Generative AI In Industrial Design Market Size 2025-2029

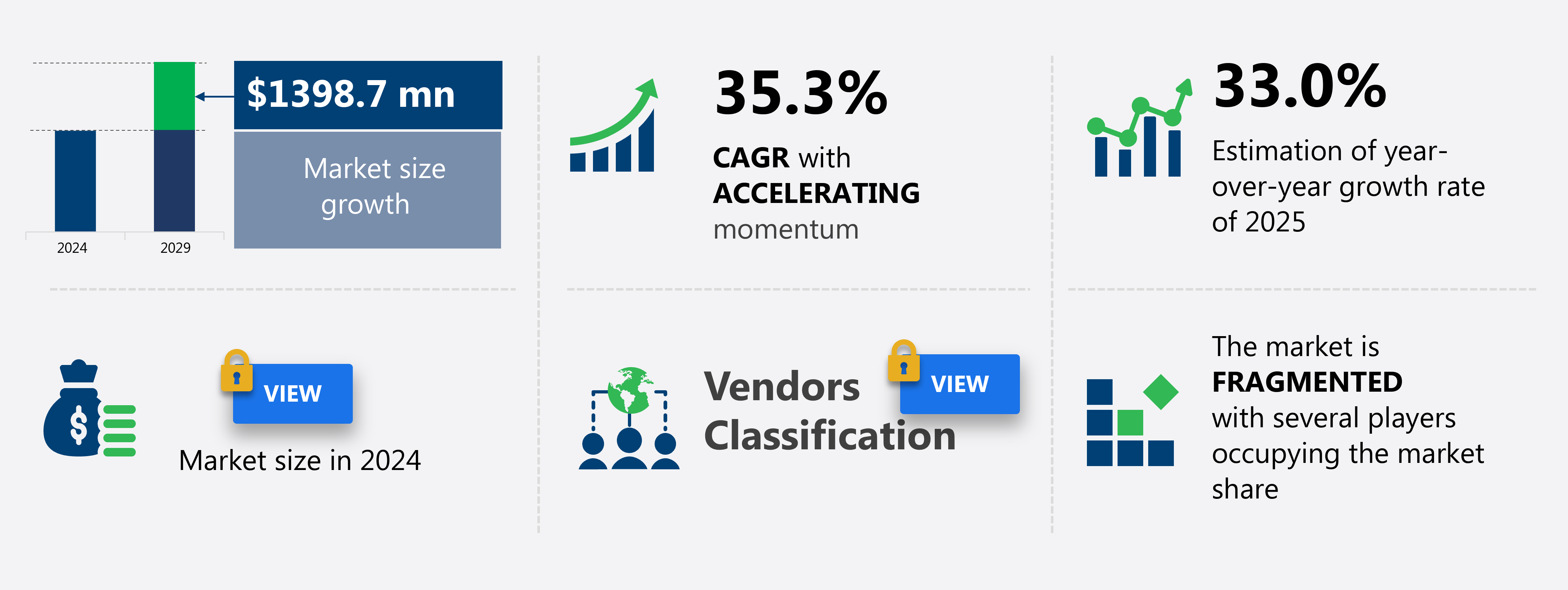

The generative AI in industrial design market size is forecast to increase by USD 1.4 billion, at a CAGR of 35.3% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing demand for accelerated innovation and reduced time to market. This trend is particularly evident in industries where design iterations are time-consuming and costly, such as automotive and consumer electronics. A key driver in this market is the integration of multi-modal and natural language interfaces, enabling designers to interact more intuitively with AI systems and generate more accurate and diverse design solutions. However, the adoption of Generative AI in industrial design faces challenges.

- One major obstacle is the high implementation costs and complex integration with legacy systems. These challenges may deter smaller companies and limit the market's growth potential. Despite these hurdles, companies that successfully navigate these challenges and effectively leverage Generative AI in their design processes are likely to gain a competitive edge, streamlining their operations and delivering innovative products to market more quickly. The market is experiencing significant growth, driven by the increasing adoption of advanced technologies such as computer-aided design (CAD) for manufacturing products.

What will be the Size of the Generative AI In Industrial Design Market during the forecast period?

