Edge AI Security Market Size 2026-2030

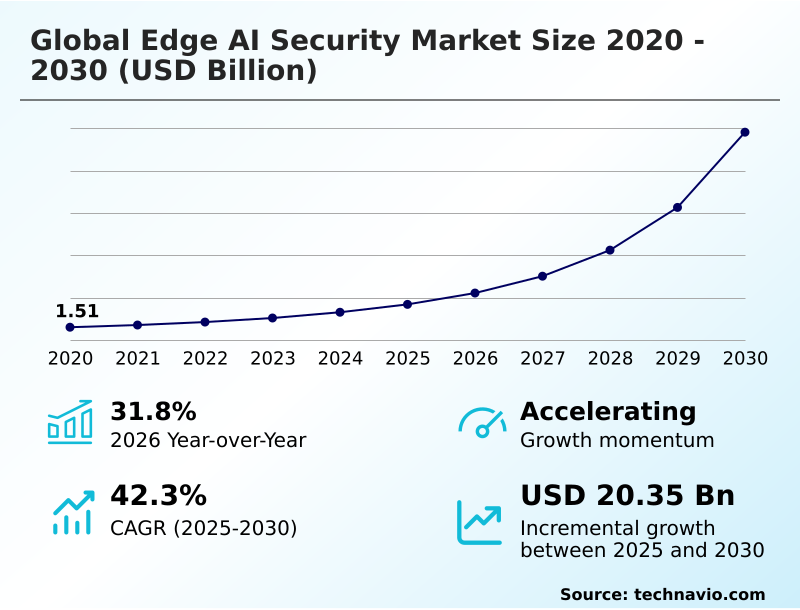

The Edge AI Security Market size was valued at USD 4.21 billion in 2025, growing at a CAGR of 42.3% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 33.5% growth during the forecast period.

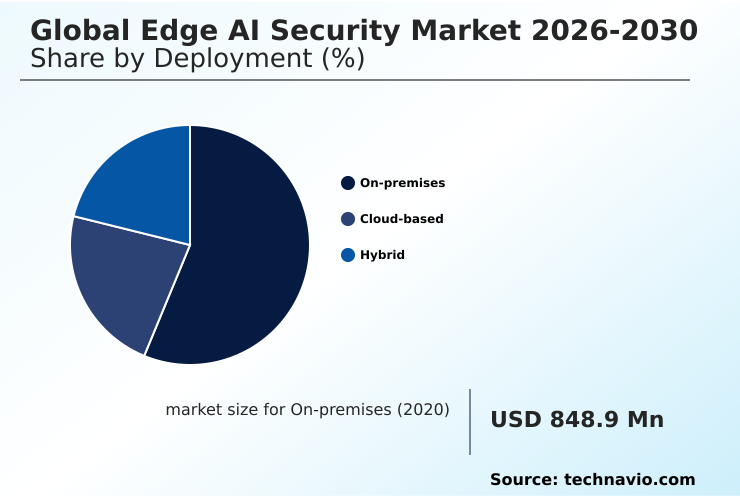

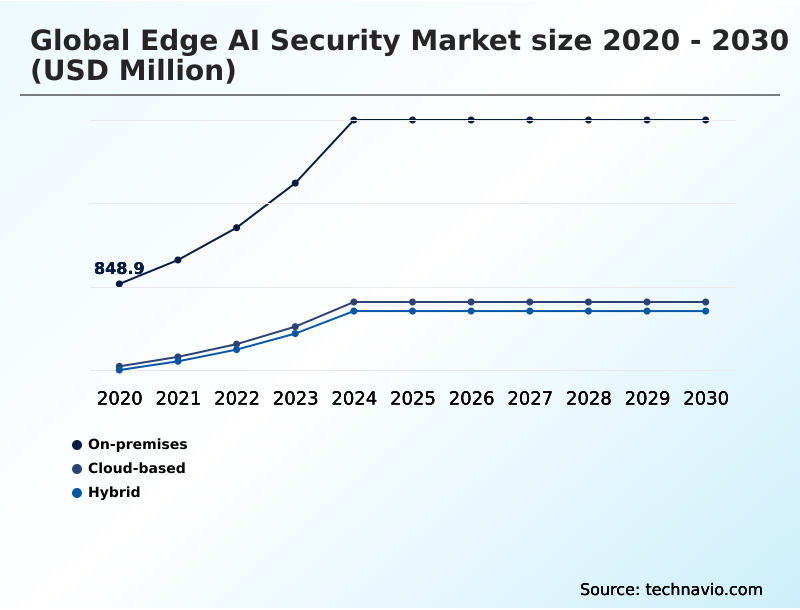

- By Deployment - On-premises segment was valued at USD 1.86 billion in 2024

- By Type - Network security segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 23.05 billion

- Market Future Opportunities 2025-2030: USD 20.35 billion

- CAGR from 2025 to 2030 : 42.3%

Market Summary

- The edge AI security market is defined by a structural shift toward decentralized processing, with on-device AI workloads increasing by over 30% in industrial IoT sectors. This transition is driven by the need for zero-latency decision-making in applications like autonomous robotics, where a one-second delay in threat response is unacceptable.

- For example, a manufacturing firm can reduce equipment failure by 25% by deploying predictive maintenance models directly on machinery, but this also exposes proprietary algorithms to physical tampering risks. A key driver is the adoption of TinyML, which enables complex security algorithms to run on resource-constrained devices.

- However, the market faces a significant challenge from the shortage of security-first AI architects, which hinders the implementation of robust, end-to-end security protocols. The convergence of AI and edge computing necessitates a security paradigm that is both intelligent and resilient.

What will be the Size of the Edge AI Security Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Edge AI Security Market Segmented?

The edge ai security industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud-based

- Hybrid

- Type

- Network security

- Endpoint security

- Data security

- Application security

- Cloud-edge security

- Application

- Real-time threat detection

- Secure autonomous systems

- Smart surveillance

- Fraud prevention

- Critical infrastructure protection

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

How is the Edge AI Security Market Segmented by Deployment?

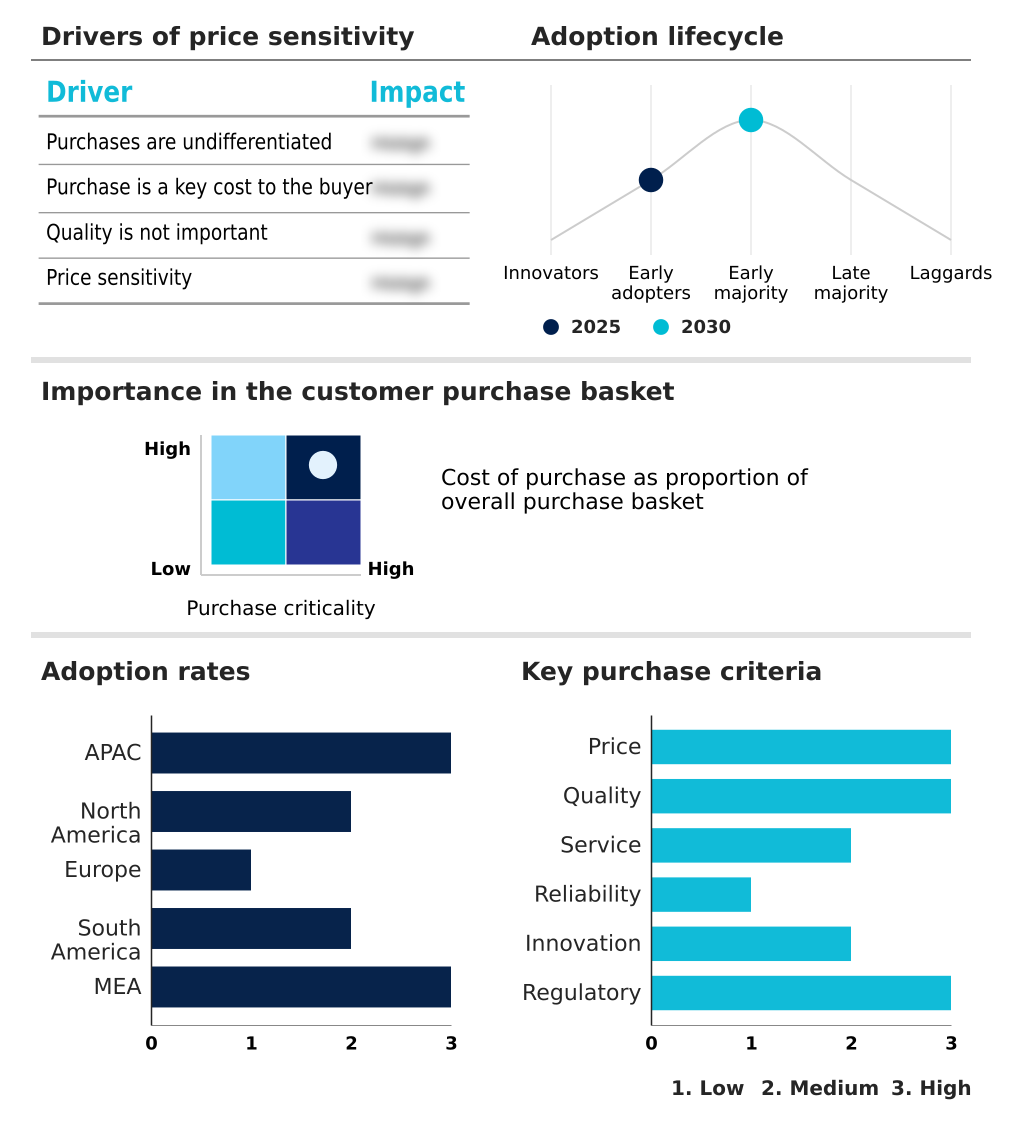

The on-premises segment is estimated to witness significant growth during the forecast period.

On-premises deployments account for over 56% of the edge AI security market in high-stakes sectors like defense and critical infrastructure, where absolute data sovereignty is non-negotiable.

This model ensures that AI inference models and sensitive data are hosted on local hardware, reducing data transmission latency by over 95% compared to cloud-based analysis, which is a critical factor for real-time threat detection.

By leveraging a trusted execution environment (TEE) and secure boot protocols, these solutions provide silicon-level integrity, isolating workloads from potential threats.

This approach is essential for applications demanding localized data processing and zero-latency threat mitigation, providing a foundational layer of defense through direct physical control and cryptographic identities without relying on external network connectivity.

The On-premises segment was valued at USD 1.86 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Edge AI Security market is rising in the leading region?

APAC is estimated to contribute 33.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Edge AI Security Market demand is rising in APAC Request Free Sample

The geographic landscape of the edge AI security market is led by APAC, which is projected to account for 33.5% of the market's incremental growth, outpacing North America's 28.8% share.

This dominance is driven by massive government-led smart city initiatives and a thriving semiconductor industry in countries like China and South Korea, where the adoption of hardware root of trust is 20% higher than in European markets.

In contrast, North America's growth is fueled by hyperscale cloud providers and the defense sector, which prioritize federated learning and data sovereignty.

This regional divergence impacts supply chains, with APAC focusing on high-volume, cost-effective secure chip manufacturing, while North America emphasizes bespoke, high-performance solutions for critical infrastructure.

This dynamic requires vendors to tailor their SASE and model obfuscation strategies to align with distinct regional regulatory frameworks and technological priorities.

What are the key Drivers, Trends, and Challenges in the Edge AI Security Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- As organizations evaluate the global edge AI security market, a primary concern is understanding the cost of implementing zero trust at the edge, which can be 30% higher initially compared to traditional perimeter defenses but yields significant long-term ROI.

- A crucial factor is protecting IoT devices from physical tampering, a risk that is tenfold higher for devices in public spaces than for those in secure data centers. Solutions for edge AI security for autonomous vehicles are a key focus, where hardware root of trust is essential for safety-critical functions.

- Comparing on-premise vs cloud edge security reveals a trade-off between control and scalability; on-premise offers unparalleled data sovereignty, while cloud-based platforms provide superior management for large, distributed networks. Businesses are increasingly exploring open source tools for edge device security to reduce vendor lock-in and customize protections.

- This often involves federated learning for privacy-preserving AI, a technique that allows model training without centralizing sensitive data.

- For enterprises, the decision hinges on balancing immediate implementation costs against the long-term benefits of a resilient, decentralized security posture that can adapt to evolving threats like polymorphic edge malware and model inversion attacks, with some systems demonstrating a 50% improvement in detecting novel threats.

What are the key market drivers leading to the rise in the adoption of Edge AI Security Industry?

