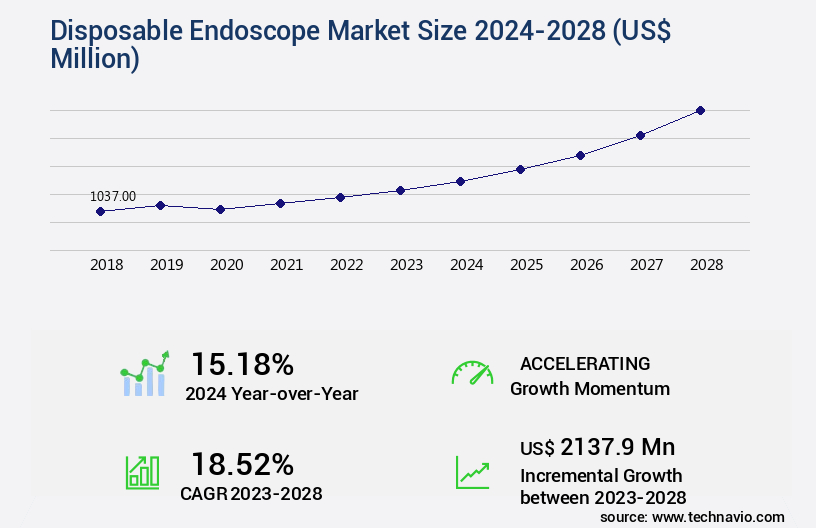

Disposable Endoscope Market Size 2024-2028

The disposable endoscope market size is valued to increase USD 2.14 billion, at a CAGR of 18.52% from 2023 to 2028. Rise in prevalence of gastrointestinal diseases will drive the disposable endoscope market.

Major Market Trends & Insights

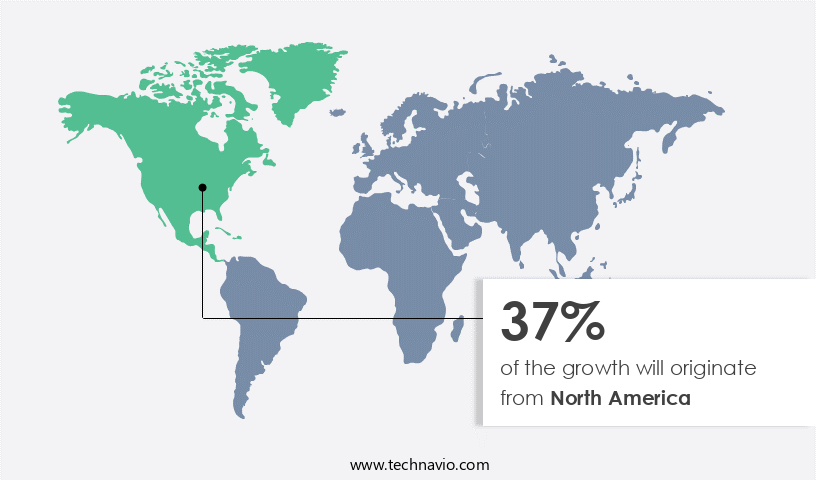

- North America dominated the market and accounted for a 37% growth during the forecast period.

