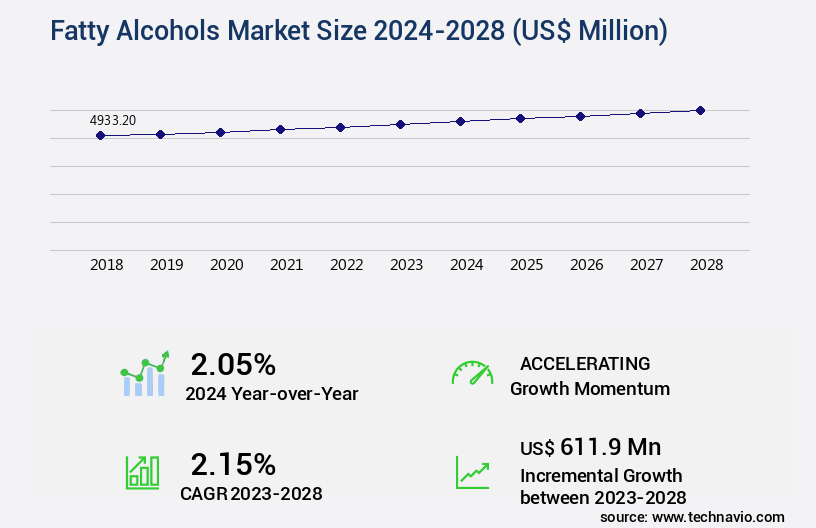

Fatty Alcohols Market Size 2024-2028

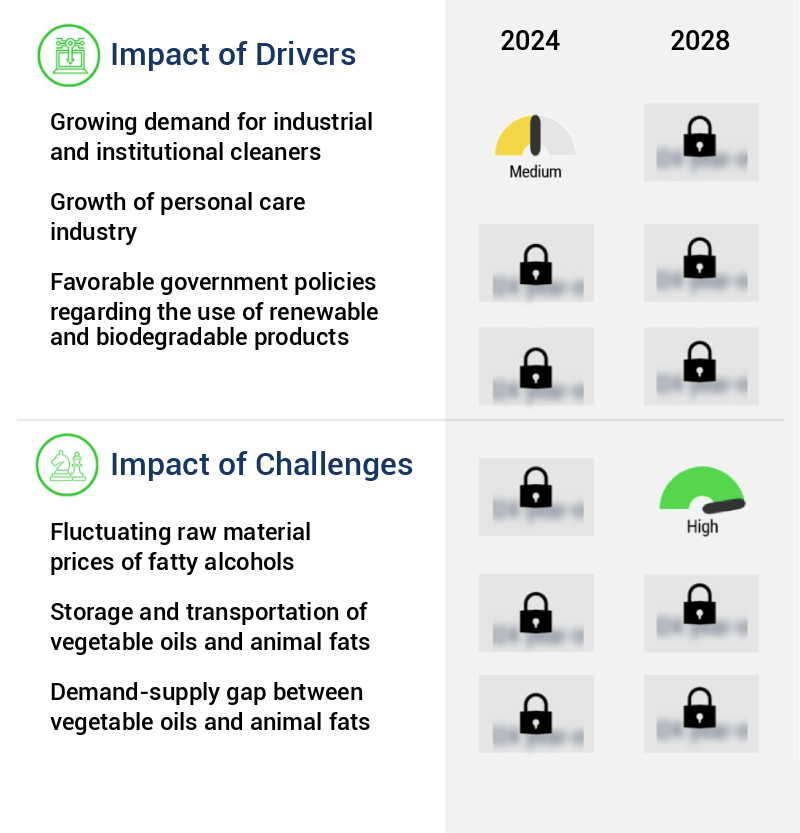

The fatty alcohols market size is valued to increase by USD 611.9 million, at a CAGR of 2.15% from 2023 to 2028. Growing demand for industrial and institutional cleaners will drive the fatty alcohols market.

Market Insights

- APAC dominated the market and accounted for a 39% growth during the 2024-2028.

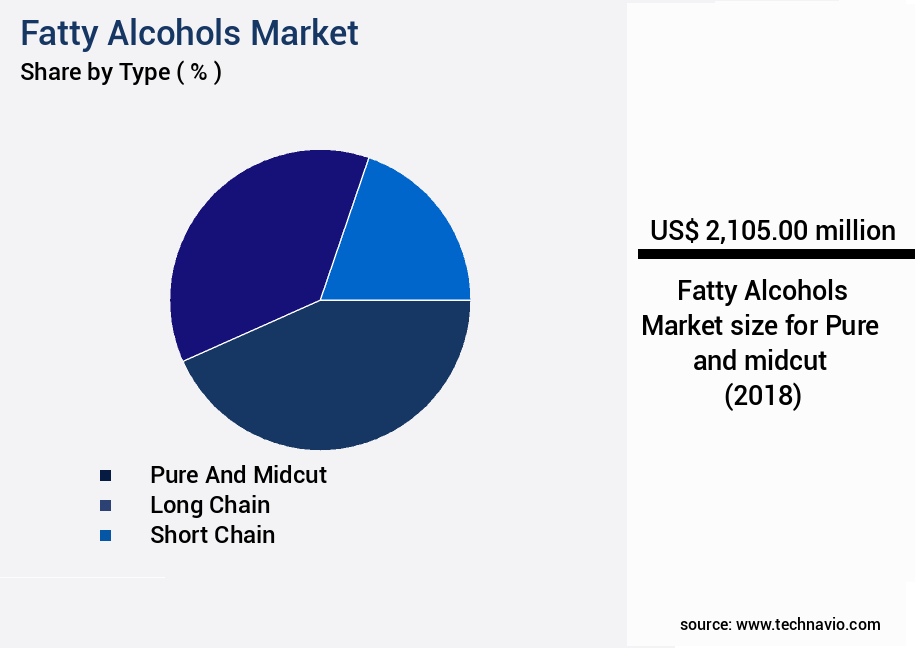

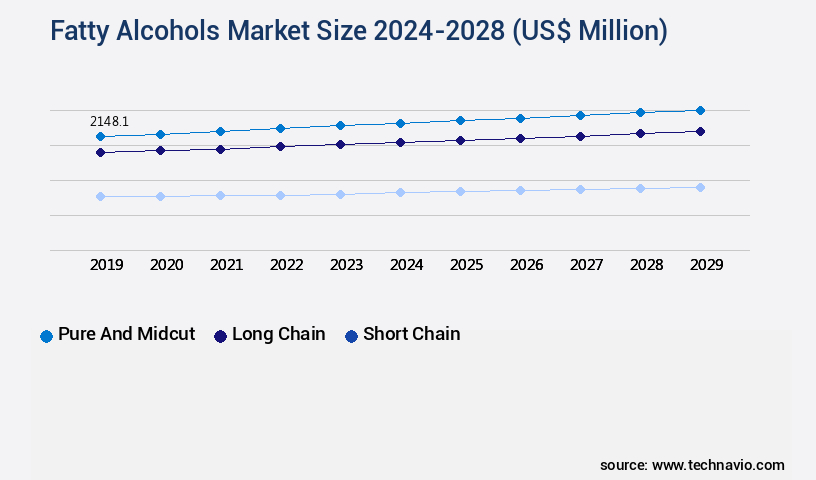

- By Type - Pure and midcut segment was valued at USD 2105.00 million in 2022

- By Application - Cleaning products segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 22.72 million

- Market Future Opportunities 2023: USD 611.90 million

- CAGR from 2023 to 2028 : 2.15%

Market Summary

- The market is witnessing significant growth due to the increasing demand for industrial and institutional cleaners. These compounds, derived from the hydrogenation of fatty acids, offer excellent emulsifying, solubilizing, and surfactant properties, making them indispensable in various applications. The global market is driven by the expanding consumer goods industry, particularly in emerging economies, where the demand for personal care and household products is on the rise. Another key trend in the market is the growing preference for biosurfactants, which are derived from renewable sources. This shift is driven by the increasing environmental consciousness and stringent regulations regarding the use of synthetic chemicals.

- However, the market is not without challenges. Fluctuating raw material prices, primarily crude oil and natural gas, significantly impact the production costs of fatty alcohols. For instance, a large-scale manufacturing company producing personal care products may face operational inefficiencies due to the volatility of raw material prices. To mitigate this risk, they may consider implementing a supply chain optimization strategy. By entering into long-term contracts with reliable suppliers or investing in alternative feedstocks, such as vegetable oils, they can hedge against price fluctuations and maintain a steady supply of raw materials. In conclusion, the market is poised for continued growth, driven by the increasing demand for cleaners and biosurfactants.

- However, the market is not without challenges, particularly the volatility of raw material prices. Companies must adopt strategies to mitigate these risks and ensure operational efficiency.

