Finished Vehicles Logistics Market Size 2026-2030

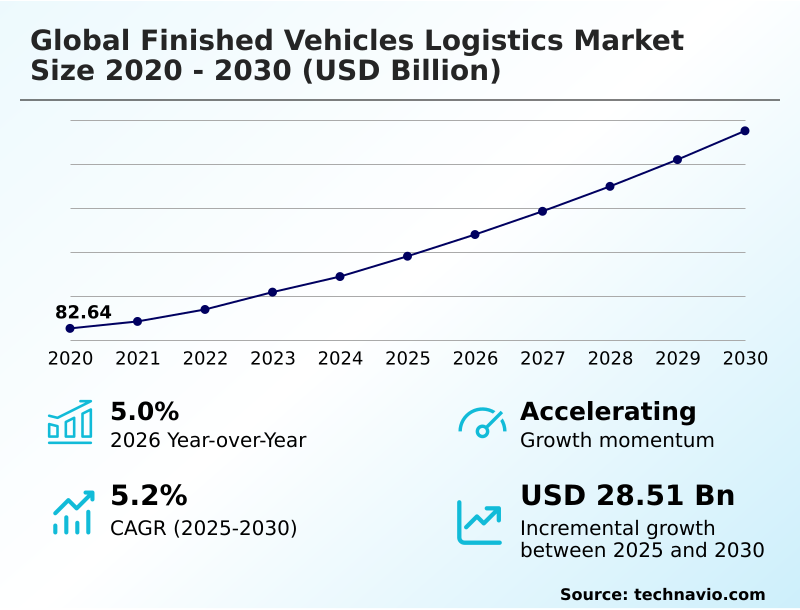

The finished vehicles logistics market size is valued to increase by USD 28.51 billion, at a CAGR of 5.2% from 2025 to 2030. Rise in electric vehicle production will drive the finished vehicles logistics market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 55.5% growth during the forecast period.

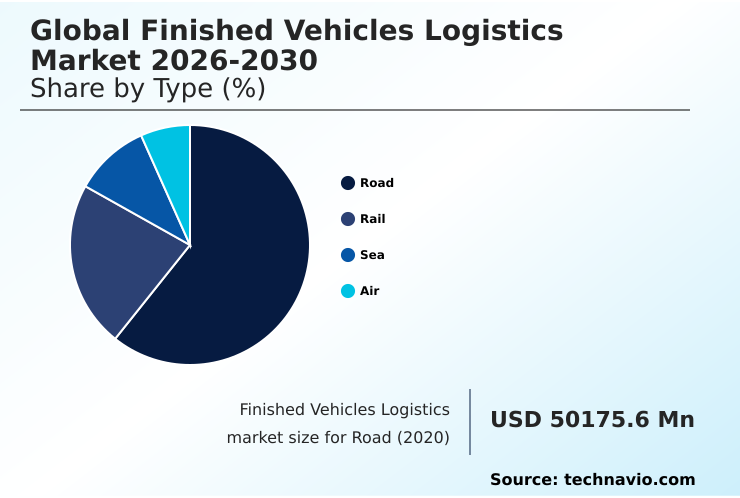

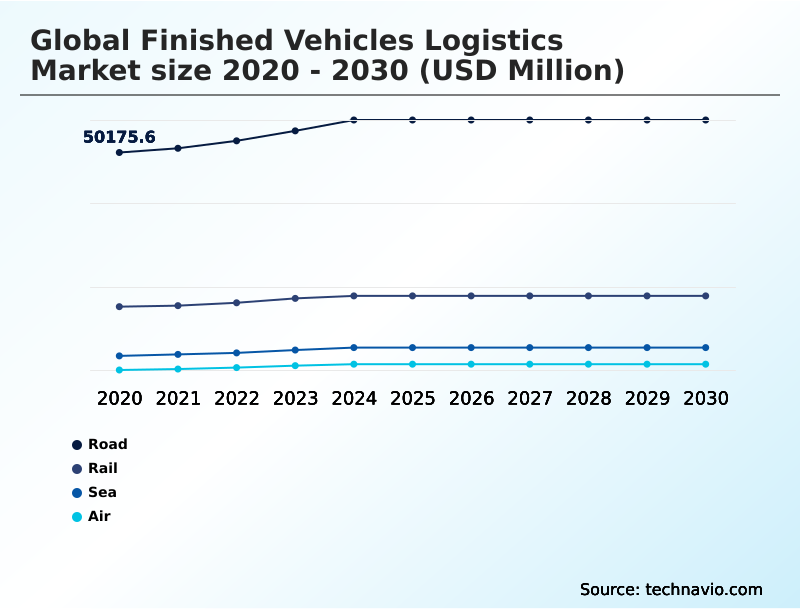

- By Type - Road segment was valued at USD 56.85 billion in 2024

- By Service - Warehousing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 44.90 billion

- Market Future Opportunities: USD 28.51 billion

- CAGR from 2025 to 2030 : 5.2%

Market Summary

- The finished vehicles logistics market is defined by the complex coordination of assets required to move automotive units from production lines to end consumers. This sector's growth is heavily influenced by the surge in electric vehicle output, which necessitates a redesign of transport networks to manage new safety protocols and weight considerations.

- Key industry drivers include the expansion of global automotive trade and an intense demand from manufacturers for complete supply chain visibility, which is being met through the integration of telematics and cloud-based logistics platforms. Prevailing trends focus on digitalization and sustainability, with digital twin fleet management and autonomous yard management gaining traction to improve efficiency and reduce operational costs.

- A primary business scenario involves optimizing multimodal transport solutions to connect disparate manufacturing hubs, like those in Southeast Asia, with consumer markets, requiring seamless handoffs between roll-on roll-off shipping and high-capacity rail wagons.

- However, the industry grapples with significant challenges, including persistent port and terminal congestion that disrupts schedules, rising fuel price volatility, and a critical shortage of specialized transport drivers, which collectively constrain capacity and increase operational pressures for logistics providers.

What will be the Size of the Finished Vehicles Logistics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Finished Vehicles Logistics Market Segmented?

The finished vehicles logistics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Road

- Rail

- Sea

- Air

- Service

- Warehousing

- Transport

- Vehicle type

- Passenger cars

- Light commercial vehicles

- Heavy commercial vehicles

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The road segment is estimated to witness significant growth during the forecast period.

The road segment is central to the finished vehicles logistics market, providing unparalleled flexibility for domestic transport and last-mile vehicle delivery.

This mode relies on a vast network of specialized car carriers and heavy-duty car haulers to move units from ports and rail hubs directly to dealerships.

The integration of advanced telematics and sensor network technology is transforming road haulage efficiency, as over 80% of automotive manufacturers now prioritize real-time vehicle tracking to enhance supply chain visibility.

Modern route optimization software helps manage complex delivery schedules and mitigate delays.

As the industry evolves, fleet management software is crucial for addressing challenges like axle weight regulations for electric vehicles and optimizing logistics cost reduction, ensuring a responsive and efficient automotive distribution network.

The Road segment was valued at USD 56.85 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 55.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Finished Vehicles Logistics Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the finished vehicles logistics market is led by APAC, which is projected to contribute over 55% of the market’s incremental growth, driven by massive production volumes and expanding automotive export hubs.

This region's maritime logistics landscape is rapidly evolving with increased ro-ro vessel capacity. North America represents a highly mature market, characterized by sophisticated intermodal logistics networks and a focus on damage-free delivery.

Europe is distinguished by its advanced port-centric logistics and a strong emphasis on green logistics solutions and zero-emission logistics, although it faces operational challenges, with terminal dwell times at major ports increasing to an average of 14 days.

The development of new vehicle processing centers in the Middle East and Africa and cross-border rail services in South America reflects growing investment in these emerging markets to improve their automotive distribution networks.

Market Dynamics

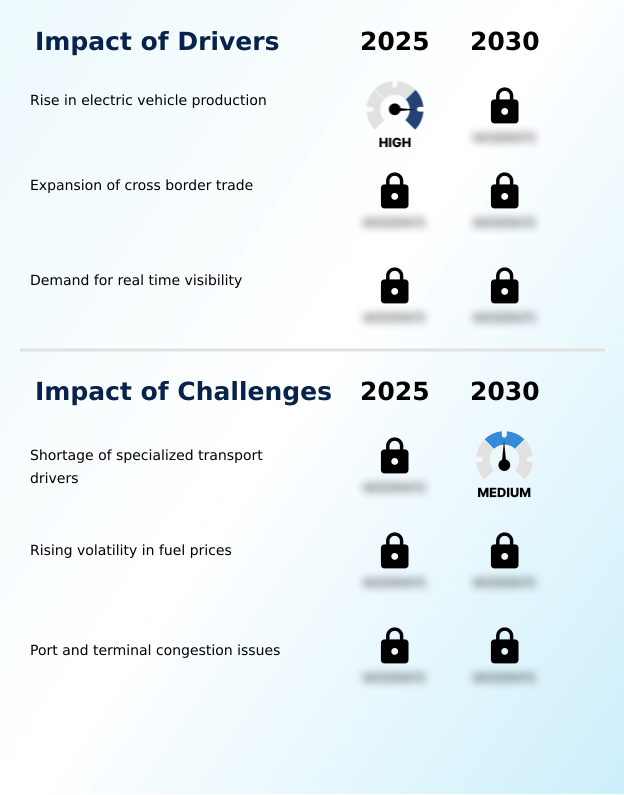

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the finished vehicles logistics market increasingly revolves around key operational questions. Optimizing finished vehicle logistics for EVs is a primary focus, forcing companies to re-evaluate transport infrastructure and safety requirements for EV transport. The push for real-time visibility in automotive supply chains is a direct response to the need for greater control and predictability.

- Another critical area is reducing port congestion in vehicle logistics, a complex problem that impacts schedules and costs globally. Internally, firms are addressing the challenges of specialized driver shortages through recruitment initiatives and by exploring shunting process automation. For global vehicle distribution, selecting the right mix of multimodal transport is essential for balancing cost and speed.

- Technologically, digital twin applications in vehicle logistics offer powerful simulation capabilities for optimizing yard capacity with software and planning for disruptions. The pursuit of sustainable logistics for finished vehicles is no longer optional, influencing everything from fuel choices to carrier design. This involves managing fuel price volatility in transport while also improving the efficiency of ro-ro shipping.

- Automating vehicle movements in port terminals using lidar and computer vision helps improve throughput and safety. Firms that successfully integrate advanced car carrier design features and robust security protocols for high-value vehicles report a significant competitive advantage, reducing damage incidents by over 25% compared to industry averages.

What are the key market drivers leading to the rise in the adoption of Finished Vehicles Logistics Industry?

- The significant rise in electric vehicle production across major automotive manufacturing regions is a primary driver for the market.

- Market growth is fundamentally driven by the confluence of surging electric vehicle production, expanding international trade, and the unceasing demand for granular visibility.

- With global EV output reaching approximately 13 million units, the need for specialized outbound logistics optimization and adherence to new safety protocols has intensified.

- The expansion of cross-border trade facilitation, driven by new automotive manufacturing hubs, increases the complexity of the outbound supply chain and demand for robust end-to-end logistics services.

- Critically, over 80% of automotive manufacturers now consider real-time vehicle tracking a top priority, fueling investment in technologies that support lean inventory principles.

- This intense demand for data-driven oversight is forcing logistics providers to enhance their capabilities to ensure damage-free delivery and maintain a competitive edge in a dynamic global market.

What are the market trends shaping the Finished Vehicles Logistics Industry?

- A key market trend is the growing adoption of specialized electric vehicle haulage systems. These are designed to accommodate the unique physical properties of battery-powered cars.

- Key market trends are reshaping the operational landscape, with a strong focus on sustainability and automation. The adoption of specialized electric vehicle haulage is critical, as logistics providers invest in carriers designed to handle units weighing 20-30% more than conventional models. This shift toward zero-emission logistics is complemented by the integration of digital twin fleet management systems.

- These platforms enable companies to run simulations on carrier availability and route efficiency, improving delivery time accuracy by up to 15%. Furthermore, the implementation of autonomous yard management systems at vehicle processing centers is addressing labor shortages and improving safety.

- These trends collectively drive the digital logistics transformation, enhancing supply chain risk mitigation and supporting the industry's move toward more resilient and efficient operations through advanced fleet management software.

What challenges does the Finished Vehicles Logistics Industry face during its growth?

- A persistent shortage of qualified drivers trained to operate specialized car carriers presents a significant challenge to industry growth.

- The market faces significant operational headwinds that challenge efficiency and profitability. A critical issue is the persistent shortage of specialized transport drivers, with vacancy rates reaching nearly 15% in major regions, which directly constrains inland transport capacity and disrupts schedules. This labor shortage puts upward pressure on costs across the entire finished vehicle supply chain.

- Compounding this is the high volatility in fuel prices, which complicates logistics cost reduction efforts for both road and maritime transport. Furthermore, severe port and terminal congestion remains a major bottleneck, with average terminal dwell times at some major ports increasing to 14 days.

- This congestion not only delays shipments but also increases storage costs and the risk of vehicle damage, undermining supply chain resilience and complicating vehicle inventory management.

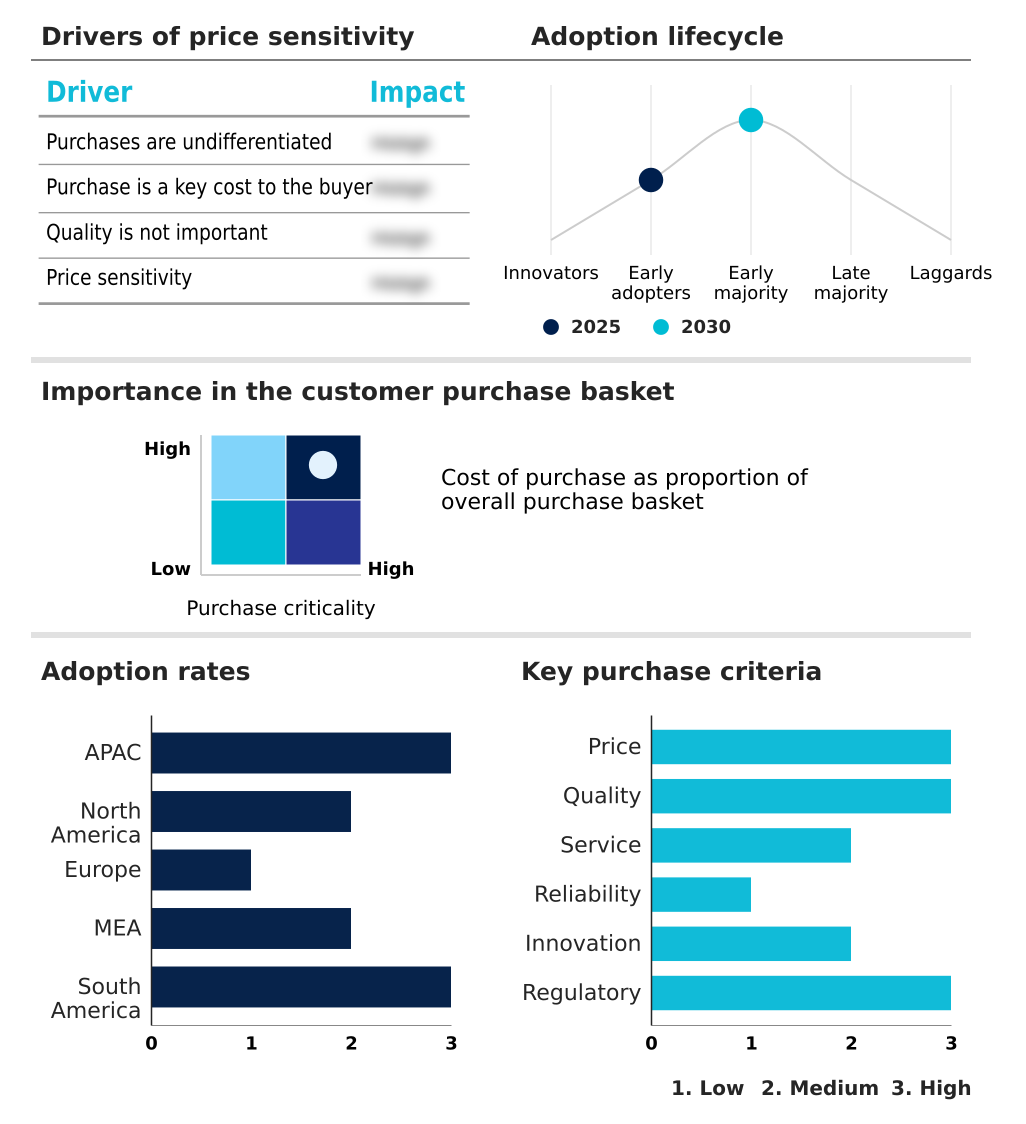

Exclusive Technavio Analysis on Customer Landscape

The finished vehicles logistics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the finished vehicles logistics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Finished Vehicles Logistics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, finished vehicles logistics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACERTUS - Provides a tech-enabled automotive logistics platform for end-to-end vehicle movement, storage, reconditioning, and registration, ensuring a seamless finished vehicle supply chain.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACERTUS

- AP Moller Maersk AS

- ARS Altmann AG

- Berge Logistics

- CMA CGM Group

- DHL International GmbH

- DP World

- DSV AS

- Ekol Lojistik AS

- Hellmann Worldwide Logistics

- Jack Cooper Logistics

- Koopman Logistics Group BV

- Kuehne Nagel Management AG

- Mitsui O.S.K. Lines Ltd.

- Nippon Express Holdings Inc.

- Omsan Lojistik AS

- Ryder System Inc.

- United Parcel Service Inc.

- Wallenius Wilhelmsen ASA

- XPO Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Finished vehicles logistics market

- In August 2024, Kuehne Nagel Management AG opened a new dedicated automotive logistics hub in the Middle East to support the growing regional demand for finished vehicle services.

- In September 2024, Ryder System Inc. introduced a new digital platform for managing outbound vehicle logistics from assembly plants, enhancing real-time visibility for manufacturers.

- In January 2025, Hellmann Worldwide Logistics SE and Co KG implemented a new artificial intelligence-based route optimization system for its vehicle haulage operations to improve efficiency.

- In May 2025, Nippon Express Holdings Inc. expanded its cross-border rail services for vehicles in Central Asia, strengthening its multimodal transport network in the region.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Finished Vehicles Logistics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.2% |

| Market growth 2026-2030 | USD 28506.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The finished vehicles logistics market is a highly specialized sector centered on the coordination of multimodal transport solutions, including roll-on roll-off shipping and high-capacity rail wagons, to ensure the efficient movement of vehicles.

- A core boardroom-level concern is the capital expenditure required for electric vehicle haulage, which involves fleet upgrades with specialized car carriers and investment in high-speed charging infrastructure to handle unique axle weight regulations and lithium-ion battery safety protocols.

- Operational integrity is maintained through advanced telematics and sensor networks, which feed data into cloud-based logistics platforms for real-time vehicle tracking and supply chain visibility. This addresses the demand for just-in-time delivery and lean inventory principles. Vehicle terminal operations are being transformed by automated damage inspection and vehicle storage yard optimization technologies.

- The market is also seeing a 15% increase in the utilization of specialized terminals equipped for EV maintenance. Strategic challenges include managing port and terminal congestion, navigating complex customs and documentation for cross-border trade, and mitigating the impact of a global shortage of specialized transport drivers, all while adhering to strict fire safety protocols.

What are the Key Data Covered in this Finished Vehicles Logistics Market Research and Growth Report?

-

What is the expected growth of the Finished Vehicles Logistics Market between 2026 and 2030?

-

USD 28.51 billion, at a CAGR of 5.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Road, Rail, Sea, and Air), Service (Warehousing, and Transport), Vehicle Type (Passenger cars, Light commercial vehicles, Heavy commercial vehicles, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rise in electric vehicle production, Shortage of specialized transport drivers

-

-

Who are the major players in the Finished Vehicles Logistics Market?

-

ACERTUS, AP Moller Maersk AS, ARS Altmann AG, Berge Logistics, CMA CGM Group, DHL International GmbH, DP World, DSV AS, Ekol Lojistik AS, Hellmann Worldwide Logistics, Jack Cooper Logistics, Koopman Logistics Group BV, Kuehne Nagel Management AG, Mitsui O.S.K. Lines Ltd., Nippon Express Holdings Inc., Omsan Lojistik AS, Ryder System Inc., United Parcel Service Inc., Wallenius Wilhelmsen ASA and XPO Inc.

-

Market Research Insights

- The finished vehicles logistics market is shaped by a convergence of operational demands and technological advancements. The need for supply chain resilience and logistics cost reduction is paramount, compelling firms to enhance their end-to-end logistics services.

- A critical dynamic is the push for greater transparency, with over 80% of manufacturers prioritizing real-time tracking, driving investment in sophisticated automotive logistics platform technology. This digital logistics transformation is essential for managing the complexities of global automotive trade.

- Concurrently, the industry faces significant labor constraints, evidenced by a driver vacancy rate nearing 15% in key regions, which impacts road haulage efficiency. The strategic selection of transport modes is also evolving, with an increased focus on sustainability and carbon footprint reduction influencing decisions across the finished vehicle supply chain.

We can help! Our analysts can customize this finished vehicles logistics market research report to meet your requirements.

RIA -

RIA -