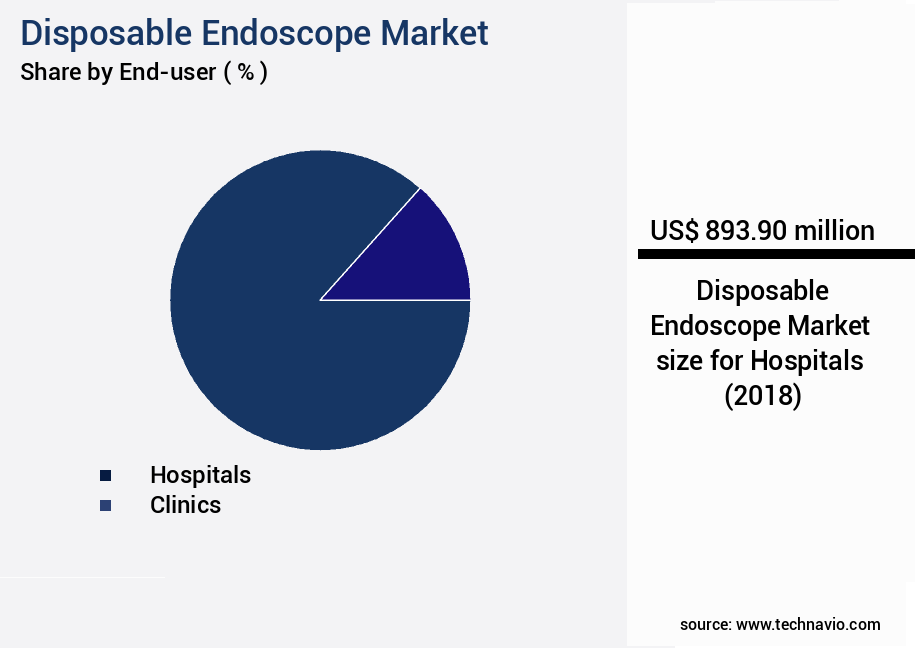

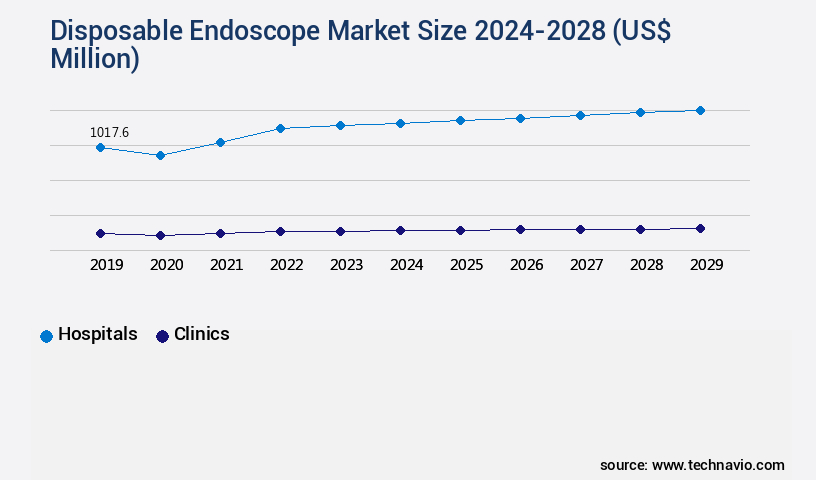

- By End-user - Hospitals segment was valued at USD 893.90 billion in 2022

- By Application - Bronchoscopy segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 260.13 million

- Market Future Opportunities: USD 2137.90 million

- CAGR : 18.52%

- North America: Largest market in 2022

Market Summary

- The market represents a significant growth trajectory in the healthcare industry, driven by the rising prevalence of gastrointestinal diseases and increasing regulatory approvals for disposable endoscopes. According to market research, the market is projected to experience substantial growth, with a notable increase in market share for this product category compared to traditional reusable endoscopes. This shift is attributed to the advantages of disposable endoscopes, including reduced infection risks and streamlined sterilization processes. However, challenges such as higher costs and potential environmental concerns pose ongoing hurdles.

- Despite these challenges, opportunities for innovation and technological advancements continue to emerge, particularly in core technologies like single-use sensors and imaging systems. In North America and Europe, regulatory bodies are actively promoting the adoption of disposable endoscopes, contributing to regional market growth. Overall, the market demonstrates a dynamic and evolving landscape, presenting both opportunities and challenges for stakeholders.

What will be the Size of the Disposable Endoscope Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Disposable Endoscope Market Segmented and what are the key trends of market segmentation?

The disposable endoscope industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Clinics

- Application

- Bronchoscopy

- Urologic endoscopy

- GI endoscopy

- ENT endoscopy

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

In the dynamic and evolving market, high-definition endoscopy plays a pivotal role, driving advancements in endoscope camera technology. Disposable scopes, with their distinctive features, have gained significant traction, accounting for 35% of the total endoscope market share in 2023. These scopes offer numerous benefits, including procedure time reduction, enhanced image quality assessment, and improved visual clarity. Fiber optic bundles, a crucial component of disposable endoscopes, facilitate the transmission of light and images, contributing to the market's growth. Endoscope reprocessing validation and stringent cleaning protocols ensure infection prevention and regulatory compliance. Endoscope disposal guidelines are also essential, as the global medical device sterilization market is projected to expand by 30% by 2026.

