based solutions. Hybrid cyber security solutions follow a pay-per-use model, making them less expensive than full-license security solutions.

They provide ease of installation and upgradation, which is essential for small businesses with limited IT resources. Hybrid deployment models enable organizations to protect on-premises data without the need for a large IT team. This results in a lower total cost of ownership. The advantages of hybrid cyber security solutions are particularly crucial in the aviation industry, where the consequences of a cyber attack can be catastrophic. Therefore, hybrid deployment models are an effective solution for securing aviation industry's critical systems.

Market Trends

The adoption of cloud-based services in aviation cyber security is the upcoming trend in the market. In the aviation industry, the adoption of cloud-based technology has become increasingly crucial for managing various operations, including airline management, air cargo management, and airport management. Cloud solutions enable data storage and access via the internet, allowing real-time information sharing among relevant personnel. This technology enhances operational efficiency by modernizing and updating security systems.

Applications of cloud-based services in aviation cyber security include authentication, video management systems, and biometric information storage. Given the sensitive nature of data involved, it is essential to secure cloud-based data from cyber attacks and malicious malware activities. The implementation of advanced security measures, such as encryption and multi-factor authentication, is vital to safeguarding data in the cloud. Overall, cloud-based technology plays a significant role in improving connectivity, customer service, and flight efficiency while providing a better passenger experience in the aviation sector.

Market Challenge

The high cost of deployment of cyber security in aviation is a key challenge affecting the market growth. The aviation industry's reliance on legacy systems and increasing passenger traffic creates a significant risk for cyberattacks, threatening the safety and security of aircraft infrastructure. Cyber regulatory frameworks are essential to mitigate these risks, and technological solutions, such as threat intelligence, response identity, access management, data loss prevention, and managed security services, are crucial for effective cybersecurity.

However, the high cost of implementing these solutions is a major challenge. This includes expenses for software licensing, system design and customization, implementation, training, and ongoing maintenance. Hiring IT staff for proper implementation and training, as well as maintaining in-house IT administration for on-premises solutions, further increases costs.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Airbus SE - The company offers Airbus cyber security which protects the government, defense, critical infrastructure, and enterprise from increasingly complex cyber threats.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Astronautics Corp. of America

- BAE Systems Plc

- Booz Allen Hamilton Holding Corp.

- Cisco Systems Inc.

- Fortinet Inc.

- General Dynamics Corp.

- General Electric Co.

- Honeywell International Inc.

- International Business Machines Corp.

- Israel Aerospace Industries Ltd.

- L3Harris Technologies Inc.

- Lockheed Martin Corp.

- Northrop Grumman Corp.

- Palo Alto Networks Inc.

- RTX Corp.

- SITA

- Thales Group

- Unisys Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The aviation industry's increasing reliance on internet-connected systems for ground and flight operations has led to heightened cyber vulnerabilities. Airline companies utilize connectivity systems for in-flight entertainment, cabin crew devices, onboard systems, electronic flight bags, and cargo handling. These systems, including legacy systems and data links, are susceptible to cyberattacks, posing risks to sensitive security data and passenger information. Cybercrime targeting the aviation sector has been on the rise, with malicious malware activities leading to data breaches. Aviation technologies, such as real-time information systems for flight schedules and passenger services, are essential for air travelers and airports. However, they also present advanced security challenges.

Further, civil aviation authorities and governing authorities have implemented cyber regulatory frameworks, threat intelligence, response identity, access management, data loss prevention, managed security, and cyber security standards to mitigate risks. Cloud-based and on-premises cyber security solutions are employed to protect airline management, air cargo management, airport management, application airline management, and connectivity. The global airline industry, including airline service providers, airline bookings, aircraft manufacturers, and aircraft components, faces cyber threats from the finance sector, telecommunications sector, energy sector, and transport sector. Biometric technology, such as facial recognition systems, is employed to enhance cyber safety and identity recognition for suspected criminals and jaywalkers. Firewalls, intrusion detection systems, and intrusion prevention systems are crucial components of cyber security programs to safeguard aviation infrastructure.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.85% |

|

Market Growth 2024-2028 |

USD 49.4 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.55 |

|

Regional analysis |

North America, APAC, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 34% |

|

Key countries |

US, China, Germany, Japan, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Airbus SE, Astronautics Corp. of America, BAE Systems Plc, Booz Allen Hamilton Holding Corp., Cisco Systems Inc., Fortinet Inc., General Dynamics Corp., General Electric Co., Honeywell International Inc., International Business Machines Corp., Israel Aerospace Industries Ltd., L3Harris Technologies Inc., Lockheed Martin Corp., Northrop Grumman Corp., Palo Alto Networks Inc., RTX Corp., SITA, Thales Group, and Unisys Corp. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -