Electric Bus Market Size 2025-2029

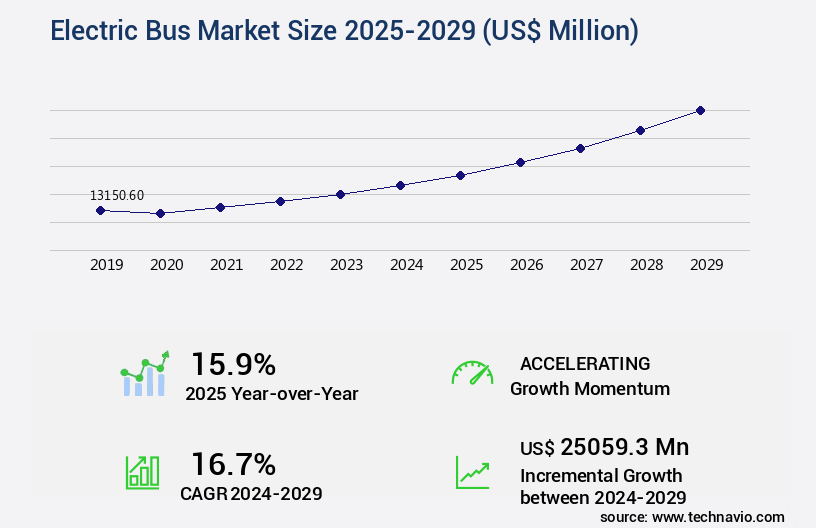

The electric bus market size is valued to increase USD 25.06 billion, at a CAGR of 16.7% from 2024 to 2029. Reduction in battery prices of electric buses will drive the electric bus market.

Major Market Trends & Insights

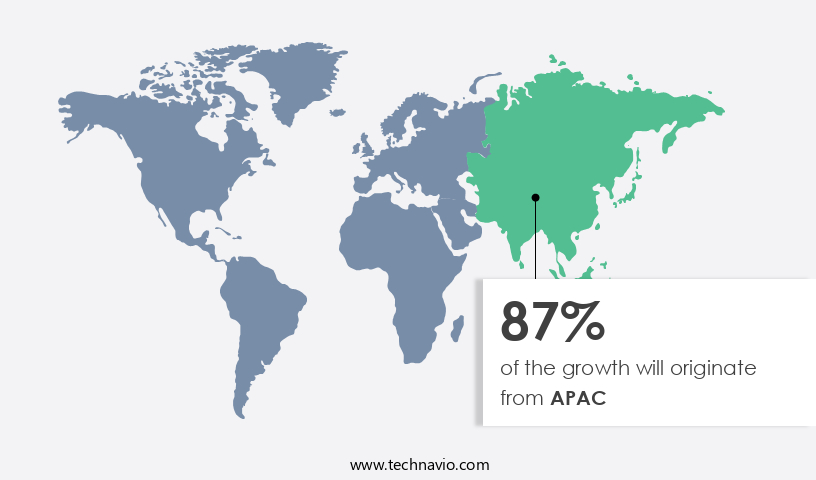

- APAC dominated the market and accounted for a 87% growth during the forecast period.

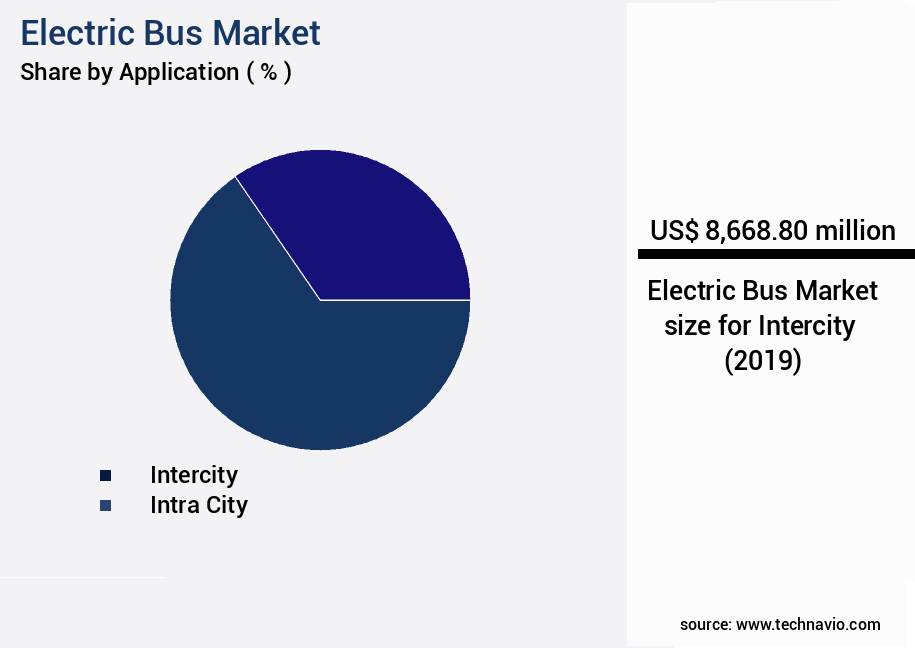

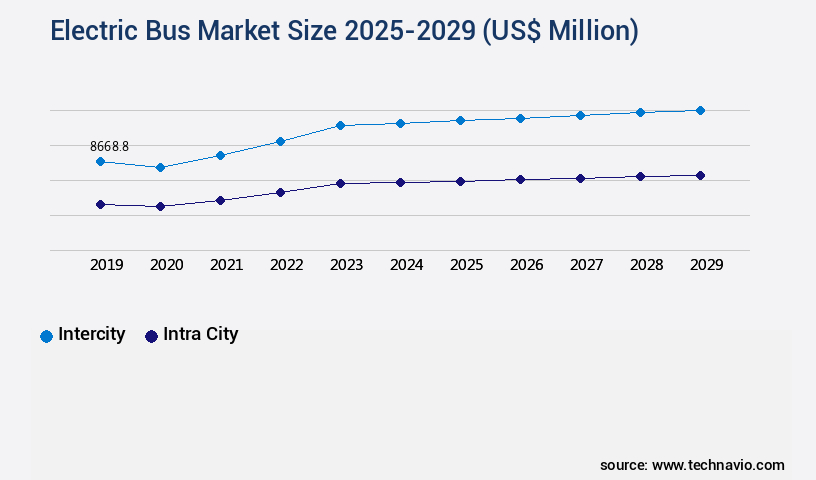

- By Application - Intercity segment was valued at USD 8.67 billion in 2023

- By Type - Pure electric bus segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 254.14 million

- Market Future Opportunities: USD 25059.30 million

- CAGR from 2024 to 2029 : 16.7%

Market Summary

- The market has experienced significant growth in recent years, driven by the global push towards sustainable transportation solutions. The market's size is projected to reach USD22.4 billion by 2027, reflecting a steady increase in demand. One of the key factors fueling this growth is the reduction in battery prices, making electric buses increasingly cost-competitive with their diesel counterparts. Another trend transforming the market is the increasing popularity of wireless charging systems. These systems enable buses to recharge while in motion, reducing downtime and improving operational efficiency. However, challenges remain, including the need for extensive infrastructure development and the ongoing debate surrounding battery range and charging infrastructure.

- Despite these challenges, the future of the market looks promising. As public transport users become more environmentally conscious, the demand for cleaner, more sustainable transportation options is expected to continue growing. Moreover, advancements in battery technology and charging infrastructure are poised to address current challenges and pave the way for a fully electrified public transport sector. In summary, the market is undergoing a transformation driven by cost reductions, technological advancements, and changing consumer preferences. With a projected market size of USD22.4 billion by 2027, the sector is poised for continued growth and innovation.

What will be the Size of the Electric Bus Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Electric Bus Market Segmented ?

The electric bus industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Intercity

- Intra city

- Type

- Pure electric bus

- Plug-in hybrid bus

- Speed

- Less than 200 Miles

- More than 200 Miles

- Capacity

- Up to 400 kWh

- Above 400 kWh

- Product Type

- Semi-autonomous

- Autonomous

- Propulsion Type

- Battery Electric Bus (BEV)

- Hybrid Electric Bus (HEV)

- Fuel Cell Electric Bus (FCEV)

- Battery Type

- Lithium-Ion

- Nickel-Metal Hydride

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The intercity segment is estimated to witness significant growth during the forecast period.

Amidst a global push towards electrification and emission reduction, the market is experiencing significant growth. In 2023, China led the APAC region with a substantial market share, as the Chinese government continues its efforts to replace diesel buses with electric ones, reducing vehicular emissions. India is following suit, aiming to have all vehicles electric by 2030. To support this transition, the Indian government is investing in electric bus infrastructure, attracting manufacturers like Volvo and BYD to establish operations. Advanced technologies, such as predictive maintenance, traction motor efficiency, and smart charging, are driving innovation in the sector. For instance, route optimization algorithms and energy consumption modeling help improve operational efficiency, while battery pack design, noise reduction technology, and thermal management systems enhance passenger comfort.

With the integration of advanced power electronics, regenerative braking systems, and onboard energy storage, electric buses are becoming increasingly competitive with their diesel counterparts. The electrification of bus fleets not only reduces emissions but also has a positive impact on the grid. By 2030, electric buses are expected to account for over 40% of the global bus market, making it a promising sector for investment.

The Intercity segment was valued at USD 8.67 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 87% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Electric Bus Market Demand is Rising in APAC Request Free Sample

The market in China is experiencing significant growth due to the increasing demand for public transportation solutions, particularly bus rapid transit (BRT), in metro cities. Consumers' heightened awareness of electric vehicles' advantages is propelling the shift from diesel to electric buses, making this a pivotal trend in the market. Buses are a ubiquitous component of transit systems, and their introduction and modification are relatively straightforward.

With a focus on mitigating traffic congestion and reducing vehicle emissions, Chinese authorities are advocating for the expansion of public transportation over private transportation. This preference for public transportation contributes to the market's robust expansion. As a professional, it is essential to acknowledge the importance of this evolving trend in the transportation sector.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as transit systems worldwide embrace the shift towards sustainable transportation. The adoption of electric buses is having a profound impact on the industry, with numerous benefits including reduced greenhouse gas emissions, improved passenger comfort, and enhanced safety features. One crucial aspect of electric bus implementation is the optimization of charging strategies. Lifecycle assessment of electric bus technologies reveals that efficient charging infrastructure deployment is essential for minimizing operational costs. Integration of renewable energy sources into electric bus fleets is another key strategy for reducing the carbon footprint and improving overall efficiency. Comparing different battery chemistries in electric buses is a topic of ongoing research, with each technology offering unique advantages.

For instance, lithium-ion batteries provide a high energy density, while sodium-ion batteries offer lower production costs. Optimizing the design of electric bus chassis and implementing efficient thermal management systems are other strategies to improve energy efficiency and reduce operation and maintenance costs. Electric bus motor technologies also warrant evaluation, as advancements in this area can lead to significant improvements in energy efficiency and range. Regenerative braking systems in electric buses are an essential feature that helps mitigate range anxiety by capturing energy during braking and storing it for later use. Smart charging algorithms and the implementation of efficient thermal management systems are essential for optimizing electric bus fleets.

Assessing the environmental impact of electric bus technologies is another critical consideration, as the production and disposal of batteries can pose environmental challenges. Reducing noise pollution is another key benefit of electric bus operations, contributing to improved urban environments and enhancing the overall passenger experience. Strategies for improving electric bus energy efficiency, such as aerodynamic design and lightweight materials, are also essential for reducing operational costs and increasing the competitiveness of electric buses in the market. Cost-benefit analysis is a crucial aspect of deploying electric bus systems, with the initial investment often outweighed by long-term savings on fuel and maintenance costs.

Planning future electric bus infrastructure needs involves careful consideration of charging infrastructure, battery swapping stations, and fleet size requirements. In conclusion, the market is poised for continued growth as transit systems worldwide adopt these sustainable vehicles. The optimization of charging strategies, integration of renewable energy sources, and evaluation of different battery chemistries are just a few of the key areas of focus for stakeholders in this dynamic and evolving industry. Adoption rates in developed regions are nearly double those in developing regions, underscoring the growing global demand for electric buses and the opportunities for innovation and growth in this sector.

What are the key market drivers leading to the rise in the adoption of Electric Bus Industry?

- The significant decrease in the cost of batteries for electric buses is the primary factor fueling market growth.

- Electric bus production costs are significantly influenced by battery prices. Battery manufacturers continue to innovate in the realm of electric bus batteries, with advancements in lithium-ion (Li-ion) technology leading to weight reduction and extended lifespan compared to conventional lead-acid and valve-regulated lead acid (VRLA) batteries. The initial cost of an electric bus is approximately 30%-35% higher than that of a conventional bus. This price difference underscores the importance of battery price trends in the market.

- As battery technology evolves, the cost differential between electric and conventional buses is expected to narrow, making electric buses increasingly competitive. This ongoing development in battery technology is a crucial factor driving the growth and evolution of the electric bus sector.

What are the market trends shaping the Electric Bus Industry?

- The rising preference for wireless charging systems represents a significant market trend in the present day. This trend is set to continue due to the increasing popularity of these systems.

- Inductive wireless charging technology for high-power electric buses is gaining traction due to its convenience for operators. The US Department of Energy's Oak Ridge National Laboratory (ORNL) has pioneered a 20-kW inductive wireless charging system for electric vehicles, which outperforms conventional plug-in systems. During testing, an electric Toyota RAV4 equipped with an additional 10-kWh battery achieved 90% efficiency using this system. This efficiency level is three times higher than that of plug-in systems, leading to the development of 50-kW wireless chargers.

- These chargers match the power capacity of quick plug-in chargers commercially available in the market. The continuous advancement in wireless charging technology signifies a shift towards more efficient and convenient charging solutions for electric buses, enhancing their overall performance and competitiveness in the transportation sector.

What challenges does the Electric Bus Industry face during its growth?

- The declining number of public transport users poses a significant challenge to the industry's growth trajectory. This trend, which is a major concern for industry professionals, threatens to hinder the expansion and progress of the public transport sector.

- The market faces challenges due to the shifting consumer preference towards personal vehicles, leading to a decline in demand for public transportation. This trend has left transit agencies hesitant to invest in expensive electric buses. The automobile industry's expansion, producing a diverse range of cars catering to various income groups, further hinders the market's growth. The demand for public transportation services is diminishing as personal vehicle ownership increases.

- Despite these challenges, the market continues to evolve, with advancements in battery technology and charging infrastructure potentially driving future adoption. The market's dynamics remain intriguing, with ongoing developments shaping its trajectory across various sectors.

Exclusive Technavio Analysis on Customer Landscape

The electric bus market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electric bus market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Electric Bus Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, electric bus market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alexander Dennis Limited

- Anhui Ankai Automobile Co. Ltd.

- Blue Bird Corporation

- BYD Company Ltd.

- CAF (Construcciones y Auxiliar de Ferrocarriles)

- CRRC Corporation Limited

- Daimler AG

- EBusco

- Gillig LLC

- GreenPower Motor Company Inc.

- Higer Bus Company Limited

- King Long United Automotive Industry Co. Ltd.

- MAN SE

- New Flyer Industries Inc.

- Proterra Inc.

- Scania AB

- Solaris Bus & Coach S.A.

- VDL Bus & Coach BV

- Volvo Buses

- Zhengzhou Yutong Bus Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electric Bus Market

- In January 2024, Proterra, a leading electric bus manufacturer, announced the launch of its new Catalyst E2 Series buses, featuring an extended range of up to 665 kilometers on a single charge, a significant leap in electric bus technology (Proterra Press Release, 2024).

- In March 2025, BYD Company Limited, the world's largest electric bus manufacturer, formed a strategic partnership with Transdev, a global mobility operator, to deploy 1,000 electric buses in Europe and South America over the next five years (BYD Company Limited Press Release, 2025).

- In April 2025, New Flyer Industries, Inc., a major North American bus manufacturer, raised USD200 million in a senior secured notes offering to accelerate its electric bus production and expand its charging infrastructure (New Flyer Industries, Inc. SEC Filing, 2025).