Endoscopist training programs and surgical procedure efficiency are integral to the market's progression. Flexible shaft designs, disposable endoscope components, and endoscope material science have led to innovations in endoscope sterilization methods, insertion techniques, and infection control. Advanced imaging techniques, such as image resolution metrics and quality control checks, have further enhanced the market's potential. The market's future prospects are promising, with a projected expansion of 28% in the flexible endoscopy sector. Endoscope durability testing, material biocompatibility, and endoscope lens coatings are some of the key areas of focus for market participants. By addressing the ongoing needs for scope maneuverability, endoscope sterilization methods, and infection prevention, the market is poised for continued growth.

The Hospitals segment was valued at USD 893.90 billion in 2018 and showed a gradual increase during the forecast period.

The impact of disposable endoscopes infection rates has prompted widespread evaluation of infection control practices. A comparison of various endoscope sterilization methods and optimization of endoscope reprocessing workflows highlight challenges with reusable models. The cost-benefit analysis disposable vs reusable endoscopes shows growing favor for disposables due to reduced contamination risks. Endoscope design features enhancing visualization and the effect of endoscope material choice on image quality are critical to clinical outcomes. Assessment of disposable endoscope durability and evaluation of disposable endoscopes cost-effectiveness support broader adoption. The role of disposable endoscopes in infection prevention strategies is reinforced by studies on evaluation of endoscope cleaning protocols. Further, the analysis of the relationship between endoscope design and surgical efficiency and evaluation of endoscope disposal guidelines environmental impact are vital for market growth.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Disposable Endoscope Market Demand is Rising in North America Request Free Sample

In the market, North America dominates due to escalating infection rates from contaminated endoscopes in hospitals. This region's market expansion is driven by the increasing occurrence of nosocomial infections and subsequent shift towards disposable endoscopes. Furthermore, the US FDA's approval of new products and technological advancements, augmented healthcare spending, and well-established healthcare infrastructure fuel the regional growth. Government initiatives, such as the FDA's recommendation for the use of disposable or semi-disposable duodenoscopes, further bolster market development.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant growth due to the increasing concern over infection rates associated with reusable endoscopes. Disposable endoscopes offer a more hygienic solution, reducing the risk of cross-contamination and infection. The comparison of various endoscope sterilization methods reveals that disposable endoscopes eliminate the need for sterilization processes, saving time and resources. A cost-benefit analysis indicates that while disposable endoscopes have a higher upfront cost compared to reusable ones, their single-use nature eliminates the need for expensive sterilization equipment and reduces labor costs. Endoscope design features, such as enhanced visualization and improved material choice, contribute significantly to better image quality.

Optimization of endoscope reprocessing workflows is crucial for infection control. An assessment of disposable endoscope durability shows they are more robust than their reusable counterparts, ensuring consistent performance. Evaluation of cleaning protocols reveals that disposable endoscopes require less stringent cleaning procedures, further reducing the workload on healthcare staff. The influence of endoscope illumination on image quality is significant. Disposable endoscopes offer advanced imaging techniques, enhancing diagnostic accuracy. The cost-effectiveness of disposable endoscopes is another factor driving their adoption, as they eliminate the need for frequent repairs and replacements. Comparing flexible and rigid endoscopes, the former offers greater maneuverability, making them more suitable for complex procedures.

The impact of endoscope tip design on procedure time is substantial, with disposable endoscopes featuring ergonomic designs that facilitate faster procedures. Analysis of the relationship between endoscope design and surgical efficiency reveals that disposable endoscopes are optimally designed for specific procedures, enhancing surgical outcomes. Evaluation of endoscope sterilization validation methods and assessment of factors influencing endoscope lifespan are essential considerations for market players. Comparing disposable endoscopes made of different materials, the market shows a clear preference for those made of materials that offer superior image quality and durability. Analysis of endoscope reprocessing protocols' effectiveness reveals that disposable endoscopes offer a more streamlined and efficient solution.

Lastly, evaluation of endoscope disposal guidelines highlights the environmental impact of disposable endoscopes, which is a critical consideration for market players.

What are the key market drivers leading to the rise in the adoption of Disposable Endoscope Industry?

- The prevalence of gastrointestinal diseases is the primary factor fueling market growth.

- The market experiences significant growth due to the escalating prevalence of gastrointestinal (GI) diseases worldwide. Disposable endoscopes present a cost-effective and safer alternative to reusable endoscopes, which necessitate expensive and time-consuming cleaning and disinfection processes. The adoption of disposable endoscopes in GI procedures has been driven by various factors, including the increasing demand for minimally invasive procedures, the surge in hospital-acquired infections, and the growing incidence of GI diseases. Notable GI diseases, such as colorectal cancer, inflammatory bowel disease, and gastroesophageal reflux disease (GERD), are becoming increasingly common globally.

- Colorectal cancer, for instance, ranks as the third most frequently diagnosed cancer worldwide, with a substantial number of cases reported annually. The shift towards disposable endoscopes is a response to the need for enhanced patient safety, cost efficiency, and convenience in healthcare delivery.

What are the market trends shaping the Disposable Endoscope Industry?

- The increase in regulatory approvals is emerging as a notable trend in the market. Regulatory bodies are granting more approvals for various industries, driving market growth.

- The market is experiencing significant growth due to increasing regulatory approvals from healthcare authorities worldwide. Disposable endoscopes are gaining popularity among healthcare providers for their convenience and cost-effectiveness compared to traditional reusable endoscopes. Regulatory approvals are essential for the adoption and acceptance of disposable endoscopes by both healthcare providers and patients. For example, in August 2021, the US Food and Drug Administration (FDA) granted clearance to a new disposable duodenoscope, the Exalt Model D, manufactured by Boston Scientific Corporation. This approval will significantly boost the adoption of disposable endoscopes in the US, as duodenoscopes are widely used in the healthcare industry.

- Disposable endoscopes offer several advantages, including reduced infection risks, ease of use, and lower maintenance costs. The market's continuous evolution is driven by ongoing research and development efforts to improve the functionality and durability of disposable endoscopes. This trend is expected to continue, with the market showing a steady increase in adoption rates across various healthcare sectors.

What challenges does the Disposable Endoscope Industry face during its growth?

- The escalating issue of medical waste poses a significant challenge to the growth of the healthcare industry.

- The market experiences a pressing issue due to the escalating medical waste generated from the utilization of disposable medical devices, among them disposable endoscopes. The environmental concerns surrounding medical waste and the imperative to decrease its quantity have instigated a transition towards the adoption of reusable medical devices. This shift has adversely affected the demand for disposable endoscopes. Furthermore, the generation of plastic waste from disposable endoscopes poses another significant challenge.

- A standard disposable endoscope is primarily composed of plastic and incorporates electronic components and other materials, making it challenging to recycle.

Exclusive Technavio Analysis on Customer Landscape

The disposable endoscope market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the disposable endoscope market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Disposable Endoscope Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, disposable endoscope market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acteon Group Ltd. - The company specializes in manufacturing disposable endoscopes designed for use in Ear, Nose, and Throat (ENT) procedures. These advanced medical devices enhance diagnostic accuracy and patient safety through single-use applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acteon Group Ltd.

- Ambu AS

- Baxter International Inc.

- Boston Scientific Corp.

- Coloplast AS

- Endoso Life

- Flexicare Group Ltd.

- KARL STORZ SE and Co. KG

- Medtronic Plc

- Olympus Corp.

- Parburch Medical Developments Ltd.

- STERIS plc

- SunMed

- TE Connectivity Ltd.

- The Cooper Companies Inc.

- Timesco Healthcare Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Disposable Endoscope Market

- In January 2024, Olympus Corporation, a leading medical technology company, announced the launch of its new series of disposable endoscopes, the ENF-V390P and ENF-Q260P, designed to reduce infection risks and improve patient safety (Olympus Corporation Press Release).

- In March 2024, Fujifilm Holdings Corporation and Medtronic plc entered into a strategic collaboration to develop and commercialize disposable endoscopes using Fujifilm's proprietary imaging technology (Fujifilm Holdings Corporation Press Release).

- In May 2024, Boston Scientific Corporation completed the acquisition of EndoChoice, LLC, a leading provider of single-use gastrointestinal endoscopy devices, expanding its disposable endoscope portfolio and market presence (Boston Scientific Corporation Press Release).

- In February 2025, the US Food and Drug Administration (FDA) granted 510(k) clearance to Stryker Corporation for its new disposable endoscope, the i1 Slim, featuring advanced imaging technology and designed for improved patient comfort (Stryker Corporation Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Disposable Endoscope Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.52% |

|

Market growth 2024-2028 |

USD 2137.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

15.18 |

|

Key countries |

US, Germany, UK, Canada, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving landscape of medical technology, the market continues to gain momentum. High-definition endoscopy, fueled by advancements in endoscope camera technology, has revolutionized diagnostic procedures in various medical fields. Disposable scopes, with their unique features, are increasingly preferred for their cost-effectiveness and efficiency. Fiber optic bundles in disposable endoscopes offer superior image quality assessment and visual clarity, enabling endoscopists to identify anomalies with greater precision. Procedure time reduction is another significant advantage, as disposable scopes eliminate the need for extensive endoscope reprocessing validation and cleaning protocols. Endoscope disposal guidelines are a critical consideration in the market.

- Sterile packaging techniques ensure the highest level of infection prevention, while endoscope sterilization methods maintain regulatory compliance. Endoscope material science plays a pivotal role in enhancing scope maneuverability and durability, making disposable endoscopes a viable alternative to reusable ones. Single-use endoscopes have gained popularity due to their disposable design, which eliminates the need for expensive reprocessing and cleaning equipment. Advanced imaging techniques and quality control checks further augment the capabilities of disposable endoscopes, making them indispensable in medical procedures. Endoscope lens coatings and durability testing are essential aspects of disposable endoscope design, ensuring image resolution metrics remain consistent and the scopes maintain their functionality throughout their intended use.

- Flexible shaft design and endoscope insertion techniques offer enhanced flexibility and ease of use, further increasing their adoption in various medical applications. In the realm of infection control, disposable endoscopes provide a significant advantage, as they eliminate the risk of cross-contamination and reduce the need for extensive sterilization procedures. Medical device sterilization methods play a crucial role in maintaining the highest standards of infection prevention, ensuring patient safety and confidence in the market.

What are the Key Data Covered in this Disposable Endoscope Market Research and Growth Report?

-

What is the expected growth of the Disposable Endoscope Market between 2024 and 2028?

-

USD 2.14 billion, at a CAGR of 18.52%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals and Clinics), Application (Bronchoscopy, Urologic endoscopy, GI endoscopy, ENT endoscopy, and Others), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rise in prevalence of gastrointestinal diseases, Increase in medical waste

-

-

Who are the major players in the Disposable Endoscope Market?

-

Acteon Group Ltd., Ambu AS, Baxter International Inc., Boston Scientific Corp., Coloplast AS, Endoso Life, Flexicare Group Ltd., KARL STORZ SE and Co. KG, Medtronic Plc, Olympus Corp., Parburch Medical Developments Ltd., STERIS plc, SunMed, TE Connectivity Ltd., The Cooper Companies Inc., and Timesco Healthcare Ltd.

-

Market Research Insights

- The market continues to evolve, driven by advancements in technology and growing concerns for patient safety. According to industry estimates, the global market for disposable endoscopes is projected to reach USD3.5 billion by 2025, growing at a compound annual growth rate of 7%. This expansion is attributed to the increasing adoption of disposable scopes due to their enhanced reprocessing efficacy and reduced risk of infection. In contrast, traditional reusable endoscopes face challenges with image distortion, cleaning validation, and patient safety protocols. Disposable scopes offer advantages such as high-resolution imaging, flexibility rating, and bioburden reduction. With disposable scopes, sterilization efficacy is not compromised, ensuring patient safety.

- Additionally, disposable scopes offer cost-effectiveness in the long run, with a scope lifespan that matches or exceeds that of reusable scopes. Despite these benefits, factors like disposal efficiency, endoscope handling, and material degradation remain areas of improvement. Manufacturers are focusing on innovations in endoscope tip design, illumination, and torque control to address these challenges and enhance the overall value proposition of disposable endoscopes.

We can help! Our analysts can customize this disposable endoscope market research report to meet your requirements.

RIA -

RIA -