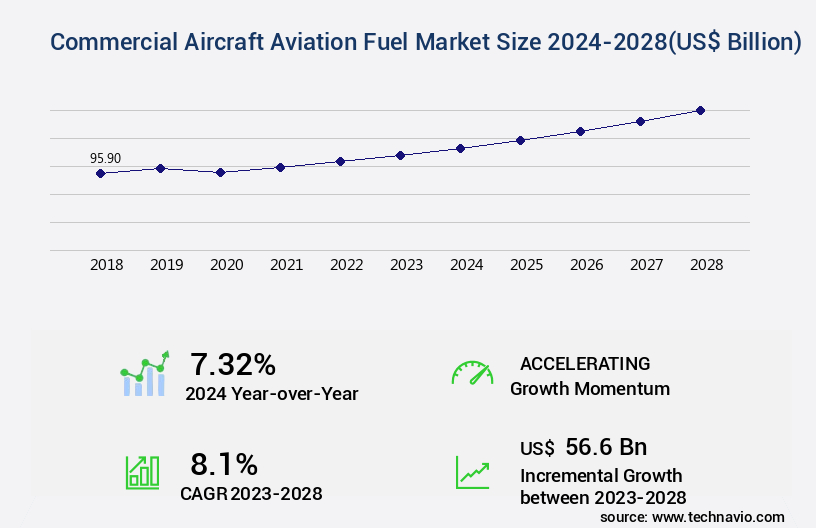

Commercial Aircraft Aviation Fuel Market Size 2024-2028

The commercial aircraft aviation fuel market size is forecast to increase by USD 56.6 billion, at a CAGR of 8.1% between 2023 and 2028.

- The market is a dynamic and ever-evolving sector that plays a crucial role in powering the global air travel industry. This market is influenced by several key factors, including the increasing demand for air travel and the ongoing pursuit of operational efficiency among airlines. One significant trend in the market is the fluctuation of oil and gas prices, which directly impact the cost of aviation fuel. These price changes can lead to increased or decreased fuel expenses for airlines, affecting their overall profitability. Despite these challenges, the market continues to grow, driven by the constant expansion of air travel and the need for reliable fuel solutions.

- In fact, according to recent industry reports, the demand for commercial aircraft aviation fuel has grown by approximately 23.3% over the past decade. Airlines are continually seeking ways to optimize their fuel consumption and reduce costs, leading to advancements in fuel efficiency and the adoption of alternative fuel sources. These efforts are essential as fuel represents a significant portion of an airline's operating expenses. The market's dynamics are influenced by various factors, including technological advancements, regulatory requirements, and geopolitical events. Understanding these trends and staying informed about market developments is crucial for businesses operating in the aviation industry or those looking to invest in it.

- In conclusion, the market is a vital component of the global air travel sector, subject to various influences and trends. Its ongoing evolution underscores the importance of staying informed and adaptable to ensure continued success in this dynamic industry.

Major Market Trends & Insights

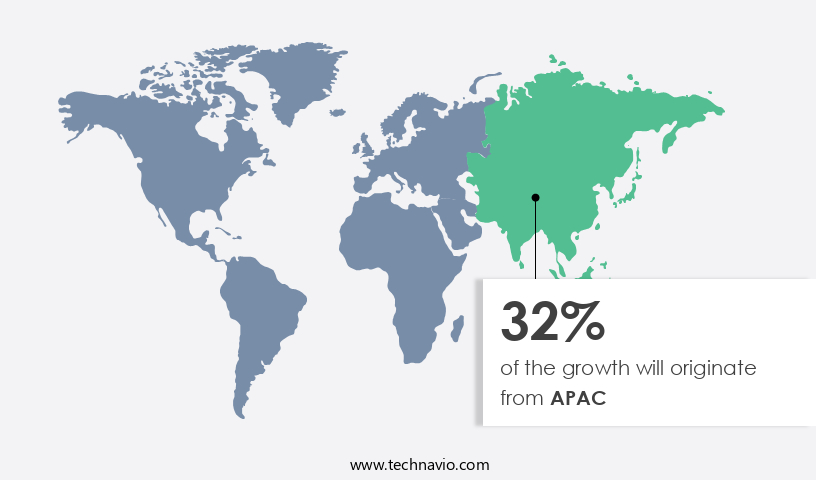

- APAC dominated the market and accounted for a 32% growth during the forecast period.

- The market is expected to grow significantly in North America as well over the forecast period.

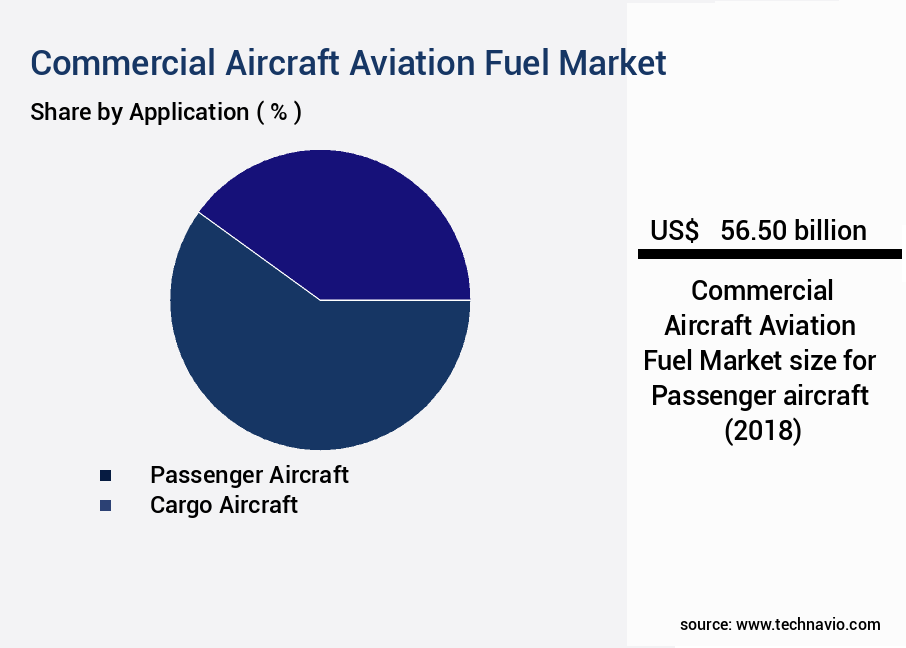

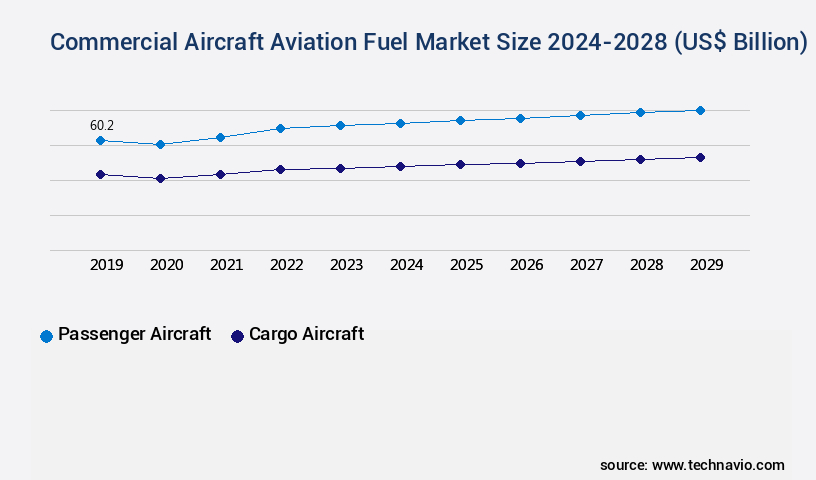

- By the Application, the Passenger aircraft sub-segment was valued at USD 56.50 billion in 2022

- By the Type, the Air turbine fuel (ATF) sub-segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: US $83.00billion

- Future Opportunities: US $56.6billion

- CAGR : 8.1%

- APAC: Largest market in 2022

What will be the Size of the Commercial Aircraft Aviation Fuel Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The commercial aircraft aviation fuel market plays a critical role in powering global air transportation, with demand driven by increasing air passenger traffic, expansion of international routes, and a growing focus on fuel-efficient aviation solutions. Aviation fuel, primarily Jet A and Jet A-1, remains the dominant energy source for commercial aircraft operations worldwide. Market dynamics are strongly influenced by crude oil price fluctuations, carbon emission regulations, and the adoption of sustainable aviation fuel (SAF) to meet greenhouse gas reduction goals.

