Oilfield Chemicals Market Size 2024-2028

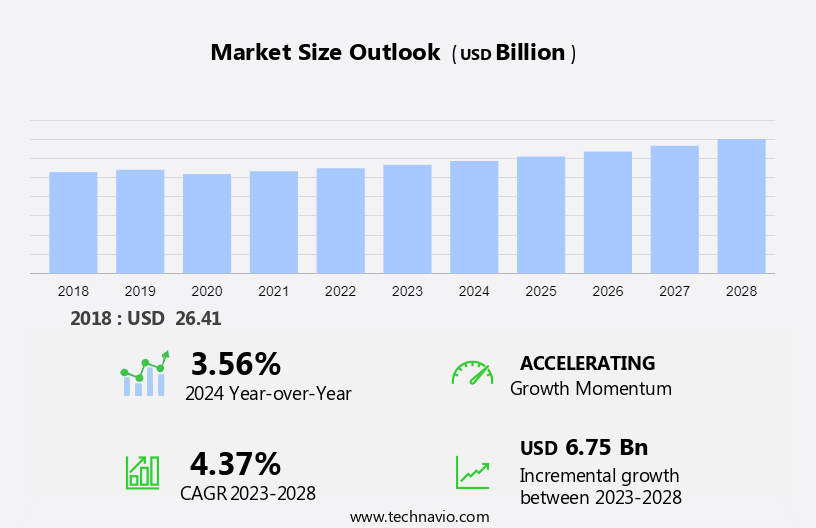

The oilfield chemicals market size is forecast to increase by USD 6.75 billion at a CAGR of 4.37% between 2023 and 2028.

- The market's growth rate hinges on various factors, such as the increased production of crude oil, advancements in oilfield technology, and the expansion of shale gas exploration and production. These elements collectively contribute to the market's trajectory, driving its upward momentum. With the continuous improvement and adoption of innovative technologies in the oilfield sector, coupled with the heightened focus on shale gas extraction, the market is poised for significant expansion in the foreseeable future. It also includes an in-depth analysis of drivers, trends, and challenges. Our report examines historical data from 2018-2022, besides analyzing the current market scenario.

What will the Oilfield Chemicals Market Size During the Forecast Period?

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Production

- Well stimulation

- Drilling fluids

- Enhanced oil recovery

- Others

- Type

- Onshore

- Offshore

- Geography

- North America

- Canada

- US

- Europe

- APAC

- China

- India

- Middle East and Africa

- South America

- North America

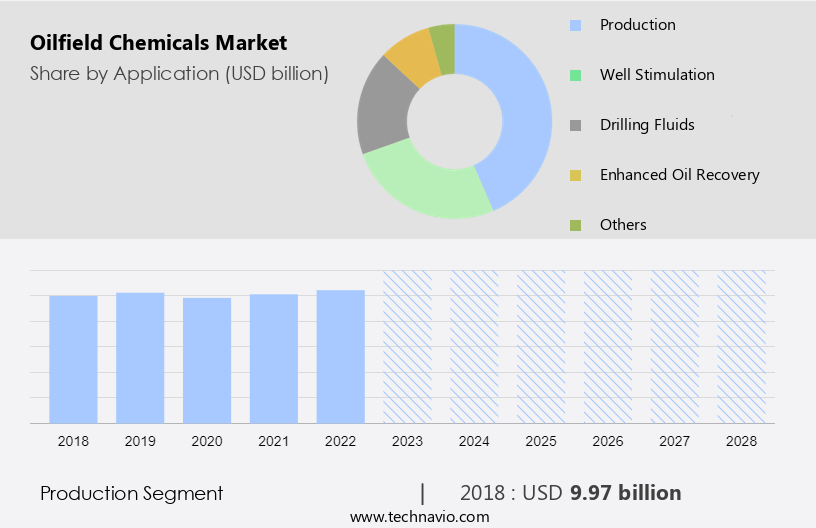

By Application Insights

- The production segment is estimated to witness significant growth during the forecast period.

In the realm of oil exploration and production activities, oilfield chemicals play a pivotal role in ensuring efficiency and safety during drilling and well-stimulation processes. The shale gas revolution has significantly increased the demand for oilfield chemicals, particularly in crude oil production from onshore fields in developing economies. These chemicals are instrumental in optimizing operations, adhering to environmental standards, and enhancing reservoir recovery. Oilfield chemicals are applied extensively in various production processes, including drilling fluids for deep drilling activities, fracturing liquids for well stimulation, and inhibitors for preventing corrosion and the formation of emulsions on metal surfaces. Product analysis reveals that the Rheology modifiers segment dominates the market, with synthetic-based drilling fluids and micro-fibrillated cellulose (MFC) and xanthan gum being commonly used.

