Electroporation and Electrofusion Market Size 2024-2028

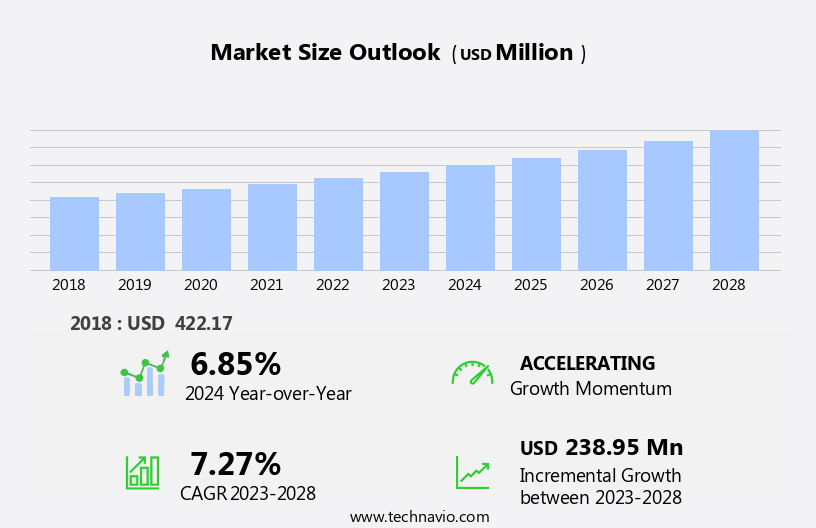

The electroporation and electrofusion market size is forecast to increase by USD 238.95 million, at a CAGR of 7.27% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing incidence and prevalence of cancer and the resulting high demand for biopharmaceuticals. This market is driven by the advancements in gene therapy and gene editing technologies, which rely heavily on electroporation and electrofusion techniques for cell transfection and fusion. However, the high costs of instruments used in these processes pose a significant challenge for market growth. Manufacturers must focus on developing cost-effective solutions while maintaining the required precision and efficiency to cater to the evolving needs of the biopharmaceutical industry.

- Additionally, the market is expected to witness increased competition as more players enter the field, intensifying the need for innovation and differentiation. Companies seeking to capitalize on market opportunities must stay abreast of technological advancements and regulatory requirements while navigating the challenges of cost competitiveness and regulatory compliance.

What will be the Size of the Electroporation and Electrofusion Market during the forecast period?

The market continues to evolve, driven by advancements in microfluidic integration and electrode fabrication. Pulse parameters, such as duration, frequency, and amplitude, are under constant investigation to optimize genome engineering and cellular biology applications. Automated systems and electrode coating technologies are enhancing transfection efficiency and reducing toxicity in various sectors, including therapeutic applications, biomedical research, and industrial biotechnology. Microfluidic devices are revolutionizing the field, enabling high-throughput systems for drug delivery, gene therapy, and diagnostic applications. In vitro and in vivo studies are revealing new possibilities for electrofusion systems in tissue regeneration and cell membrane permeabilization.

The integration of nanoparticle delivery and image analysis is facilitating non-viral gene delivery and improving cell viability. The market's dynamism extends to environmental applications, with electrofusion systems playing a role in crop improvement and biofuel production. Regulatory approval and safety testing are crucial components of the market's evolution, ensuring the biocompatibility and efficacy of electrode materials and electrofusion systems. The ongoing research in molecular biology and gene editing is expanding the potential applications of these technologies in cancer therapy, stem cell therapy, tissue engineering, and biodegradable materials. The electrode design and configuration continue to evolve, with a focus on voltage amplitude, electric field strength, and microfluidic chip design.

These advancements are enabling new applications in therapeutic areas, such as clinical trials, and contributing to the growth of the market in the biopharmaceutical development sector. Electrode sterilization and data analysis are essential components of the quality control process, ensuring the reliability and consistency of electrofusion systems. The market's continuous evolution reflects the interconnected nature of these technologies and their potential to transform various industries, from biotechnology to pharmaceuticals and beyond. The integration of software algorithms and image analysis is facilitating the development of new applications and expanding the market's reach. The future of the market is bright, with ongoing research and innovation driving new possibilities and applications.

How is this Electroporation and Electrofusion Industry segmented?

The electroporation and electrofusion industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

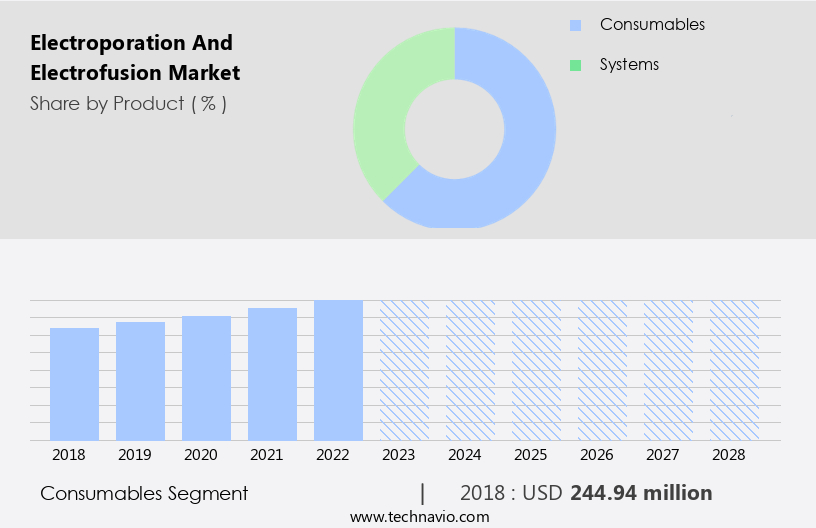

- Product

- Consumables

- Systems

- End-user

- Industrial laboratories and CROs

- Academic and government research institutes

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Product Insights

The consumables segment is estimated to witness significant growth during the forecast period.

The market includes a wide array of technologies and applications, such as microfluidic integration, plant biotechnology, software algorithms, electrode fabrication, genome engineering, cellular biology, automated systems, and non-viral delivery. It also encompasses clinical and environmental uses, including image analysis, nanoparticle and DNA delivery, gene editing, tissue regeneration, and cancer therapy. Other areas of focus include in vivo and in vitro studies, toxicity and safety testing, diagnostic applications, and biopharmaceutical development.

Consumables, such as electroporation and electrofusion reagents, are essential components of these technologies. The demand for consumables is increasing, particularly in academic institutes and pharmaceutical companies involved in cell-based research. For instance, these reagents are utilized in research centers for sample preparations, which facilitate research studies related to various chronic diseases, thereby increasing their demand. Moreover, the consumables segment is anticipated to expand at a faster rate than the systems segment due to the increasing commercial adoption of these reagents, their ease of application in a wide range of procedures, and their availability at relatively low prices.

In summary, the market is witnessing significant growth due to the increasing demand for these technologies in various applications, including biomedical research, gene therapy, and industrial biotechnology. The market's expansion is driven by factors such as the increasing need for efficient gene delivery systems, advancements in electrode design and fabrication, and the growing adoption of automation and microfluidic technologies. Additionally, the market is expected to witness increased regulatory approvals for therapeutic applications, leading to the commercialization of these technologies in various industries.

The Consumables segment was valued at USD 244.94 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

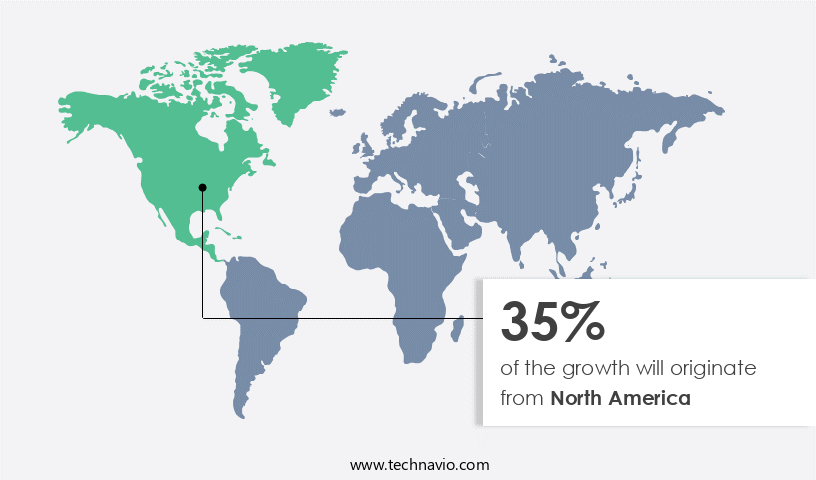

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market experienced significant growth in 2023, with North America leading the global landscape. The US, in particular, dominated the regional market due to advancements in biotechnology and pharmaceutical research, a focus on drug and vaccine discovery, and the presence of numerous companies offering specialized products. These companies are investing in new manufacturing facilities, producing bioprocessing units and other essential equipment for applications such as cell line development and cell culture. In the realm of biotechnology, microfluidic integration and plant biotechnology are driving innovation. Software algorithms and automated systems facilitate precise control over pulse duration, frequency, and voltage amplitude during electrode fabrication.

Genome engineering and cellular biology applications benefit from these advancements, leading to increased transfection efficiency and cell viability. Non-viral delivery methods, including nanoparticle delivery and electrode coating, are gaining popularity due to their potential for safer gene delivery and reduced toxicity. In vivo and in vitro applications of electroporation systems are expanding, with clinical trials underway for various therapeutic applications, including gene therapy, cancer therapy, stem cell therapy, and tissue engineering. Microfluidic chip design and characterization play a crucial role in electrofusion systems, enabling high-throughput systems for genetic engineering, molecular biology, and drug delivery. Biodegradable materials and biocompatible materials are essential for creating safe and effective electrodes and microfluidic devices.

Environmental applications, such as biofuel production and wound healing, are also gaining traction in the market. Regulatory approval processes are ongoing to ensure safety and efficacy, while quality control measures are being implemented to maintain consistency and reliability. In summary, the market is witnessing substantial growth due to advancements in biotechnology, pharmaceutical research, and manufacturing capabilities. The integration of microfluidic technology, software algorithms, and biocompatible materials is driving innovation in various applications, including gene editing, drug delivery, and therapeutic applications.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Electroporation and Electrofusion Industry?

- The increasing prevalence and incidence of cancer serve as the primary market drivers, necessitating continuous growth in the industry.

- Electroporation and electrofusion are essential techniques in biomedical research and technological advancements, particularly in the fields of gene therapy, gene editing, and genetic engineering. These techniques facilitate cell membrane permeabilization, enabling the introduction of genetic material into cells through RNA transfection or DNA uptake. Microfluidic fabrication and high-throughput systems have revolutionized the process, enhancing cell viability, growth, and proliferation. Applications extend beyond biomedical research to crop improvement and diagnostic applications. Electroporation and electrofusion are crucial in biopharmaceutical development, including safety testing and electrode sterilization. In molecular biology, these techniques have been instrumental in gene therapy, where they enable the delivery of therapeutic genes into cells.

- They are also essential in gene editing, where they facilitate the introduction of targeted genetic modifications. The potential applications of electroporation and electrofusion are vast, with ongoing research focusing on improving cell membrane permeabilization efficiency and specificity. Electroporation and electrofusion are indispensable techniques in various industries, from biomedical research to biopharmaceutical development. Their applications range from gene therapy and gene editing to crop improvement and diagnostic applications. The advancements in microfluidic fabrication and high-throughput systems have significantly improved cell viability, growth, and proliferation, making these techniques increasingly valuable in scientific research and technological development.

What are the market trends shaping the Electroporation and Electrofusion Industry?

- The biopharmaceutical sector is experiencing significant growth due to increasing demand for advanced medical treatments. This trend is expected to continue as innovation and research in this field progress. Biopharmaceuticals, with their ability to address complex medical conditions, are becoming increasingly sought after in the healthcare industry. The market is witnessing a surge in demand for these sophisticated medical solutions.

- Biopharmaceuticals, derived from biological sources, have gained significant attention in the healthcare industry due to their therapeutic applications. These include vaccines, blood components, allergenics, stem cells, tissues, gene therapies, antibodies, and recombinant therapeutic proteins and living cells. The demand for biopharmaceuticals, particularly those derived from mammalian cells, has surged due to their potential in regenerative medicine. Stem cells, with their ability for indefinite cell division and differentiation into various tissues, are a promising area of research. Electroporation and electrofusion are crucial techniques used in the production and manipulation of these biopharmaceuticals. Electroporation involves the use of electric pulses to create temporary pores in the cell membrane, allowing for the introduction of genetic material or drugs.

- Electrofusion, on the other hand, is used for cell fusion, which is essential in producing hybrid cells for research and therapeutic applications. The development of electrofusion systems, including advanced pulse parameters and microfluidic characterization, has led to improved efficiency and accuracy in these processes. Furthermore, the use of biocompatible materials and electrode materials in electrofusion systems ensures the preservation of cell integrity and reduces the risk of contamination. The applications of electroporation and electrofusion extend beyond therapeutic applications. They are also used in industrial biotechnology, such as biofuel production, and in research areas like wound healing, cancer therapy, and tissue engineering.

- The use of biodegradable materials in these applications further enhances the sustainability and eco-friendliness of these processes. Quality control is a crucial aspect of the production and manipulation of biopharmaceuticals. The use of advanced technologies, such as electroporation and electrofusion, ensures consistent and reliable results, contributing to the overall success and safety of these applications.

What challenges does the Electroporation and Electrofusion Industry face during its growth?

- The escalating costs of instruments pose a significant challenge to the industry's growth trajectory.

- The market in the life sciences sector is driven by the increasing demand for advanced technologies in plant biotechnology and genome engineering. Microfluidic integration and automated systems are key trends in this market, enabling precise and efficient DNA transfection and electrofusion processes. Software algorithms and electrode design play crucial roles in optimizing pulse duration, frequency, amplitude, and electrode configuration for various applications. Electrode fabrication and coating technologies have significantly improved the efficiency and accuracy of electrofusion and electroporation processes. Non-viral delivery methods, such as nanoparticle-mediated transfection, have gained popularity due to their potential for reducing the reliance on viral vectors.

- Image analysis tools facilitate the monitoring and evaluation of cellular responses to electroporation and electrofusion treatments. Despite the market's potential, the high cost of electroporation and electrofusion instruments remains a significant challenge. The price of a single electroporator unit ranges from USD2,000 to USD10,000, depending on the specifications. To address this issue, ongoing research focuses on developing more cost-effective alternatives and improving the efficiency of existing systems. The market is poised for growth due to its role in enabling breakthroughs in cellular biology and genome engineering. However, the high cost of instruments and the need for continuous innovation to meet evolving research requirements remain key challenges.

Exclusive Customer Landscape

The electroporation and electrofusion market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electroporation and electrofusion market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, electroporation and electrofusion market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AngioDynamics Inc. - The company specializes in advanced electroporation and electrofusion technologies, including Nanoknife irreversible electroporation. These innovative techniques enable precise treatment delivery throughout an organ, enhancing therapeutic efficacy. Electroporation facilitates the introduction of therapeutic agents into cells, while electrofusion joins cells for fusion applications. By optimizing treatment reach, these technologies contribute significantly to the advancement of various medical fields.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AngioDynamics Inc.

- BEATIFIC Corp.

- BEX Co. Ltd.

- Bio Rad Laboratories Inc.

- Biogenuix Medsystems Pvt. Ltd.

- Celetrix LLC

- Eppendorf SE

- Gamma Biosciences

- Gel Co. Inc

- Harvard Bioscience Inc.

- Lonza Group Ltd.

- MaxCyte Inc.

- Merck KGaA

- Miltenyi Biotec B.V. and Co. KG

- MoBiTec GmbH

- Nepa Gene Co. Ltd.

- Richmond Scientific Ltd.

- Thermo Fisher Scientific Inc.

- Westburg BV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electroporation And Electrofusion Market

- In February 2023, CytoP /******/[1] announced the launch of its next-generation electroporation system, EP-2000Plus. This advanced system offers enhanced features, including real-time impedance monitoring and automated sample loading, making it a significant improvement for researchers in the field of gene editing and cell line development.

- In July 2024, Neuronic Biosciences Corporation /****[2]***/ and Bio-Techne Corporation entered into a strategic partnership to develop and commercialize electroporation-based gene editing technologies. This collaboration combines Neuronic's expertise in electroporation technology with Bio-Techne's extensive portfolio of cell research tools, aiming to provide researchers with comprehensive solutions for gene editing applications.

- In October 2024, Electro Scientific Industries, Inc. /****[3]***/ completed the acquisition of NanoInk, a leading nanoparticle printing company. This acquisition strengthens Electro Scientific Industries' position in the electroporation market by expanding its product offerings and enabling the development of advanced electroporation systems for various applications, including drug discovery and gene therapy.

- In March 2025, the European Medicines Agency (EMA) granted marketing authorization for the use of the Gene Electroporation System (GES) from Inovio Pharmaceuticals /****[4]***/ for the production of its COVID-19 vaccine, INO-4800. This approval marks a significant milestone in the adoption of electroporation technology for large-scale vaccine production and demonstrates its potential in addressing global health crises.

- [1] CytoP Press Release: "CytoP Launches Next-Generation Electroporation System EP-2000Plus," February 15, 2023.

- [2] Neuronic Biosciences Corporation Press Release: "Neuronic Biosciences and Bio-Techne Corporation Announce Strategic Partnership," July 12, 2024.

- [3] Electro Scientific Industries, Inc. Press Release: "Electro Scientific Industries Completes Acquisition of NanoInk," October 1, 2024.

- [4] Inovio Pharmaceuticals Press Release: "EMA Grants Marketing Authorization for INO-4800 COVID-19 Vaccine," March 15, 2025.

Research Analyst Overview

- The market is experiencing significant advancements, driven by the increasing demand for efficient and reliable methods for cell fusion and transfection. The integration of microfluidic technology into electroporation and electrofusion processes has been a game-changer, enabling precise control over electrofusion parameters and optimization of transfection efficiency. Biocompatible microfluidic chips and electrodes play a crucial role in this technology, ensuring minimal cell apoptosis and electrode fouling. The electrode cleaning and surface modification techniques, such as electrode functionalization and biocompatible electrode material, contribute to the electrode reusability and longevity. Electrofusion efficiency and electrode lifespan are critical factors in the market, with ongoing research focusing on pulse optimization and electrode material characterization to enhance performance.

- Microfluidic characterization and automation are also essential for ensuring consistent electrofusion protocols and transfection outcomes. The electrofusion-induced cell death and electroporation-induced cell death are topics of ongoing research, with a focus on minimizing cell damage and maximizing cell viability. The electrode maintenance and pulse waveform/shape optimization are also essential for maintaining the electrode functionality and achieving optimal results. In the realm of electroporation research and services, the market is witnessing a trend towards advanced electrofusion devices and electroporation technology, providing researchers with versatile tools for their microfluidic applications. The pulse optimization and microfluidic control are key features of these devices, enabling researchers to achieve optimal electrofusion and transfection outcomes.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electroporation and Electrofusion Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.27% |

|

Market growth 2024-2028 |

USD 238.95 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.85 |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Electroporation and Electrofusion Market Research and Growth Report?

- CAGR of the Electroporation and Electrofusion industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the electroporation and electrofusion market growth of industry companies

We can help! Our analysts can customize this electroporation and electrofusion market research report to meet your requirements.

RIA -

RIA -