Functional Flours Market Size 2024-2028

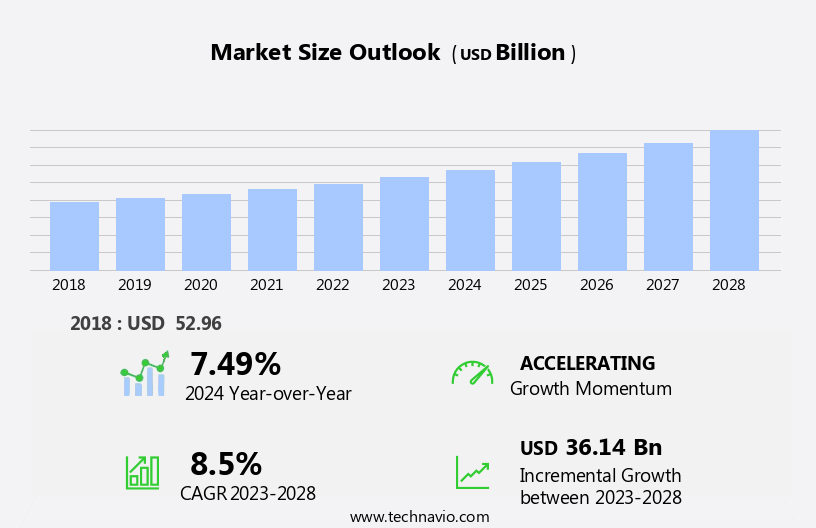

The functional flours market size is forecast to increase by USD 36.14 billion, at a CAGR of 8.5% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing demand for ready-to-eat food products from manufacturers. This trend is driven by consumers' preference for convenience and healthier food options. Consumers are increasingly seeking fiber-rich and nutrient-dense alternatives to traditional wheat, leading to a rise in demand for functional flours fortified with vitamins, herbs, nutraceuticals, and other health-promoting ingredients. Furthermore, innovations in functional flour blends are providing new opportunities for market expansion. However, the market faces challenges due to fluctuations in the availability of raw materials for functional flours. Weather conditions and natural calamities can significantly impact the production of key raw materials, leading to supply chain disruptions and price volatility.

- To capitalize on market opportunities and navigate these challenges effectively, companies must focus on supply chain resilience and diversification of raw material sources. Additionally, investing in research and development to create innovative functional flour blends can help differentiate offerings and cater to evolving consumer preferences.

What will be the Size of the Functional Flours Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

Functional flours continue to revolutionize the baking industry, with their unique properties and applications driving market dynamics. These innovative flours offer enhanced water absorption capacity, improved fiber enrichment methods, and superior bread making properties. Consumer acceptance testing and quality control metrics play a crucial role in ensuring the optimal sensory experience. Flour milling technology advances, enabling the production of specialized pastry flours with distinct characteristics. Ingredient cost analysis and product development lifecycle are essential considerations in the evolving market landscape. Starch modification techniques offer opportunities for enhanced ingredient functionality and nutritional labeling regulations. Functional flour applications span various sectors, from baked goods to beverages and supplements.

Ingredient sourcing strategies, food safety standards, and ingredient traceability systems are paramount in maintaining consumer trust and regulatory compliance. Colorimetric analysis techniques and dough rheology testing provide valuable insights into flour quality and baking performance indices. Flour storage conditions and process optimization strategies further contribute to the cost-effectiveness and efficiency of functional flour production. Continuous innovation in functional flours is fueled by ongoing research and development, with a focus on improving texture analysis methods, microscopic analysis techniques, protein content analysis, and gluten-free flours. The market's dynamic nature underscores the importance of staying informed and adaptive to meet the ever-evolving needs of consumers and industries.

How is this Functional Flours Industry segmented?

The functional flours industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- RTE products

- Bakery products

- Soups and sauces

- Others

- Type

- Fortified

- Specialty

- Pre-cooked

- Source

- Cereals (Wheat, Rice, Corn, Oats, Barley)

- Legumes (Chickpea, Lentil, Pea, Bean)

- Oilseeds (Soy, Flaxseed)

- Nuts (Almond, Coconut)

- Pseudocereals (Quinoa, Buckwheat, Amaranth)

- Nature

- Organic

- Conventional

- Function

- Thickening

- Binding

- Emulsifying

- Texturizing

- Nutritional Enrichment

- Shelf Life Extension

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

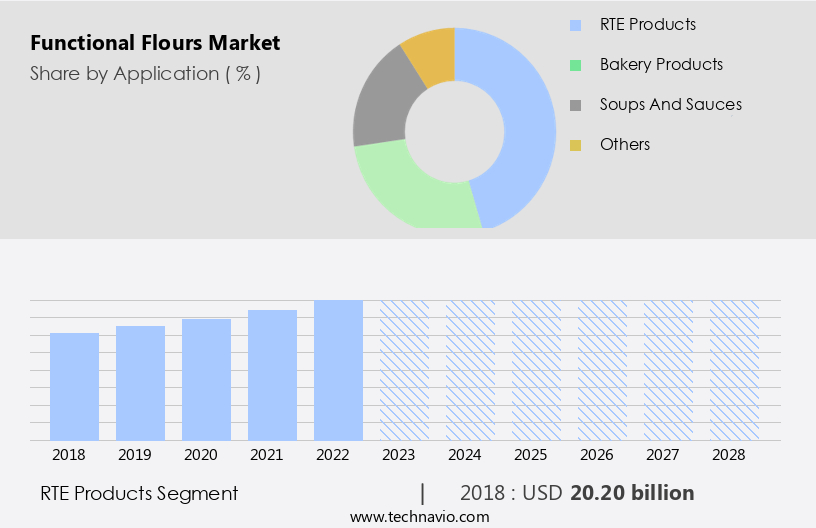

The RTE products segment is estimated to witness significant growth during the forecast period.

Functional flours have gained significant attention in the food industry due to consumers' increasing preference for healthier options. Manufacturers are leveraging functional flours to produce various snack foods, such as extruded snacks, with improved nutritional content. For instance, HOMECRAFT Pulse Flours from Ingredion is a functional flour suitable for ready-to-eat (RTE) products like snacks and pasta. The demand for functional flour in snack applications is surging due to consumers' quest for breakfast products with enhanced protein, fiber, and energy sources. Nutritional labeling is a crucial factor for consumers, who carefully read and consider the claims on product labels. Manufacturers employ various fiber enrichment methods to produce functional flours, ensuring they meet the nutritional demands of consumers.

Quality control metrics, such as protein content analysis and dough rheology testing, are essential to maintain consistency in the production process. Flour milling technology plays a pivotal role in producing functional flours with desirable bread making properties and water absorption capacity. Texture analysis methods, microscopic analysis techniques, and sensory evaluation methods are used to assess the functionality and overall quality of functional flours. In the baking industry, functional flour applications include pastry flour, which offers improved texture and baking performance indices. Cost-effectiveness analysis and supply chain management are essential considerations for manufacturers to ensure the competitiveness of their functional flour products.

Food safety standards and ingredient traceability systems are essential for maintaining consumer trust and regulatory compliance. Starch modification techniques, such as enzymatic modification and physical modification, are used to enhance the functionality of functional flours. Gluten-free baking formulations and functional flour blends cater to the growing demand for gluten-free food options. Product development lifecycle, from ingredient sourcing strategies to process optimization strategies, is a critical aspect of manufacturing functional flours. Flour storage conditions and flour oxidation control are essential to maintain the quality and functionality of functional flours throughout the production process.

The RTE products segment was valued at USD 20.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