The inhibitors segment is also gaining traction due to its ability to mitigate impurities derived from crude oil production. Water-soluble inhibitors, such as amides and long-chain amines, are popular choices for preventing corrosion and scaling in onshore exploration activities. As the industry dynamics evolve, oilfield chemicals continue to play a crucial role in enhancing oilfield exploration endeavors while addressing the challenges of drilling in diverse geological conditions. Moreover, the shift towards renewable energy sources like solar power and wind power has led to a decline in demand for oilfield chemicals in certain applications. However, the ongoing demand for oil and gas, coupled with the need for optimization and safety in production processes, ensures that the market remains a significant player in the energy sector.

Get a glance at the market report of share of various segments Request Free Sample

The Production segment was valued at USD 9.97 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

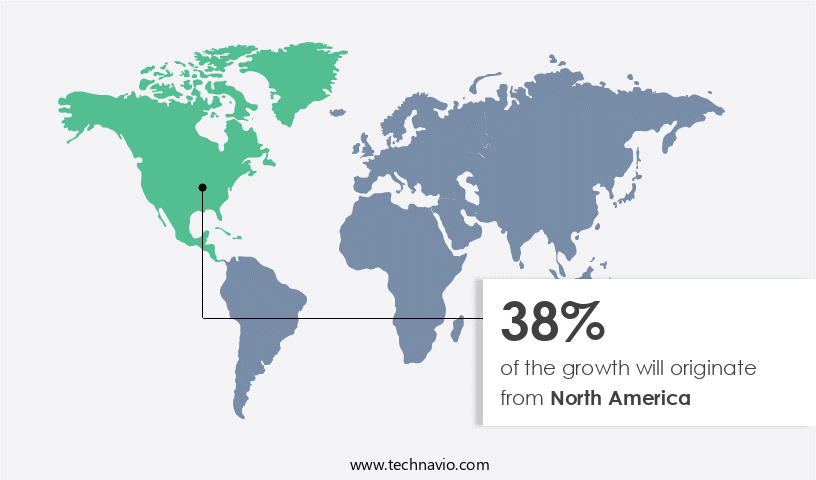

- North America is estimated to contribute 38% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In the Oil & gas industry, the application analysis of oilfield chemicals in North America experienced substantial growth in 2023, driven by the recovery of West Texas Intermediate and Brent crude prices and the significant expansion of shale oil and gas production. The level of exploration and production activities in the US and Canada significantly impacted the demand for oilfield chemicals, including solid-free fluids, fracture stimulation agents, water shut-off compounds, gravel packing additives, and acid stimulation catalysts. These chemicals are essential for post-oil extraction processes, ensuring efficient drilling and production. Advancements in technology, such as automation and IoT, have encouraged oil rig operators to adopt innovative drilling solutions, including the use of O2 for onshore and offshore projects.

The susceptibility of oil and gas infrastructure to corrosion necessitates the employment of corrosion inhibitors, such as O2-rendering agents, to maintain operational efficiency. Moreover, the market in North America caters to various applications, including drilling fluids, cementing, stimulation, and petrochemical production. The market encompasses demulsifiers, water clarifiers, biocides, scale inhibitors, paraffin inhibitors, hydrogen sulfide scavengers, and gas well foamers. The adoption of renewable energy, electric vehicles, and sustainable practices in the industry is expected to influence the future demand for oilfield chemicals. Nouryon, a leading chemical company, has been a significant player in the market, providing solutions for shale gas production and petrochemicals manufacturing.

The market's expansion is further fueled by the increasing demand for plastics and other industrial applications. In summary, the market in North America experienced robust growth in 2023, driven by the recovery of crude oil prices and the expansion of shale oil and gas production. The market caters to various applications, including drilling, cementing, stimulation, and petrochemicals production, and employs a range of chemicals, including solid-free fluids, fracture stimulation agents, water shut-off compounds, gravel packing additives, and acid stimulation catalysts. The market's future growth is expected to be influenced by technological advancements, the adoption of renewable energy, and the increasing demand for plastics and other industrial applications.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Oilfield Chemicals Market ?

Increased production of crude oil is the key driver of the market.