- As airlines work to reduce operational costs and improve fleet efficiency, alternative fuels such as bio-based jet fuel, synthetic aviation fuel, and blended SAF options are gaining momentum. Regulatory frameworks, such as CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation) and ICAO sustainability targets, are accelerating investments in low-emission fuel technologies and renewable fuel production capacity.

- Market growth is further supported by aircraft modernization initiatives, engine technology advancements, and partnerships between fuel producers, airline operators, and airports for fuel supply chain optimization. Key players such as ExxonMobil, Shell Aviation, BP, Chevron, and TotalEnergies dominate the market, focusing on strategic alliances for SAF adoption and carbon footprint reduction strategies.

- Regionally, North America and Europe lead in sustainable aviation fuel adoption, while Asia-Pacific (APAC) emerges as a major growth hub, driven by expanding fleets, low-cost carriers, and rising air travel demand. Meanwhile, Middle East carriers remain key consumers due to large long-haul operations and hub-based networks. The market is projected to grow steadily, supported by aviation decarbonization initiatives, airline fleet renewals, and fuel efficiency improvements.

How is this Commercial Aircraft Aviation Fuel Industry segmented?

The commercial aircraft aviation fuel industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Passenger aircraft

- Cargo aircraft

- Type

- Air turbine fuel (ATF)

- Aviation biofuel

- Others

- Product Type

- Jet A

- Jet A-1

- Jet B

- Others

- Distribution Channel

- Direct Sales

- Fuel Distributors

- Airports

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Russia

- UK

- Middle East and Africa

- South Africa

- UAE

- APAC

- China

- India

- Japan

- South Korea

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The passenger aircraft segment is estimated to witness significant growth during the forecast period.

The market is driven by the significant demand from the passenger aircraft segment. This segment holds a substantial position due to the continuous fuel requirements of large commercial airlines. The aviation industry has experienced a surge in passenger traffic, leading to a rise in demand for commercial aircraft. According to recent industry estimates, domestic passenger traffic for FY2023 is projected at 1360 million, slightly higher than the Indian aviation industry's predictions of 1300-1350 million. Furthermore, the overall airline capacity deployment for FY2023 increased by 38% compared to FY2022. Domestic air passenger traffic for March 2023 has shown an 8% growth compared to February 2023.

Aviation fuel efficiency is a critical focus area, with ongoing efforts to improve aerodynamic designs, fuel system integration, and turbofan engine efficiency. Fuel quality control, fuel storage management, and fuel pipeline infrastructure are essential components of the aviation fuel market. The industry is also exploring alternative fuel sources such as hydrogen fuel cells, aviation fuel blends, and synthetic jet fuel. Fuel contamination prevention, thermal energy storage, and CO2 emissions reduction are essential considerations for the aviation industry. Engine maintenance schedules, fuel tank design, and aircraft engine performance are other crucial factors. Fuel consumption reduction is a continuous priority, with initiatives like fuel handling procedures, fuel cell technology, and turboprop engine efficiency.

The market for sustainable aviation fuel, flight planning optimization, fuel delivery systems, and jet fuel additives is evolving rapidly. Greenhouse gas emissions and alternative jet fuels are significant areas of focus for the aviation industry. Fuel combustion optimization and the use of bio-based jet fuel are essential strategies to reduce carbon emissions. In conclusion, the market is a dynamic and evolving industry, with a focus on improving fuel efficiency, reducing emissions, and exploring alternative fuel sources. The passenger aircraft segment remains a significant contributor, with ongoing demand driving market growth. The industry is continuously innovating to meet the demands of the aviation sector and reduce its environmental impact.

The Passenger aircraft segment was valued at USD 56.50 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 32% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Commercial Aircraft Aviation Fuel Market Demand is Rising in APAC Request Free Sample

The market in North America is experiencing steady growth, fueled by the substantial investments in the aviation sector. With a well-established aviation industry, particularly in the United States, the demand for efficient aircraft systems has increased significantly. This trend is driven by the global surge in demand for new aircraft. For instance, in 2021, Deutsche Lufthansa AG, a leading aviation company, announced its plans to purchase five long-haul aircraft each from Airbus SE and The Boeing Company. This market expansion is not limited to North America alone. The market is expected to grow at a substantial pace due to the increasing number of aircraft orders and deliveries.

According to recent industry reports, the global commercial aircraft fleet is projected to grow at a steady rate, leading to a corresponding increase in fuel demand. This growth is expected to continue, with the market reaching a significant size by 2026. Comparatively, the Asia Pacific region is expected to witness the fastest growth in the market due to the increasing number of low-cost carriers and the expanding middle class population. This trend is expected to continue as more people travel for business and leisure purposes. In conclusion, the market is experiencing steady growth due to the increasing demand for new aircraft and the expanding aviation industry.

This trend is expected to continue, with the market reaching significant size by 2026. The Asia Pacific region is expected to witness the fastest growth in this market due to the increasing number of low-cost carriers and the expanding middle class population.

Economic dynamics remain highly influential, as fuel price volatility often fluctuating by 8% to 15% annually is shaped by geopolitical fuel dynamics and global demand patterns. To mitigate risks, airlines are focusing on fuel cost optimization strategies while ensuring compliance with aviation fuel certification requirements. Ongoing developments in engine thermal management, exhaust gas analysis, and renewable jet fuel sources underscore the industry's commitment to achieving both efficiency and sustainability.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global aviation fuel market continues to evolve as airlines and manufacturers adopt strategies for reducing carbon footprint of aviation and improving operational efficiency. A critical factor influencing engine performance is the impact of fuel additives on engine performance, as advanced formulations enhance combustion stability and reduce deposits. With growing sustainability initiatives, sustainable aviation fuel production methods and innovative solutions for sustainable aviation fuel are gaining traction, supported by a life cycle analysis of bio-based jet fuel to evaluate environmental benefits over conventional fuels. The optimization of jet fuel combustion efficiency has become central to reducing costs, while advanced engine technologies for fuel consumption reduction deliver efficiency improvements of 10% to 15% compared to legacy systems.

Market players are increasingly focused on regulatory compliance for alternative jet fuels, ensuring compatibility with global standards. Hydrogen fuel cell integration in aircraft and challenges in developing hydrogen-powered aircraft highlight the industry's shift toward zero-emission solutions, although these technologies currently cost 30% to 50% more than conventional systems. Additionally, aircraft design for fuel efficiency improvements and fuel management systems for improved aircraft operations aim to optimize performance and minimize fuel burn.

Economic factors affecting aviation fuel prices remain volatile, with fluctuations of 8% to 12% annually driven by crude oil trends and supply constraints. Technological advancements in aviation fuel storage and global aviation fuel distribution infrastructure enhance resilience in the supply chain. Safety considerations related to alternative aviation fuels and comparison of different renewable jet fuel options are critical in adoption decisions. Overall, the integration of new fuel additives for enhanced combustion and continued investment in next-generation fuels underpin the transition toward sustainable aviation solutions.

What are the key market drivers leading to the rise in the adoption of Commercial Aircraft Aviation Fuel Industry?

- The primary factor fueling market growth is the rising demand for air travel. The market is a significant contributor to the global energy sector, experiencing continuous growth driven by the expanding air travel industry and the need for compliance with aviation fuel regulations. The increasing affluence of the middle classes in emerging economies is fueling the demand for commercial aviation, leading to greater emphasis on fuel testing methods and fuel storage stability to maintain safety and performance standards. Fuel infrastructure investment is also increasing to support a robust fuel distribution network and ensure fuel security concerns are addressed across the aviation ecosystem.

- The yearly expansion of air traffic necessitates the induction of new aircraft to cater to the growing demand, which directly impacts aircraft fuel burn and the demand for advanced fuel efficiency metrics. According to data, the global commercial aircraft fleet is projected to grow at a substantial rate, with an estimated 10,000 new aircraft deliveries expected between 2020 and 2040. In comparison, the current global commercial aircraft fleet stands at approximately 23,000 aircraft, with continued investment in fuel injector design and combustion chamber design to optimize thermal management and reduce emissions. Geopolitical fuel dynamics and fuel price volatility, which can fluctuate by 8% to 15% annually, further shape strategic decisions across the industry.

- The market is witnessing a shift toward renewable jet fuel sources and sustainable fuel production methods, including hydrogen storage systems and innovative fuel cell power output technologies. Regulatory frameworks such as emissions trading schemes and aviation fuel certification drive the adoption of sustainable practices. Additionally, advancements in aircraft performance monitoring, flight data analytics, and fuel cost optimization are improving operational efficiency. Engine thermal management, exhaust gas analysis, and life cycle assessment remain critical for reducing carbon footprints, while emerging trends in fuel infrastructure and supply chain resilience highlight the market's evolving nature.

- The market is poised for continued growth, driven by technological advancements in engine design, circular efficiency initiatives, and innovative solutions for renewable jet fuels. With ongoing development in fuel management systems and compliance with international standards, the aviation fuel sector continues to adapt to new challenges and opportunities shaping the future of global air travel.

What are the market trends shaping the Commercial Aircraft Aviation Fuel Industry?

- The increasing efficiency of airlines is a current market trend. This is achieved through various means, including technological advancements and operational improvements.

- The market is a critical sector that plays a significant role in the global aviation industry. Fuel efficiency has emerged as a top priority due to increasing passenger numbers and cargo weight per flight. This trend has led to a decrease in energy consumption per useful service delivered. One factor contributing to this improvement is better aircraft utilization. Another significant driver of efficiency gains is fleet renewal. To meet the global climate goals, aviation energy efficiency needs to improve by more than 3% per year by 2040. Several countries, such as India and China, have set targets for domestic aviation efficiency improvements under various frameworks, including the Paris Agreement.

- The International Civil Aviation Organization (ICAO) has implemented policies to enhance aircraft efficiency and limit CO2 emissions from international flights. Comparatively, the demand for jet fuel in the commercial aircraft sector has been growing steadily. According to recent data, the global jet fuel consumption in the commercial aviation sector was approximately 323 billion gallons in 2020. This figure represents a notable increase from the 288 billion gallons consumed in 2015. Despite the growth, the sector's fuel efficiency has improved, with the average fuel consumption per available seat mile (ASM) decreasing by approximately 1.5% annually between 2015 and 2020.

- In conclusion, the market is undergoing continuous evolution, driven by factors such as increasing passenger numbers, cargo weight, and fleet renewal. These trends are leading to improved fuel efficiency and contributing to the sector's overall growth. Policymakers and industry stakeholders are taking steps to further enhance efficiency and reduce emissions, ensuring the sector remains sustainable and aligned with global climate goals.

What challenges does the Commercial Aircraft Aviation Fuel Industry face during its growth?

- The volatile nature of oil and gas prices poses a significant challenge to the industry's growth trajectory.

- The market is a significant component of the global energy sector, with fuel accounting for a substantial portion of an airline's operating costs. The market's dynamics are closely tied to the price of crude oil, which has experienced considerable volatility in recent years. From July 2014 to the present, crude oil prices have seen a prolonged period of decline due to a persistent supply-demand imbalance. During this time, the price of crude oil dropped from around USD110 per barrel (bbl) in June 2014 to a low of USD35/bbl by January 2020. However, the market experienced a reversal, with the price of crude oil increasing to USD71 in 2021 and further rising to USD115 in 2022.

- The declining crude oil prices significantly impacted the revenues of upstream oil and gas companies. The decrease in revenues led to a reduction in their cash flow, which, in turn, affected the market. The lower revenues forced airlines to reconsider their fuel purchasing strategies and explore alternative fuel options. Despite the challenges, the market continues to evolve, with ongoing research and development efforts focused on improving fuel efficiency and reducing emissions. Some of the key trends in the market include the increasing adoption of biofuels, the development of sustainable aviation fuels, and the implementation of fuel efficiency technologies.

- In terms of numerical data, the global commercial aircraft aviation fuel consumption was estimated to be around 318.5 billion gallons in 2021. However, the market is expected to face challenges due to the ongoing volatility in crude oil prices and the increasing focus on reducing carbon emissions. Despite these challenges, the market is projected to grow steadily, driven by the increasing demand for air travel and the ongoing efforts to improve fuel efficiency and reduce emissions. In conclusion, the market is a critical component of the global energy management sector, with its dynamics closely tied to the price of crude oil.

- The market has experienced significant challenges in recent years due to the prolonged period of low crude oil prices. However, it continues to evolve, with ongoing research and development efforts focused on improving fuel efficiency and reducing emissions. The market is projected to grow steadily, driven by the increasing demand for air travel and the ongoing efforts to address the challenges posed by volatile crude oil prices and carbon emissions.

Exclusive Customer Landscape

The commercial aircraft aviation fuel market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the commercial aircraft aviation fuel market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Commercial Aircraft Aviation Fuel Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, commercial aircraft aviation fuel market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abu Dhabi National Oil Co. - This subsidiary of the company specializes in providing commercial aviation fuel services at Shanghai Pudong International Airport. The company's Shanghai Pudong International Airport Aviation Fuel Supply Company Ltd. Ensures efficient and reliable fuel supply for aircraft operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abu Dhabi National Oil Co.

- Bharat Petroleum Corp. Ltd.

- BP Plc

- Chevron Corp.

- Essar

- Exxon Mobil Corp.

- Indian Oil Corp. Ltd.

- Kuwait Petroleum International Ltd.

- Marathon Petroleum Corp.

- Neste Corp.

- PJSC LUKOIL

- PT Pertamina Persero

- Reliance Industries Ltd.

- Rosneft Deutschland GmbH

- Shell plc

- TotalEnergies SE

- Valero Energy Corp.

- Vitol Netherlands Cooperatief UA

- Viva Energy Group Ltd.

- World Kinect Corp

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Commercial Aircraft Aviation Fuel Market

- In January 2024, Boeing and Airbus, the two leading commercial aircraft manufacturers, announced significant investments in sustainable aviation fuel (SAF) production. Boeing committed USD100 million to LanzaTech to expand its gas fermentation technology, while Airbus pledged €200 million to Carbon Clean Solutions for its scalable carbon capture technology (Boeing Press Release, 2024; Airbus Press Release, 2024).

- In March 2024, Shell and Gevo, Inc. Entered into a strategic partnership to produce SAF from renewable feedstocks. The collaboration aimed to produce at least 10 million gallons of SAF per year by 2026 (Shell Press Release, 2024).

- In April 2025, the European Union (EU) approved the Sustainable Aviation Fuel (SAF) uplift mechanism under the European Emissions Trading System (ETS). The mechanism incentivizes airlines to use SAF by granting them additional emission allowances (European Commission Press Release, 2025).

- In May 2025, JetBlue and United Airlines signed a memorandum of understanding (MOU) with AltAir Fuels to purchase 1 billion gallons of SAF over 10 years. This deal represented the largest SAF purchase agreement to date (JetBlue Press Release, 2025; United Airlines Press Release, 2025).

Research Analyst Overview

- The market is a dynamic and evolving sector that continues to adapt to advancements in technology and industry demands. Aviation fuel plays a crucial role in powering the global aviation industry, with fuel consumption projected to grow at a rate of 3.5% annually over the next decade. Aerodynamic improvements and fuel system integration are key areas of focus in the market, as aircraft manufacturers and operators seek to optimize fuel efficiency and reduce greenhouse gas emissions. For instance, the adoption of turbofan engines, which are more fuel-efficient than older turboprop engines, has led to significant fuel savings for airlines.

- Fuel quality control and management are also critical aspects of the aviation fuel market. Fuel storage management, fuel pipeline infrastructure, and fuel handling procedures are essential to ensure the delivery of high-quality fuel to aircraft. Hydrogen fuel cells and synthetic jet fuels are emerging alternatives that offer potential for significant fuel consumption reduction and CO2 emissions reduction. Fuel contamination prevention is another area of concern, with fuel tank design and fuel tanker operations playing a crucial role in maintaining fuel quality and ensuring safe transportation. Engine maintenance schedules and fuel delivery systems are also essential components of the aviation fuel market, as they impact aircraft engine performance and fuel consumption.

- The market is further driven by the development and adoption of alternative jet fuels, such as bio-based jet fuel and sustainable aviation fuel. Thermal energy storage and flight planning optimization are also areas of interest, as they offer potential for reducing fuel consumption and optimizing aircraft operations. Fuel combustion optimization and jet fuel additives are other areas of focus, as they can improve engine efficiency and reduce emissions. Hydrogen fuel cells and fuel cell technology are also gaining attention as potential solutions for the future of aviation fuel. In conclusion, the market is a complex and dynamic sector that is continuously evolving to meet the demands of the global aviation industry.

- From fuel efficiency and emissions reduction to fuel quality control and alternative fuel sources, innovation and advancements are driving the market forward.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Commercial Aircraft Aviation Fuel Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.1% |

|

Market growth 2024-2028 |

USD 56.6 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.32 |

|

Key countries |

Brazil, South Africa, UAE, US, Canada, Germany, UK, China, France, Italy, Japan, India, South Korea, Argentina, and Russia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Commercial Aircraft Aviation Fuel Market Research and Growth Report?

- CAGR of the Commercial Aircraft Aviation Fuel industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the commercial aircraft aviation fuel market growth of industry companies

We can help! Our analysts can customize this commercial aircraft aviation fuel market research report to meet your requirements.

RIA -

RIA -