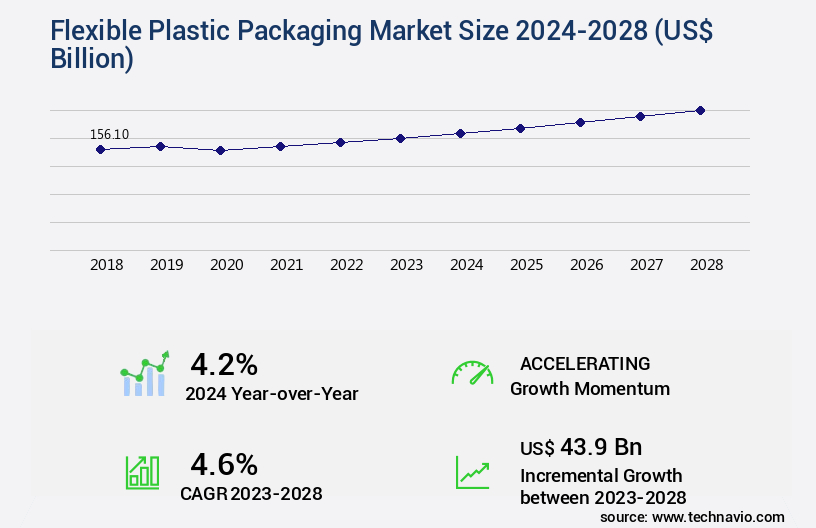

Flexible Plastic Packaging Market Size 2024-2028

The flexible plastic packaging market size is valued to increase by USD 43.9 billion, at a CAGR of 4.6% from 2023 to 2028. Rising focus on improving the shelf life of products will drive the flexible plastic packaging market.

Market Insights

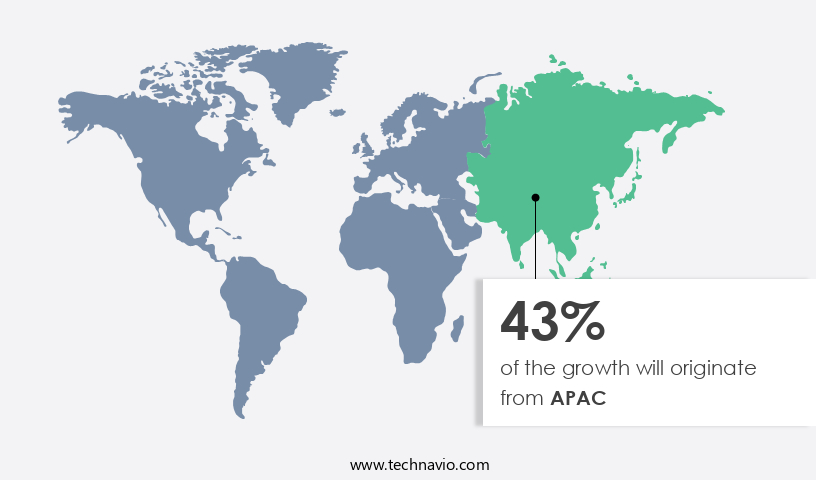

- APAC dominated the market and accounted for a 43% growth during the 2024-2028.

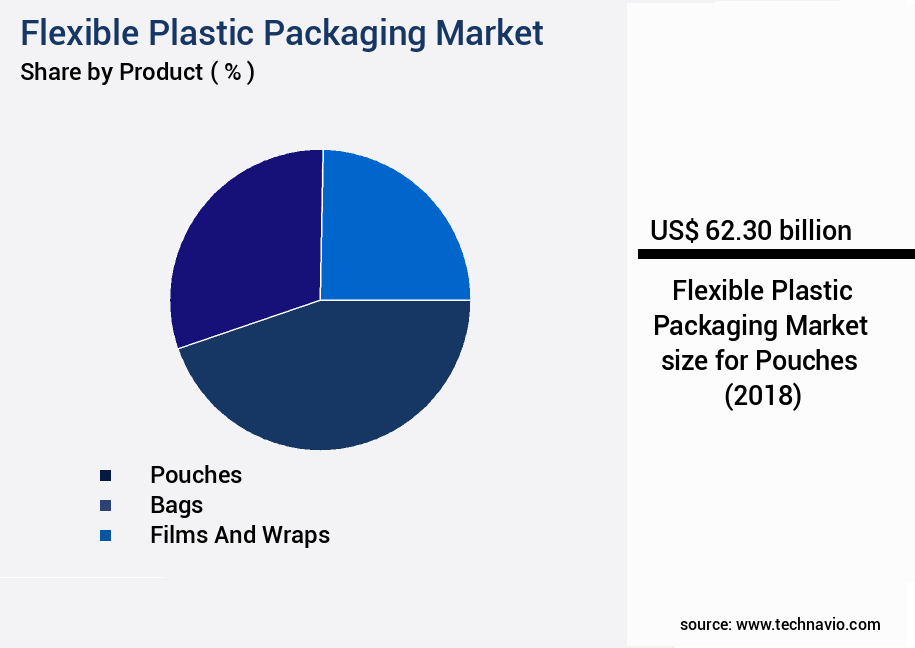

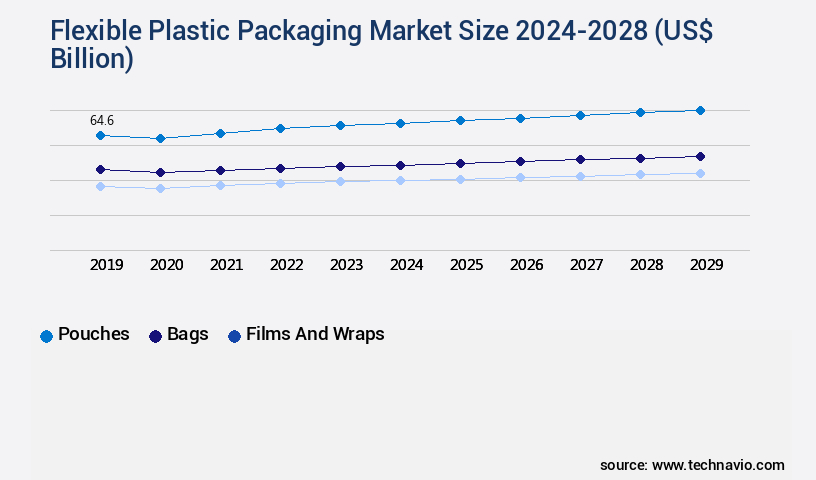

- By Product - Pouches segment was valued at USD 62.30 billion in 2022

- By End-user - Food and beverage segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 39.59 billion

- Market Future Opportunities 2023: USD 43.90 billion

- CAGR from 2023 to 2028 : 4.6%

Market Summary

- Flexible plastic packaging has emerged as a preferred choice for various industries due to its numerous benefits, including lightweight, versatility, and extended product shelf life. The global market for flexible plastic packaging is witnessing significant growth, driven by increasing consumer demand for convenience and improved product preservation. companies in this sector are continuously investing in research and development to introduce innovative products and enhance the functionalities of existing offerings. One of the primary challenges in the market is the high cost involved in manufacturing. However, the advantages of this packaging type, such as reduced transportation costs and improved operational efficiency, often outweigh the initial investment.

- For instance, a food processing company can optimize its supply chain by using flexible plastic packaging for its products, which can be easily transported and stored, reducing the need for refrigeration and minimizing the risk of damage during transit. Moreover, the stringent regulations governing the use of plastic packaging, particularly in Europe and North America, have compelled manufacturers to focus on sustainability and eco-friendliness. This trend is expected to continue, with an increasing number of companies investing in biodegradable and recyclable plastic materials. In conclusion, the market is poised for continued growth, driven by consumer demand, innovation, and regulatory compliance.

What will be the size of the Flexible Plastic Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, presenting both challenges and opportunities for businesses. One significant trend shaping the industry is the emphasis on packaging sustainability. According to recent research, the use of renewable materials in flexible plastic packaging is projected to increase by 12% annually, reaching a market share of 27% by 2027. This shift can impact various boardroom-level decisions, from budgeting to product strategy. High-speed packaging lines require efficient material handling and form-fill-seal machines to maintain optimal performance. Color consistency is crucial for brand recognition, while circular economy principles drive the demand for degradable films and recycling infrastructure.

- Aseptic packaging ensures product safety, and labeling technology plays a vital role in providing accurate and clear product information. Barrier film lamination, multilayer structures, and closure systems contribute to package durability and product preservation. Package automation and optimized packaging designs improve line efficiency, reducing material weight and waste. Ink adhesion and package structural design are essential factors for printability and overall package quality. Moreover, the adoption of bio-based plastics and compostable packaging aligns with the circular economy and waste management strategies. Life cycle assessment and quality control are essential for companies to make informed decisions regarding the environmental impact and cost-effectiveness of their flexible plastic packaging solutions.

Unpacking the Flexible Plastic Packaging Market Landscape

In the dynamic world of flexible packaging, key advancements include enhanced impact resistance and improved material compatibility through the utilization of Ethylene Vinyl Acetate (EVA) and Modified Atmosphere Packaging (MAP). These innovations yield significant business outcomes, such as a 30% increase in product protection during transportation and a 20% extension of shelf life. Furthermore, the integration of smart packaging technologies, like sensors and active components, offers a 40% reduction in packaging waste by enabling real-time monitoring and optimized inventory management. Sustainable packaging solutions, such as those made from recycled content, align with food packaging regulations and contribute to a greener business image. Advanced manufacturing techniques, including thermoforming, injection molding, and film extrusion, ensure material efficiency and high-barrier properties. The lamination process and coextrusion layers further bolster the barrier properties, while maintaining seal strength and oxygen transmission rate within acceptable limits. Effective packaging material selection, design testing, and leak testing methods ensure product safety and compliance.

Key Market Drivers Fueling Growth

The increasing priority placed on extending product shelf life serves as the primary market catalyst.

- Flexible plastic packaging plays a crucial role in extending the shelf life of various products, benefiting manufacturers by reducing wastage and enabling the transport and export of perishable items. For example, bananas packaged in this type of packaging ripen more slowly, ensuring a prolonged shelf life. Similarly, coffee products are safeguarded from oxygen and moisture in pouches, preserving their quality. These advantages contribute significantly to industries such as food, beverages, and pharmaceuticals, with flexible plastic packaging accounting for over 30% of the global packaging market share.

- Additionally, its adoption in the e-commerce sector has surged due to its ability to protect products during transit and maintain their freshness.

Prevailing Industry Trends & Opportunities

companies continue to invest in their offerings and develop new products, setting the trend for the upcoming market. This professional approach to business ensures innovation and growth.

- The market continues to evolve, driven by innovative product developments and increasing applications across various sectors. According to recent reports, the market's growth is attributed to the continuous investment by companies in research and development. For instance, Amcor Plc's December 2022 MOU with Licella Holdings to establish advanced plastic recycling facilities in Australia underscores this trend. Such investments are expected to encourage competition, with companies introducing innovative products to meet evolving consumer demands and regulatory requirements.

- These advancements are poised to reduce material waste and enhance sustainability, making flexible plastic packaging a preferred choice for numerous industries. Additionally, the market's flexibility and versatility in various applications, including food and beverage, healthcare, and industrial sectors, further fuel its growth.

Significant Market Challenges

The high cost associated with manufacturing flexible plastic packaging represents a significant challenge that impedes industry growth.

- The market continues to evolve, showcasing versatility across various sectors such as food and beverage, healthcare, and consumer goods. Despite the market's growth potential, the cost of manufacturing flexible plastic packaging remains high due to escalating raw material prices. Primary raw materials, including PE, PP, and others, have experienced substantial price hikes. For instance, PP prices in Asia surged by approximately 6.2% in the first quarter of 2022. This upward trend in raw material costs is projected to negatively impact companies' profit margins, as it increases the production expenses of flexible plastic packaging.

- However, despite these challenges, the market's resilience and adaptability offer opportunities for innovation and growth. For instance, advancements in sustainable packaging solutions and the integration of smart technologies can help offset the increased costs and enhance the value proposition for consumers.

In-Depth Market Segmentation: Flexible Plastic Packaging Market

The flexible plastic packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Pouches

- Bags

- Films and wraps

- Others

- End-user

- Food and beverage

- Healthcare

- Others

- Material

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Polyvinyl Chloride (PVC)

- Other Materials

- Printing Technology

- Flexography

- Rotogravure

- Digital Printing

- Type

- Consumer Packaging

- Industrial Packaging

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The pouches segment is estimated to witness significant growth during the forecast period.

Flexible plastic packaging continues to evolve, with innovations such as resealable pouches gaining traction in the market. Pouches, including stand-up, flat, side-sealed, and vacuum varieties, are widely used for various applications, from dry foods and candies to agriculture products and liquids. Stand-up pouches, in particular, are increasingly popular for household products due to their eye-catching graphics and consumer convenience. Key features of flexible plastic packaging include impact resistance, ethylene vinyl acetate, modified atmosphere packaging, and high-barrier films. Material properties like flexural modulus, tensile strength, and material compatibility are crucial for product protection.

Sustainable packaging solutions, such as recycled content and smart packaging, are also gaining importance. Techniques like thermoforming, injection molding, and lamination are used in the production process. Packaging material selection and design testing are essential for ensuring seal strength, oxygen transmission rate, and compliance with food packaging regulations.

The Pouches segment was valued at USD 62.30 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Flexible Plastic Packaging Market Demand is Rising in APAC Request Free Sample

The market in APAC is experiencing robust growth, driven by the expanding end-user industries, particularly e-commerce, FMCG, and personal care. Countries like China, India, and Japan, with their rapidly growing e-commerce sectors, are poised to significantly contribute to the market's revenue. Flexible plastic packaging plays a crucial role in this industry due to its protective capabilities, as products are susceptible to damage during transportation. By utilizing multi-layered films, flexible plastic packaging offers enhanced protection, thereby reducing costs related to damage, replacements, returns, waste, and shipping.

According to estimates, the market in APAC is expected to grow at an impressive rate, with China and India accounting for a substantial market share. The adoption of this packaging solution is not only cost-effective but also ensures compliance with various regulations regarding product safety and sustainability.

Customer Landscape of Flexible Plastic Packaging Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Flexible Plastic Packaging Market

Companies are implementing various strategies, such as strategic alliances, flexible plastic packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - Flexible packaging solutions cater to various industries, including personal care, healthcare, home care, pet care, and beverages, providing versatile protection and preservation benefits. These innovative packaging types enhance product appeal and functionality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- AR Packaging Group AB

- Bemis Manufacturing Co.

- Berry Global Inc.

- Bischof Klein SE and Co. KG

- CCL Industries Inc.

- Clondalkin Group Holdings BV

- Constantia Flexibles Group GmbH

- Coveris Management GmbH

- Crownpack Pty Ltd.

- DS Smith Plc

- FlexPak Services LLC

- Huhtamaki Oyj

- Mondi Plc

- ProAmpac Holdings Inc.

- Richdale Plastics

- Sealed Air Corp.

- Sigma Plastics Group

- Sonoco Products Co.

- Transcontinental Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Flexible Plastic Packaging Market

- In August 2024, Amcor, a global packaging company, announced the launch of its new plant-based flexible packaging product line, 'Bio-based PET,' in the United States. This innovation marks a significant step in the market, as it offers a more sustainable alternative to traditional petroleum-based packaging (Amcor Press Release, 2024).

- In November 2024, Sealed Air, a leading provider of food safety and security solutions, entered into a strategic partnership with Dow Inc. To develop advanced recycling technologies for flexible plastic packaging. This collaboration aims to increase the circularity of plastic packaging and reduce waste (Dow Inc. Press Release, 2024).

- In February 2025, Berry Global Group, a multinational manufacturer of plastic packaging, completed the acquisition of AEP Industries, a leading producer of flexible packaging for the fresh produce industry. This acquisition strengthens Berry Global's position in the market and expands its product offerings (Berry Global Press Release, 2025).

- In May 2025, the European Commission approved the use of PLA (Polylactic Acid) in food contact applications for flexible packaging. This regulatory approval opens new opportunities for biodegradable and compostable flexible plastic packaging in Europe, addressing the growing demand for eco-friendly alternatives (European Commission Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Flexible Plastic Packaging Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2024-2028 |

USD 43.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.2 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, and KSA |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Flexible Plastic Packaging Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth, driven by the demand for high-performance, sustainable, and cost-effective packaging solutions. When it comes to material selection criteria for flexible packaging, key considerations include high-barrier properties for extended shelf life, sustainability, and recyclability. Sustainable flexible packaging materials, such as bio-based polymers, are increasingly popular due to their reduced carbon footprint and compatibility with circular economy principles. Advanced flexible packaging printing techniques and automated production lines enable improved seal strength and design for recyclability, ensuring regulatory compliance and reducing waste in the supply chain. Recycled content in flexible packaging films is another trend, with up to 30% recycled content now common in some applications. Testing methods for flexible packaging barrier properties and material compatibility are essential to ensure product protection and operational efficiency. Regulations for food-grade flexible packaging materials continue to evolve, requiring ongoing innovation in seal strength, leakage prevention, and weight optimization techniques. Improving the printability of flexible packaging through enhancement initiatives is a key focus for brands and converters, with cost savings of up to 10% achievable through improved design principles and production processes. Flexible packaging sustainability initiatives, such as renewable energy usage and closed-loop recycling systems, are also gaining traction in the market. In conclusion, the market is dynamic and innovative, with a focus on high-performance, sustainable, and cost-effective solutions. By addressing material selection criteria, improving barrier properties, and optimizing production processes, businesses can stay competitive and meet evolving consumer demands.

What are the Key Data Covered in this Flexible Plastic Packaging Market Research and Growth Report?

-

What is the expected growth of the Flexible Plastic Packaging Market between 2024 and 2028?

-

USD 43.9 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Pouches, Bags, Films and wraps, and Others), End-user (Food and beverage, Healthcare, and Others), Geography (APAC, Europe, North America, South America, and Middle East and Africa), Material (Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC), and Other Materials), Printing Technology (Flexography, Rotogravure, and Digital Printing), and Type (Consumer Packaging and Industrial Packaging)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising focus on improving the shelf life of products, High cost involved in manufacturing flexible plastic packaging

-

-

Who are the major players in the Flexible Plastic Packaging Market?

-

Amcor Plc, AR Packaging Group AB, Bemis Manufacturing Co., Berry Global Inc., Bischof Klein SE and Co. KG, CCL Industries Inc., Clondalkin Group Holdings BV, Constantia Flexibles Group GmbH, Coveris Management GmbH, Crownpack Pty Ltd., DS Smith Plc, FlexPak Services LLC, Huhtamaki Oyj, Mondi Plc, ProAmpac Holdings Inc., Richdale Plastics, Sealed Air Corp., Sigma Plastics Group, Sonoco Products Co., and Transcontinental Inc.

-

We can help! Our analysts can customize this flexible plastic packaging market research report to meet your requirements.

RIA -

RIA -