- In the realm of oil exploration and production activities, the shale gas revolution has significantly boosted the necessity for oilfield chemicals. With the rise in crude oil production, the need for well-stimulation techniques, such as hydraulic fracturing (fracking) and acidizing, has become increasingly important. Oilfield chemicals, including fracturing fluids and acidizing agents, play a pivotal role in these processes by enhancing reservoir permeability and stimulating oil flow from wells. As onshore exploration activities expand in developing economies and onshore fields, maintaining flow assurance becomes crucial to prevent operational disruptions. Oilfield chemicals are applied to mitigate issues such as wax deposition, asphaltene flocculation, hydrate formation, and scale accumulation in pipelines and production facilities.

-

These additives help maintain the desired viscosity and prevent the formation of solids, ensuring the smooth progression of drilling activities. Fracturing liquids, another essential category of oilfield chemicals, are used extensively in well stimulation processes. These liquids, which include a variety of additives and surfactants, help enhance the efficiency of the fracturing process by improving the contact between the fracturing fluid and the rock formation. The industry dynamics of oilfield chemicals are influenced by various factors, including the demand for oil and gas, technological advancements, and regulatory requirements. The market for oilfield chemicals is expected to grow as oil and gas companies continue to invest in onshore exploration activities and seek to maximize hydrocarbon recovery while ensuring operational efficiency and safety. The decline in demand for oilfield chemicals in solar power and wind power industries may, however, pose a challenge to market growth.

What are the market trends shaping the Oilfield Chemicals Market?

Rising oilfield activities due to deepwater drilling operations is the upcoming trend in the market.

- In the realm of oil exploration and production activities, the significance of oilfield chemicals has grown exponentially due to the shale gas revolution and the increase in crude oil production. These essential chemicals play a pivotal role in enhancing efficiency, ensuring safety, and managing downhole conditions during drilling and well stimulation. In deepwater environments, where corrosive conditions such as high salinity and the presence of hydrogen sulfide (H2S) are prevalent, oilfield chemicals act as crucial protectants for equipment, pipelines, and infrastructure. The market encompasses a wide array of products used in various stages of oil exploration and production. These include drilling fluids for optimizing drilling operations, deep drilling activities for managing impurities, and the formation of emulsions.

- The inhibitors segment, which comprises corrosion inhibitors and scale inhibitors, is a key component of this market. These inhibitors prevent the formation of emulsions and protect metal surfaces from corrosion. Moreover, oilfield chemicals are indispensable in onshore exploration activities, particularly in developing economies and onshore fields, where investments in advanced technologies are on the rise. In the realm of well stimulation and reservoir recovery, oilfield chemicals such as rheology modifiers, synthetic-based drilling fluids, and fracturing liquids play a vital role. Micro-fibrillated cellulose (MFC) and xanthan gum are popular rheology modifiers that help manage downhole conditions and improve reservoir access.

What challenges does the Oilfield Chemicals Market face during its growth?

Increasing corrosion of materials in oilfields is a key challenge affecting the market growth.

- In the realm of oil exploration and production activities, the significance of oilfield chemicals has grown substantially. The shale gas revolution and the increase in crude oil production have necessitated greater efficiency, safety, and optimization in drilling and well-stimulation processes. Oilfield chemicals play a pivotal role in reservoir recovery, formation of emulsions, and addressing impurities in derived oil products. The onshore exploration activities in developing economies and onshore fields have led to increased investments in oilfield chemicals. Solar power and wind power, as alternative energy sources, have caused a decline in demand for traditional oil-based energy, making it crucial for oilfield companies to maintain their operations and meet production targets.

- Oilfield chemicals are essential in various aspects of oilfield operations, including drilling fluids, deep drilling activities, and inhibitors. Synthetic-based drilling fluids, such as those containing Rheology modifiers like micro-fibrillated cellulose (MFC), xanthan gum, and fracturing liquids, are used to enhance drilling efficiency and ensure safety. Inhibitors, including water-soluble inhibitors, amides, and long-chain amines, are employed to protect metal surfaces from corrosion, a common issue in oilfield equipment. Corrosion, which can lead to equipment failures and unplanned downtime, is a significant challenge in the industry dynamics. The market encompasses a wide range of products, including drilling fluids, deep drilling chemicals, and inhibitors.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Ashland Inc.

- Baker Hughes Co.

- BASF SE

- Chevron Corp.

- Clariant International Ltd.

- Croda International Plc

- Evonik Industries AG

- FMC Corp.