- In May 2025, the European Union passed the Fit for 55 package, a set of legislative proposals to reduce greenhouse gas emissions by at least 55% by 2030, which includes incentives for the adoption of electric buses and other zero-emission vehicles (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electric Bus Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

245 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.7% |

|

Market growth 2025-2029 |

USD 25059.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

15.9 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Amidst the global shift towards sustainable transportation, the market continues to evolve, driven by advancements in charging infrastructure, motor technology, and energy management systems. Charging station deployment has become a critical focus, with predictive maintenance ensuring optimal performance and minimizing downtime. Traction motor efficiency, a key performance indicator, is continually improving, thanks to motor control algorithms and DC fast charging technology. Energy consumption modeling and route optimization algorithms are essential tools for fleet operators, enabling them to maximize efficiency and reduce operational costs. Auxiliary power systems, battery pack design, and noise reduction technology contribute to enhancing passenger comfort and reducing the environmental impact of electric buses.

- Power electronics efficiency and regenerative braking systems play a significant role in minimizing energy loss and extending range. The electrification of bus infrastructure, including inverter technology and smart charging systems, is crucial for accommodating the increasing adoption of battery electric buses and electrification conversion kits. Emission reduction standards and the integration of onboard energy storage and battery management systems are shaping the future of electric buses. Lightweight bus materials, fleet management software, and thermal management systems further contribute to the growing appeal of these vehicles. Grid impact assessment and wireless charging technology are emerging trends, with the potential to revolutionize the market by addressing range anxiety and reducing the need for traditional charging infrastructure.

- In the realm of electric motor technology, advancements in electrification strategies and power electronics are paving the way for more efficient and cost-effective solutions.

What are the Key Data Covered in this Electric Bus Market Research and Growth Report?

-

What is the expected growth of the Electric Bus Market between 2025 and 2029?

-

USD 25.06 billion, at a CAGR of 16.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Intercity and Intra city), Type (Pure electric bus and Plug-in hybrid bus), Speed (Less than 200 Miles and More than 200 Miles), Capacity (Up to 400 kWh and Above 400 kWh), Product Type (Semi-autonomous and Autonomous), Geography (APAC, Europe, North America, Middle East and Africa, and South America), Propulsion Type (Battery Electric Bus (BEV), Hybrid Electric Bus (HEV), and Fuel Cell Electric Bus (FCEV)), and Battery Type (Lithium-Ion, Nickel-Metal Hydride, and Others)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Reduction in battery prices of electric buses, Declining number of public transport users

-

-

Who are the major players in the Electric Bus Market?

-

Alexander Dennis Limited, Anhui Ankai Automobile Co. Ltd., Blue Bird Corporation, BYD Company Ltd., CAF (Construcciones y Auxiliar de Ferrocarriles), CRRC Corporation Limited, Daimler AG, EBusco, Gillig LLC, GreenPower Motor Company Inc., Higer Bus Company Limited, King Long United Automotive Industry Co. Ltd., MAN SE, New Flyer Industries Inc., Proterra Inc., Scania AB, Solaris Bus & Coach S.A., VDL Bus & Coach BV, Volvo Buses, and Zhengzhou Yutong Bus Co. Ltd.

-

Market Research Insights

- The market is a dynamic and evolving sector within the broader transportation industry, characterized by ongoing advancements in technology and infrastructure. Two significant aspects of this market include the cost of charging infrastructure and the integration of passenger information systems. According to industry estimates, charging infrastructure costs have decreased by 30% over the past five years, making electric buses increasingly competitive with their diesel counterparts. Meanwhile, the adoption of advanced passenger information systems has improved operational efficiency and user experience, with over 70% of new electric buses now featuring real-time tracking and communication capabilities. Battery cell chemistry, electrification strategies, bus fleet electrification, and maintenance scheduling are other crucial elements shaping the market.

- Range anxiety mitigation through fast charging networks and powertrain integration are essential for the widespread adoption of electric buses in urban transport solutions. Sustainable transportation initiatives, accessibility features, and the integration of renewable energy sources further underscore the importance of this market. Challenges, such as electrification costs, battery life expectancy, public transit planning, and energy recovery systems, continue to be addressed through innovative solutions like battery recycling processes, smart charging algorithms, and grid stability solutions. The ongoing development of electric bus technology is a testament to the industry's commitment to providing efficient, sustainable, and accessible transportation solutions.

We can help! Our analysts can customize this electric bus market research report to meet your requirements.

RIA -

RIA -