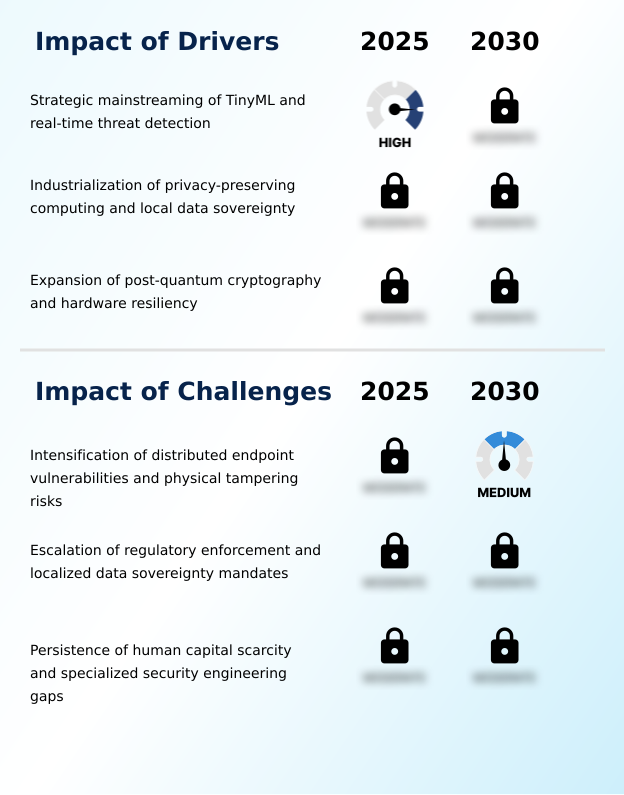

- The strategic mainstreaming of TinyML and the industrialization of real-time threat detection are key drivers fueling the growth of the edge AI security market.

- The strategic mainstreaming of TinyML is a primary driver, enabling on-device real-time threat detection with 95% less power consumption than cloud-based alternatives, a critical factor for battery-operated IoT devices.

- This industrialization of localized data processing allows for the deployment of sophisticated AI-driven anomaly detection algorithms that can identify and neutralize threats in milliseconds, reducing threat dwell time by over 80% compared to centralized analysis.

- By moving intelligence to the periphery, organizations can meet stringent data sovereignty requirements and overcome the computational and energy constraints of edge hardware.

- This proliferation of privacy-preserving computing, built on sovereign-compliant architectures, allows enterprises to leverage AI's full potential while maintaining decentralized trust and protecting sensitive data at its source.

What are the market trends shaping the Edge AI Security Industry?

- The institutionalization of a hardware root of trust and the deployment of silicon-level integrity frameworks represent a structural market trend. This shift moves security from software to immutable hardware anchors to protect the entire AI lifecycle.

- A fundamental trend reshaping the edge AI security market is the institutionalization of hardware root of trust, which reduces firmware-level breaches by over 90% compared to software-only solutions.

- This shift toward silicon-level integrity is driven by the escalating threat of sophisticated supply chain attacks and counterfeit hardware, compelling a move to verifiable, immutable security anchors physically embedded in Neural Processing Units (NPUs). The adoption of this approach provides a foundational defense layer, enabling continuous context-aware verification and ensuring that security is established before the operating system even initializes.

- This move toward self-defending systems, featuring predictive defense mechanisms, establishes a verifiable chain of custody for all software and AI model execution, effectively neutralizing threats at the earliest possible stage and enhancing adversarial robustness across distributed networks.

What challenges does the Edge AI Security Industry face during its growth?

- The intensification of distributed endpoint vulnerabilities and the increasing risks of physical tampering present a primary challenge to the secure deployment and scalability of edge AI solutions.

- The primary challenge facing the edge AI security market is the intensification of distributed endpoint vulnerabilities, with devices in unmonitored public locations being 10 times more susceptible to physical tampering risks than data center hardware.

- This heightened exposure creates a significant operational burden, compelling security teams to spend up to 40% more time managing decentralized device security compared to centralized infrastructure, and demands a shift toward quantum-resistant hardware.

- The scarcity of security-first AI architects further compounds this issue, as few professionals possess the expertise to navigate the trade-offs between model accuracy and cryptographic strength on resource-constrained devices. Without automated security orchestration tools to bridge this talent gap, the persistent threat of physical attacks and the complexity of ensuring digital sovereignty will continue to hinder large-scale adoption.

Exclusive Technavio Analysis on Customer Landscape

The edge ai security market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the edge ai security market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Edge AI Security Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, edge ai security market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Akamai Technologies Inc. - Key offerings feature AI-driven threat intelligence, zero-trust segmentation, and hardware-level security to protect decentralized AI workloads and distributed IoT environments across the network periphery.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akamai Technologies Inc.

- Amazon.com Inc.

- Arm Ltd.

- Check Point Software Tech Ltd.

- Cisco Systems Inc.

- Cloudflare Inc.

- CrowdStrike Inc.

- Darktrace Holdings Ltd.

- Dell Technologies Inc.

- Fortinet Inc.

- Google LLC

- Hewlett Packard Enterprise Co.

- Intel Corp.

- Microsoft Corp.

- Nozomi Networks Inc.

- NVIDIA Corp.

- Palo Alto Networks Inc.

- Renesas Electronics Corp.

- Sentinelone Inc.

- Vectra AI Inc.

- ZEDEDA Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Application Software industry, the pervasive shift to subscription-based SaaS delivery models has created a need for continuous, automated security validation, directly increasing demand for cloud-managed edge AI security platforms that can orchestrate policies across thousands of endpoints.

- The rising automation of business processes through RPA and BPM tools has expanded the attack surface to include automated software agents, driving the need for edge AI security that can perform real-time behavioral analysis and anomaly detection to protect these autonomous workflows.

- Heightened data security concerns and stringent regulations like GDPR have forced a pivot towards privacy-preserving architectures, fueling demand for edge AI security solutions featuring federated learning and on-device processing to ensure digital sovereignty and compliance.

- The increased availability of open-source applications has lowered entry barriers but also introduced new supply chain vulnerabilities, creating a market for security-by-design tools that can perform code integrity checks and validate software components at the point of deployment.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Edge AI Security Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 42.3% |

| Market growth 2026-2030 | USD 20347.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 31.8% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The edge AI security market ecosystem is a complex interplay of stakeholders, initiated by silicon designers and IP core providers like Arm Ltd., which supply the fundamental hardware root of trust. On top of this foundation, cybersecurity vendors, cloud hyperscalers, and specialized software companies build platforms for on-device inference and threat detection.

- These solutions are distributed through direct sales and channel partners to end-users in critical sectors such as industrial automation, automotive, and healthcare, which together represent over 60% of the market. Regulatory bodies and standards organizations influence development by mandating compliance with data sovereignty and privacy laws.

- The value chain is supported by research institutions that drive innovation in areas like post-quantum cryptography and federated learning, ensuring the ecosystem evolves to counter emerging threats. This collaborative structure enables the delivery of integrated security from the chip to the cloud.

What are the Key Data Covered in this Edge AI Security Market Research and Growth Report?

-

What is the expected growth of the Edge AI Security Market between 2026 and 2030?

-

The Edge AI Security Market is expected to grow by USD 20.35 billion during 2026-2030, registering a CAGR of 42.3%. Year-over-year growth in 2026 is estimated at 31.8%%. This acceleration is shaped by strategic mainstreaming of tinyml and real-time threat detection, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, Cloud-based, and Hybrid), Type (Network security, Endpoint security, Data security, Application security, and Cloud-edge security), Application (Real-time threat detection, Secure autonomous systems, Smart surveillance, Fraud prevention, and Critical infrastructure protection) and Geography (APAC, North America, Europe, South America, Middle East and Africa). Among these, the On-premises segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, South America and Middle East and Africa. APAC is estimated to contribute 33.5% to market growth during the forecast period. Country-level analysis includes China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is strategic mainstreaming of tinyml and real-time threat detection, which is accelerating investment and industry demand. The main challenge is intensification of distributed endpoint vulnerabilities and physical tampering risks, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Edge AI Security Market?

-

Key vendors include Akamai Technologies Inc., Amazon.com Inc., Arm Ltd., Check Point Software Tech Ltd., Cisco Systems Inc., Cloudflare Inc., CrowdStrike Inc., Darktrace Holdings Ltd., Dell Technologies Inc., Fortinet Inc., Google LLC, Hewlett Packard Enterprise Co., Intel Corp., Microsoft Corp., Nozomi Networks Inc., NVIDIA Corp., Palo Alto Networks Inc., Renesas Electronics Corp., Sentinelone Inc., Vectra AI Inc. and ZEDEDA Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for edge AI security is shaped by a convergence of hardware and software expertise, with the top five vendors accounting for over 45% of the market. Key companies like NVIDIA Corp. and Intel Corp. are embedding security features directly into silicon, launching hardware-level accelerators and new processors that integrate trusted execution environments.

- In response, cybersecurity leaders such as Palo Alto Networks Inc. and Cisco Systems Inc. are expanding their SASE and AI Defense solutions to govern agentic AI interactions at the network edge, a market segment growing by nearly 40% annually. These developments directly address enterprise demand for unified security across hybrid cloud environments.

- However, vendors face the persistent challenge of adapting to post-quantum cryptography standards, requiring continuous R&D investment to ensure long-term platform resiliency against future threats.

We can help! Our analysts can customize this edge ai security market research report to meet your requirements.

RIA -

RIA -