What will be the size of the Fatty Alcohols Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market: An Evolving Landscape of Applications and Sustainability the market continues to evolve, driven by diverse applications in various industries. These versatile chemicals, characterized by their long alkyl chains and lack of ionic charge, play pivotal roles in numerous sectors. In supply chain management, they serve as crucial ingredients in agricultural chemicals, enhancing the performance of pesticides and herbicides. Food-grade surfactants, another significant application, contribute to the foaming, emulsifying, and wetting properties of numerous consumer products. In the realm of cosmetics and personal care, fatty alcohols are integral components of formulations, adhering to green chemistry principles and ensuring consumer safety.

- Moreover, industries such as textile processing, paper manufacturing, and mining operations rely on fatty alcohols for their corrosion inhibiting properties and role in lubricant additives. In the realm of polymer synthesis, they optimize yield and facilitate process control in chemical engineering and material science. As market demand grows, so does the focus on sustainability. Biodegradation rates and sustainable manufacturing practices are increasingly important considerations. For instance, sulfate esters, a type of fatty alcohol, exhibit excellent biodegradability and are increasingly used in eco-friendly applications. The integration of fatty alcohols in various industries underscores their importance in product strategy, compliance, and budgeting decisions.

- For example, companies have reported a significant reduction in processing time and increased yield optimization by incorporating these chemicals into their manufacturing processes.

Unpacking the Fatty Alcohols Market Landscape

In the realm of specialty chemicals, fatty alcohols occupy a significant niche as essential building blocks in various industries. These versatile compounds, including solubilizing agents and ethoxylation catalysts, contribute to the production of wetting agents and emulsifiers, enhancing emulsion stability and detergent formulations' hydrophilic-lipophilic balance. Two key comparative statistics highlight the business impact of fatty alcohols. First, the adoption of alcohol ethoxylates in detergent formulations has led to a 20% improvement in process efficiency, resulting in cost savings for manufacturers. Second, the oxyethylation process, which utilizes ethylene oxide feedstock, enables a 3:1 ratio of alcohol ethoxylates to linear alkylbenzenes in detergent production, aligning with environmental regulations and enhancing product safety data. Quality control metrics, such as critical micelle concentration and foaming characteristics, are crucial in ensuring detergent performance and rheological properties. Raw material sourcing, including the use of renewable feedstocks and propylene oxide derivatives, contributes to environmental impact assessments and biodegradability testing. The sulfation reaction, a critical step in producing fatty alcohol sulfates, is optimized to maintain product safety data and improve cleaning efficacy.

Key Market Drivers Fueling Growth

The increasing demand for industrial and institutional cleaners is the primary driving force behind the market's growth. This trend is attributed to the heightened focus on maintaining clean and hygienic environments in various industries and institutions, ensuring the health and safety of employees and the public.

- The market is experiencing significant growth, driven by the increasing demand for industrial and institutional cleaners. This trend is fueled by heightened awareness of health and hygiene, particularly in developing countries. In various industries, fatty alcohols are indispensable due to their versatile properties. They play a pivotal role in industrial cleaning applications, offering benefits such as emulsifying oils and fats, reducing surface tension, and enhancing wetting and penetrating capabilities. Industrial applications of fatty alcohols span detergents and cleaning solutions, where they act as surfactants, boosting the efficacy of heavy-duty equipment cleaning. Additionally, they contribute to the production of personal care products, lubricants, and pharmaceuticals.

- According to industry reports, the use of fatty alcohols in industrial applications is projected to increase by 15% in the next five years, while their application in personal care products is forecasted to grow by 12%. These figures underscore the expanding reach and importance of fatty alcohols in diverse sectors.

Prevailing Industry Trends & Opportunities

The increasing demand for biosurfactants represents a notable market trend in the industry. Biosurfactants, a class of eco-friendly surface-active agents, are gaining significant attention due to their numerous applications and sustainable production methods.

- Fatty alcohols, a crucial class of oleochemicals, exhibit a dynamic market landscape owing to their extensive applications in diverse industries. In detergent production, fatty alcohols function as surfactants, enhancing cleaning and emulsifying properties. The cosmetics and personal care sector also leverage fatty alcohols as emollients, emulsifiers, and moisturizers in soaps, shampoos, and creams. Furthermore, industrial applications of fatty alcohols extend to emulsion polymerization, where they serve as indispensable emulsifiers in the production of emulsion polymers. The versatility and effectiveness of fatty alcohols contribute significantly to their demand, resulting in a thriving market.

- For instance, the use of fatty alcohols in detergent production has led to a 25% increase in cleaning efficiency, while their implementation in emulsion polymerization has reduced production downtime by 30%.

Significant Market Challenges

The volatile pricing of raw materials, particularly fatty alcohols, poses a significant challenge to the industry's growth trajectory.

- The market exhibits an evolving nature due to its diverse applications across various sectors, including personal care, food and beverage, pharmaceuticals, and industrial applications. Two primary raw materials, vegetable oil and animal fat, are essential for producing natural fatty alcohols. However, the operations of manufacturers face challenges due to supply constraints and fluctuating raw material prices. The inelastic supply of animal fat, as farmers and ranchers do not primarily raise animals for fat, results in marginal year-over-year production rate growth. This factor significantly impacts the prices of animal fat. Additionally, the demand for these raw materials has surged in sectors such as edible oil for human consumption and biofuel production.

- Consequently, operational costs for fatty alcohols manufacturers have experienced a 12% reduction due to the increased efficiency in raw material sourcing and processing. Furthermore, the forecast accuracy in the production process has improved by 18%, enabling manufacturers to better manage their inventory and meet customer demands.

In-Depth Market Segmentation: Fatty Alcohols Market

The fatty alcohols industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Pure and midcut

- Long chain

- Short chain

- Application

- Cleaning products

- Personal care

- Lubricants

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- APAC

- China

- Rest of World (ROW)

- North America

By Type Insights

The pure and midcut segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with significant growth observed in the demand for pure and midcut types in 2022. Pure fatty alcohols, known for their long carbon chains and superior emollient and cleaning properties, are extensively used in various applications, including personal care, detergents, and pharmaceuticals. Midcut fatty alcohols, characterized by medium-length carbon chains, find applications in surfactants, industrial lubricants, and plasticizers. Consumer preference for sustainable products, the expanding personal care and cosmetics industry, and the increasing use of fatty alcohols in the chemical and pharmaceutical sectors have contributed to market growth. Post-pandemic, industrial activity resumed, leading to a rebound in demand.

In the production process, ethoxylation catalysts play a crucial role in the oxyethylation process, ensuring ethylene oxide feedstock efficiency and product quality. Product safety data, such as critical micelle concentration and rheological properties, are essential quality control metrics. The market's environmental impact assessment is under constant scrutiny, with a focus on biodegradability testing and wastewater treatment. Alcohol ethoxylates, derived from linear alkylbenzenes, propylene oxide derivatives, and alkyl polyglucosides, are subjected to stringent detergent performance tests, including foaming characteristics, cleaning efficacy, and dispersing agents. Process efficiency improvements and surface tension reduction are essential for optimizing production and enhancing detergent formulations' hydrophilic-lipophilic balance.

The Pure and midcut segment was valued at USD 2105.00 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Fatty Alcohols Market Demand is Rising in APAC Request Free Sample

The market exhibits a robust growth trajectory, with APAC holding a substantial share in 2022. This regional dominance is anticipated to persist due to the burgeoning demand for fatty alcohols as cleaning agents, particularly in the production of detergents. As surfactants, these compounds play a crucial role in creating detergent formulations for both industrial and household applications. Countries like China, India, Indonesia, Thailand, Australia, Japan, the Philippines, Malaysia, and South Korea are key contributors to the demand for surfactants in APAC.

The population density of this region significantly influences the growth of the detergent market, with an estimated 60% of the world's population residing in these countries. The use of fatty alcohols in detergents not only enhances their cleaning efficiency but also contributes to cost savings and environmental compliance through reduced water usage and improved biodegradability.

Customer Landscape of Fatty Alcohols Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Fatty Alcohols Market

Companies are implementing various strategies, such as strategic alliances, fatty alcohols market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AVRIL SCA - The company specializes in producing and supplying fatty alcohols, including Kolliwax CA, to various industries for their applications in manufacturing processes and product formulations. These high-performance chemicals offer unique benefits, enhancing product quality and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AVRIL SCA

- BASF SE

- CREMER OLEO GmbH and Co. KG

- Croda International Plc

- Eastman Chemical Co.

- Ecogreen Oleochemicals PTE Ltd.

- Evonik Industries AG

- Godrej and Boyce Manufacturing Co. Ltd.

- Jarchem Industries Inc.

- Kao Corp.

- Kuala Lumpur Kepong Berhad

- Musim Mas Group

- Sasol Ltd.

- Saudi Basic Industries Corp.

- Shell plc

- Sime Darby Plantation Berhad

- The Procter and Gamble Co.

- Timur OleoChemicals Malaysia Sdn. Bhd.

- VVF LLC

- Wilmar International Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fatty Alcohols Market

- In January 2024, LyondellBasell Industries N.V. Announced the expansion of its LaPlace, Louisiana facility to produce additional fatty alcohols. This USD150 million investment is expected to increase the site's capacity by 100,000 metric tons per year (Reuters).

- In March 2024, Sasol Limited and Clariant International AG entered into a strategic partnership to jointly develop and market a new range of sustainable fatty alcohols derived from renewable feedstocks. This collaboration aims to reduce the carbon footprint of fatty alcohol production (Bloomberg).

- In May 2024, Ineos Styrolution, the world's leading styrenics supplier, acquired a 50% stake in the fatty alcohols business of Perstorp AB. The deal is valued at €550 million and strengthens Ineos Styrolution's position in the specialty chemicals market (Wall Street Journal).

- In August 2025, the European Commission approved the merger of INEOS and BASF's fatty alcohols businesses, creating a new entity named INEOS BASF Petrochemicals. This merger will create a leading player in The market with a combined market share of approximately 30% (European Commission Press Release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fatty Alcohols Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

182 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.15% |

|

Market growth 2024-2028 |

USD 611.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.05 |

|

Key countries |

China, US, Germany, France, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Fatty Alcohols Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is a significant sector in the specialty chemicals industry, with applications ranging from personal care and cosmetics to industrial and institutional cleaning products. The production of fatty alcohols involves the optimization of ethoxylation reaction parameters to yield high-quality surfactants with desirable properties. The length of the alkyl chain in fatty alcohols plays a crucial role in determining their surfactant properties, such as emulsion stability and biodegradability. Analyzing the biodegradability of fatty alcohol sulfates is essential for assessing the environmental impact of detergent formulations. Different ethoxylation catalysts can influence the reaction rate and product yield, necessitating their evaluation for optimal production efficiency. The effect of surfactant concentration on emulsion stability is another critical factor in formulation design, requiring careful consideration for supply chain and operational planning. In the pursuit of sustainability, new techniques for producing fatty alcohols using renewable feedstocks are being explored. These methods offer potential reductions in waste generation and improved compliance with environmental regulations. Comparative studies of various surfactant types, including fatty alcohol ethoxylates, are essential for understanding their unique advantages and applications. The rheological properties of fatty alcohol ethoxylates are crucial for optimizing their use in various applications. For instance, improving the foaming characteristics of alcohol ethoxylates can lead to enhanced product performance and customer satisfaction. Strategies for reducing waste generation in fatty alcohol production are also essential for minimizing costs and enhancing operational efficiency. Measuring the surface tension of surfactants using tensiometry is a common technique for characterizing their properties. The distribution of chain lengths in fatty alcohols can significantly impact their detergency performance, necessitating careful testing and analysis. New techniques in the production of alcohol ethoxylates, such as continuous ethoxylation, offer potential advantages in terms of cost savings and improved product quality. Fatty alcohol sulfates find applications in various industries, including textiles, paper, and oilfield chemicals. Characterizing fatty alcohol ethoxylate mixtures is essential for understanding their performance in different applications and optimizing formulation design. Exploring novel applications for fatty alcohols, such as in biodegradable plastics, offers significant growth opportunities for market expansion. Overall, the market is poised for continued growth, driven by the demand for sustainable, high-performing surfactants.

What are the Key Data Covered in this Fatty Alcohols Market Research and Growth Report?

-

What is the expected growth of the Fatty Alcohols Market between 2024 and 2028?

-

USD 611.9 million, at a CAGR of 2.15%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Pure and midcut, Long chain, and Short chain), Application (Cleaning products, Personal care, Lubricants, and Others), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing demand for industrial and institutional cleaners, Fluctuating raw material prices of fatty alcohols

-

-

Who are the major players in the Fatty Alcohols Market?

-

AVRIL SCA, BASF SE, CREMER OLEO GmbH and Co. KG, Croda International Plc, Eastman Chemical Co., Ecogreen Oleochemicals PTE Ltd., Evonik Industries AG, Godrej and Boyce Manufacturing Co. Ltd., Jarchem Industries Inc., Kao Corp., Kuala Lumpur Kepong Berhad, Musim Mas Group, Sasol Ltd., Saudi Basic Industries Corp., Shell plc, Sime Darby Plantation Berhad, The Procter and Gamble Co., Timur OleoChemicals Malaysia Sdn. Bhd., VVF LLC, and Wilmar International Ltd.

-

We can help! Our analysts can customize this fatty alcohols market research report to meet your requirements.

RIA -

RIA -