North America Facility Management Services Market Size 2026-2030

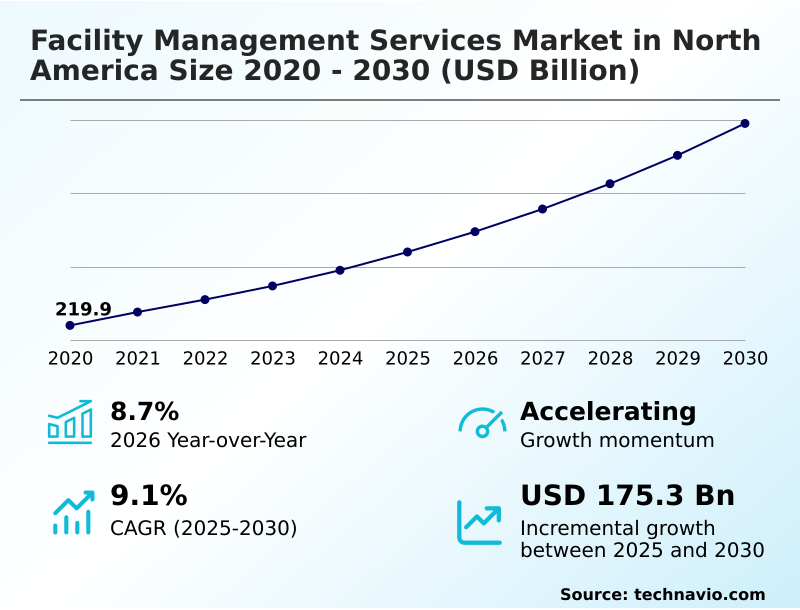

The north america facility management services market size is valued to increase by USD 175.3 billion, at a CAGR of 9.1% from 2025 to 2030. Rapid adoption of AI and ML for predictive maintenance will drive the north america facility management services market.

Major Market Trends & Insights

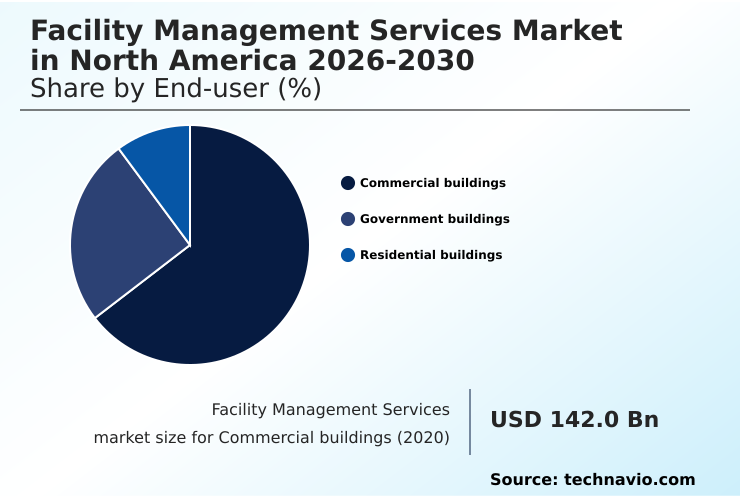

- By End-user - Commercial buildings segment was valued at USD 191.9 billion in 2024

- By Service - Soft services segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 275.4 billion

- Market Future Opportunities: USD 175.3 billion

- CAGR from 2025 to 2030 : 9.1%

Market Summary

- The facility management services market in North America is undergoing a significant transformation, driven by technological innovation and evolving business needs. This shift moves beyond simple maintenance to encompass strategic asset lifecycle management and the enhancement of the workplace experience.

- Key trends include the adoption of digital twin technology for virtual asset management and the consolidation of services under an integrated facility management model. These advancements enable data-driven decisions that improve operational efficiency and occupant comfort.

- For instance, a large corporate campus can leverage an integrated workplace management system to analyze space utilization data, leading to optimized layouts that support both collaborative and individual work styles while also reducing energy consumption. However, the industry faces challenges such as the widening skills gap for technologically advanced roles and the cybersecurity risks associated with increasingly connected buildings.

- Addressing these issues through targeted training and robust security protocols is crucial for service providers to deliver value and maintain a competitive edge in this dynamic market.

What will be the Size of the North America Facility Management Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the North America Facility Management Services Market Segmented?

The north america facility management services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

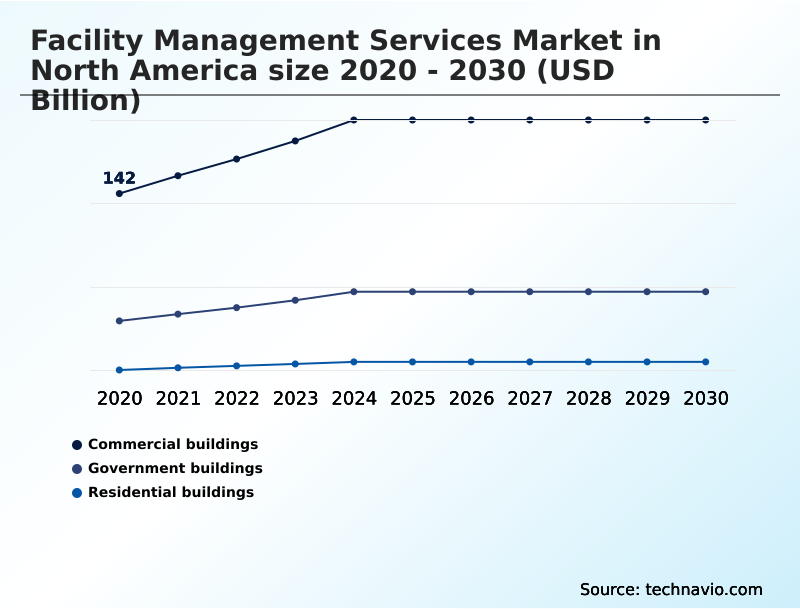

- Commercial buildings

- Government buildings

- Residential buildings

- Service

- Soft services

- Hard services

- Type

- Fixed-term

- On-demand

- Geography

- North America

- US

- Canada

- Mexico

- North America

By End-user Insights

The commercial buildings segment is estimated to witness significant growth during the forecast period.

The commercial buildings segment is shifting beyond traditional operations to create human-centric environments. This pivot is driven by the need to support hybrid work model support and enhance workplace experience through superior soft services and hard services.

Facility management providers are leveraging proptech solutions and IoT for building management to optimize space utilization and asset lifecycle management, with some achieving a 15% improvement in work order processing efficiency.

The focus on decarbonization services and implementing an integrated FM model is critical for corporate sustainability goals.

These changes reflect a move toward creating intelligent, responsive buildings that align with environmental, social, and governance objectives, making sustainable facility practices a cornerstone of modern property management and real estate portfolio management.

The Commercial buildings segment was valued at USD 191.9 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The facility management services market in North America is increasingly complex, demanding a strategic approach to service delivery. Understanding the cost of predictive maintenance implementation is crucial for organizations weighing the long-term benefits of asset longevity against initial capital outlay.

- The benefits of integrated facility management are compelling, offering streamlined operations and a single point of accountability, which can reduce administrative overhead by more than 15% compared to managing multiple vendors. However, this model raises questions about service provider consolidation trends and how to maintain competitive pricing.

- A key consideration is navigating cybersecurity best practices for smart buildings, as interconnected systems create new vulnerabilities. The ROI of digital twin technology is a major discussion point, as it enables advanced simulations for capital planning. Similarly, firms explore how AI improves work order processing, automating dispatch and diagnostics.

- The impact of hybrid work on soft services necessitates a re-evaluation of janitorial and concierge offerings to create inviting workplace experiences. Addressing the facility management talent shortage solutions involves significant investment in upskilling programs.

- Finally, comparing hard vs soft facility services is less about which is more important and more about achieving a seamless integration that enhances the overall built environment and occupant well-being.

What are the key market drivers leading to the rise in the adoption of North America Facility Management Services Industry?

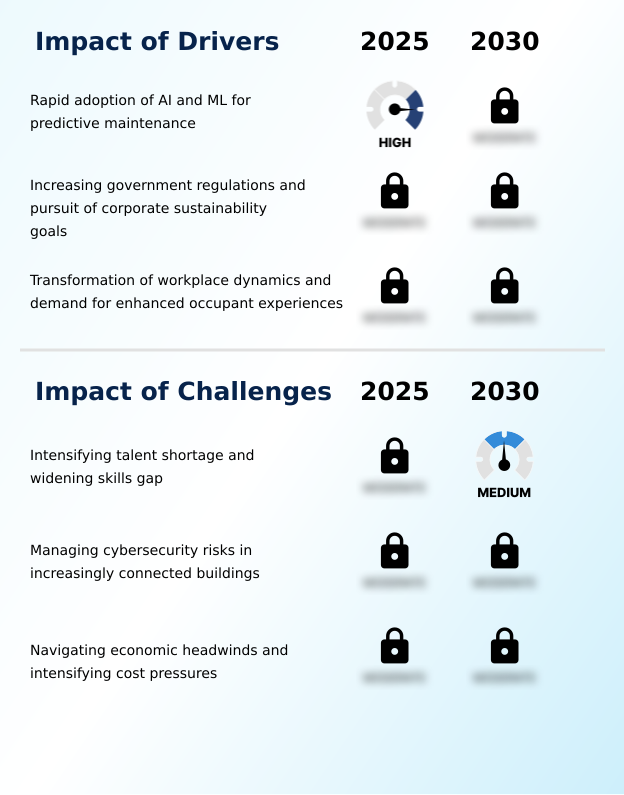

- The rapid adoption of AI and machine learning for predictive maintenance is a key driver propelling market growth and enhancing operational efficiency.

- Market growth is propelled by several key drivers transforming building operations. The rapid adoption of AI and ML for predictive maintenance is paramount, with some firms reporting a 40% decrease in reactive maintenance calls.

- The increasing pressure from government building maintenance regulations and corporate sustainability goals is accelerating the demand for specialized decarbonization services and comprehensive energy management solutions.

- This focus on sustainable facility practices is now a core component of real estate portfolio management.

- Additionally, the evolution of hybrid work models is driving demand for an enhanced workplace experience, boosting the need for advanced soft services, indoor air quality monitoring, and employee wellness programs.

- These drivers compel service providers to offer more sophisticated, technology-driven solutions to remain competitive.

What are the market trends shaping the North America Facility Management Services Industry?

- The proliferation of robotic process automation and autonomous maintenance systems marks a significant market trend, reshaping operational strategies and augmenting workforce capabilities.

- Key trends are reshaping the facility management services market, with a strong emphasis on technology and integration. The proliferation of robotic process automation is a major development, with autonomous cleaning robots enhancing efficiency in high-traffic commercial building services by up to 30%.

- The strategic adoption of digital twin technology allows for advanced virtual asset management, providing a level of foresight that improves capital planning. Another significant trend is the transition toward an integrated FM model, where a single facility management provider handles all services. This consolidation simplifies accountability and can lead to a 15% reduction in administrative overhead.

- The application of AI in facility management and IoT for building management is becoming standard, enabling smarter, more proactive operations and supporting a better workplace strategy.

What challenges does the North America Facility Management Services Industry face during its growth?

- An intensifying talent shortage and a widening skills gap present a significant challenge, constraining service delivery and technology adoption across the industry.

- The market faces significant challenges that could impede growth if not addressed strategically. A primary issue is the intensifying talent shortage, which is widening the skills gap for technicians who must now manage complex building automation systems and smart sensor maintenance.

- This scarcity of qualified personnel increases labor costs and can delay critical maintenance, with some projects experiencing delays of up to 25%. Another formidable challenge is managing the escalating cybersecurity risks in increasingly connected buildings. A single breach can compromise building security systems and disrupt operations, highlighting the urgent need for robust security protocols.

- Furthermore, navigating economic headwinds and cost pressures from clients creates a difficult balancing act, forcing firms to innovate on efficiency without sacrificing the quality of essential services.

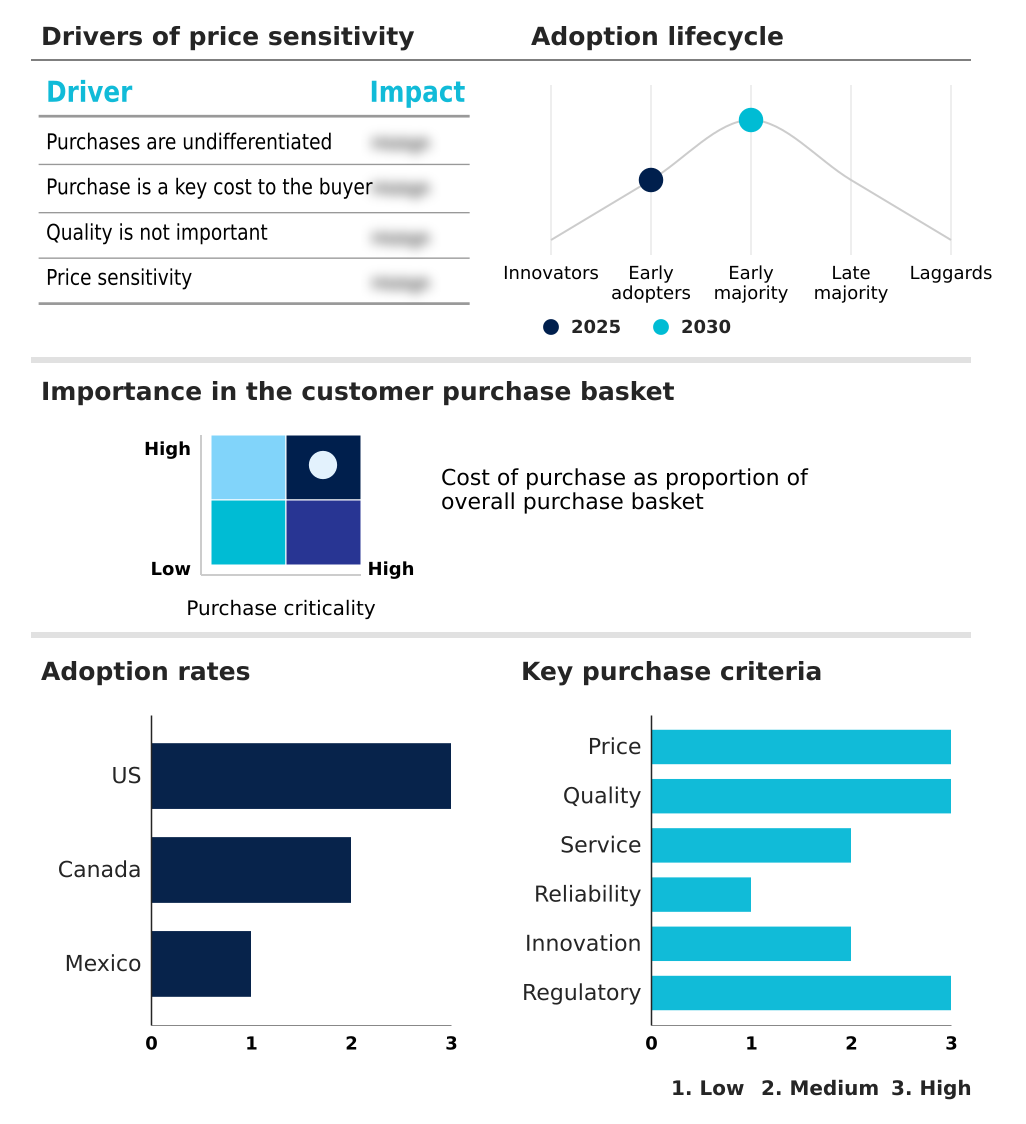

Exclusive Technavio Analysis on Customer Landscape

The north america facility management services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the north america facility management services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of North America Facility Management Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, north america facility management services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABM Industries Inc. - Offers integrated facility solutions, including janitorial, HVAC, electrical, and energy services, to enhance building operational efficiency and performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABM Industries Inc.