Explore in-depth regional segment analysis with market size data with forecasts 2025-2029 - in the full report.

Request Free Sample

- The market for AI in industrial design continues to evolve, with applications spanning various sectors. Design pattern recognition and AI-driven manufacturing are transforming the design process, enabling more efficient and accurate product development. AI design software integrates with industrial design software, facilitating design feedback systems and design collaboration tools. Design for cost, design for assembly, design for sustainability, and design optimization techniques are being augmented by generative design applications and AI design process. Parametric design systems and generative design libraries are streamlining design exploration techniques, while design rule checking and design data management tools ensure consistency and accuracy.

- The integration of generative design process and software with CAD software, design automation tools, and 3D printing is revolutionizing product design. According to recent reports, the global market for AI in industrial design is expected to grow by over 25% annually, reflecting the ongoing unfolding of market activities and evolving patterns. For instance, a leading automotive manufacturer reported a 30% increase in design efficiency after implementing an AI-driven design process.

How is this Generative AI In Industrial Design Market segmented?

The generative AI in industrial design market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029,for the following segments.

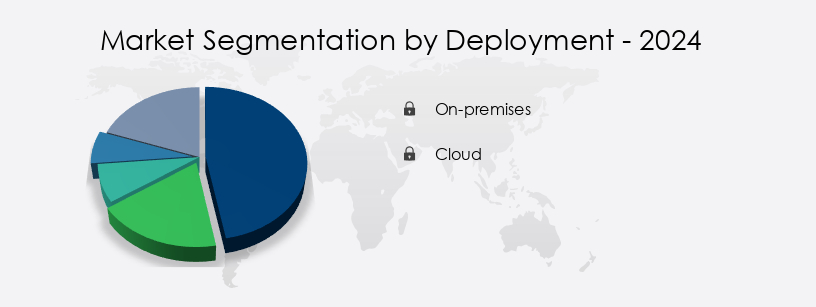

- Deployment

- On-premises

- Cloud

- Application

- Product design

- Prototyping and simulation

- Generative 3D modeling

- Design customization

- Others

- End-user

- Automotive

- Aerospace

- Furniture

- Construction

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Deployment Insights

The On-premises segment is estimated to witness significant growth during the forecast period. The on-premises model holds a substantial presence in the market. This approach, which involves installing and managing design software and infrastructure within an organization's physical facilities, is favored by industries with a strong emphasis on data security, intellectual property protection, performance control, and regulatory compliance. In sectors like automotive, aerospace, defense, and high-tech electronics, where design blueprints, material specifications, and engineering processes are critical competitive advantages, the risk of data breaches or IP leakage on external platforms is unacceptable. Parametric modeling software, generative design workflow, and topological optimization are integral components of on-premises generative AI solutions.

These technologies enable designers to explore design spaces, generate design patterns, and optimize shapes and materials, leading to innovative and efficient designs. Machine learning and reinforcement learning algorithms are also employed to enhance the design process, allowing for interactive generative design and iterative improvements. Moreover, digital twin technology and simulation-driven design are increasingly integrated into generative AI solutions, enabling real-time design analysis, optimization, and testing. Design constraint management and collaborative design platforms further streamline the design process, ensuring that all stakeholders are aligned and informed. According to recent industry reports, the market is projected to grow by over 25% annually, driven by the increasing adoption of AI-driven product design, customization, and optimization across various industries.

For instance, a leading automotive manufacturer reported a 30% reduction in design iteration cycles after implementing an AI-driven design solution, resulting in significant time and cost savings. Another key trend is the integration of Internet of Things (IoT) technology into machinery and equipment, enabling smart manufacturing and improved product performance.

Get Key Insights on Market Forecast (PDF)- Request Free Sample

Regional Analysis

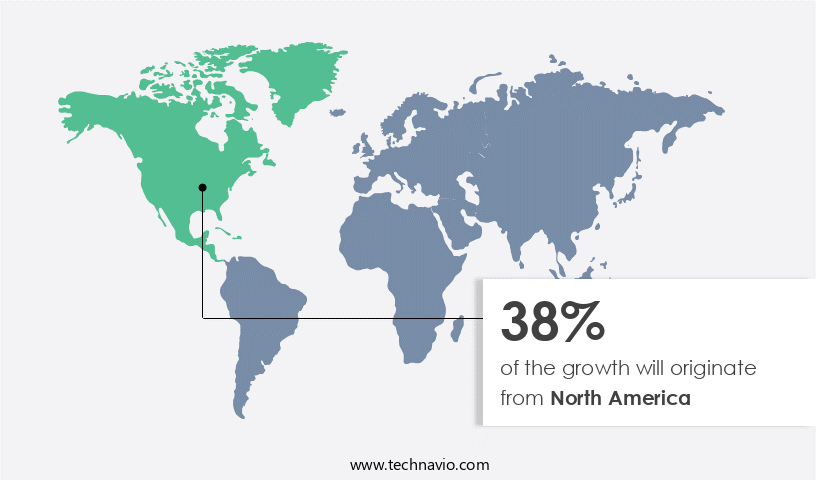

North America is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How generative AI in industrial design market Demand is Rising in North America Request Free Sample

In the market, North America, led by the United States, holds a prominent position. Factors fueling this dominance include a strong culture of technological innovation, substantial R&D investment, the presence of major software companies' headquarters, and the concentration of advanced end-user industries. The aerospace and defense sector, a significant contributor to the North American economy, is driving adoption. Companies in this sector utilize generative AI to design lightweight aircraft components for enhanced fuel efficiency and extended range, as well as to create intricate, high-performance parts for defense systems. For instance, a leading aircraft manufacturer reported a 15% reduction in design time using generative design algorithms.

Moreover, industry growth is anticipated to expand at a significant rate, with estimates suggesting a 20% increase in AI adoption in industrial design by 2025. This trend is fueled by the integration of advanced technologies such as reinforcement learning design, machine learning design, topological optimization, digital twin technology, and parametric modeling software into the generative design workflow. Additionally, the implementation of human-in-the-loop design, simulation-driven design, and design constraint management enhances the efficiency and accuracy of the design process. Furthermore, collaborative design platforms facilitate real-time design exploration, visualization, and iteration using generative design algorithms, neural network design, design pattern generation, and variational design methods.

AI-based design analysis and AI-assisted prototyping expedite the design optimization process, while deep learning design and shape optimization algorithms enable the creation of innovative designs. AI-powered material selection ensures the optimal use of resources, contributing to the overall sustainability of the design process.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The Generative AI in Industrial Design Market is transforming how products are conceptualized, optimized, and manufactured. Technologies like 3D generative design tools and CAD generative design enable engineers and designers to achieve AI design optimization through design exploration software and industrial design automation. These tools accelerate generative design iteration and enhance design space exploration, leading to more efficient solutions.

Applications such as design for additive manufacturing and collaborative design platforms are reshaping production workflows. AI design customization combined with design space visualization allows tailored solutions for unique use cases. By integrating parametric design systems with 3D printing integration and AI design applications, companies achieve seamless workflows in product design software and CAD software integration. Additionally, principles like design for manufacturability and design for user experience ensure functional and customer-centric outcomes, supported by an intelligent design feedback system.

Advanced solutions include generative AI for complex product design, AI-driven optimization of industrial components, and parametric modeling for rapid prototyping. Innovations such as machine learning algorithms for design exploration and neural network-based shape optimization in CAD drive precision and efficiency. Techniques like topological optimization for lightweight designs, deep learning models for design pattern generation, and reinforcement learning in design space exploration are becoming standard in high-performance industries. Workflows such as generative design workflow in industrial settings leverage AI-powered material selection for specific applications and human-in-the-loop systems for generative design processes to combine automation with expert oversight.

Efficiency is further enhanced through AI-assisted design review and feedback mechanisms, interactive generative design tools for industrial design, and collaborative design platforms based on generative AI. Trends like AI-driven design customization for mass personalization, generative design for sustainable industrial products, and design space visualization and interactive exploration support innovation while addressing environmental concerns. Finally, design constraint management for complex product design ensures all solutions meet performance, regulatory, and safety requirements. Simulation-driven design processes for complex products and design for additive manufacturing using generative AI ensure optimal production quality.

What are the key market drivers leading to the rise in the adoption of Generative AI In Industrial Design Industry?

- Expediting innovation and decreasing time-to-market is a key driver for the Generative AI in Industrial Design market, addressing the demands of today's competitive marketplace. This imperative drives both businesses and consumers alike, prioritizing agility and efficiency in product development. The global industrial design market, fueled by the increasing pressure to expedite innovation and product development, is experiencing robust growth due to the integration of generative AI. In sectors like automotive, consumer electronics, and industrial machinery, where competition is fierce and time-to-market is crucial, generative AI is revolutionizing the design process.

- According to recent studies, the industrial design market is expected to grow by 12% annually over the next five years. For instance, a leading automotive company reported a 10% increase in sales after implementing generative AI in their design process. This technology is transforming the industry landscape, enabling companies to stay competitive and innovate at an unprecedented pace. Traditional methods, which are linear, sequential, and reliant on a small team's expertise, are being replaced with AI-driven solutions that generate numerous design concepts in a fraction of the time.

What are the market trends shaping the Generative AI In Industrial Design Industry?

- The integration of multi-modal and natural language interfaces is an emerging market trend. This approach combines text and speech inputs to enhance user experience. Generative AI in industrial design is experiencing significant advancements, with a notable trend being the adoption of multi-modal and natural language prompting. This shift is set to expand access to this technology, moving beyond the realm of specialized engineers and analysts. Previously, utilizing generative design software demanded a profound comprehension of the underlying technology and the intricate process of defining design problems through a multitude of numerical inputs, boundary conditions, and manufacturing constraints.

- According to recent market research, the market is projected to grow by over 20% in the next year, demonstrating the technology's increasing relevance and potential impact. A prominent example of this trend's success can be seen in a leading manufacturing company, which reported a 15% increase in design efficiency after implementing a generative AI solution with natural language capabilities. However, the industry is now transitioning to more user-friendly, human-centric interfaces, making generative AI in industrial design more accessible and democratized.

What challenges does the Generative AI In Industrial Design Industry face during its growth?

- The high implementation costs and intricate integration with legacy systems pose a significant challenge, impeding the growth of industries. Generative AI holds immense potential in industrial design, offering the ability to create innovative and optimized designs through automated processes. However, the adoption of this technology faces substantial challenges due to the substantial financial investment and technical complexity involved. Major software companies offer leading generative design platforms as premium modules or top-tier subscription packages, representing a significant recurring expenditure.

- The industrial design market is expected to grow by over 25% in the next five years, reflecting the increasing demand for advanced design tools and the potential of generative AI to drive innovation and efficiency. The process of generating and simulating numerous design iterations is computationally intensive, necessitating powerful on-premises high performance computing (HPC) infrastructure or substantial cloud computing credits from providers like Amazon Web Services or Microsoft Azure. For instance, a leading automotive manufacturer reported a 30% reduction in design time and a 20% increase in design efficiency after implementing generative AI.

Exclusive Customer Landscape

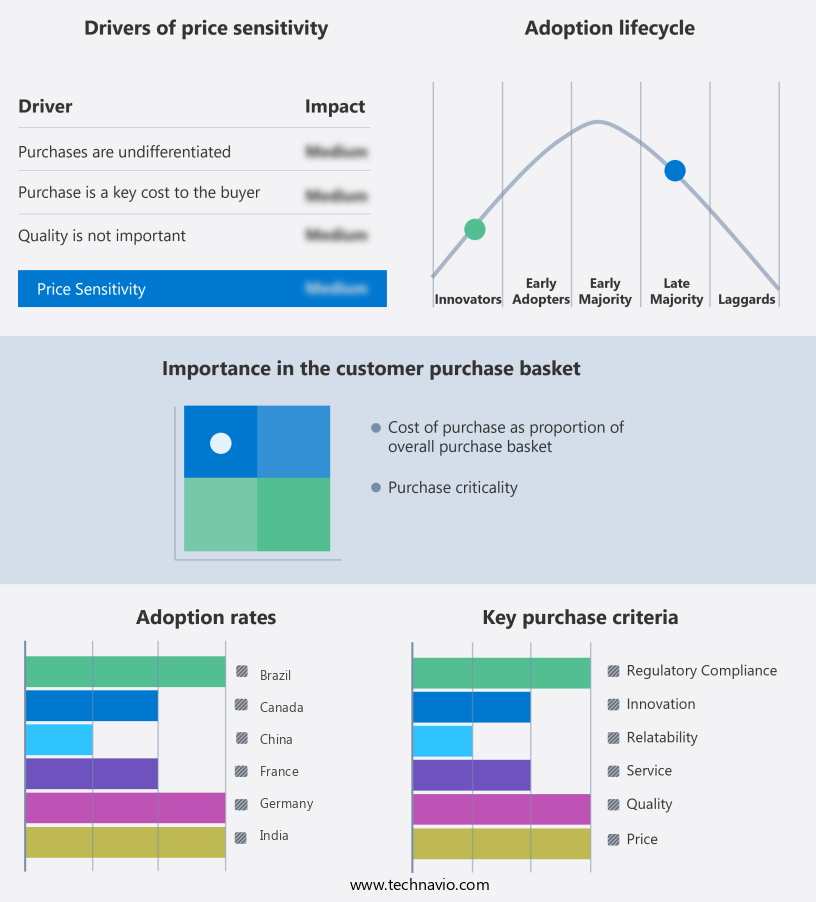

The generative AI in industrial design market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative AI in industrial design market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, generative AI in industrial design market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - The company specializes in generative AI technology for industrial design, featuring Firefly and GenStudio.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Altair Engineering Inc.

- ANSYS Inc.

- Aras Corp.

- Autodesk Inc.

- Bionic Mesh Design GmbH

- Dassault Systemes SE

- DeepMind Technologies Ltd.

- Desktop Metal Inc.

- ESI Group SA

- Hexagon AB

- Neural Concept.

- nTopology Inc.

- NVIDIA Corp.

- Proto Labs Inc.

- PTC Inc.

- RECRAFT INC.

- Siemens AG

- Trimble Inc.

- ZWSOFT CO. LTD.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative AI In Industrial Design Market

- In January 2024, Adidas and Autodesk announced a strategic partnership to integrate generative AI into Adidas' industrial design process. Autodesk's Dreamcatcher AI technology was employed to create innovative and unique sneaker designs, marking a significant step forward in the application of generative AI in industrial design (Adidas Press Release).

- In March 2024, Puma and NVIDIA collaborated to develop a generative AI model for creating sports footwear designs. The AI model was trained on historical Puma designs and customer preferences, enabling the creation of unique and customized designs (NVIDIA Press Release).

- In April 2025, Framatome, a global nuclear energy player, raised USD 100 million in a Series B funding round led by Airbus Ventures. The funds will be used to expand Framatome's generative AI capabilities in the industrial design of nuclear components, aiming for increased efficiency and safety (Business Wire).

- In May 2025, Ford Motor Company announced the acquisition of Generative Design Technologies, a startup specializing in generative AI for automotive design. The acquisition will enable Ford to significantly reduce design iteration cycles and create more innovative vehicle designs (Ford Press Release).

Research Analyst Overview

- The market for AI in industrial design continues to evolve, with applications spanning various sectors. Design pattern recognition and AI-driven manufacturing are transforming the design process, enabling more efficient and accurate product development. AI design software integrates with industrial design software, facilitating design feedback systems and design collaboration tools. Parametric design systems and generative design libraries are streamlining design exploration techniques, while design rule checking and design data management tools ensure consistency and accuracy.

- The integration of generative design process and software with CAD software, design automation tools, and 3D printing is revolutionizing product design. According to recent reports, the global market for AI in industrial design is expected to grow by over 25% annually, reflecting the ongoing unfolding of market activities and evolving patterns. For instance, a leading automotive manufacturer reported a 30% increase in design efficiency after implementing an AI-driven design process.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Industrial Design Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

242 |

|

Base year |

2024 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 35.3% |

|

Market growth 2025-2029 |

USD 1.4 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

33.0 |

|

Key countries |

China, Japan, India, South Korea, Germany, UK, France, US, Canada, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Generative AI In Industrial Design Market Research and Growth Report?

- CAGR of the Generative AI In Industrial Design industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the generative AI in industrial design market growth of industry companies

We can help! Our analysts can customize this generative AI in industrial design market research report to meet your requirements.

RIA -

RIA -