Direct Carrier Billing Market Size 2025-2029

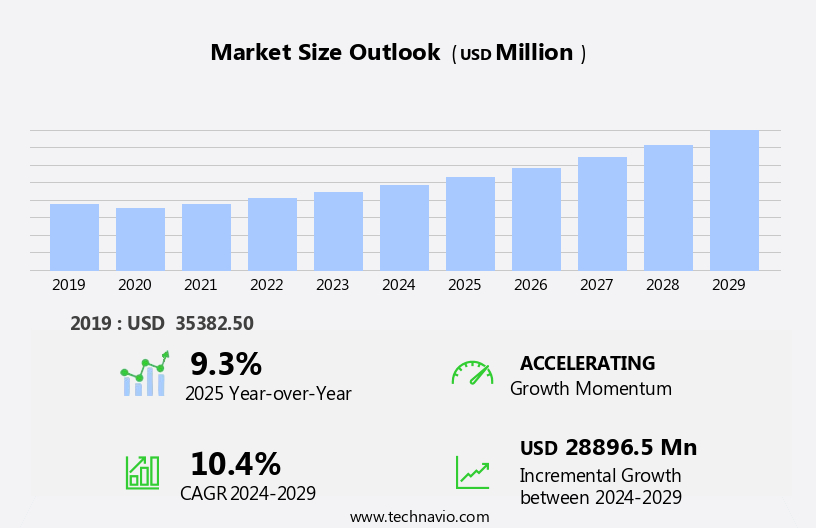

The direct carrier billing market size is forecast to increase by USD 28.9 billion at a CAGR of 10.4% between 2024 and 2029.

- The market is experiencing significant growth due to the increasing consumer demand for digital content. This trend is driven by the convenience and ease of use offered by carrier billing, allowing customers to charge mobile transactions directly to their phone bills. Furthermore, the popularity of cryptocurrencies is adding momentum to the market, as some carriers have started to accept digital currencies as payment methods for carrier billing. However, the market faces intense competition from alternative payment technologies, such as mobile wallets and online payment platforms.

- Companies must navigate these challenges by focusing on enhancing their security measures, offering competitive pricing, and providing seamless user experiences to attract and retain customers. By capitalizing on these opportunities and addressing the competition, market players can effectively position themselves in the evolving digital payment landscape. With the rise in smartphone usage and mobile internet penetration, DCB has emerged as a convenient and secure payment method for digital goods and services.

What will be the Size of the Direct Carrier Billing Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market is witnessing significant activity and trends as businesses seek alternative payment methods to credit card processing. In this dynamic landscape, payment gateway selection and integration with e-wallets, debit cards, and cryptocurrencies are crucial for multi-currency support and global expansion. Premium services, such as content monetization, affiliate marketing, and loyalty programs, are driving revenue growth. However, security risks, including data breaches and fraud, necessitate advanced technology innovation, such as AI-powered fraud detection and blockchain technology. Operating costs, scalability issues, and integration challenges persist, requiring strategic partnerships and compliance with regulatory standards.

Predictive analytics, discount codes, and promotional offers help businesses optimize revenue and customer onboarding. Meanwhile, international payments, chargeback management, and dispute resolution demand efficient solutions to minimize maintenance costs and maintain privacy protection. Risk management and regulatory compliance are essential for cross-border transactions, ensuring a seamless customer experience. Additionally, the popularity of cryptocurrencies has introduced new opportunities for DCB, as carriers explore partnerships with blockchain platforms to offer cryptocurrency billing.

How is this Direct Carrier Billing Industry segmented?

The direct carrier billing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Platform

- Android

- Web-based platforms

- iOS

- Type

- Pure DCB

- OTP-based DCB

- PIN-based DCB

- Limited DCB

- Hybrid DCB

- End-user

- Apps and games

- Online media

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Spain

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Platform Insights

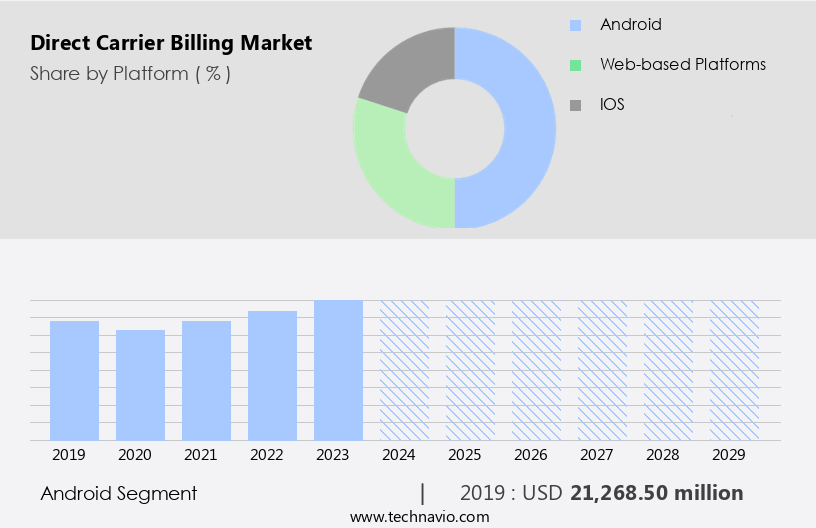

The Android segment is estimated to witness significant growth during the forecast period. The Direct Carrier Billing (DCB) market is witnessing significant growth, particularly in regions with low credit card penetration and high mobile usage. Android, as the dominant mobile operating system, plays a crucial role in driving digital monetization through DCB. Its vast user base and open ecosystem enable seamless integration of DCB across a multitude of devices and app stores. This accessibility empowers users to make purchases for digital content, such as games, streaming services, and in-app features, by charging payments to their mobile phone bills. Telecom operators and digital merchants favor Android for DCB deployments due to its flexibility and compatibility with various billing platforms, third-party payment processors, and wallet integrations.

Security protocols and fraud prevention measures are prioritized to ensure secure transactions. Real-time processing and customer support are essential components of DCB, enabling user-friendly experiences and efficient account management. Business models range from revenue sharing to flat fees, while technical support and integration partners facilitate seamless implementation. DCB also supports various pricing models, including subscription management and in-app purchases. The market's evolution includes the integration of marketing automation, reporting tools, and mobile marketing to enhance user engagement and acquisition. DCB's penetration rate continues to grow, driving the expansion of mobile commerce, digital content delivery, and other industries.

The Android segment was valued at USD 21.27 billion in 2019 and showed a gradual increase during the forecast period.

The Direct Carrier Billing (DCB) Market is growing rapidly, fueled by innovations in rewards programs and personalized mobile advertising that enhance user engagement. As digital transactions diversify, support for debit card processing, ewallet integration, and cryptocurrency payments broadens DCB's appeal. Service providers are leveraging big data analytics to optimize user experiences while adhering to strict compliance standards and reinforcing data security. Accurate payment reconciliation ensures smooth financial operations, though integration costs remain a consideration for smaller players.

Regional Analysis

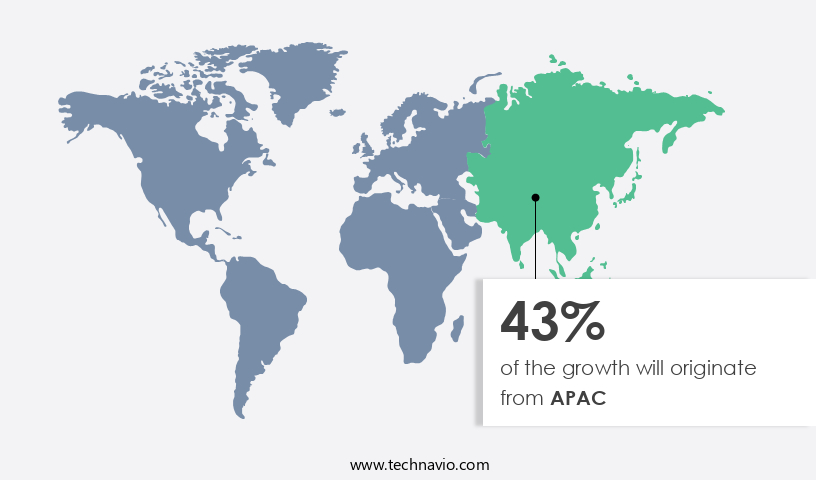

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The global Direct Carrier Billing (DCB) market is experiencing significant growth, particularly in the Asia-Pacific (APAC) region. This expansion is attributed to the lower penetration of credit and debit cards in APAC compared to other regions, which includes several populous emerging economies. Consumer income growth and their increasing technological adoption fuel the market's expansion in APAC. The widespread use of mobile devices, especially smartphones with high-speed networks, and the digital world's growing appeal are key factors driving market focus towards expanding their customer base in this region. The DCB market's technology stack includes recurring billing, conversion optimization, customer support, global coverage, wallet integration, operator billing, payment gateways, security protocols, payment solutions, USSD billing, third-party payment processors, SMS billing, pricing models, in-app purchases, SDK integration, carrier billing platform, customer segmentation, account management, business models, technical support, and MMS billing.

The DCB platform's ability to offer real-time processing, security, and seamless integration with various partners and systems is crucial for its success. The market's focus on conversion optimization, fraud prevention, and customer segmentation helps businesses maximize revenue and minimize churn. The market's penetration rate is increasing as more businesses recognize the potential of DCB as a payment solution, especially for digital content delivery and mobile commerce. The market's future growth is expected to be driven by continued innovation, increased focus on user experience, and the integration of advanced technologies like AI and machine learning.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Direct Carrier Billing market drivers leading to the rise in the adoption of Industry?

- The significant growth in consumer demand for digital content serves as the primary market catalyst. The global market for Direct Carrier Billing (DCB) is experiencing significant growth due to the increasing preference of consumers for digital content. DCB enables wireless subscribers of telecommunication networks to purchase digital goods online by charging the cost to their phone bills. This payment method offers several advantages, including convenience and reliability, making it an attractive option for consumers. The rise of digital media is a key driver for the DCB market. The availability of various digital formats and the increasing number of portable devices that promote digital media consumption have expanded consumers' choices. Additionally, the increasing speed of the Internet ensures that digital content can be accessed at any time and from anywhere.

- The pricing models for DCB services vary, with some providers offering SDK integration and others utilizing carrier billing platforms. Businesses can also segment their customer base and offer account management services to enhance the user experience. Technical support and real-time processing are essential features of DCB services, ensuring a seamless transaction process. The penetration rate of DCB services is expected to increase as more consumers opt for digital content and telecommunication providers continue to invest in this payment method. Overall, the DCB market is poised for continued growth as it offers a convenient and reliable payment solution for digital goods and services. Platforms like Android and iOS support DCB, enabling in-app purchases and subscriptions for services like mobile gaming, music streaming, and video-on-demand.

What are the Direct Carrier Billing market trends shaping the Industry?

- The rising prevalence of cryptocurrencies represents a significant market trend in the present day. This increasing popularity signifies a notable shift in the financial landscape. The Direct Carrier Billing (DCB) market is witnessing significant growth due to the increasing popularity of mobile commerce and digital content delivery. This market allows consumers to make payments for digital goods and services directly through their mobile phone bills. Security is a top priority in this market, with regular security audits ensuring the protection of sensitive customer data. Transaction fees are a crucial factor in the DCB market, with API integration enabling seamless and cost-effective payment processing. Customer acquisition cost is a significant challenge, but data analytics and A/B testing help optimize marketing strategies. Subscription management is essential for recurring billing, while user interface (UI) design is crucial for enhancing the customer experience.

- Integration with partners is vital for expanding reach and increasing conversion rates. DCB is particularly beneficial for emerging economies where credit card usage is low, and mobile phones are the primary means of internet access. The market's dynamics are influenced by factors such as transaction fees, customer acquisition cost, and conversion rates. Overall, the DCB market offers immense potential for businesses looking to tap into the mobile payment trend. Billing, enables smartphone users to make online purchases and subscriptions for Over-The-Top (OTT) content, including games, music streaming, and video-on-demand services, by charging the amount directly to their mobile phone bills.

How does Direct Carrier Billing market faces challenges during its growth?

- The intense competition posed by emerging alternative payment technologies represents a significant challenge to the industry's growth trajectory. The global Direct Carrier Billing (DCB) market faces competition from other payment technologies, such as payment wallet apps, credit cards, debit cards, and internet banking, posing a challenge to its growth. The online payment industry experiences continuous change, with disruptive and emerging technologies frequently altering consumer payment preferences. The market is concentrated, with major players offering similar services with varying checkout times. Alternate payment modes aim to accelerate transactions without compromising data protection. Batch processing, user experience (UX), marketing automation, reporting tools, and fraud prevention are crucial elements shaping the DCB market. Payment processing through a mobile payment gateway ensures seamless transactions, while payment aggregators simplify the payment process for merchants.