- Allied Universal

- Aramark

- BGIS Global Integrated Solutions

- Black and McDonald Ltd.

- CBRE Group Inc.

- Colliers International Group

- Compass Group Plc

- Cushman and Wakefield Plc

- Dexterra Group

- EMCOR Group Inc.

- GDI Integrated Facility Services

- Harvard Maintenance

- ISS AS

- Johnson Controls International

- Jones Lang LaSalle Inc.

- Kellermeyer Bergensons Services

- Newmark Group Inc.

- Sodexo SA

- UG2 LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in North america facility management services market

- In March, 2025, Jones Lang LaSalle Inc. announced a strategic collaboration to integrate generative artificial intelligence agents into its building operations platform to automate work order processing and optimize technician dispatching.

- In April, 2025, Cushman and Wakefield Plc formed a partnership with a spatial data provider to implement comprehensive digital twin modeling across its North American industrial and logistics portfolio.

- In June, 2025, CBRE Group Inc. introduced a suite of decarbonization and energy management services for the North American logistics and warehousing sector to help clients with green building certifications.

- In August, 2025, Sodexo SA North America launched an integrated workplace experience platform that uses a mobile app to harmonize food services, facilities management, and employee wellness programs.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled North America Facility Management Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 205 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.1% |

| Market growth 2026-2030 | USD 175.3 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.7% |

| Key countries | US, Canada and Mexico |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The facility management services market in North America is evolving into a technology-centric field where data-driven strategies are paramount. The integration of building automation systems and computerized maintenance management system (CMMS) is no longer a differentiator but a baseline expectation for achieving operational efficiency.

- At the boardroom level, capital planning decisions are now heavily influenced by insights from digital twin technology, which allows for virtual asset management and lifecycle simulations. This move toward predictive maintenance, facilitated by AI and machine learning, has enabled some organizations to reduce critical equipment downtime by over 30%.

- Key industry drivers include pressing sustainability mandates and the need for enhanced occupant comfort, pushing firms toward comprehensive energy management and waste reduction programs.

- However, the sector grapples with significant cybersecurity risks in connected buildings and a persistent skills gap, making investment in talent development and robust security protocols essential for long-term viability and growth in providing both hard services and soft services.

What are the Key Data Covered in this North America Facility Management Services Market Research and Growth Report?

-

What is the expected growth of the North America Facility Management Services Market between 2026 and 2030?

-

USD 175.3 billion, at a CAGR of 9.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Commercial buildings, Government buildings, and Residential buildings), Service (Soft services, and Hard services), Type (Fixed-term, and On-demand) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Rapid adoption of AI and ML for predictive maintenance, Intensifying talent shortage and widening skills gap

-

-

Who are the major players in the North America Facility Management Services Market?

-

ABM Industries Inc., Allied Universal, Aramark, BGIS Global Integrated Solutions, Black and McDonald Ltd., CBRE Group Inc., Colliers International Group, Compass Group Plc, Cushman and Wakefield Plc, Dexterra Group, EMCOR Group Inc., GDI Integrated Facility Services, Harvard Maintenance, ISS AS, Johnson Controls International, Jones Lang LaSalle Inc., Kellermeyer Bergensons Services, Newmark Group Inc., Sodexo SA and UG2 LLC

-

Market Research Insights

- The market's momentum is shaped by a strategic shift towards integrated and technology-driven service delivery. The adoption of an integrated FM model has shown to improve operational transparency, while AI in facility management can enhance work order processing efficiency by over 25%.

- Service providers are leveraging building operations platforms and smart asset initiatives to meet demands for sustainable facility practices and net-zero operations. The integration of employee wellness programs within service offerings is also growing, with organizations seeing a correlation between enhanced workplace environments and employee retention.

- This move towards holistic solutions, where hard services provider and soft services company roles merge, demonstrates a clear market trajectory toward comprehensive, value-added partnerships that optimize both building performance and occupant well-being.

We can help! Our analysts can customize this north america facility management services market research report to meet your requirements.

RIA -

RIA -