- Halliburton Co.

- Kao Corp.

- Qixia Aotong Chemical Co. Ltd.

- Sasol Ltd.

- Schlumberger Ltd.

- Solvay SA

- The Lubrizol Corp.

- The SNF Group

- Yantai Humon Group Co. Ltd.

- Artek Surfin Chemicals Ltd.

- Huntsman International LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market plays a crucial role in the oil and gas industry. These chemicals are essential for various applications such as drilling, completion, production, and enhancement of oil and gas reserves. The market for Oilfield Chemicals is driven by several factors including the increasing demand for oil and gas, the need for enhanced oil recovery, and the growing focus on environmental sustainability. The market encompasses a wide range of products including biocides, corrosion inhibitors, demulsifiers, scale inhibitors, and surfactants. These chemicals help in enhancing the productivity of oil and gas wells, reducing downtime, and minimizing operational costs. The market for Oilfield Chemicals is expected to grow significantly due to the increasing exploration and production activities in various regions including North America, Europe, Asia Pacific, and the Middle East and Africa.

Moreover, the market is also being driven by the ongoing technological advancements in the oil and gas industry, which are leading to the development of new and more efficient chemicals. The demand for Oilfield Chemicals is also being driven by the stringent regulations regarding the environmental sustainability of oil and gas operations. These regulations are leading to the adoption of eco-friendly chemicals, which are expected to be a major trend in the market in the coming years. In conclusion, the market is a dynamic and growing market, driven by various factors including the increasing demand for oil and gas, the need for enhanced oil recovery, and the growing focus on environmental sustainability. The market is expected to continue growing in the coming years, driven by the ongoing technological advancements and the adoption of eco-friendly chemicals.

The Oilfield Chemicals Market plays a pivotal role in the upstream oil industry, encompassing a diverse range of specialized chemicals used in various applications, including oilfield waste management, drilling fluid optimization, oilfield production chemicals, and gas exploration chemicals. These chemicals facilitate drilling and production processes, ensuring wellbore stability, enhancing reservoir stimulation, and controlling corrosion. Drilling fluid optimization involves the use of oilfield chemicals for managing yield stress, filtration, and rheology to optimize drilling performance and prevent formation damage. Workover chemicals and fracking chemicals are essential for well workovers and hydraulic fracturing, respectively. Infrastructure corrosion control is another critical application, ensuring the longevity of oil and gas infrastructure.

Gas exploration chemicals, such as gas injection chemicals, are used to enhance reservoir engineering and improve hydrocarbon exploration. Downhole corrosion prevention and environmental impact assessment are essential components of oilfield safety, minimizing the impact on the environment while ensuring sustainable and low-carbon oil production. Oilfield logistics and automation streamline operations, reducing costs and improving efficiency. Carbon capture, storage, and sustainable oil are the future of the oilfield chemicals market, as the industry transitions towards more environmentally-friendly practices. The market's continued growth is driven by the increasing demand for oil and gas, advancements in reservoir engineering, and the need for improved oilfield safety and environmental sustainability.

The Oilfield Chemicals Market is a critical sector that supports the global energy industry, encompassing drilling mud rheology modifiers, filtration agents for drilling fluid, formation damage control agents, hydraulic fracturing chemicals, and completion fluids. These chemicals ensure efficient drilling, wellbore integrity, and enhanced oil recovery. However, the market faces challenges, including oilfield environmental impact, chemical safety, and the transition to renewable energy sources. Innovations in oilfield automation, downhole technology, and digital oilfield solutions are addressing these challenges. The energy transition, driven by energy efficiency, energy innovation, and clean energy technologies, is transforming the market. The formulation of green energy alternatives, such as geothermal energy, hydropower, and carbon sequestration, is a growing trend. The circular economy and chemical safety are essential considerations in the oilfield chemicals market. Energy security, energy independence, and fossil fuel alternatives are also shaping the market.

As the industry evolves, energy storage and smart grid technologies are becoming increasingly important. The integration of renewable energy sources and the adoption of clean energy technologies are expected to significantly impact the oilfield chemicals market in the future. The focus on energy efficiency and reducing the carbon footprint is driving the development of new, eco-friendly oilfield chemicals.

|

Oilfield Chemicals Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.37% |

|

Market growth 2024-2028 |

USD 6.75 billion |

|

Market structure |

USD Fragmented |

|

YoY growth 2023-2024(%) |

3.56 |

|

Key countries |

US, Canada, China, India, and Russia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -