Generative Ai In Data Analytics Market Size 2026-2030

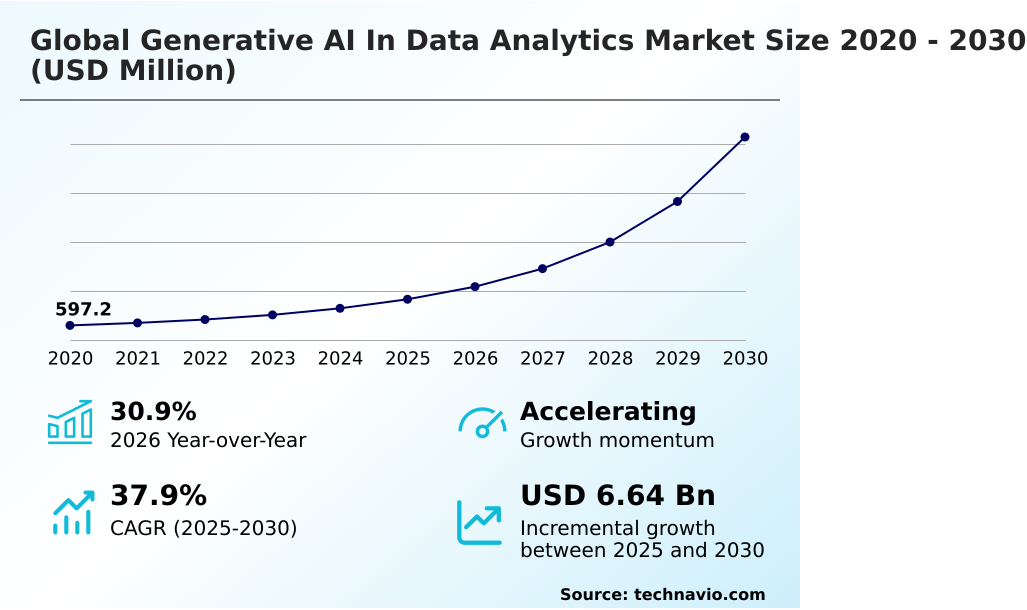

The generative ai in data analytics market size is valued to increase by USD 6.64 billion, at a CAGR of 37.9% from 2025 to 2030. Increasing demand for automated data synthesis and synthetic data generation will drive the generative ai in data analytics market.

Major Market Trends & Insights

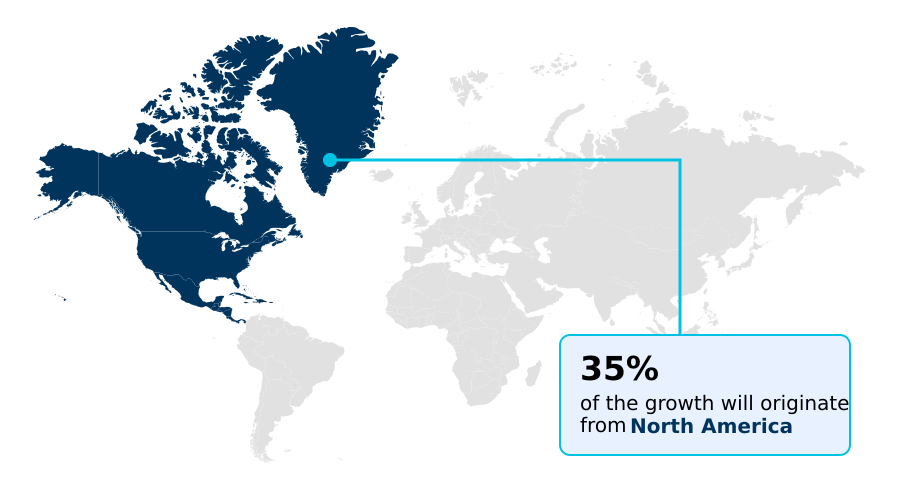

- North America dominated the market and accounted for a 35.3% growth during the forecast period.

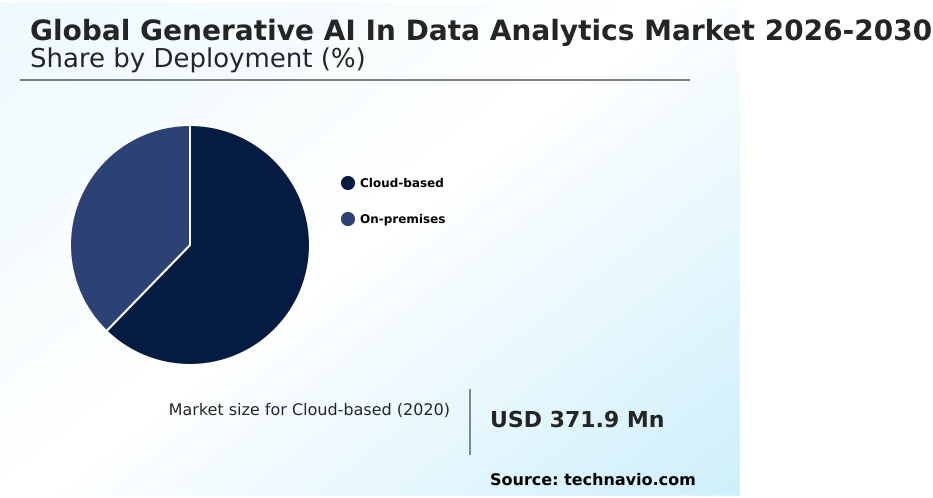

- By Deployment - Cloud-based segment was valued at USD 810.3 million in 2024

- By Technology - Machine learning segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 7.71 billion

- Market Future Opportunities: USD 6.64 billion

- CAGR from 2025 to 2030 : 37.9%

Market Summary

- The Generative AI In Data Analytics Market is experiencing a rapid transition from experimental frameworks to deeply integrated, autonomous enterprise operations. This evolution is primarily driven by the escalating need for automated data synthesis, allowing organizations to convert vast, unstructured data lakes into actionable strategic insights instantaneously.

- For example, in supply chain operations, predictive algorithms process global logistics variables to automatically reroute shipments, effectively mitigating disruption risks before they materialize. This capability drastically enhances productivity, enabling enterprises to achieve a 35% reduction in manual data processing time compared to traditional analytics methods.

- However, the market faces significant headwinds due to the fragmentation of data privacy regulations across different jurisdictions. Because international compliance frameworks dictate strict algorithmic transparency, multinational corporations encounter substantial difficulties in deploying unified analytical models, often resulting in localized silos that limit systemic efficiency.

- Despite these regulatory frictions, the continuous integration of conversational interfaces guarantees that business intelligence becomes increasingly democratized, establishing a resilient foundation for long-term organizational agility and proactive strategic planning.

What will be the Size of the Generative Ai In Data Analytics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Generative Ai In Data Analytics Market Segmented?

The generative ai in data analytics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Technology

- Machine learning

- Natural language processing

- Deep learning

- Computer vision

- Robotic process automation

- Application

- Data augmentation

- Text generation

- Anomaly detection

- Simulation and forecasting

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Turkey

- North America

By Deployment Insights

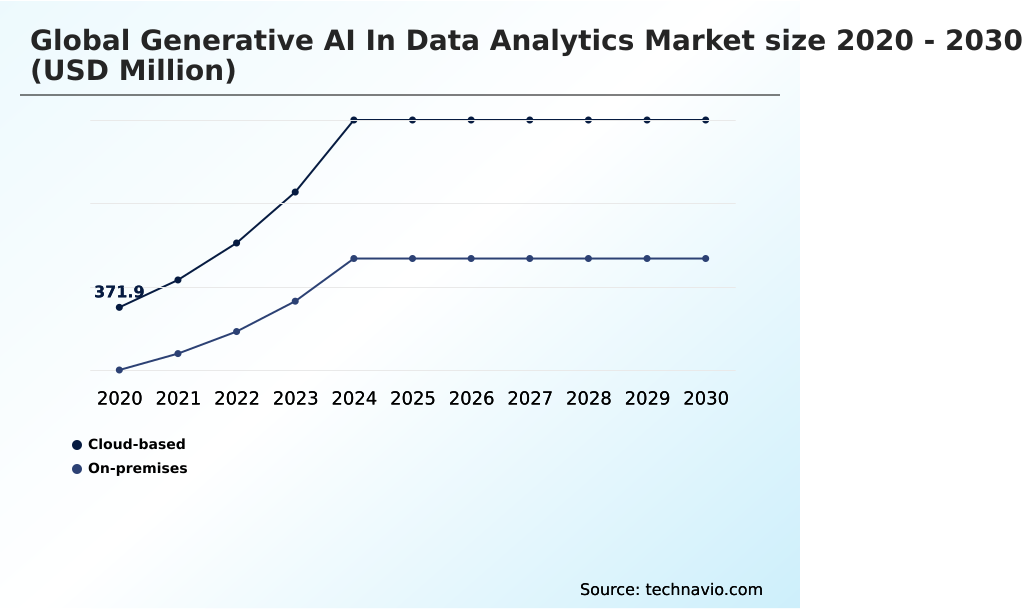

The cloud-based segment is estimated to witness significant growth during the forecast period.

Cloud-based architectures form the operational backbone of the Generative AI In Data Analytics, offering the massive computational elasticity required to process complex datasets.

This deployment model fundamentally alters how enterprises handle large language models and transformer architectures by replacing capital-intensive physical servers with scalable virtual resources.

By utilizing cloud native scalability, organizations rapidly execute synthetic data generation and natural language querying without bandwidth constraints. Conversely, on premises deployment remains essential for highly regulated sectors requiring strict data residency compliance.

The shift toward hybrid cloud infrastructure allows companies to balance external processing power with internal security protocols. Integrating these advanced systems improves unstructured data interpretation, as cloud-hosted analytics models see error detection improved by 15% compared to isolated legacy servers.

This structural evolution significantly enhances model hallucination reduction, ensuring that dynamic data pipelines maintain rigorous consistency while delivering accelerated business intelligence.

The Cloud-based segment was valued at USD 810.3 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Generative Ai In Data Analytics Market Demand is Rising in North America Get Free Sample

North America and APAC exhibit distinct adoption trajectories within the Generative AI In Data Analytics due to differing regulatory environments and digital infrastructure maturities. North America heavily prioritizes explainable artificial intelligence and algorithmic transparency to navigate stringent governance mandates.

By integrating machine learning orchestration and prompt engineering optimization, North American firms align closely with strict data governance protocols, resulting in risk assessment overhead reduced by 20%.

Conversely, APAC rapidly scales deep learning pipelines and computer vision synthesis to address the exponential growth of unstructured digital platforms.

This rapid integration of robotic process automation and multivariate analysis automation in APAC manufacturing hubs directly fuels efficiency, driving supply chain visibility improved by 28%.

Consequently, while North America focuses on rigid compliance, APAC leverages automated intelligence to address diverse consumer behaviors, creating a regional divide where APAC operational deployment speed outpaces Western counterparts by 18%.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The integration of advanced machine learning into corporate infrastructure is systematically dismantling the traditional barriers associated with complex business intelligence. By leveraging automated executive summary generation, management teams can instantly distill extensive quarterly reports into concise, actionable strategies, bypassing the labor-intensive manual review process.

- This analytical transformation is particularly critical within highly regulated environments, where the application of synthetic healthcare dataset creation enables pharmaceutical researchers to rigorously test diagnostic algorithms without compromising patient confidentiality. In the banking sector, the deployment of financial transaction anomaly detection ensures that irregular patterns are identified instantaneously, providing a level of security that significantly surpasses legacy rule-based monitoring.

- Consequently, institutions utilizing these autonomous oversight mechanisms report threat response times improved by nearly 40% compared to standard reactive protocols. Furthermore, logistics and urban planning departments are increasingly utilizing multimodal geospatial image analysis to optimize routing and infrastructure development, translating raw satellite feeds into coherent logistical roadmaps.

- As enterprise software platforms mature, the integration of conversational sql query formulation democratizes database access, allowing operational leaders to interrogate complex data lakes using plain language rather than specialized code. This evolution ensures that sophisticated analytical capabilities are no longer confined to specialized engineering teams but are seamlessly integrated across the entire organizational hierarchy.

- As a result, businesses can proactively navigate supply chain volatility and compliance mandates with unprecedented agility, establishing a highly responsive operational framework that maximizes the strategic value of internal data assets.

What are the key market drivers leading to the rise in the adoption of Generative Ai In Data Analytics Industry?

- The escalating demand for automated data synthesis and the generation of synthetic datasets acts as a primary driver propelling market expansion.

- The escalating demand for automated data interpretation serves as a primary catalyst for the Generative AI In Data Analytics, fundamentally driven by the need to accelerate decision-making cycles.

- Because traditional analytics require specialized skills, companies rapidly adopt conversational analytics and self service analytics to eliminate internal reporting bottlenecks. This widespread business intelligence democratization ensures that non-technical personnel can extract actionable intelligence instantly.

- By utilizing data lakehouse integration and federated learning frameworks, enterprises securely conduct proprietary data fine tuning without exposing sensitive information. Consequently, the deployment of privacy preserving synthetic datasets allows rigorous testing under strict regulatory constraints.

- These advancements generate profound operational benefits, as predictive maintenance forecasting and fraud detection modeling enable organizations to realize operational costs lowered by 12%.

- Additionally, highly improved neural network inference accelerates query response times, ensuring decision latency is reduced by 25% across complex global workflows.

What are the market trends shaping the Generative Ai In Data Analytics Industry?

- The emergence of autonomous agentic workflows within enterprise analytics represents a significant upcoming trend in the market. This advancement enables organizations to transition from static reporting to independent, self-refining analytical systems.

- The emergence of autonomous agentic workflows is fundamentally reshaping enterprise analytics by replacing static dashboards with self-executing diagnostic systems. This transition occurs because multimodal reasoning allows algorithms to simultaneously process text, visual feeds, and structured tables, ensuring comprehensive insight extraction.

- As a result, businesses deploy automated data synthesis alongside dynamic dashboard generation to navigate complex supply networks, enabling agile responses to market disruptions. By leveraging graphical processing unit optimization and low rank adaptation, organizations can fine-tune these intelligent automation workflows efficiently, drastically reducing infrastructure overhead.

- Consequently, conversational data exploration becomes seamless, leading to scenario modeling where predictive visualizations demonstrate that forecast accuracy improved by 18%. Furthermore, the integration of these systems accelerates real time insight generation, allowing proactive monitoring that has successfully seen diagnostic downtime reduced by 30%.

What challenges does the Generative Ai In Data Analytics Industry face during its growth?

- The proliferation of data privacy mandates and the fragmentation of regulatory compliance frameworks pose significant challenges to industry growth.

- Stringent global data privacy regulations and fragmented compliance requirements present significant structural barriers to the Generative AI In Data Analytics. Because international privacy laws mandate rigorous algorithmic oversight, enterprises struggle to deploy unified foundation models across diverse operational geographies.

- This legislative friction directly complicates cross border data sovereignty, forcing multinational corporations to localize their semantic search pipelines and vector database integration efforts. As organizations attempt to implement automated sql generation within their enterprise resource planning integration and customer relationship management synthesis, the necessary security localizations cause processing delays.

- Consequently, the fragmentation of compliance protocols creates friction in supply chain simulation and complex anomaly detection algorithms. These regulatory hurdles significantly impact performance, resulting in compliance management costs increased by 22%. Furthermore, the requirement to isolate regional data silos frequently leads to a situation where global reporting efficiency decreased by 15%, highlighting a critical operational constraint.

Exclusive Technavio Analysis on Customer Landscape

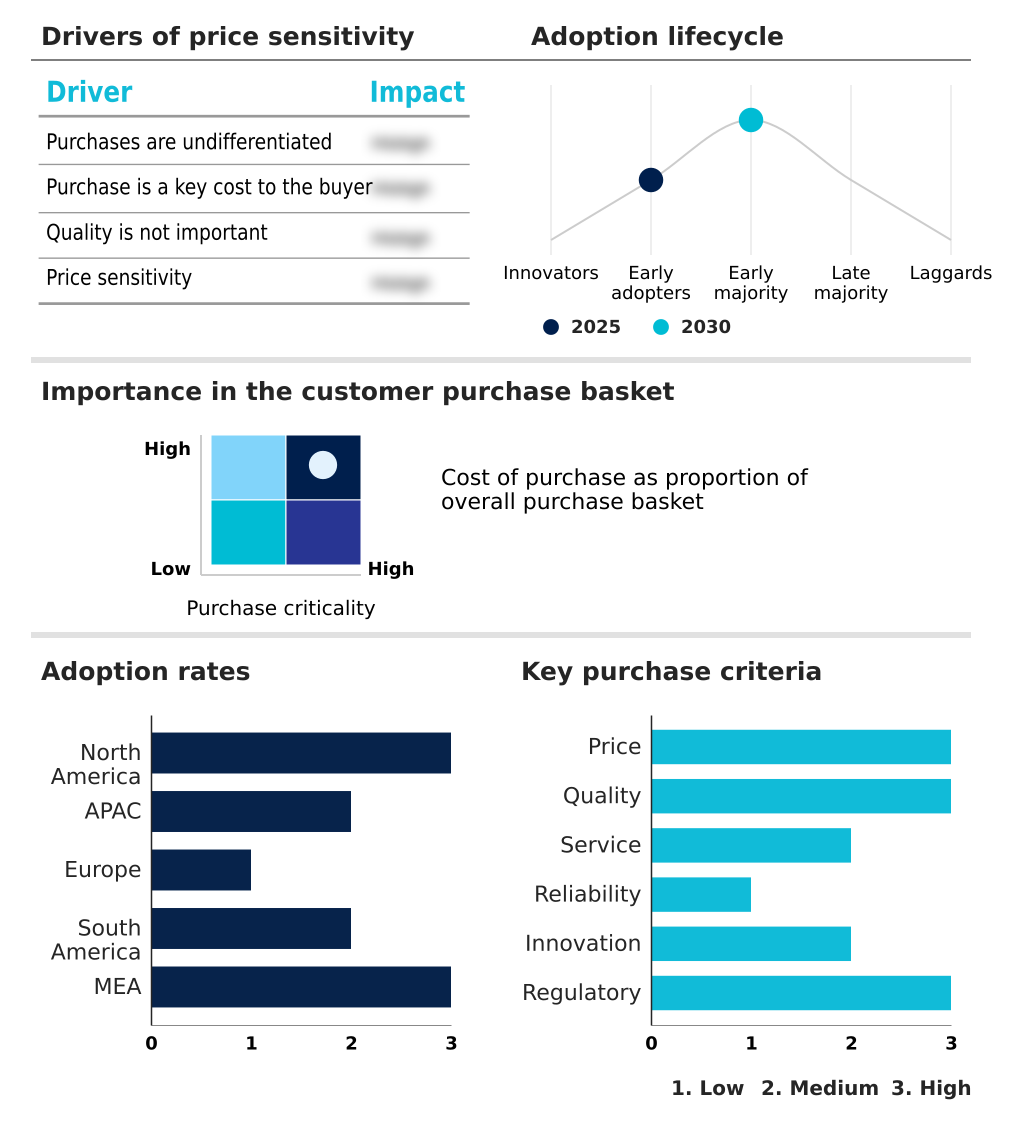

The generative ai in data analytics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative ai in data analytics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Generative Ai In Data Analytics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, generative ai in data analytics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - The firm provides sophisticated generative business intelligence capabilities, enabling automated data insights, predictive infrastructure analysis, and natural language query generation to optimize enterprise analytics workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Amazon Web Services Inc.

- Atlassian Corp.

- Automatic Data Processing Inc.

- Box Inc.

- Databricks Inc.

- Dell Technologies Inc.

- Google LLC

- Hugging Face Inc.

- IBM Corp.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- ServiceNow Inc.

- Siemens AG

- Slack Technologies LLC

- Snowflake Inc.

- Workday Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative ai in data analytics market

- In the Application Software industry, the widespread adoption of cloud-based delivery models has lowered the capital barrier for deploying resource-intensive machine learning workloads, directly accelerating Generative AI In Data Analytics demand by enabling smaller enterprises to access scalable computational power.

- The implementation of strict data privacy regulations, such as the European Union General Data Protection Regulation, has necessitated advanced anonymization techniques, thereby driving the Generative AI In Data Analytics market to rapidly innovate in high-fidelity synthetic data generation.

- The integration of enterprise automation tools with legacy enterprise resource planning systems has reduced manual data entry bottlenecks, creating a robust foundation of structured data that enhances the accuracy of Generative AI In Data Analytics forecasting models.

- The standardization of workflow interoperability protocols across major business intelligence platforms has simplified the cross-platform sharing of unstructured data, allowing Generative AI In Data Analytics solutions to seamlessly execute complex, multimodal reasoning tasks across decentralized corporate networks.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative Ai In Data Analytics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 37.9% |

| Market growth 2026-2030 | USD 6638.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 30.9% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Generative AI In Data Analytics Market is actively transitioning toward sophisticated, self-executing business intelligence frameworks that eliminate conventional manual reporting bottlenecks. As organizations embed large language models and foundation models directly into their operational infrastructure, the capacity for real-time strategic foresight expands significantly.

- Through automated data synthesis, enterprises can instantly aggregate diverse information streams to inform dynamic pricing strategies and critical compliance decisions. By applying multimodal reasoning to complex operational challenges, businesses successfully convert disparate text, image, and numerical inputs into unified strategic roadmaps.

- This structural shift toward autonomous agentic workflows enables procurement departments to optimize inventory management independently, systematically bypassing the latency of human intervention. Consequently, early adopters of these integrated analytics architectures report decision-making latency decreased by 28% when compared to reliance on traditional software systems.

- The simultaneous integration of robotic process automation ensures that repetitive data extraction occurs flawlessly, while rigorous algorithmic transparency maintains the auditability required for high-level corporate governance. This fundamental technological progression ensures that raw data consistently drives proactive, enterprise-wide agility.

What are the Key Data Covered in this Generative Ai In Data Analytics Market Research and Growth Report?

-

What is the expected growth of the Generative Ai In Data Analytics Market between 2026 and 2030?

-

USD 6.64 billion, at a CAGR of 37.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, and On-premises), Technology (Machine learning, Natural language processing, Deep learning, Computer vision, and Robotic process automation), Application (Data augmentation, Text generation, Anomaly detection, and Simulation and forecasting) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for automated data synthesis and synthetic data generation, Data privacy proliferation and regulatory compliance fragmentation

-

-

Who are the major players in the Generative Ai In Data Analytics Market?

-

Accenture Plc, Amazon Web Services Inc., Atlassian Corp., Automatic Data Processing Inc., Box Inc., Databricks Inc., Dell Technologies Inc., Google LLC, Hugging Face Inc., IBM Corp., Microsoft Corp., NVIDIA Corp., Oracle Corp., Salesforce Inc., SAP SE, ServiceNow Inc., Siemens AG, Slack Technologies LLC, Snowflake Inc. and Workday Inc.

-

Market Research Insights

- The Generative AI In Data Analytics Market is undergoing a fundamental structural transformation driven by the rapid adoption of intelligent automation workflows and self service analytics. This shift enables business intelligence democratization, empowering non-technical stakeholders to extract immediate insights without relying on specialized engineering teams.

- By implementing predictive maintenance forecasting algorithms, industrial enterprises have successfully achieved machine downtime reduced by 24%. Concurrently, the rigorous enforcement of data governance protocols ensures that conversational query platforms maintain high operational security, which has led to unauthorized access incidents lowered by 18%.

- These technological advancements streamline complex organizational strategies, fostering a highly responsive operational environment where data-driven precision systematically outpaces traditional reporting methods.

We can help! Our analysts can customize this generative ai in data analytics market research report to meet your requirements.

RIA -

RIA -