Food Wrapping Paper Market Size 2024-2028

The food wrapping paper market size is valued to increase by USD 1.32 billion, at a CAGR of 5.23% from 2023 to 2028. Growing demand for sustainable food packaging will drive the food wrapping paper market.

Market Insights

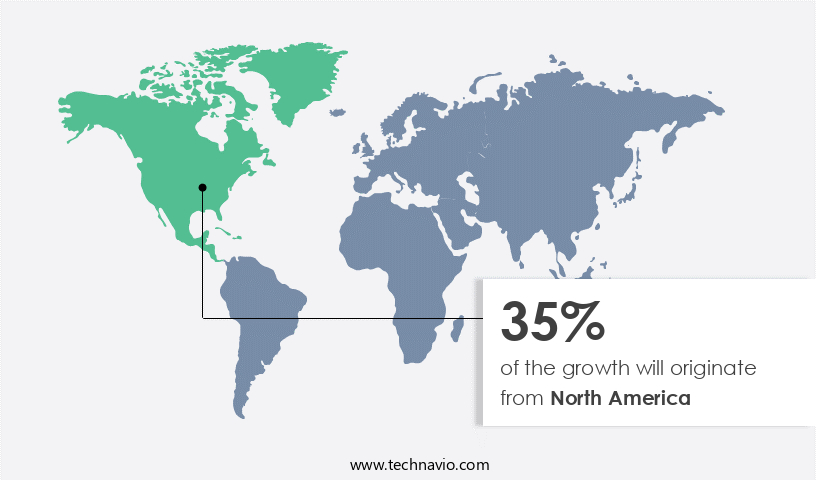

- North America dominated the market and accounted for a 35% growth during the 2024-2028.

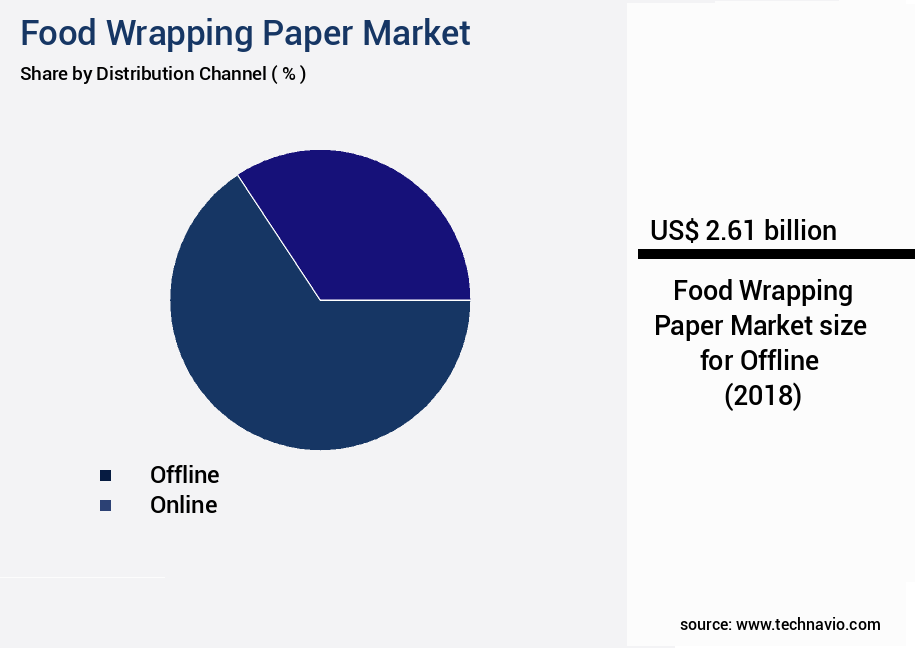

- By Distribution Channel - Offline segment was valued at USD 2.61 billion in 2022

- By Product Type - Wrapping Paper segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 48.35 billion

- Market Future Opportunities 2023: USD 1.32 billion

- CAGR from 2023 to 2028 : 5.23%

Market Summary

- The market witnesses significant growth driven by the increasing demand for sustainable food packaging solutions. Consumers are increasingly conscious of the environmental impact of their choices, leading to a surge in demand for eco-friendly food wrapping paper made from renewable resources such as sugarcane bagasse, maize, and wheat straw. Additionally, the adoption of innovative materials like biodegradable plastics, PLA (polylactic acid), and nanotechnology in food wrapping paper production is revolutionizing the industry. However, the market faces challenges due to the rise in prices of raw materials such as pulp and petroleum, which are essential for the manufacturing of food wrapping paper.

- The supply chain optimization becomes crucial for companies to mitigate the impact of these price fluctuations. For instance, a food processing company may partner with multiple suppliers to ensure a steady supply of raw materials and maintain operational efficiency. Moreover, regulatory compliance is another critical factor influencing the market. Governments worldwide are implementing stringent regulations to reduce plastic waste and promote sustainable packaging. Companies must invest in research and development to create compliant food wrapping paper that meets the evolving regulatory landscape while maintaining the required functionality and shelf life.

What will be the size of the Food Wrapping Paper Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with a growing emphasis on sustainability and reducing carbon footprint. According to recent research, the use of renewable resources in food wrapping paper production has increased by 25% over the past five years. This trend is driven by consumer demand for eco-friendly packaging solutions and regulatory compliance. Sustainable product labeling and waste management are key considerations for companies in this market. Life cycle assessment plays a crucial role in determining the environmental impact of food wrapping paper. Bio-based polymers, recycling programs, and storage conditions are essential factors in ensuring product quality and shelf life.

- Ink adhesion, material sourcing, and paper grades are critical aspects of manufacturing processes. Surface treatment, color accuracy, and distribution logistics are essential for maintaining quality control and assurance. Film extrusion and coating application are crucial manufacturing processes that impact product efficiency and print quality. Consumer testing is a vital component of product strategy, with companies investing in shelf life studies to ensure their food wrapping paper meets consumer expectations. Raw material costs and packaging efficiency are essential budgeting considerations. The market is a dynamic and competitive landscape, with companies continually seeking to improve their manufacturing processes and product offerings to meet evolving consumer demands and regulatory requirements.

Unpacking the Food Wrapping Paper Market Landscape

The market encompasses a diverse range of products engineered to safeguard and enhance food items. Key performance indicators include UV resistance for maintaining product quality and shelf life extension through impeding light penetration. Moisture vapor transmission rates are crucial for preventing spoilage and ensuring consumer safety. Labeling requirements dictate the use of printing inks that adhere to food safety standards, while seal integrity is vital for maintaining product protection. Barrier properties such as oxygen permeability and microbial barriers play a significant role in preserving food freshness and prolonging shelf life. Supply chain optimization and converting processes are essential for efficient production and timely delivery. Sustainability metrics, including recycling infrastructure, compostable films, and biodegradable materials, are increasingly important to meet evolving consumer preferences. Printing techniques, water resistance, and laminating techniques contribute to superior product presentation and protection. Aroma protection is a key consideration for sensitive food items, while thermal resistance and grease resistance are essential for various food applications. Roll stock handling and tear resistance ensure ease of use and convenience for food manufacturers and retailers. Waste reduction strategies, such as recycled paper content and recycling infrastructure, are increasingly important for companies seeking to minimize their environmental footprint.

Key Market Drivers Fueling Growth

The increasing demand for eco-friendly food packaging solutions is the primary market driver, reflecting growing consumer consciousness towards reducing waste and minimizing the environmental impact of packaging.

- The market is experiencing significant evolution due to growing environmental concerns and shifting consumer preferences. Traditional materials like polystyrene and polypropylene, used in food service disposables, face criticism for their long decomposition times and resulting pollution. In response, companies are offering eco-friendly packaging solutions, utilizing compostable raw materials for food wrapping paper production. This shift has led to a surge in demand for paper-based packaging.

- Notably, paper packaging offers advantages beyond sustainability. Its recyclability sets it apart from metals and plastics, making it a cost-effective and environmentally friendly choice. This trend is reflected in the increasing adoption of paper-based packaging in various sectors, resulting in energy savings of up to 12% and reduced waste generation.

Prevailing Industry Trends & Opportunities

The use of innovative materials is becoming mandatory in the manufacturing process for food wrapping paper. This trend is shaping the market.

- The market is experiencing notable growth due to the increasing demand for eco-friendly and sustainable packaging solutions across various sectors. Manufacturers are turning to plant-based raw materials, such as grass, hemp, and bamboo, to produce food wrapping paper. For instance, hemp, a versatile raw material, can significantly reduce waste during processing, making it an attractive choice for sustainable packaging production. Constantia Flexibles Group GmbH, a leading player, produces grass-based food wrapping paper without bleach or chemical treatments, using minimal water consumption.

- Another player in the market, unspecified, has reported a reduction of up to 25% in production costs by adopting hemp-based raw materials. These eco-friendly initiatives are expected to boost the market's growth in the coming years. Additionally, the adoption of these sustainable packaging solutions is projected to increase by 15% in the food service industry alone.

Significant Market Challenges

The food wrapping paper industry faces significant challenges due to rising costs of raw materials, which poses a substantial obstacle to industry growth.

- The market continues to evolve, with applications expanding across various sectors including food service, retail, and industrial packaging. A significant component of food wrapping paper manufacturing involves the use of paper pulp, primarily sourced from wood pulp. The producer price index (PPI) for pulp, paper, and allied products experienced a substantial increase, reaching 198.59 in October 2023 compared to 139.80 in October 2020. This price surge can be attributed to rising transportation costs, as paper and paper products are transported globally.

- The increased prices have resulted in operational cost implications for manufacturers. For instance, a 60% increase in paper prices could lead to a 12% increase in overall production costs. Despite these challenges, the market remains dynamic, with innovations in sustainable materials and advanced printing technologies driving growth.

In-Depth Market Segmentation: Food Wrapping Paper Market

The food wrapping paper industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Distribution Channel

- Offline

- Online

- Product Type

- Wrapping Paper

- Food Bags

- Food Wraps

- Others

- Material Type

- Paper

- Plastic

- Aluminum Foil

- Biodegradable Materials

- Application

- Food Service

- Retail

- Household

- Commercial Packaging

- End-User

- Restaurants & Cafes

- Supermarkets

- Food Manufacturers

- Households

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

In the dynamic the market, the demand for advanced packaging solutions continues to evolve. UV resistance and moisture vapor transmission are crucial factors in ensuring shelf life extension. Labeling requirements and printing inks play a significant role in meeting consumer preferences. Oxygen permeability, recycling infrastructure, and microbial barrier are essential considerations for maintaining food safety standards. Supply chain optimization, aroma protection, and product protection are key areas of focus for manufacturers. Packaging machinery and design are critical components of the production process, with an emphasis on seal integrity, material strength, and barrier properties. Converting processes and paper coatings are also essential for creating high-quality, functional wrapping paper.

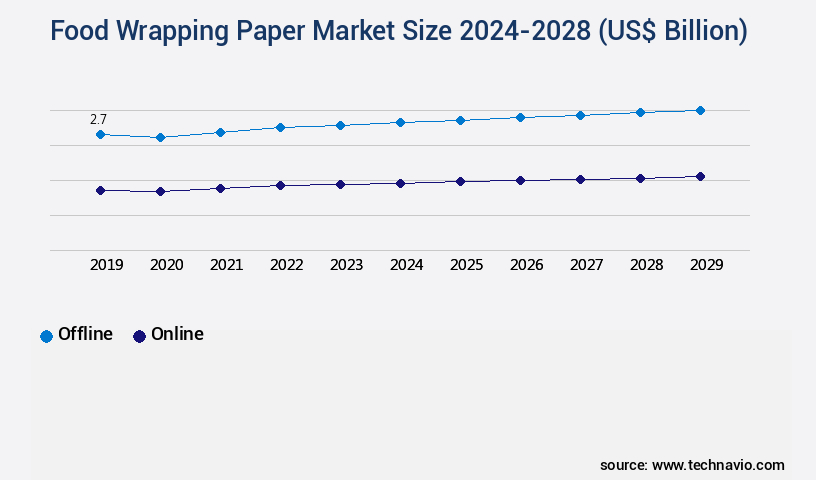

Sustainability metrics, such as compostable films and biodegradable materials, are increasingly important to consumers. In the 2024-2028 period, offline sales channels will continue to account for a significant portion of market share, with traditional retailers and wholesale distributors playing vital roles. Approximately 70% of food wrapping paper sales are estimated to occur through these channels. Manufacturers, distributors, and customers will continue to engage in face-to-face interactions at trade shows and exhibits to build relationships and showcase new products.

The Offline segment was valued at USD 2.61 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Food Wrapping Paper Market Demand is Rising in North America Request Free Sample

The North American the market is experiencing steady expansion, driven by the dynamic foodservice industry and increasing consumer preference for convenient food options. The US dominates this market due to the presence of numerous restaurants and fast-food chains. According to industry reports, the foodservice industry in the US is projected to grow at a steady pace, with an estimated 4-5% annual increase in the number of restaurants from 2021 to 2026. In this context, the market is poised to benefit significantly from the rising demand for disposable packaging solutions. Furthermore, the market in Mexico and Canada is also growing, fueled by their expanding foodservice sectors, which include various types of restaurants and hotels.

For instance, Dominos Pizza Inc. Reported a net store growth of 468 stores in the fourth quarter of their fiscal year 2021, with 89 new stores in the US and 379 net international store openings. The market's growth is also influenced by the need for operational efficiency and cost reduction, as food wrapping paper offers a more cost-effective alternative to traditional packaging methods while ensuring food safety and compliance with regulations.

Customer Landscape of Food Wrapping Paper Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Food Wrapping Paper Market

Companies are implementing various strategies, such as strategic alliances, food wrapping paper market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - This company specializes in providing food wrapping solutions through innovative products such as Food Wrapping paper, Eco wraps, and Grease proof paper. Their offerings prioritize sustainability and functionality, setting industry standards.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Anchor Packaging

- Ardagh Group

- Berry Global Inc.

- BillerudKorsnäs AB

- Dart Container Corporation

- Duni Group

- Georgia-Pacific LLC

- Huhtamaki Oyj

- International Paper Company

- Intertek Group Plc

- Mondi Plc

- Novolex

- Reynolds Consumer Products

- Sealed Air Corporation

- Smurfit Kappa Group

- Tetra Pak International S.A.

- Toyo Seikan Group Holdings

- Uflex Ltd.

- WestRock Company

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Food Wrapping Paper Market

- In January 2025, Sealed Air Corporation, a leading global provider of food safety and security solutions, announced the launch of its new line of advanced food wrapping papers infused with antimicrobial technology. This innovation aims to extend the shelf life of food products and reduce food waste (Sealed Air Corporation Press Release).

- In March 2025, Amcor plc, a global packaging company, entered into a strategic partnership with Danish food packaging firm, Tetra Pak, to expand their joint offerings in sustainable food packaging solutions. This collaboration will combine Amcor's expertise in flexible packaging with Tetra Pak's knowledge in aseptic carton packaging (Amcor plc Press Release).

- In April 2025, Sonoco Products Company, a leading provider of consumer packaging, completed the acquisition of C&M Containers, a leading manufacturer of paper-based food containers. This acquisition will enable Sonoco to expand its product offerings and strengthen its position in the food packaging market (Sonoco Products Company Press Release).

- In May 2025, the European Union (EU) approved a new regulation on single-use plastics, which includes food wrapping papers. The regulation aims to reduce the usage of single-use plastics by 50% by 2030, driving the demand for biodegradable and compostable food wrapping papers (European Commission Press Release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Food Wrapping Paper Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.23% |

|

Market growth 2024-2028 |

USD 1.32 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.75 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Food Wrapping Paper Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market encompasses a range of packaging solutions designed to protect and preserve various food items. Paperboard packaging materials, with their desirable properties such as strength and durability, form the basis of many food wrapping applications. However, to effectively safeguard food from external elements, these materials often undergo enhancements like greaseproof paper coatings and high-barrier food packaging films. Sustainability is a significant trend in the market, with increasing demand for sustainable compostable food wraps and those containing recycled content. These eco-friendly alternatives not only cater to consumer perception but also contribute to reducing food waste and optimizing supply chain operations. Water-resistant paper and films with oxygen barrier properties are essential for maintaining food freshness and extending shelf life. Food safety regulations mandate stringent requirements for paper packaging materials, ensuring microbial barrier properties and safe production methods. Printing techniques play a crucial role in food packaging design, allowing for vibrant branding and essential labeling information. Cost-effective sustainable packaging solutions are increasingly popular, with improved seal integrity reducing the need for excessive materials and minimizing wastage. Testing methods are essential to ensure the quality and performance of food packaging materials. Biodegradable alternatives to plastic films, such as paper-based packaging, are gaining traction as more businesses seek to improve their sustainability profiles. Paper-based packaging machinery operations must be efficient and adaptable to accommodate various paper types and printing methods. Labeling requirements for food packaging are rigorous, necessitating precise machinery and adhesive applications. In comparison to traditional plastic films, paper-based food wrapping solutions offer a more sustainable and eco-friendly alternative, reducing reliance on non-renewable resources and contributing to a more circular economy. This shift not only addresses consumer demands for sustainable packaging but also streamlines operational planning and compliance within the food industry.

What are the Key Data Covered in this Food Wrapping Paper Market Research and Growth Report?

-

What is the expected growth of the Food Wrapping Paper Market between 2024 and 2028?

-

USD 1.32 billion, at a CAGR of 5.23%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline and Online), Product Type (Wrapping Paper, Food Bags, Food Wraps, and Others), Geography (North America, Europe, APAC, Middle East and Africa, and South America), Material Type (Paper, Plastic, Aluminum Foil, and Biodegradable Materials), Application (Food Service, Retail, Household, and Commercial Packaging), and End-User (Restaurants & Cafes, Supermarkets, Food Manufacturers, and Households)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing demand for sustainable food packaging, Increase in prices of raw materials for food wrapping paper

-

-

Who are the major players in the Food Wrapping Paper Market?

-

Amcor Plc, Anchor Packaging, Ardagh Group, Berry Global Inc., BillerudKorsnäs AB, Dart Container Corporation, Duni Group, Georgia-Pacific LLC, Huhtamaki Oyj, International Paper Company, Intertek Group Plc, Mondi Plc, Novolex, Reynolds Consumer Products, Sealed Air Corporation, Smurfit Kappa Group, Tetra Pak International S.A., Toyo Seikan Group Holdings, Uflex Ltd., and WestRock Company

-

We can help! Our analysts can customize this food wrapping paper market research report to meet your requirements.

RIA -

RIA -