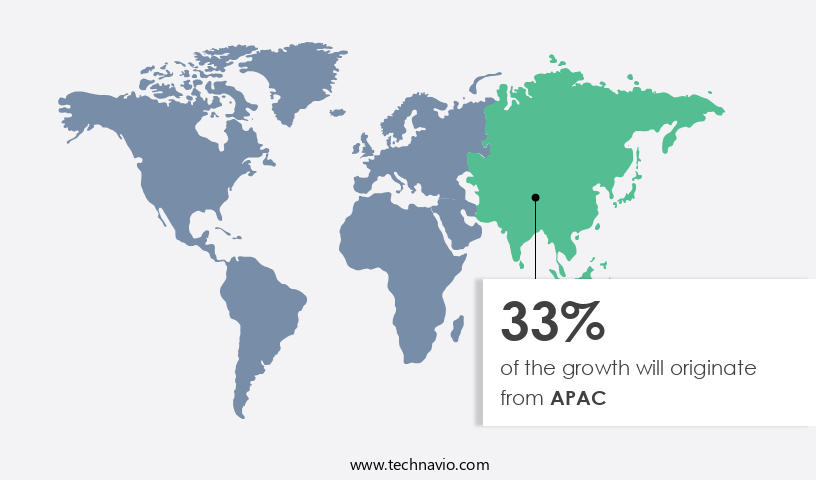

APAC is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in Asia Pacific (APAC) exhibits rapid growth, surpassing other regions. Japan and Australia lead the consumption of functional flours due to a thriving food processing industry, expanding population, and rising demand for ready-to-eat (RTE) food products. The bread and rolls market's expansion, driven by urbanization and the preference for convenience and gluten-free options, significantly contributes to the market's growth. The APAC bread market's growth rate surpasses that of Europe. Water absorption capacity, fiber enrichment methods, and consumer acceptance testing are crucial factors in functional flour production. Quality control metrics, packaging material selection, and flour milling technology are essential for maintaining product consistency.

Starch modification techniques and nutritional labeling regulations impact ingredient cost analysis and product development lifecycle. Supply chain management, texture analysis methods, microscopic analysis techniques, and sensory evaluation methods ensure product quality and consumer satisfaction. Gluten-free baking formulations, functional flour blends, and ingredient sourcing strategies cater to diverse consumer needs. Food safety standards, ingredient traceability systems, colorimetric analysis techniques, dough rheology testing, and functional flour applications expand the market's scope. Protein content analysis, process optimization strategies, baking performance indices, and flour storage conditions are essential for optimizing product functionality. Flour oxidation control is a critical aspect of maintaining product quality and shelf life.

Market Dynamics

The Functional Flours Market is booming as consumers demand healthier, sustainable options like gluten-free flours and organic functional flours. Functional flours in bakery and functional flours in snacks cater to functional flours for health-conscious consumers, while functional flours clean label and Non-GMO functional flours appeal to those seeking transparency. Functional flours high-protein and functional flours low-carb support functional flours for vegan diets and functional flours for gluten-free diets, driving growth in the functional flours gluten-free market and functional flours organic market. Innovations in functional flour processing and functional flours sustainable production enhance quality, with best functional flours for gluten-free baking and functional flours for plant-based nutrition meeting diverse dietary needs, ensuring market expansion.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Functional Flours Industry?

- The significant surge in consumer preference for convenient and ready-to-eat food items is the primary factor fueling the market growth for product manufacturers in this sector.

- Functional flours have gained significant attention in the food industry due to their enhanced baking properties and fiber enrichment methods. These flours offer advantages such as reduced gluten formation and increased moisture, making them a popular choice among ready-to-eat food manufacturers. The demand for functional flours is driven by the growing preference for convenience and the increasing awareness of health concerns, particularly gluten intolerance, in Europe. Rice and legume-derived functional flours are widely used in RTE food production. Consumer acceptance is crucial in this market, and quality control metrics, such as water absorption capacity and pastry flour characteristics, are essential considerations for manufacturers.

- Flour milling technology plays a significant role in producing high-quality functional flours. Proper packaging material selection is also vital to ensure the longevity and freshness of the product. Overall, the market is witnessing steady growth due to these factors and the increasing demand for healthier and convenient food options.

What are the market trends shaping the Functional Flours Industry?

- Functional flour blends are currently experiencing innovations as the market trend. This sector is witnessing advancements in creating high-performance flour blends for various industries.

- Functional flours have gained significant attention in the food industry due to their ability to enhance the nutritional value and sensory appeal of food products. Manufacturers are increasingly investing in the development of functional flours by incorporating blends of various grains and seeds. These blends can boost proteins and other essential nutrients, making them an attractive alternative to traditional wheat flour. Gluten-free functional flours are particularly popular, as they cater to the growing demand for healthier and allergen-free food options. Seed flour blends, in particular, are gaining traction in the market. The product development lifecycle for functional flours involves rigorous testing and analysis, including ingredient cost analysis, texture analysis methods, microscopic analysis techniques, and nutritional labeling regulations.

- Cost-effectiveness analysis and supply chain management are crucial considerations in the production of functional flours. Functional flours made from non-wheat grains, lower salt, sugar, and higher fiber content are in high demand due to health consciousness. Innovations in this area are a priority, as these functional flours offer numerous benefits while maintaining cost-effectiveness and meeting consumer preferences. Starch modification techniques are used to improve the functionality of functional flours, making them more versatile in various food applications. As the market for functional flours continues to evolve, manufacturers must stay informed about the latest trends and regulations to remain competitive.

What challenges does the Functional Flours Industry face during its growth?

- The industry's growth is significantly impacted by unpredictable fluctuations in the availability of functional flour raw materials, which can be attributed to various weather conditions and natural calamities.

- The market relies heavily on the availability of raw materials, primarily grains and non-grains. Fluctuations in their production due to adverse weather conditions or climatic changes can hinder market growth. For instance, wheat, a common raw material, requires specific temperature conditions to thrive, and its yield can be significantly impacted by unfavorable weather. In developing countries, agricultural sectors often account for over 23% of total losses due to natural disasters. To ensure product consistency and safety, functional flour manufacturers employ various testing methods such as sensory evaluation, dough rheology, colorimetric analysis, and ingredient traceability systems.

- Compliance with stringent food safety standards is crucial to maintain consumer trust and market reputation. Ingredient sourcing strategies play a significant role in maintaining product quality and price competitiveness. Strategic partnerships with reliable suppliers and implementing robust quality control measures can help mitigate the risks associated with raw material availability.

Exclusive Customer Landscape

The functional flours market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the functional flours market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, functional flours market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGRANA Beteiligungs AG - This company specializes in functional flours, including Organiv vital wheat gluten, which is utilized in premium organic bakery items and serves as a key ingredient in vegetarian and vegan meat substitutes. The high-quality gluten enhances the texture and elasticity of baked goods and contributes to the creation of savory plant-based alternatives.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGRANA Beteiligungs AG

- Archer Daniels Midland Co.

- Associated British Foods Plc

- Dohler GmbH

- GEMEF Industries

- General Mills Inc.

- Ingredion Inc.

- Kerry Group Plc

- MGP Ingredients Inc.

- Olam Group Ltd.

- Parrish and Heimbecker Ltd.

- Sudzucker AG

- Symrise AG

- Tate and Lyle PLC

- The Hain Celestial Group Inc.

- The Scoular Co.

- Bunge Global SA

- Caremoli SpA

- Cargill Inc.

- Sensient Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Functional Flours Market

- In January 2024, Ardent Mills, a leading flour milling and ingredient company, announced the launch of its new line of Ancient Grains Functional Flours, including quinoa, amaranth, and teff flours, at the International Baking Industry Exposition (IBIE). These new offerings aim to cater to the growing demand for clean-label, nutrient-rich ingredients in the food industry (Source: Ardent Mills Press Release).

- In March 2024, Cargill and Bühler Group, two global leaders in food and agriculture, formed a strategic partnership to jointly develop and commercialize innovative plant-based protein and functional flour solutions. This collaboration is expected to leverage Bühler's expertise in technology and Cargill's market reach and resources to deliver sustainable, high-performance ingredients for various industries (Source: Cargill Press Release).

- In May 2024, ADM Milling Company, a subsidiary of Archer Daniels Midland Company, completed the acquisition of the specialty ingredients business of DSM Nutritional Products. This acquisition significantly expanded ADM's portfolio of functional ingredients, including functional flours, and strengthened its position as a leading supplier in the global food and beverage industry (Source: ADM Press Release).

- In April 2025, the European Commission approved the use of pulses, including chickpeas, lentils, and peas, as functional ingredients in food products. This approval is expected to boost the demand for functional flours derived from these pulses, as they offer high nutritional value and functional benefits (Source: European Commission Press Release).

Research Analyst Overview

- Functional flours have gained significant traction in the food industry due to their ability to enhance product quality and consumer appeal. According to recent consumer preference surveys, dough development time and bread texture parameters are key factors influencing purchasing decisions. To meet these demands, manufacturers focus on process efficiency improvements and baking process optimization. Thermal processing effects on functional flours' antioxidant capacity and mineral content assessment are crucial for marketing claims verification. Allergen control measures and ingredient declaration guidelines are essential for regulatory compliance procedures. Sensory attribute profiling and carbohydrate composition analysis help in product differentiation strategies.

- Production capacity planning and sustainable sourcing practices ensure consistent quality and reduce costs. Flour-water interactions, cake volume determination, and vitamin content analysis are essential for optimizing baking processes. Functional food ingredients, such as enzymatic hydrolysis processes, play a vital role in improving product functionality. Packaging design optimization and product shelf-life prediction are crucial for maintaining consumer trust and satisfaction.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Functional Flours Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

182 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.5% |

|

Market growth 2024-2028 |

USD 36.14 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.49 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Functional Flours Market Research and Growth Report?

- CAGR of the Functional Flours industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the functional flours market growth of industry companies

We can help! Our analysts can customize this functional flours market research report to meet your requirements.

RIA -

RIA -