Europe Cancer Therapies Market Size and Trends

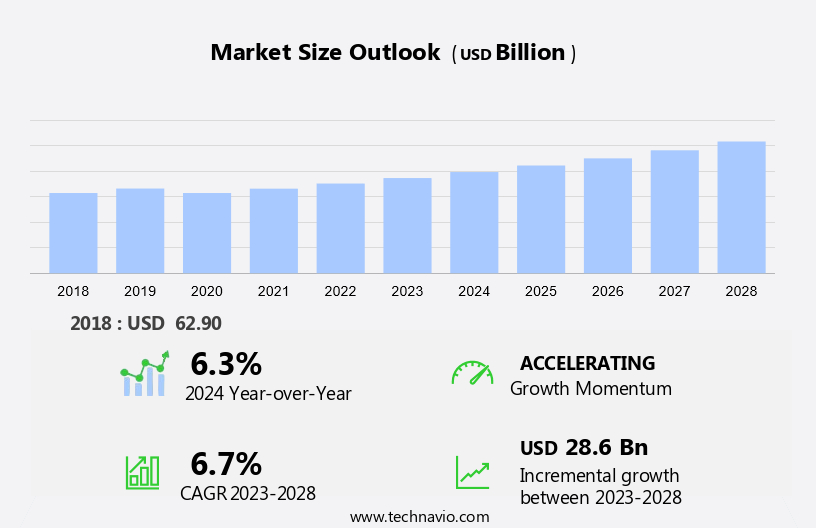

The Europe cancer therapies market size is forecast to increase by USD 28.6 billion, at a CAGR of 6.7% between 2023 and 2028. The market is experiencing significant growth due to the increasing number of new cancer cases and cancer deaths, particularly in the geriatric population. Early diagnosis through advanced screening protocols and public health campaigns is a key driver for this market. The rise in research and development investment in cancer therapeutics is also contributing to market growth. However, the high cost of cancer treatments remains a challenge for both patients and healthcare systems. Breast cancer is a major focus area for cancer research and treatment, accounting for a significant portion of new cases and deaths. The market is expected to continue growing as new therapies and treatments are developed to address the unmet needs of cancer patients

The market encompasses a significant segment of the healthcare industry, catering to the growing number of cancer cases and the demand for advanced treatment options. According to the American Cancer Society, an estimated 1.9 million new cancer cases are projected to be diagnosed in the United States in 2021. This number underscores the immense potential for growth in the cancer therapeutics market. Diagnostic techniques play a crucial role in the early detection and treatment of cancer. The advancements in diagnostic tools, such as imaging technologies and molecular tests, have led to earlier diagnosis and more effective treatment plans. Early detection is essential, as it increases the chances of successful treatment and reduces the overall cost of care. The pharmaceutical industry is at the forefront of developing new cancer therapeutics. These advanced treatments, including targeted drugs, are designed to specifically address the unique characteristics of various cancer types. This targeted approach reduces the side effects associated with conventional treatments, such as chemotherapy, and improves patient outcomes.

The geriatric population is a growing demographic within the cancer patient population. As the population ages, the prevalence of cancer is expected to increase. Therefore, the development of cancer therapeutics that cater to the unique needs of older adults is a critical area of focus. The healthcare landscape is evolving, with the integration of telehealth and virtual medicine in cancer care. Oncologists are increasingly utilizing telehealth platforms to provide consultations, monitor patients, and manage their care remotely. This trend is particularly important in the context of the ongoing COVID-19 pandemic, which has necessitated the adoption of remote care solutions to minimize in-person interactions and maintain social distancing. The cancer therapeutics market is driven by the increasing number of newly diagnosed cancer cases and the growing demand for advanced treatment options. The market is expected to witness steady growth in the coming years, as new therapeutics are developed and approved for use. Drug development is a complex and lengthy process, involving extensive research, clinical trials, and regulatory approval. However, the potential rewards are significant, as new cancer therapeutics can offer improved patient outcomes and increased quality of life.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Type

- Chemotherapy

- Targeted therapy

- Immunotherapy

- Others

- Geography

- Europe

- Germany

- UK

- France

- Italy

- Europe

By Type Insights

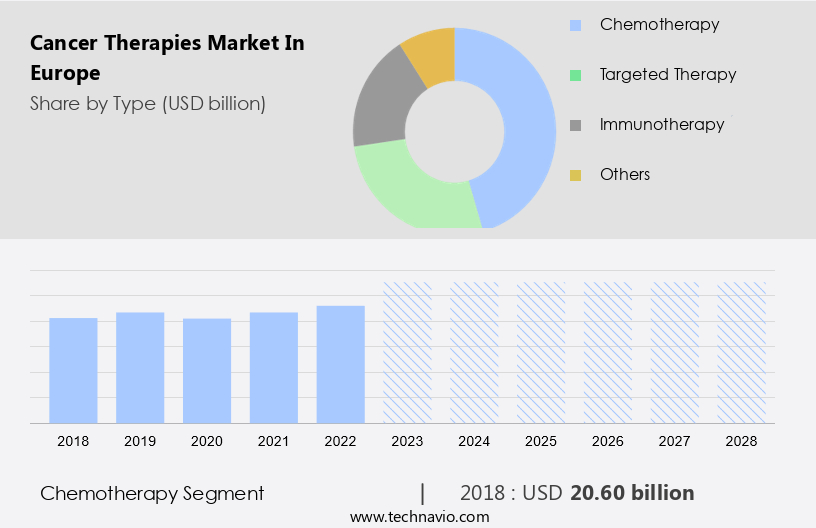

The chemotherapy segment is estimated to witness significant growth during the forecast period. Chemotherapy is the use of drugs to destroy cancer cells or to stop the growth of rapidly dividing cancer cells in the body. A chemotherapy regimen usually consists of a specific number of cycles that can be given over a set period. During a chemotherapy schedule, patients with cancer may receive a single therapeutic drug at a time or a combination of different therapeutics at the same time.

Get a glance at the market share of various segment Download the PDF Sample

The chemotherapy segment was valued at USD 20.60 billion in 2018. Chemotherapy is often given along with radiation therapy, called chemoradiation therapy, to increase the effectiveness of radiation therapy. Hence, the use of chemotherapy is expected to drive the growth of the segment during the forecast period. However, even a small dose of chemotherapy drugs can cause life-threatening side effects. Hence, physicians are inclined toward targeted therapy and immunotherapy. Dose-related side effects and long-term use of chemotherapy drugs for the treatment of cancer are expected to hamper the growth of the chemotherapy segment during the forecast period. Moreover, the market approvals of chemotherapy-based therapeutics for the treatment of cancer are expected to drive the growth of the segment further during the forecast period.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Europe Cancer Therapies Market Driver

The increased prevalence of cancer is notably driving market growth. In the US, unhealthy lifestyle choices and environmental factors contribute significantly to the development of various types of cancer, including those affecting the lungs, stomach, kidneys, head, neck, and larynx. Exposure to radiation, chemicals, infectious agents, and pollutants are also known cancer risk factors. According to Cancer Research in the US, an estimated 1.8 million new cancer cases are diagnosed annually. The National Cancer Institute reports that the total cost of cancer care in the country reached approximately USD 88.3 billion in 2020. With an aging population and increased cancer diagnoses, healthcare expenditures on cancer treatment are expected to rise.

New, expensive therapies, such as targeted drugs, are increasingly being adopted as standard treatments. Diagnostic techniques for early detection are also a focus for healthcare providers and specialty clinics, as well as cancer research centers, to improve patient outcomes and reduce costs. Thus, such factors are driving the growth of the market during the forecast period.

Europe Cancer Therapies Market Trends

The rise in research and development investment is the key trend in the market. In the realm of healthcare, the fight against breast cancer continues to be a top priority for researchers and pharmaceutical companies. The importance of early diagnosis and effective treatment cannot be overstated, making the cancer therapeutics market a significant area of investment. Public health campaigns and screening protocols play a crucial role in increasing awareness and ensuring timely detection of new cancer cases among the population. Surgical therapies remain a mainstay in cancer treatment, but innovative approaches such as nanoparticle-based cancer theranostics are gaining traction. These advanced therapies involve the use of gold nanoparticles to combine a therapeutic and diagnostic agent.

This dual functionality allows for effective monitoring of target tumors and a better understanding of the impact of cancer drugs. The geriatric population, a demographic with a higher prevalence of cancer cases and deaths, stands to benefit greatly from these new theranostic combined therapeutics. As these innovative treatments become available, the demand for cancer diagnostic devices is expected to rise, contributing to the growth of the cancer therapeutics market. Investment in research and development is essential to bring these novel therapies to market and improve patient outcomes. By focusing on early diagnosis and effective treatment, we can make a significant impact on the number of cancer cases and deaths. Thus, such trends will shape the growth of the market during the forecast period.

Europe Cancer Therapies Market Challenge

The high cost of products is the major challenge that affects the growth of the market, with ongoing research focusing on various types of cancer, including platinum-resistant ovarian cancer and lung cancer. However, the high cost of cancer treatment remains a significant challenge for patients, particularly those in the lower income bracket. This financial barrier often results in patients forgoing treatment or delaying diagnosis. Drug approval regulations and the associated costs contribute to the high price of cancer therapies. These costs are further compounded by the need for drug safety measures and the development of new and innovative therapies, such as target therapy, immunotherapy, and radiotherapy, which address genetic defects specific to certain types of cancer. Lung Cancer Awareness initiatives aim to increase public awareness and early detection, but the high cost of cancer therapies remains a major concern.

For instance, the recent approval of Retevmo (selpercatinib) for the treatment of certain types of lung cancer comes with a hefty price tag. To mitigate these costs, it is essential to prioritize patient access to affordable cancer therapies. This can be achieved through government subsidies, insurance coverage, and collaborations between pharmaceutical companies and healthcare providers to offer discounts and payment plans. In conclusion, the market in Europe is continually evolving, with ongoing research and innovation in various cancer treatments. However, the high cost of cancer therapies remains a significant challenge, particularly for patients in the lower income bracket. Addressing this issue requires a multi-faceted approach, including government subsidies, insurance coverage, and collaborations between stakeholders to ensure patient access to affordable and effective cancer therapies. Hence, the above factors will impede the growth of the market during the forecast period.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Amgen Inc. - The company offers Imdelltra (tarlatamab), which received FDA approval for the treatment of advanced small-cell lung cancer

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Apotex Inc.

- AstraZeneca Plc

- Bayer AG

- Bristol Myers Squibb Co.

- Cipla Inc.

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- Fresenius Kabi AG

- GlaxoSmithKline Plc

- Lupin Ltd.

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- Sanofi SA

- Sun Pharmaceutical Industries Ltd.

- Takeda Pharmaceutical Co. Ltd.

- Viatris Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market is witnessing significant growth due to the increasing prevalence of cancer and the development of advanced therapies. Cancer treatment has evolved from conventional methods like chemotherapy and radiation therapy to targeted drugs and immunotherapy. Diagnostic techniques for early detection have also played a crucial role in improving patient outcomes. Targeted drugs are designed to attack specific genetic defects, such as those related to the BCR-ABL protein kinase or RAS gene mutation. Companies are focusing on developing new therapies for platinum-resistant ovarian cancer and other types of advanced cancers.

Drug approval regulations and safety concerns are key considerations in the development process. Lung cancer, breast cancer, and multiple myeloma are some of the most common types of cancer. Pharmaceutical companies are investing heavily in drug development, clinical trials, and specific therapeutics for newly diagnosed patients. Telehealth and virtual medicine are also gaining popularity in delivering high-quality cancer care to the geriatric population. Cancer cases and deaths continue to rise, making it essential to increase public awareness and screening protocols through healthcare campaigns. Combination therapy, immunomodulatory drugs, and breakthrough therapies are some of the new trends in cancer therapeutics.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

146 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.7% |

|

Market Growth 2024-2028 |

USD 28.6 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.3 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AbbVie Inc., Amgen Inc., Apotex Inc., AstraZeneca Plc, Bayer AG, Bristol Myers Squibb Co., Cipla Inc., Eli Lilly and Co., F. Hoffmann La Roche Ltd., Fresenius Kabi AG, GlaxoSmithKline Plc, Lupin Ltd., Merck and Co. Inc., Novartis AG, Pfizer Inc., Sanofi SA, Sun Pharmaceutical Industries Ltd., Takeda Pharmaceutical Co. Ltd., and Viatris Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for market forecast period. |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -