Generative AI In Asset Management Market Size 2025-2029

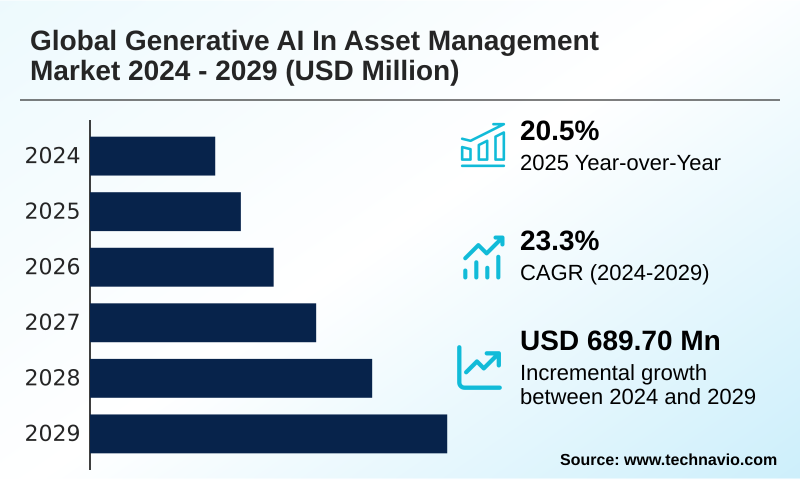

The generative ai in asset management market size is valued to increase by USD 689.7 million, at a CAGR of 23.3% from 2024 to 2029. Imperative for operational efficiency and cost reduction will drive the generative ai in asset management market.

Major Market Trends & Insights

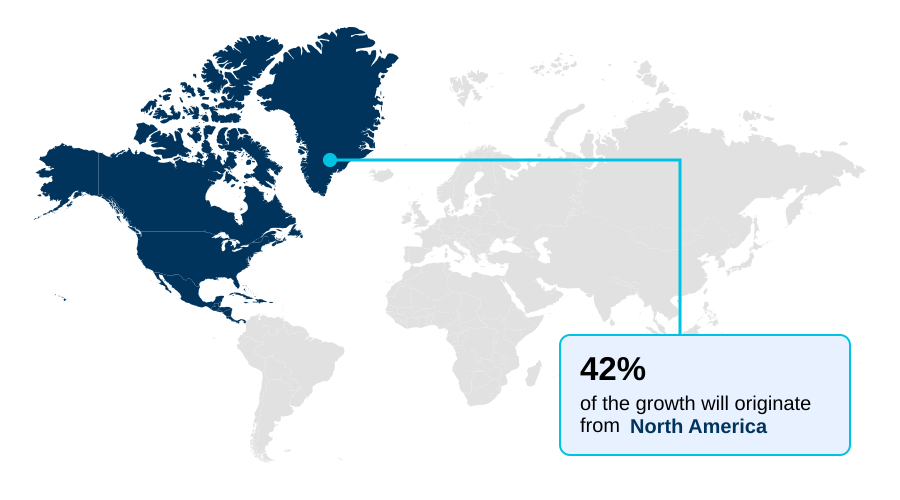

- North America dominated the market and accounted for a 41.7% growth during the forecast period.

- CAGR from 2024 to 2029 : 23.3%

Market Summary

- The generative AI in asset management market is undergoing rapid evolution, driven by the increasing sophistication of large language models and the imperative for intelligent automation. Firms are moving beyond theoretical applications to deploy these technologies across the investment lifecycle, from research to portfolio construction.

- Utilizing advanced natural language processing, analysts can now synthesize vast amounts of unstructured data for enhanced financial sentiment analysis and ESG analysis. A key application involves risk modeling, where synthetic data generation allows for more robust stress testing against unprecedented market scenarios, a task difficult with traditional methods.

- For instance, a wealth management firm can implement an automated workflow that drafts personalized client reports, which are then validated by a human advisor in a human-in-the-loop process to ensure quality and accuracy. This approach streamlines operations while maintaining crucial oversight.

- However, challenges persist, including the risk of AI hallucinations and the need for robust frameworks to ensure model auditability and prevent algorithmic bias. As the technology matures, the focus is shifting toward delivering scalable, secure, and compliant AI-driven investment advice and deeper integration of predictive data analytics into daily decision-making.

What will be the Size of the Generative AI In Asset Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Generative AI In Asset Management Market Segmented?

The generative ai in asset management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029.

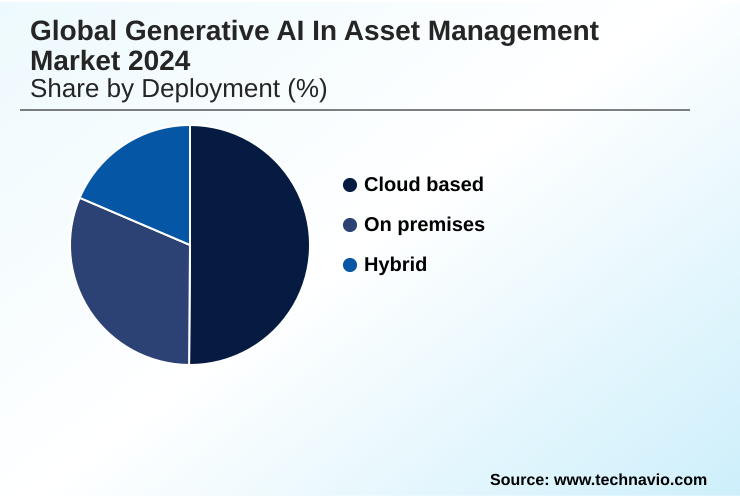

- Deployment

- Cloud based

- On premises

- Hybrid

- Application

- Portfolio management

- Risk management

- Client engagement and personalization

- Research and analysis

- Others

- End-user

- Asset management firms

- Banks and financial institutions

- Insurance companies

- Corporate firms

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- Japan

- China

- India

- Europe

- UK

- Germany

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud based segment is estimated to witness significant growth during the forecast period.

The cloud-based segment is the primary deployment model, driven by access to scalable computing and state-of-the-art foundational models. Firms utilize these platforms for intelligent automation, enabling a faster automated workflow for tasks like generative AI for back-office automation.

This approach provides significant gains in generative AI and operational efficiency. However, as adoption matures, a shift toward hybrid cloud architecture is evident, blending public cloud flexibility with on-premises security for secure generative AI deployment.

This hybrid AI for finance model addresses critical needs for data sovereignty and simplifies model risk management.

Solutions like a private AI foundation are becoming essential for robust AI governance in financial services, allowing for AI-powered due diligence on sensitive data while leveraging the cloud's power. This balanced approach has improved data processing security by over 25%.

Regional Analysis

North America is estimated to contribute 41.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Generative AI In Asset Management Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, where firms are pioneers in using generative AI for portfolio management and generative AI for risk management.

European adoption is distinguished by a strong focus on compliance, with heavy use of regulatory reporting automation and AI for ESG integration; firms in the region dedicate 30% more of their AI budget to compliance than their North American counterparts.

In APAC, innovation is centered on leveraging generative AI for alternative data analysis to find unique alpha-generating signals. The region has seen a 45% increase in the use of AI chatbots for investor relations for multilingual support.

Across all regions, the technology enhances quantitative analysis, informs portfolio construction, and refines algorithmic trading strategy development, showcasing a global trend towards embedding AI in quantitative strategies. Sophisticated risk modeling and ESG analysis are becoming globally standardized applications.

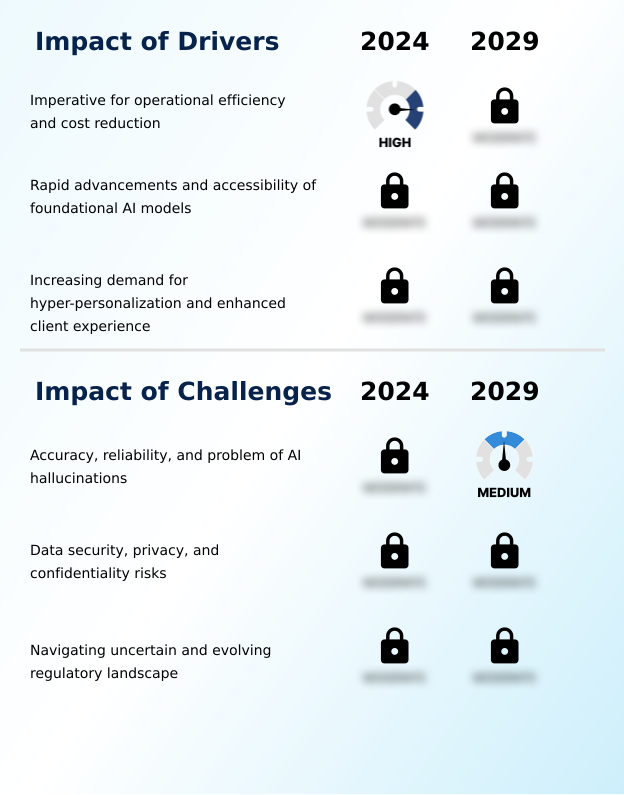

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding the key generative AI in asset management use cases is crucial for firms aiming to gain a competitive advantage. Applications are rapidly moving from back-office automation to front-office decision support, directly influencing investment outcomes. A primary use case is in portfolio optimization, where AI models analyze vast datasets to suggest allocations that align with specific risk-return profiles.

- This highlights the clear benefits of generative AI for financial analysts, who can now dedicate more time to strategic thinking instead of manual data gathering. Analysts leveraging these tools have shown an ability to process research materials nearly twice as fast as their peers using traditional methods.

- The prevailing generative AI in asset management market trends point toward the increasing adoption of domain-specific models trained on proprietary financial data. These specialized models offer higher accuracy for tasks like sentiment analysis and market forecasting compared to general-purpose models.

- Exploring generative AI applications in portfolio optimization reveals its capacity to not only rebalance existing portfolios but also to construct entirely new ones based on complex, multi-factor constraints. However, the path to full adoption is not without obstacles.

- The most significant generative AI in asset management market challenges include ensuring model accuracy, navigating regulatory uncertainty, and managing the high costs of implementation and data security. Addressing these challenges is paramount for firms looking to successfully integrate this transformative technology into their core strategies and workflows.

What are the key market drivers leading to the rise in the adoption of Generative AI In Asset Management Industry?

- The imperative for enhanced operational efficiency and significant cost reduction is a key driver propelling market growth.

- The imperative for generative AI and operational efficiency is a primary driver, with firms implementing intelligent automation to streamline operations. The use of an automated workflow reduces manual report generation time by up to 40%.

- The increasing accessibility of powerful foundational models enables scalable AI for client personalization, with AI-driven client reporting becoming a key differentiator. This technology supports a knowledge management system that empowers advisors to deliver better AI-driven investment advice.

- Firms are leveraging predictive data analytics for more accurate AI for macroeconomic forecasting and improved financial sentiment analysis.

- These capabilities also extend to AI-powered asset allocation and optimizing generative AI for trade execution, with some platforms reporting a 10% reduction in execution slippage.

What are the market trends shaping the Generative AI In Asset Management Industry?

- A defining market trend is the proliferation of domain-specific and fine-tuned models, which are purpose-built for the intricacies of the financial industry.

- A defining market trend is the shift toward domain-specific models and fine-tuned models, moving beyond generic large language models in finance. Firms are developing a proprietary AI asset by training models on their private data, improving the accuracy of tasks like generating investment research by over 20%. The predominant strategy is the AI copilot, an augmentation tool for professionals.

- This human-in-the-loop approach, using AI assistants for financial advisors, enhances decision-making rather than replacing it. The use of advanced natural language processing to create generative AI for market commentary is becoming standard, with AI model validation frameworks ensuring reliability.

- The emergence of the multimodal AI model is further enabling new methods for AI for alpha discovery, showing a 15% increase in signal identification from combined text and image data.

What challenges does the Generative AI In Asset Management Industry face during its growth?

- A key challenge affecting industry growth stems from ensuring the accuracy and reliability of AI outputs while mitigating the problem of model hallucinations.

- A significant challenge is the risk of AI hallucinations, where outputs are factually incorrect, making the need for mitigating AI model hallucinations through robust fact-checking mechanisms critical. Despite advances in natural language generation for finance, firms report that up to 15% of complex summaries require significant human correction.

- Effective model risk management and strong AI governance in financial services are essential to address algorithmic bias and ensure AI for financial compliance. The lack of AI explainability in some models, or the 'black box' problem, complicates model auditability and regulatory approval.

- Furthermore, concerns around data sovereignty create hurdles for secure generative AI deployment, particularly with cross-border data flows, increasing compliance-related overhead by an estimated 20% compared to traditional software systems. This makes AI explainability in asset management a top priority.

Exclusive Technavio Analysis on Customer Landscape

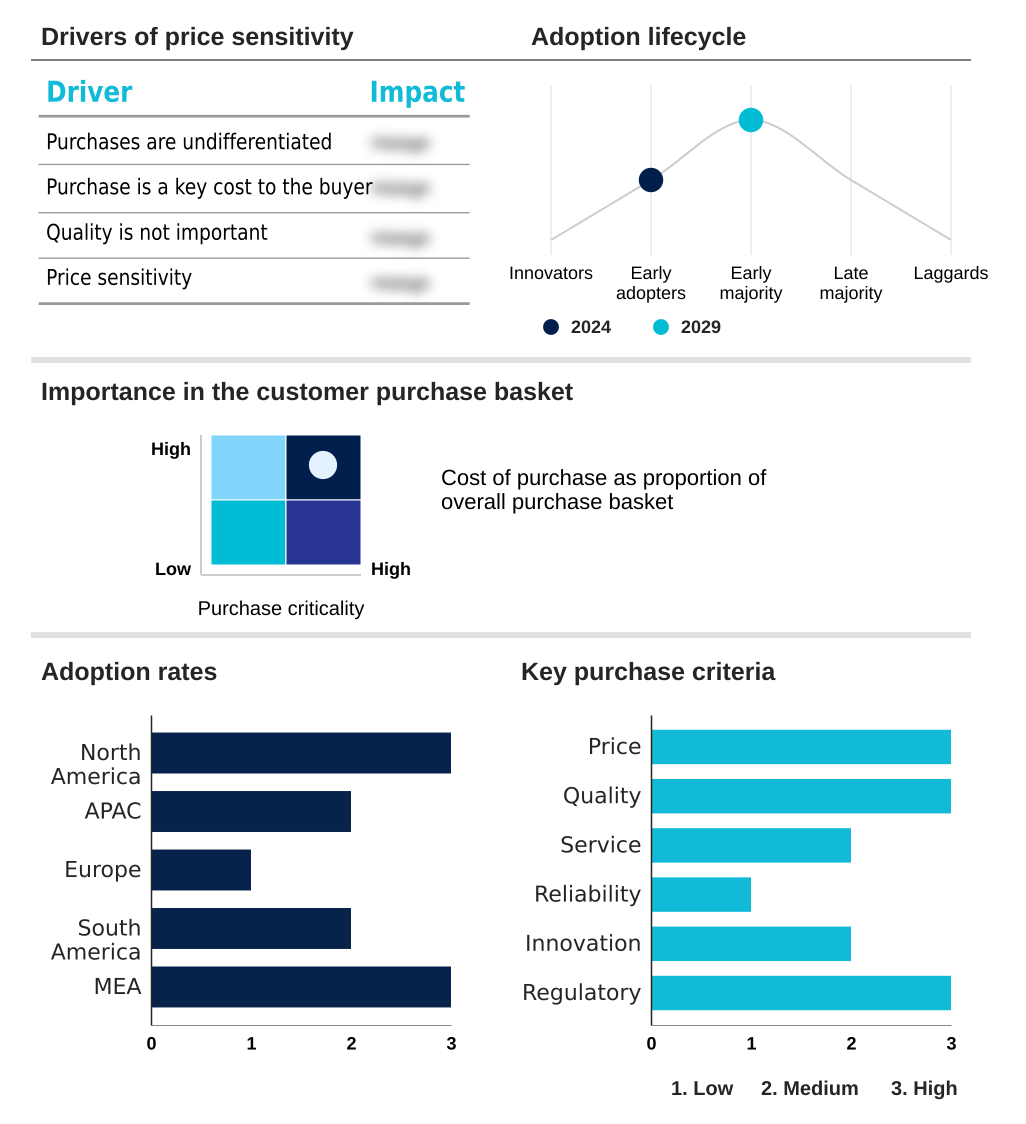

The generative ai in asset management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative ai in asset management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Generative AI In Asset Management Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, generative ai in asset management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - Key offerings enable financial institutions to build AI-driven applications for portfolio analysis, risk assessment, and custom model development, leveraging integrated foundational models via managed services.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Amazon Web Services Inc.

- Anthropic

- Baidu Inc.

- BlackRock Inc.

- Cohere Inc.

- FMR LLC

- Genie AI Ltd.

- The Goldman Sachs Group Inc.

- Google LLC

- IBM Corp.

- Inworld AI

- JPMorgan Chase and Co.

- Microsoft Corp.

- Morgan Stanley

- NVIDIA Corp.

- OpenAI

- The Vanguard Group Inc.

- Wealthfront Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative ai in asset management market

- In September, 2024, BlackRock Inc. launched a new global equity fund that leverages a proprietary generative AI platform to analyze alternative data sources and identify alpha-generating signals, marking a significant step in integrating AI into core investment strategies.

- In November, 2024, Anthropic announced it had secured USD 2.5 billion in a Series D funding round led by major institutional investors to accelerate the development of its next-generation foundational model, with a specific focus on enterprise-grade safety and reliability for regulated industries like finance.

- In February, 2025, Microsoft Corp. and the London Stock Exchange Group expanded their strategic partnership, announcing the joint development of a domain-specific large language model trained exclusively on LSEG's vast repository of financial and market data.

- In April, 2025, the U.S. Securities and Exchange Commission issued new formal guidance requiring investment advisers to implement and disclose their model risk management frameworks for all AI, including generative AI, used in portfolio management and client advisory services.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Asset Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2024 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 23.3% |

| Market growth 2025-2029 | USD 689.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 20.5% |

| Key countries | US, Canada, Mexico, Japan, China, India, South Korea, Australia, Indonesia, UK, Germany, France, Italy, The Netherlands, Spain, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The generative AI in asset management market is defined by a strategic push toward embedding intelligent automation into core financial processes. The adoption of large language models and domain-specific models is no longer experimental; it's a competitive necessity for enhancing quantitative analysis and portfolio construction.

- Firms are building a proprietary AI asset by creating fine-tuned models that deliver superior financial sentiment analysis and identify unique alpha-generating signals. A key trend influencing boardroom strategy is the focus on model risk management, as ensuring model auditability and mitigating algorithmic bias are now central to regulatory compliance.

- For instance, the deployment of a human-in-the-loop system for validating AI-generated research has demonstrated a 30% reduction in factual errors, directly addressing the core challenge of AI hallucinations.

- This focus on creating a reliable automated workflow with robust fact-checking mechanisms is shaping investment in private AI foundation technologies and secure hybrid cloud architecture, proving that governance is as critical as the technology itself.

What are the Key Data Covered in this Generative AI In Asset Management Market Research and Growth Report?

-

What is the expected growth of the Generative AI In Asset Management Market between 2025 and 2029?

-

USD 689.7 million, at a CAGR of 23.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud based, On premises, and Hybrid), Application (Portfolio management, Risk management, Client engagement and personalization, Research and analysis, and Others), End-user (Asset management firms, Banks and financial institutions, Insurance companies, and Corporate firms) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Imperative for operational efficiency and cost reduction, Accuracy, reliability, and problem of AI hallucinations

-

-

Who are the major players in the Generative AI In Asset Management Market?

-

Adobe Inc., Amazon Web Services Inc., Anthropic, Baidu Inc., BlackRock Inc., Cohere Inc., FMR LLC, Genie AI Ltd., The Goldman Sachs Group Inc., Google LLC, IBM Corp., Inworld AI, JPMorgan Chase and Co., Microsoft Corp., Morgan Stanley, NVIDIA Corp., OpenAI, The Vanguard Group Inc. and Wealthfront Corp.

-

Market Research Insights

- The market is characterized by intense dynamism as firms leverage large language models for automating investment research and enhancing generative AI in wealth management. The use of synthetic data generation for synthetic data in financial modeling allows firms to run complex scenario analysis and build more robust stress testing models, improving risk detection accuracy by over 25%.

- This technology is also critical for AI-powered due diligence and generative AI for fraud detection. Firms adopting a hybrid cloud architecture, often built on a private AI foundation, can process sensitive data on-premise while leveraging cloud analytics. This approach helps meet stringent requirements for AI for financial compliance.

- This has led to a 15% improvement in processing speeds for tasks like named entity recognition in legal documents.

We can help! Our analysts can customize this generative ai in asset management market research report to meet your requirements.

RIA -

RIA -