Europe Electric Motors for Electric Vehicle Market Size 2024-2028

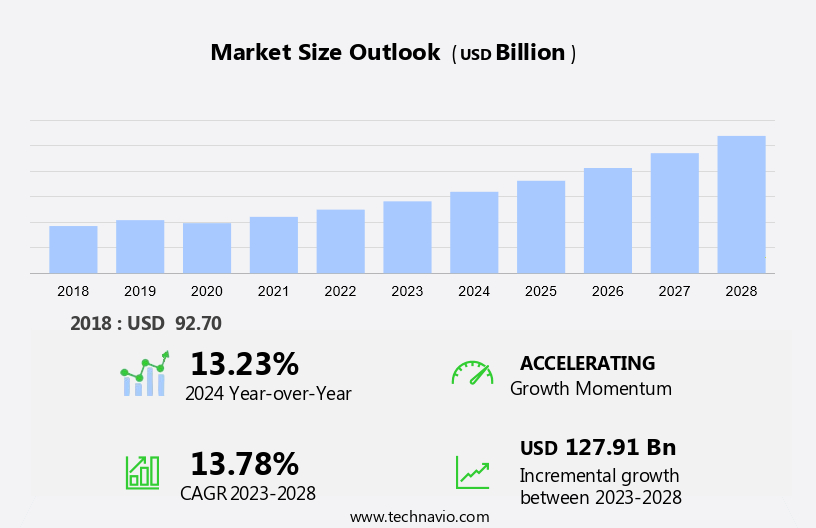

The Europe electric motors for EV market size is forecast to increase by USD 127.91 billion at a CAGR of 13.78% between 2023 and 2028.

- The electric vehicle (EV) market in Europe is experiencing significant growth due to the increasing demand for sustainable transportation solutions. One of the key driving factors is the growing awareness and adoption of EVs to reduce carbon emissions and combat climate change. Another trend influencing the market is the rise of Silicon Carbide inverters, which are increasingly being used in electric motors for EVs to enhance efficiency and reduce energy losses.

- However, the market faces challenges such as raw material scarcity and price volatility associated with the manufacturing of electric motors for EVs. The scarcity of neodymium and dysprosium, key components in the production of permanent magnets used in electric motors, can impact the cost and availability of EVs. Therefore, the market is witnessing ongoing research and development efforts to explore alternative materials and manufacturing processes to mitigate these challenges.

Europe Electric Motors for Electric Vehicle Market Analysis

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Application

- Passenger vehicle

- Commercial vehicle

- Type

- AC motor

- DC motor

- Geography

- Europe

- Germany

- UK

- France

- Italy

- Europe

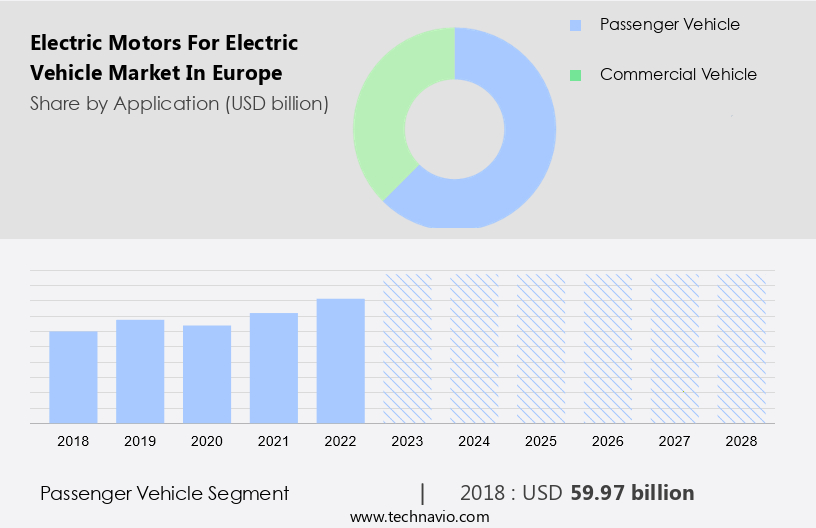

By Application Insights

The passenger vehicle segment is estimated to witness significant growth during the forecast period. The European electric vehicle market is experiencing significant growth due to increasing concerns over environmental issues, including air pollution and climate change. Governments across Europe are offering incentives such as tax credits, subsidies, and reduced registration fees to promote the adoption of electric passenger vehicles. These initiatives aim to mitigate the environmental impact of traditional vehicles and reduce dependence on fossil fuels. Advancements in electric motor technology, energy storage, and efficiency have led to lower battery costs, making electric vehicles (EVs) more affordable for consumers. The smaller carbon impact, cheaper operating costs, less maintenance, and performance parity with conventional vehicles are further driving demand.

