Europe Automotive Financing Market Size 2024-2028

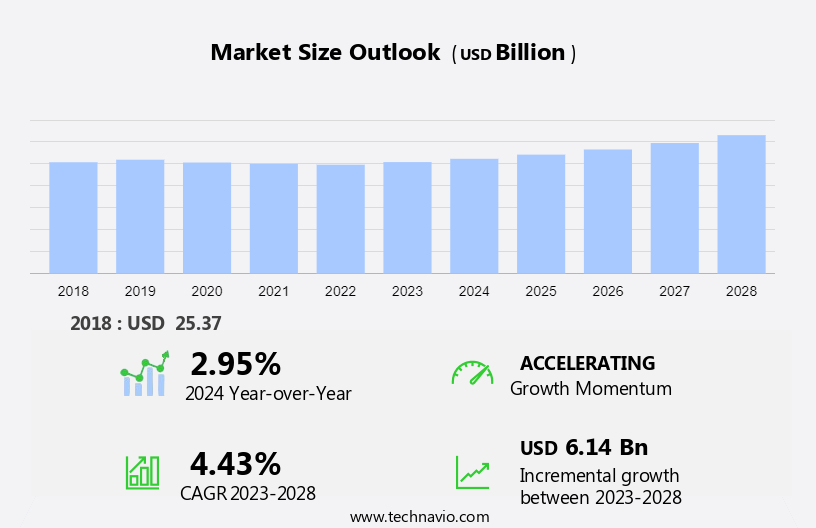

The Europe automotive financing market size is forecast to increase by USD 6.14 billion at a CAGR of 4.43% between 2023 and 2028. The European automotive financing market is witnessing significant growth, driven by the increasing demand for financing options for commercial vehicles and electric vehicles (EVs). Telematics technology and digital tools are revolutionizing the financing landscape, enabling real-time vehicle monitoring and customized financing solutions. Digital payment systems, such as mobile banking, are gaining popularity, offering convenience and security to customers. Further, the market is witnessing a shift towards digitalization, with the adoption of digital tools and loan services becoming increasingly common. The emergence of autonomous vehicles and the growth of ride-hailing and car-sharing services are also impacting the market dynamics. The rise of car-sharing and ride-hailing services is also fueling market growth, as these platforms require flexible financing arrangements. However, the increasing use of public transport due to environmental concerns poses a challenge to the market. In the US market, similar trends are emerging, with the demand for financing solutions for commercial vehicles and EVs on the rise. The integration of telematics and digital tools, as well as the adoption of digital payment systems, is transforming the financing landscape. Car-sharing and ride-hailing services are also driving market growth, offering flexible financing options to meet the unique needs of these businesses.

The European automotive financing market is witnessing significant advancements, driven by the integration of innovative technologies such as electric vehicles (EVs), captive finance, and digitalization. These trends are transforming the way financial institutions provide loan services for new and used passenger cars. Captive finance, a financing arm of an Original Equipment Manufacturer (OEM), plays a crucial role in the European automotive financing market. It offers personalized finance options to customers, ensuring a seamless buying experience. This financing model allows OEMs to have more control over the sales process and customer relationships. The digitization of captive automotive finance is transforming car finance options for hybrid purchasers and those interested in battery electric vehicles, enabling seamless access to innovative automotive technology for new vehicles.

OEM warranty programs are also being integrated into financing packages to provide additional value to customers. Interest rates remain a critical factor in the European automotive financing market. The European Central Bank's monetary policy influences interest rates, which can impact the affordability of car loans. However, the ongoing digitalization trend is expected to lead to increased competition and potentially lower interest rates. Leasing suppliers are also playing a significant role in the European automotive financing market. They offer flexible lease terms, maintenance services, and attractive financing options to attract customers. This can put pressure on traditional financial institutions to adapt and offer competitive lease options. In conclusion, the European automotive financing market is undergoing significant changes, driven by the integration of innovative technologies and alternative ownership models. Financial institutions must adapt to these trends to remain competitive and offer personalized finance options to meet the evolving needs of European consumers.

Market Segmentation

The market forecast research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Used vehicle

- New vehicle

- Type

- Passenger vehicle

- Commercial vehicle

- Geography

- Europe

- Germany

- UK

- France

- Italy

- Europe

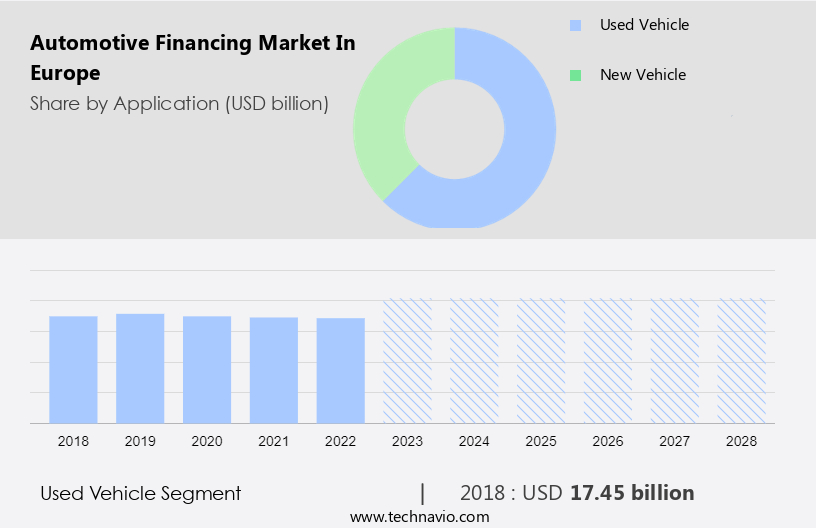

By Application Insights

The used vehicle segment is estimated to witness significant growth during the forecast period. In Europe, the automotive financing market has experienced growth due to the increasing preference for used vehicles among customers. The trend of upgrading cars every few years has driven this market forward. Used cars offer significant cost savings compared to new ones, making them an attractive option for many consumers.

Moreover, some European countries have registration fee structures that decrease significantly for vehicles that are a few years old. This can result in substantial savings for customers purchasing slightly used passenger cars. Financial institutions cater to this demand by offering various financing options for used vehicles. The automotive loans market in Europe has seen digitalization with the advent of subscription-based models and online applications. Vehicle maintenance is another crucial factor influencing the automotive financing market, as many financial institutions offer maintenance packages as part of their financing deals.

Get a glance at the market share of various segments Request Free Sample

The used vehicle segment accounted for USD 17.45 billion in 2018 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The rise in cab service financing is the key driver of the market. In Europe, the increasing popularity of electric vehicles (EVs) has led to a significant shift in the automotive financing market. Captive finance companies, which are subsidiaries of automakers, are offering personalized finance options for EV buyers. These financing programs provide flexible repayment terms and customized deals to attract customers. Moreover, the integration of advanced technologies like AI technology, cryptocurrency, and blockchain in automotive financing is revolutionizing the industry. Credit underwriting processes are becoming more efficient and transparent, making it easier for individuals to secure financing.

For those aspiring to become cab drivers, these financing programs offer a viable solution. Despite the high upfront cost of purchasing a new EV, these financing options enable them to overcome financial barriers and join the growing ride-hailing industry. Overall, the market is evolving to cater to the changing needs of consumers and the emerging trends in the transportation sector.

Market Trends

The rise in demand for EVs is the upcoming trend in the market. In Europe, the automotive financing market is witnessing significant advancements with the increasing popularity of Electric Vehicles (EVs). These vehicles, which can be charged using external sources of electricity, contribute to reduced air pollution and, when charged using renewable energy, result in a decrease in greenhouse gases. European governments are incentivizing EV purchases through tax rebates and subsidies. For instance, the French government offers cash incentives ranging from USD 5,000 to USD 7,000 to buyers of EVs.

Moreover, the automotive financing sector in Europe is being transformed by digital tools and financing options. Telematics, digital payment systems, mobile banking, and car-sharing services are becoming increasingly common. ide-hailing services, such as Uber and Lyft, are also gaining popularity, leading to new financing models. These trends are expected to continue, shaping the future of automotive financing in Europe.

Market Challenge

Growing use of public transport due to an increase in air pollution is a key challenge affecting the market growth. In Europe, the automotive financing market encompasses various financing options for both commercial and passenger vehicles. These financing methods include direct financing from Original Equipment Manufacturers (OEMs) and indirect financing through banks and leasing companies. Direct financing allows buyers to obtain loans directly from the vehicle manufacturer, while indirect financing involves obtaining loans through banks or leasing companies. The European automotive industry has experienced significant growth in recent years, particularly in the commercial vehicle and passenger vehicle segments. This expansion has resulted in increased air pollution levels, primarily due to the rise in the number of vehicles on the road.

As the European automotive industry continues to evolve, the financing market will play a crucial role in facilitating the transition towards sustainable transportation. In conclusion, the European automotive financing market is an essential component of the industry's growth, particularly in the context of the increasing demand for eco-friendly vehicles. Banks, OEMs, and leasing companies are offering various financing solutions to cater to this demand, making it easier for consumers to make the switch to more sustainable transportation options. The future of the European automotive industry lies in its ability to adapt to the changing regulatory landscape and consumer preferences, and the financing market will be a key player in this transition.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

ALPHERA Financial Services - The company offers automotive financing solutions at the point-of-sale and directly to consumers.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bank of America Corp.

- Bayerische Motoren Werke AG

- Blue Motor Finance Ltd.

- Capital One Financial Corp.

- Credit Agricole SA

- ESKA Finance s.r.o.

- First Response Finance Ltd.

- Ford Motor Co.

- Honda Motor Co. Ltd.

- JPMorgan Chase and Co.

- Mercedes Benz Group AG

- NatWest Group plc

- Porsche Automobil Holding SE

- Startline Motor Finance Ltd.

- Sumitomo Corp.

- Toyota Motor Corp.

- Wells Fargo and Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The European automotive financing market is witnessing significant changes due to the integration of advanced technologies such as electric vehicles (EVs), captive finance, and digitalization. Captive finance, a financing solution provided directly by Original Equipment Manufacturers (OEMs), is becoming increasingly popular among consumers seeking personalized finance options. The rise of EVs is driving the demand for new financing solutions, including loans and leasing for both passenger and commercial vehicles. Banks and financial institutions are collaborating with OEMs to offer direct and indirect financing options. The use of artificial intelligence (AI) technology in credit underwriting and telematics is streamlining the financing process and providing more accurate risk assessments.

Additionally, digital payment systems, mobile banking, and car-sharing platforms are also gaining traction in the market. The fragmented market includes various financing options such as automotive refinancing, subscription-based models, and car rental. The integration of blockchain and cryptocurrency in automotive finance is expected to provide more secure and transparent transactions. Digital automotive finance is also gaining popularity, with virtual dealerships and car dealership buyback programs offering convenience and flexibility to consumers. Interest rates, sales rebound, and safety systems are key factors influencing the European automotive financing market. OEM warranty programs and monthly loan payments are also important considerations for consumers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

152 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.43% |

|

Market growth 2024-2028 |

USD 6.14 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.95 |

|

Key companies profiled |

ALPHERA Financial Services, Banco Santander SA, Bank of America Corp., Bayerische Motoren Werke AG, Blue Motor Finance Ltd., Capital One Financial Corp., Credit Agricole SA, ESKA Finance s.r.o., First Response Finance Ltd., Ford Motor Co., Honda Motor Co. Ltd., JPMorgan Chase and Co., Mercedes Benz Group AG, NatWest Group plc, Porsche Automobil Holding SE, Startline Motor Finance Ltd., Sumitomo Corp., Toyota Motor Corp., and Wells Fargo and Co. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles,market forecast , fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -