Meat Substitutes Market Size 2025-2029

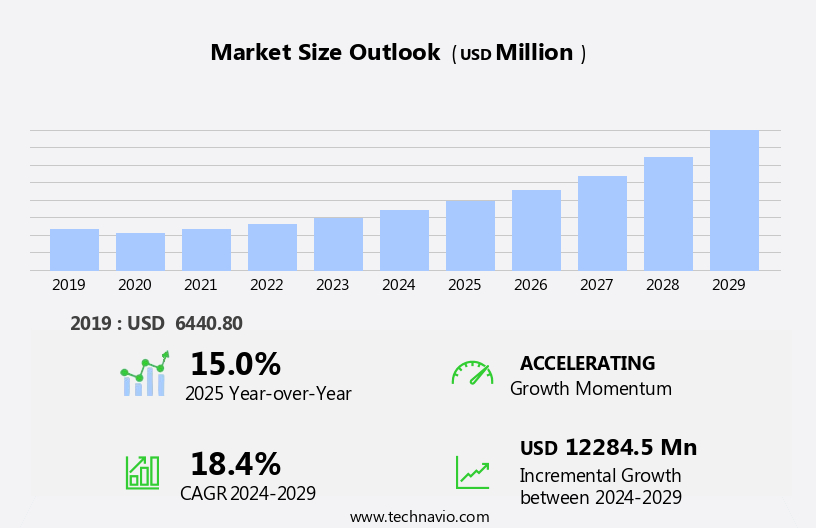

The meat substitutes market size is forecast to increase by USD 12.28 billion at a CAGR of 18.4% between 2024 and 2029.

- The market is experiencing significant growth due to the increasing research and development efforts in creating alternative protein sources. Soya chunks, Hot Dogs, and Veggie burgers are popular choices, with Canola oil and other nutrients enhancing their nutritional value. New product launches are a key driver in this market, as companies seek to cater to the rising demand for sustainable and ethical food options. However, the relatively high price point of meat substitutes remains a challenge for market penetration. Consumers, particularly those in developing economies, may find these alternatives less accessible due to cost.

- Companies looking to capitalize on this market should focus on innovation and affordability, aiming to create products that meet consumer demand while remaining competitive in pricing. Additionally, partnerships and collaborations between industry players and research institutions could lead to breakthroughs in technology and production methods, further driving market growth. Convenience stores and Mini markets cater to the demand for Shelf-stable and Low-fat protein options. Despite this obstacle, the potential for growth is substantial, as the global population continues to increase and concerns over animal welfare and environmental sustainability become more prevalent.

What will be the Size of the Meat Substitutes Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market is experiencing significant growth as diets focusing on plant-based options gain popularity due to health concerns and animal welfare considerations. Plant-based chicken, pork, fish, and beef alternatives are increasingly preferred by consumers seeking to reduce their intake of animal products. These substitutes offer similar nutrition value, including essential minerals like iron and calcium, making them suitable for individuals dealing with health issues such as diabetes, obesity, and heart disease. Next meats, such as soy milk, bean curd, tofu, and cooked soybeans, are popular choices due to their high protein content and versatility.

- Crumbles and grounds derived from these sources provide texture and taste comparable to their animal counterparts. Plant-based fish alternatives, like soybean curd, offer a solution for those dealing with digestive problems. The Good Food Institute reports that the market for plant-based meat substitutes is expanding, with companies like Novameat and vegan meat India leading the way. The shift towards plant-based options is driven by health concerns related to non-communicable diseases and the ethical implications of intensive animal farming. Plant-based burgers, patties, and other meat substitute products cater to this growing demand, offering consumers a viable alternative to traditional animal products.

How is this Meat Substitutes Industry segmented?

The meat substitutes industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

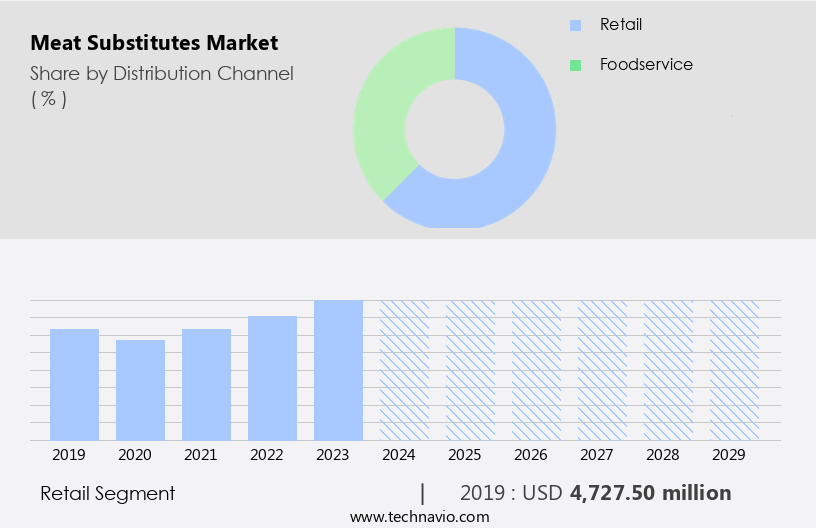

- Distribution Channel

- Retail

- Foodservice

- Product Type

- Soy-based

- Wheat-based

- Mycoprotein-based

- Others

- Form Factor

- Solid

- Liquid

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- The Netherlands

- UK

- APAC

- China

- India

- South America

- Brazil

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The retail segment is estimated to witness significant growth during the forecast period. The Plant-based patties segment experiences significant growth in the retail sector due to shifting consumer preferences, health concerns, and environmental awareness. Traditional grocery stores and supermarkets expand their offerings, stocking a diverse range of high-quality meat substitute products. Diabetes patients and those managing their weight seek out Plant-based Chicken, Meatballs, and Fish alternatives. Health-conscious buyers prefer Iron-rich liquid and Meatloaf formulations, while Vegetarian and Vegan lifestyles fuel the demand for Soybean curd, Tofu, and Quorn. Lab-grown meat, Mycoprotein, and Cereal grains cater to the flexitarian and functional ingredient markets.

Fiber, Antioxidants, and essential amino acids are crucial components in these products, addressing health issues like Heart disease and Non-communicable diseases. Plant-based protein manufacturers innovate with Pea, Rice, and Wheat protein, while customization and moisture retention are essential for Foodservice and Food product applications. The future of the market lies in the exploration of novel plant-based protein sources, such as Oligosaccharides from Mushrooms and Jackfruit, and the development of Immunity Boosting Products. Restaurants and Hotels increasingly offer Plant-based menus, while Food safety and Labeling standards remain crucial considerations.

The market's evolution reflects consumers' growing desire for sustainable, healthier, and more diverse dietary options.

The Retail segment was valued at USD 4.73 billion in 2019 and showed a gradual increase during the forecast period.

The Meat Substitutes Market is rapidly expanding, driven by growing awareness of healthy dietary habits, the rise of the vegan diet and vegetarian lifestyle, and increasing concerns about fat consumption. Alternatives made from soybean legumes, protein isolates, and plant protein serve as nutrient-rich raw material for various food products, including frozen items and plant-based beef. These products often come in dry powder form, are fat-free, rich in carbohydrate, and formulated to emulsify well, delivering a nutty taste and appealing texture. With meat shortages and rising nonmeat-based meals demand among the meat-eating population, nutritious products are gaining space in departmental stores. Innovations focus on binder efficiency, vitamin fortification, and clinical nutrition benefits like lowering blood cholesterol and blood sugar. The market also addresses the needs of non-vegans seeking a healthier diet with whole veggies and superfood blends.

Regional Analysis

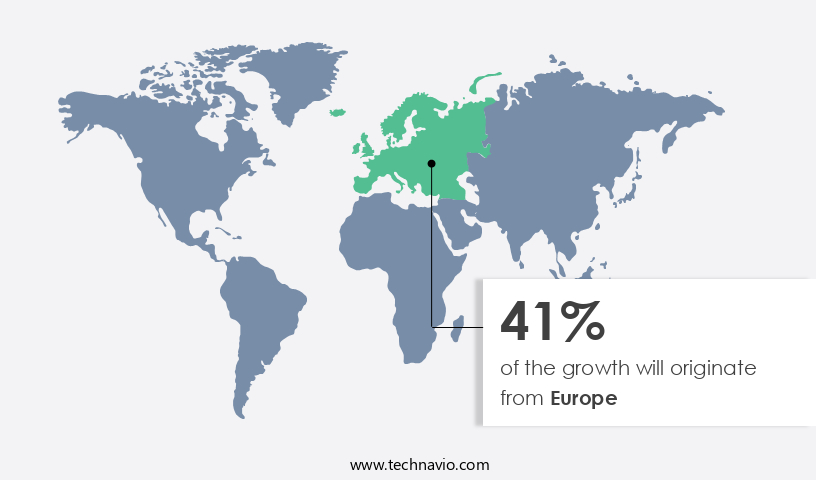

Europe is estimated to contribute 41% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The European market is experiencing notable growth due to the rising preference for plant-based protein products and increasing health consciousness among consumers. This trend is reflected in the increasing number of product launches and new market entrants. The vegan lifestyle is gaining popularity in Europe, leading to a rise in demand for meat substitutes. In response, companies are expanding their production capabilities by setting up new facilities in Europe. Plant-based alternatives to various meat products, such as patties, hot dogs, sausages, chicken, and fish, are in high demand. These substitutes are derived from various sources, including soy, pea, wheat, and mycoprotein.

Formulations often include essential nutrients, such as iron, calcium, potassium, and vitamins, to cater to the health-conscious consumer base. Companies are also focusing on customization, offering low-fat, cholesterol-free, and gluten-free options. The market is also witnessing the emergence of lab-grown meat and plant-based pork. The trend towards healthier dietary habits and weight management is driving the demand for meat substitutes as alternatives to red meat and processed meat. Additionally, the rise of flexitarianism and vegetarianism is contributing to the growth of the market. Companies are investing in research and development to enhance the texture, taste, and nutrition value of their plant-based meat substitutes.

Foodservice establishments, hotels, and convenience stores are increasingly offering plant-based options on their menus. The market is expected to continue growing as consumers seek out nutritious, sustainable, and ethical food choices.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Meat Substitutes market drivers leading to the rise in the adoption of Industry?

- The new product launches in the market serve as the primary driver for market growth. The market is experiencing significant growth due to increasing consumer awareness of health and environmental concerns. Animal meat production contributes to the emission of substantial greenhouse gases, with every gram of beef produced resulting in 221 grams of carbon dioxide. To cater to this expanding market, companies are introducing new meat substitute products. For instance, in March 2025, Impossible Foods launched its plant-based steak product, Impossible Steak Bites, at Natural Products Expo West. These pre-cooked, bite-sized pieces mimic the texture and taste of traditional steak while offering a protein alternative derived from plants. This innovation not only enhances the revenue stream and market presence of the company but also provides consumers with a healthier and more sustainable option.

- Additionally, meat substitutes made through bacterial fermentation, such as cottage cheese and soybean curd, are gaining popularity due to their high protein content and customization possibilities. Furthermore, vegetarian and vegan diets, including flexitarian and meat-free, are increasingly common, driving demand for functional ingredients like fiber, antioxidants, vitamins, and binders in meat substitute products. Mushrooms, oligosaccharides, and vegetable protein are other essential components of meat substitutes that cater to various dietary needs and preferences.

What are the Meat Substitutes market trends shaping the Industry?

- The ongoing trend in the market involves continuous research and development and the production of meat substitute products. This sector is seeing significant growth and innovation. The global market for meat substitutes is witnessing significant growth as consumers seek immunity-boosting, cholesterol-free protein alternatives to animal products. Plant-protein menu innovations, such as mycoprotein, pea, wheat gluten, and seitan, are gaining popularity among both plant-based and non-vegetarian consumers. These alternatives offer similar protein content to meat but provide additional minerals like calcium, potassium, and iron. To address common challenges with meat substitutes, such as beany flavor and moisture retention, plant-based protein manufacturers are focusing on improving taste and texture through emulsification and flavor enhancements. Convenience stores, foodservice outlets, lounges, and other food establishments are increasingly offering plant-based protein products as menu items.

- Scientists are also working to develop new raw materials and production methods to nullify allergens in soy and wheat, addressing concerns for consumers with allergies. Additionally, low-fat and high-carbohydrate plant-based protein sources are gaining traction as health and nutrition become key priorities for consumers. The market is expected to continue growing as companies invest in research and development to launch superior products and expand their offerings to cater to the evolving demand for meat substitutes.

How does Meat Substitutes market face challenges during its growth?

- The high price point of meat substitutes poses a significant challenge to the industry's growth trajectory. Meat substitutes have gained popularity among consumers seeking healthier and more sustainable food options, despite their higher cost compared to traditional meat products. Plant-based alternatives, such as vegan burgers, sausages, and nuggets, are increasingly being chosen due to concerns over animal welfare, food safety, and health benefits. These meat substitutes are derived from various plant sources, including soy milk, tofu, grains, and legumes. Companies like Novameat, Next Meats, and Quorn produce these products using essential amino acids and natural flavors, such as ginger, fennel, and soy sauce, to mimic the taste and texture of meat. Plant-based meat substitutes offer several advantages, including being free from cholesterol, low in saturated fats, and rich in essential nutrients like iron, protein, and fiber.

- However, some consumers may experience digestive problems due to the high fiber content. To address this issue, these products are often fortified with nutrients and available in various forms, including dry powders and refrigerated options. Restaurants and foodservice providers have also started incorporating meat substitutes into their menus to cater to the growing demand for plant-based options. Despite the higher cost, consumers are willing to pay a premium for these nutritious and ethical alternatives. However, it is crucial for companies to adhere to labeling standards and maintain food safety to ensure consumer trust and satisfaction. The shift towards plant-based meat substitutes is driven by various factors, including health, ethical concerns, and sustainability. While these products may be more expensive than traditional meat, their nutritional benefits and ethical appeal make them a viable option for consumers seeking to reduce their meat intake.

Exclusive Customer Landscape

The meat substitutes market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the meat substitutes market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, meat substitutes market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Archer Daniels Midland Co. - The company specializes in producing plant-based meat alternatives, including beef, steak, meatballs, and more.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Archer Daniels Midland Co.

- Beyond Meat Inc.

- Conagra Brands Inc.

- Continental Coffee Pvt. Ltd.

- Hormel Foods Corp.

- Impossible Foods Inc.

- International Flavors and Fragrances Inc.

- Kellogg Co.

- Kerry Group Plc

- Maple Leaf Foods Inc.

- Monde Nissin Corp.

- Morinaga and Co. Ltd.

- Morinaga Milk Industry

- Nestle SA

- New Wave Foods

- Tata Consumer Products Ltd.

- The Kraft Heinz Co.

- Tyson Foods Inc.

- Unilever PLC

- Wicked Kitchen Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Meat Substitutes Market

- In January 2024, Beyond Meat, a leading player in the market, announced the launch of its new plant-based sausage product in collaboration with Dunkin' (Dunkin Brands Group, Inc.), making Beyond Meat's sausages available at over 9,000 Dunkin' restaurants in the United States (Beyond Meat Press Release, 2024).

- In March 2024, Impossible Foods, another major player, secured a strategic investment of USD500 million from Microsoft Corporation and Mirae Asset Global Investments, bringing the company's total funding to over USD 1.5 billion (Impossible Foods Press Release, 2024).

- In April 2025, Nestlé, the world's largest food and beverage company, acquired a controlling stake in the plant-based meat alternative company, Sweet Earth Foods, expanding its presence in the market (Nestlé Press Release, 2025).

- In May 2025, the European Union (EU) approved the use of plant-based alternatives with the term "meat" in their labels, a significant regulatory development that is expected to boost the market growth for meat substitutes in the EU (European Commission Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by health-conscious buyers seeking alternatives to traditional animal products. Soya chunks, soybean curd, and pea-based proteins are among the popular plant-based options, with manufacturers constantly innovating to meet consumer demands. Mycoprotein, a fungus-based protein, and cereal grains are emerging as viable alternatives, offering unique textures and nutritional profiles. Gen Z, with its preference for plant-based diets and ethical consumption, is fueling the growth of this sector. The Good Food Institute, an industry organization, reports that plant-based meat substitutes now account for a significant portion of the market. These products are not limited to vegan and vegetarian consumers; many non-vegetarians are incorporating plant-based options into their diets for health reasons.

Plant-based protein formulations are being used to create a wide range of products, from veggie burgers and sausages to plant-based chicken and fish. These products offer the convenience of meat without the cholesterol and saturated fat, making them a popular choice for those managing weight and dealing with health concerns related to non-communicable diseases. Foodservice establishments, from convenience stores to high-end lounges, are embracing plant-based protein products. These establishments are seeking to cater to diverse customer needs, offering plant-based options that retain moisture and have a meat-like texture. Raw materials like pea protein, wheat gluten, and seitan are being used to create plant-based patties, pork, and beef substitutes.

Plant-based protein products are also being used to create low-fat, high-protein snacks and meals. Hummus, made from chickpeas, is a popular plant-based protein source, while tofu and soy milk are staples in many diets. Labeling standards are becoming more stringent, ensuring that these products are safe and nutritious, with essential amino acids and vitamins like calcium, potassium, and iron. Plant-based protein manufacturers are constantly innovating, using functional ingredients like garlic, paprika, and ginger to enhance flavors. Binders and emulsifiers are being used to improve texture and moisture retention. Plant-based meat substitutes are being used to cater to various dietary needs, from low-carbohydrate to low-fat diets.

The market for plant-based protein products is dynamic and evolving, with new players and products entering the market regularly. From lab-grown meat to plant-based fish, the possibilities are endless. The future of this market is bright, with continued innovation and customization expected to drive growth.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Meat Substitutes Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

221 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.4% |

|

Market growth 2025-2029 |

USD 12.28 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

15.0 |

|

Key countries |

US, Germany, UK, China, Canada, The Netherlands, France, India, Brazil, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Meat Substitutes Market Research and Growth Report?

- CAGR of the Meat Substitutes industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the meat substitutes market growth of industry companies

We can help! Our analysts can customize this meat substitutes market research report to meet your requirements.

RIA -

RIA -