- Mobile marketing and IVR billing offer convenience to consumers, enhancing the overall user experience. The churn rate is a significant concern for market participants, requiring robust fraud prevention measures to minimize revenue loss. The customer lifetime value is a crucial metric for businesses, emphasizing the importance of maintaining a positive user experience. Reporting tools enable businesses to monitor and analyze transaction data, enabling data-driven decision-making. The DCB market is dynamic, with various factors influencing its growth and development. The focus on enhancing the user experience, ensuring data protection, and maintaining a competitive edge in the market are essential for market success.

Exclusive Customer Landscape

The direct carrier billing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the direct carrier billing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, direct carrier billing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amdocs Ltd. - This company specializes in providing direct carrier billing solutions for app stores and digital content, enabling seamless integration into customers' mobile bills.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amdocs Ltd.

- AT and T Inc.

- Bango Plc

- BCE Inc.

- Boku Inc.

- Centili Ltd.

- Deutsche Telekom AG

- Digital Virgo

- DIMOCO Carrier Billing GmbH

- LINK Mobility Group Holding ASA

- Nippon Telegraph and Telephone Corp.

- Orange SA

- RGK Mobile

- Singapore Telecommunications Ltd.

- SLA Digital

- Swisscom Ltd.

- Telenor Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Direct Carrier Billing Market

- In January 2024, global telecommunications giant Vodafone Group announced the expansion of its Direct Carrier Billing (DCB) service to 15 new markets, including Indonesia, Mexico, and South Africa. This move aimed to increase the reach of its DCB offering and cater to the growing demand for convenient digital payments in these regions (Vodafone Group Press Release, 2024).

- In March 2024, mobile payment platform, Mobikwik, partnered with leading mobile operator, Airtel Africa, to offer Direct Carrier Billing for its services across seven African countries. This collaboration aimed to provide Mobikwik users with a more convenient and accessible payment option, particularly in areas with limited banking infrastructure (Mobikwik Press Release, 2024).

- In May 2024, fintech company, Paytm, raised a USD1 billion funding round led by Alibaba Group and Ant Financial. A significant portion of the funds was earmarked for expanding Paytm's Direct Carrier Billing services, which had already seen significant growth in India (Paytm Press Release, 2024).

- In February 2025, the European Union's Revised Payment Services Directive (PSD2) came into effect, mandating that telecom operators provide third-party providers access to their billing systems for payment initiation services. This regulatory change opened up new opportunities for Direct Carrier Billing in Europe, particularly for digital content providers and mobile payment platforms (European Parliament and Council of the European Union, 2025).

Research Analyst Overview

The market continues to evolve, driven by the increasing demand for seamless and convenient payment solutions across various sectors. Recurring billing and conversion optimization are key focus areas, with telecommunication providers offering global coverage and wallet integration to enhance user experience (UX). Operator billing, payment gateways, and security protocols form the technology stack for these platforms, ensuring real-time processing and fraud prevention. Customer segmentation, account management, and business models are essential components of carrier billing platforms, enabling telecoms to cater to diverse customer needs. Technical support, pricing models, and in-app purchases are integrated to optimize customer acquisition cost and increase conversion rates.

Mobile commerce, digital content delivery, and mobile marketing are primary applications of carrier billing. SDK integration and API integration facilitate seamless partnerships with third-party payment processors, enabling a wide range of payment solutions. Penetration rate, transaction fees, and data analytics are critical performance indicators for carrier billing platforms. Telecommunication providers undergo security audits and offer technical support to ensure the highest levels of security and reliability. Churn rate, batch processing, and customer lifetime value are essential metrics for telecoms to monitor and manage. Usability, pricing, and marketing automation are key factors influencing customer satisfaction and loyalty.

Payment aggregators, SMS billing, USSD billing, MMS billing, and IVR billing are additional features that expand the reach and versatility of carrier billing platforms. Reporting tools provide valuable insights into platform performance and customer behavior, enabling continuous improvement and innovation. This method is increasingly popular, especially among smartphone users who consume OTT (Over-The-Top) content such as games, music streaming, and video-on-demand services.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Direct Carrier Billing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

229 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.4% |

|

Market growth 2025-2029 |

USD 28.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.3 |

|

Key countries |

US, China, India, Japan, Germany, South Korea, UK, France, Spain, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Direct Carrier Billing Market Research and Growth Report?

- CAGR of the Direct Carrier Billing industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the direct carrier billing market growth of industry companies

We can help! Our analysts can customize this direct carrier billing market research report to meet your requirements.

RIA -

RIA -