Global automakers are responding by introducing more electric models, addressing concerns over range anxiety through improved charging infrastructure and longer driving ranges. Despite the high initial costs, consumer spending power, investment decisions, and innovative mobility solutions are enabling the mass adoption of electric vehicles. Challenges such as performance issues, dependability, worker skills, manufacturing procedures, infrastructure adaptation, and consumer knowledge are being addressed through continuous innovation and collaboration between industry stakeholders. Overall, the European electric vehicle market is poised for growth, with a focus on enhancing vehicle performance, overall efficiency, and consumer appeal.

Get a glance at the market share of various segments Request Free Sample

The passenger vehicle segment accounted for USD 59.97 billion in 2018 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Dynamics

- Electric motors have become a pivotal component in the rapidly growing electric vehicle (EV) market in Europe. The increasing concern towards environmental issues, such as air pollution and climate change, has led to the adoption of EVs as a viable alternative to traditional internal combustion engine vehicles. European governments offer tax credits and subsidies to incentivize the purchase of EVs, making them more affordable for consumers. The advancements in electric motor technology have led to improvements in power density, energy storage system, and efficiency. Lower battery costs have also contributed to the affordability of EVs, making them a more viable option for consumers.

- The smaller carbon impact of EVs is a significant factor in their increasing popularity. Global automakers are investing heavily in the development and production of EVs with electric motors. The cheaper operating costs and less maintenance required for EVs compared to traditional vehicles make them an attractive option for consumers. The European EV market is expected to grow significantly in the coming years, driven by the increasing availability of affordable EVs and the growing concern towards environmental issues

What are the key market drivers leading to the rise in adoption of Europe Electric Motors ?

Growing demand for EVs in Europe is the key driver of the market.

- In Europe, the market for electric vehicles (EVs) is experiencing significant growth, driven by various factors such as environmental concerns, pollution requirements, and fuel price trends.Governments in Europe have implemented tax credits and subsidies to incentivize the adoption of EVs, addressing both consumer spending power and the high initial costs associated with these vehicles. As a result, countries like Germany, the UK, Norway, the Netherlands, France, and Sweden have seen a increase in electric motor sales. In 2023, Germany sold approximately 5 million full electric cars, leading the market in Europe. The UK's electric vehicle fleet is also expanding rapidly due to increasing customer demand and improved availability of electric models.

- Environmental issues, including air pollution and climate change, are significant concerns in Europe, leading to stricter pollution regulations. This, coupled with the lower operating costs, less maintenance, and smaller carbon impact of EVs, make them an attractive alternative to traditional internal combustion engine vehicles. The innovation in mobility solutions, such as charging infrastructure, is addressing range anxiety concerns, further increasing the appeal of EVs. However, challenges remain, including the need for larger capacity batteries, infrastructure adaptation, and the development of more affordable electric vehicles with better performance and dependability. Worker skills and manufacturing procedures are also essential considerations in the growth of the electric motor market for EVs in Europe.

Overall, the efficiency, power density, and energy storage capabilities of electric motors continue to improve, making them a viable and increasingly popular choice for European consumers.

What are the trends shaping the Europe Electric Motors ?

Rise of SiC inverters to increase efficiency of electric motors for EVs is the upcoming trend in the market.

- Electric motors, a crucial component of electric vehicles (EVs) in Europe, are experiencing significant advancements, particularly with the adoption of Silicon Carbide (SiC) inverters. SiC, a semiconductor material with superior thermal conductivity and power-handling capabilities, enhances electric motor efficiency by reducing power losses during energy conversion. This leads to improved performance, energy density, and extended driving range for EVs, addressing consumer concerns and boosting acceptance. SiC inverters also enable faster charging speeds, addressing range anxiety and charging time concerns. These technological advancements contribute to the overall efficiency of electric vehicles, making them a more affordable and viable alternative to traditional gasoline-powered vehicles.

- Additionally, environmental issues, such as air pollution and climate change, are driving the demand for electric vehicles in Europe. Governments offer tax credits and subsidies to incentivize the adoption of EVs, making them more accessible to consumers. However, high initial costs, lack of charging infrastructure, and consumer spending power influence investment decisions. Innovative mobility solutions and infrastructure adaptation are necessary to overcome these challenges and ensure the success of the electric vehicle market in Europe.

What challenges does Europe Electric Motors face during the growth?

Raw material scarcity and price volatility associated with manufacturing of electric motors for EVs are key challenges affecting the market growth.

- Electric motors play a pivotal role in the electric vehicle (EV) market in Europe, with tax credits and subsidies driving demand for affordable electric models. However, environmental issues, including air pollution and climate change, are major factors propelling the shift towards EVs. Power density and energy storage efficiency are crucial considerations, as are lower battery costs and cheaper operating costs, which offer less maintenance and smaller carbon impacts. Global automakers are investing in electric models to meet pollution requirements and address fuel price volatility, while innovative mobility solutions mitigate range anxiety concerns. Despite these advantages, the electric motor industry faces challenges, such as high initial costs, large-capacity battery production, and a lack of consumer knowledge.

- Performance issues and dependability concerns necessitate ongoing research and development, as well as the acquisition of new worker skills and adaptation of manufacturing procedures. Infrastructure adaptation, including electric charging infrastructure expansion, is also essential to address consumer spending power and investment decisions. The production of electric motors relies on key materials like rare-earth elements (REEs), copper, and aluminum, making the industry susceptible to supply chain disruptions and price fluctuations. Geopolitical tensions, such as the Russia-Ukraine war, add complexity, with Russia being a major supplier of critical raw materials like REEs. These disruptions can impact production volumes and increase material costs, particularly for rare-earth magnets containing neodymium and dysprosium, and copper and aluminum essential for winding and housing components.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

ABB Ltd. - The company offers advanced electric motor solutions for various EV models, including the BMW Externally Excited Synchronous Motor, or EESM.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMETEK Inc.

- Bayerische Motoren Werke AG

- BorgWarner Inc.

- Continental AG

- DENSO Corp.

- GEM motors d.o.o

- Hitachi Ltd.

- Magna International Inc.

- Mitsubishi Electric Corp.

- Nidec Corp.

- Robert Bosch GmbH

- Siemens AG

- Tesla Inc.

- Toshiba Corp.

- Valeo SA

- Ford Motor Co.

- General Motors Co.

- Renault SAS

- Volkswagen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Electric motors have become a pivotal component in the shift towards sustainable transportation, particularly in Europe where environmental issues, air pollution, and climate change concerns have fueled the demand for electric vehicles (EVs). Governments across Europe have introduced tax credits and subsidies to incentivize the adoption of EVs, making them more affordable for consumers. Power density and energy storage efficiency are key considerations for electric motor manufacturers, as larger capacity batteries are required to increase the range of EVs. Lower battery costs have also played a significant role in making EVs more accessible to consumers, leading to cheaper operating costs, less maintenance, and a smaller carbon impact.

Global automakers are investing heavily in electric models to meet stricter pollution requirements and rising fuel prices. However, range anxiety concerns and the lack of charging infrastructure continue to be challenges for the EV market. Innovative mobility solutions, such as car-sharing and ride-hailing services, are also gaining popularity. The high initial costs of EVs and performance issues, including dependability and worker skills required for manufacturing procedures, remain obstacles. Infrastructure adaptation and investment decisions are also crucial factors, as the EV market continues to evolve. Consumer spending power and overall efficiency will continue to influence the market's growth.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

159 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.78% |

|

Market growth 2024-2028 |

USD 127.91 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

13.23 |

|

Key companies profiled |

ABB Ltd., AMETEK Inc., Bayerische Motoren Werke AG, BorgWarner Inc., Continental AG, DENSO Corp., GEM motors d.o.o, Hitachi Ltd., Magna International Inc., Mitsubishi Electric Corp., Nidec Corp., Robert Bosch GmbH, Siemens AG, Tesla Inc., Toshiba Corp., Valeo SA, Ford Motor Co., General Motors Co., Renault SAS, and Volkswagen AG |

|

Market dynamics |

Parent market analysis, market forecast , market growth inducers and obstacles,market forecast , fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -