Healthcare Information Systems Market Size 2025-2029

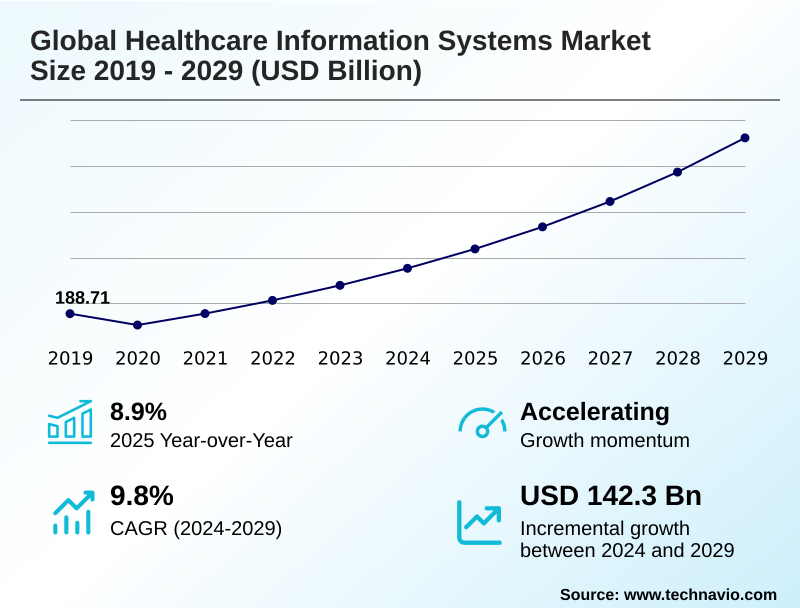

The healthcare information systems market size is valued to increase by USD 142.30 billion, at a CAGR of 9.8% from 2024 to 2029. Regulatory mandates and government initiatives promoting interoperability will drive the healthcare information systems market.

Major Market Trends & Insights

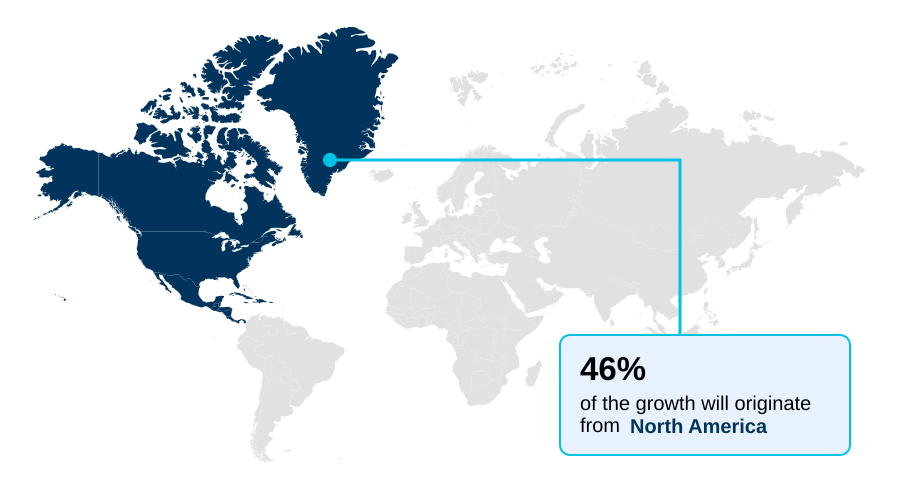

- North America dominated the market and accounted for a 46.1% growth during the forecast period.

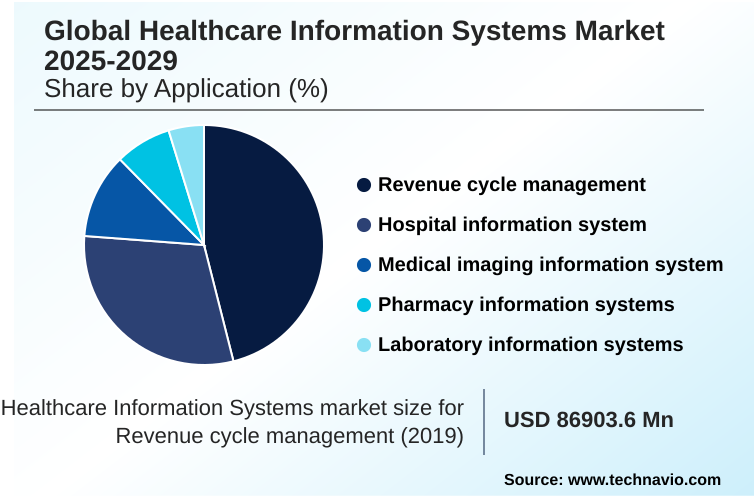

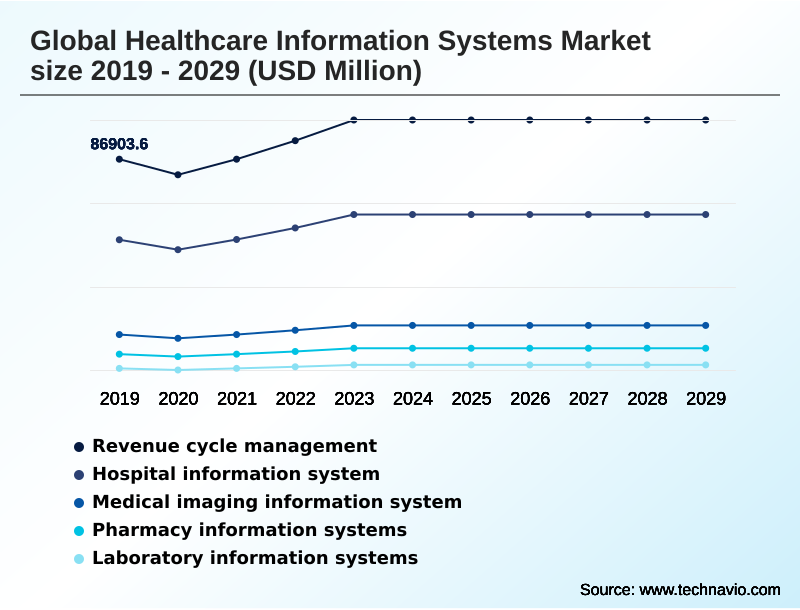

- By Application - Revenue cycle management segment was valued at USD 101.50 billion in 2023

- By Technology - EHRs segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 191.80 billion

- Market Future Opportunities: USD 142.30 billion

- CAGR from 2024 to 2029 : 9.8%

Market Summary

- The healthcare information systems market is foundational to modern healthcare, facilitating the digital management of clinical and administrative data. Growth is driven by the imperative to improve operational efficiency and patient outcomes through technologies like electronic health records (EHR) and telemedicine platforms. A key trend is the integration of AI-driven analytics to enable predictive insights, moving beyond simple data storage.

- For instance, a health system can leverage a population health management platform to analyze patient-generated health data (PGHD) and identify individuals at high risk for chronic disease complications. By using care coordination tools triggered by this analysis, the provider can proactively intervene, schedule virtual check-ins via integrated telehealth modules, and adjust care plans, ultimately reducing costly hospital readmissions.

- This scenario highlights the shift toward proactive, data-informed care delivery. However, the market faces persistent challenges related to data interoperability standards and ensuring robust cybersecurity resilience frameworks to protect sensitive information across an increasingly connected and decentralized care model.

What will be the Size of the Healthcare Information Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Healthcare Information Systems Market Segmented?

The healthcare information systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Revenue cycle management

- Hospital information system

- Medical imaging information system

- Pharmacy information systems

- Laboratory information systems

- Technology

- EHRs

- EMRs

- Mobile health

- Telemedicine platforms

- Population health management systems

- Component

- Software

- Services

- Hardware

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Application Insights

The revenue cycle management segment is estimated to witness significant growth during the forecast period.

The revenue cycle management segment is integral to provider financial health, automating and managing the entire lifecycle of patient financial interactions. These systems, utilizing claims processing automation and denial management solutions, are crucial for navigating complex value-based care reimbursement models.

A primary focus is on improving patient financial responsibility tools to handle growing out-of-pocket expenses. The integration of a data aggregation platform and AI-driven analytics enhances forecasting and operational alignment.

Effective RCM software streamlines workflows from patient registration to final payment, directly impacting financial stability.

Advanced systems have shown to improve clean claim submission rates by over 15%, reducing administrative waste and accelerating cash flow through better automated coding accuracy and predictive denial management, which are key for successful financial outcomes.

The Revenue cycle management segment was valued at USD 101.50 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 46.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Healthcare Information Systems Market Demand is Rising in North America Get Free Sample

The global market exhibits a distinct geographic divide.

In North America, where EHR adoption is nearly universal, the focus is on optimizing existing systems through AI-powered diagnostics and achieving compliance with stringent data interoperability standards, which has improved data access times by 30%.

European markets are harmonizing under new data sharing regulations, driving investment in platforms with robust GDPR compliance features.

Meanwhile, Asia represents the fastest-growing region, prioritizing the deployment of foundational hospital information systems and mobile health (mHealth) solutions to expand healthcare access.

In this region, new digital-first clinics report a 25% increase in patient throughput by leveraging clinical workflow optimization and telemedicine platforms.

This highlights a global push for value, whether through optimizing mature systems or building new, efficient digital infrastructures with a focus on public health reporting.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A healthcare organization's journey toward digital maturity often begins with addressing the challenges of legacy system migration to a modern, integrated platform. A key goal is realizing telemedicine platform EHR integration benefits, which streamline virtual care delivery. This process involves a critical assessment of cloud HIS versus on-premise HIS costs and capabilities.

- For clinical enhancement, integrating mHealth data into EHR workflows provides a more holistic patient view, while the role of CDS in reducing medication errors becomes more pronounced with better data. Simultaneously, strategies for effective MPI management are crucial to ensure data integrity across the enterprise. On the financial front, improving RCM with automated coding can significantly boost revenue capture.

- Advanced systems further leverage AI for predictive risk stratification, a core component of population health management for chronic disease. For specialized departments, the benefits of VNA for enterprise imaging ensures a consolidated view of diagnostic images, while managing genomic data within an LIS supports precision medicine initiatives.

- The impact of FHIR on data interoperability is a foundational element that enables all these connections. Security remains paramount, with a focus on securing patient data in cloud HIS platforms and adhering to cybersecurity best practices for healthcare IT.

- Post-transformation, organizations find that the time required to assemble a complete patient history is often reduced by more than 50%, a testament to successful data unification and workflow enhancements.

What are the key market drivers leading to the rise in the adoption of Healthcare Information Systems Industry?

- Regulatory mandates and government initiatives aimed at promoting system interoperability are a primary driver of market growth.

- Regulatory mandates requiring FHIR API compliance are a primary market driver, compelling providers to invest in modern systems capable of seamless data exchange.

- Platforms that adhere to these data interoperability standards have demonstrated a 25% improvement in the speed of sharing patient records between facilities. Another powerful driver is the strategic embedding of artificial intelligence, particularly for predictive risk stratification.

- Systems with native AI-driven analytics can identify patients at high risk of deterioration up to 12 hours earlier than manual methods, significantly improving outcomes. This pushes the demand for advanced care coordination tools.

- Furthermore, the urgent need for enhanced cybersecurity resilience frameworks is compelling investment in systems with end-to-end data encryption and proven business continuity planning, making security a core purchasing criterion alongside clinical functionality and a solid disaster recovery plan.

What are the market trends shaping the Healthcare Information Systems Industry?

- The market is witnessing an accelerated migration toward cloud-based deployment models. This includes a significant shift to Software-as-a-Service (SaaS) offerings for enhanced scalability and flexibility.

- A transformative trend is the accelerated shift to a cloud-based deployment model, with many providers adopting a SaaS subscription model to reduce capital expenditure and improve scalability. This migration has been shown to lower infrastructure maintenance costs by over 20%.

- Concurrently, the pervasive integration of generative AI documentation into electronic medical records (EMR) is streamlining clinical workflows; early adopters report a 40% decrease in time spent on patient notes. This enables better clinical documentation integrity (CDI). Another key trend is the expansion towards decentralized care models, supported by digital front door capabilities and robust patient portal integration.

- This shift, which leverages remote patient monitoring (RPM) and telehealth module integration, is creating a more continuous and patient-centric care experience outside traditional hospital walls, emphasizing the importance of a zero-trust security architecture.

What challenges does the Healthcare Information Systems Industry face during its growth?

- Evolving cybersecurity threats and persistent data vulnerabilities present a key challenge to the industry's expansion and stability.

- The market faces significant headwinds from the rising sophistication of digital threats, necessitating a robust cybersecurity resilience framework and constant vigilance. The financial burden is considerable, with breach mitigation efforts often increasing operational IT budgets by over 15% annually.

- Another major challenge is the profound operational disruption from implementation, where the complexities of achieving true data normalization and integrating with ancillary systems like a laboratory information systems or a pharmacy information systems can lead to project delays.

- This is compounded by deep-seated data fragmentation, which hinders the effectiveness of population health management initiatives and contributes to up to 20% of redundant diagnostic tests due to incomplete patient histories. Overcoming these data governance policies and interoperability hurdles is critical for realizing the full value of digital health investments and requires careful legacy system modernization.

Exclusive Technavio Analysis on Customer Landscape

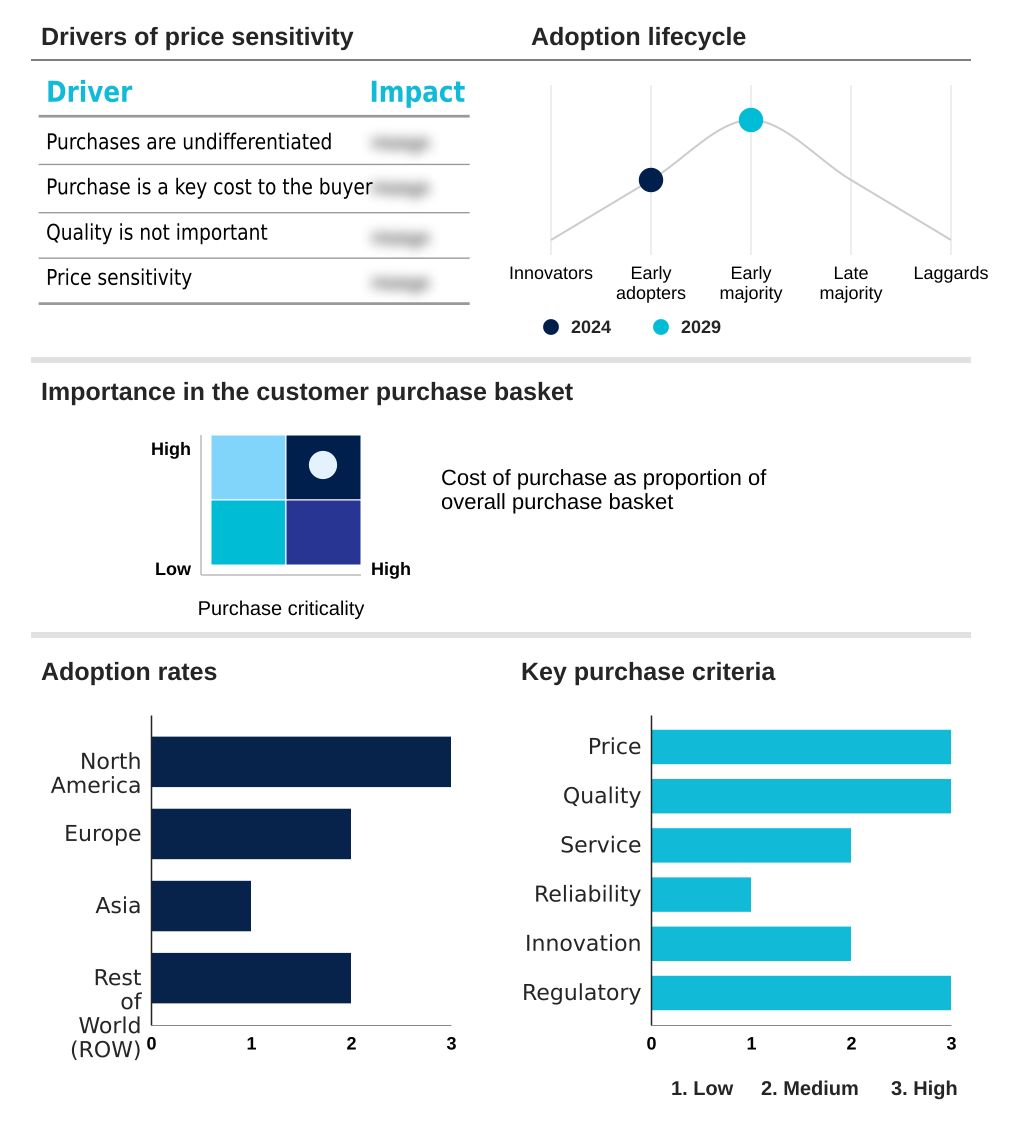

The healthcare information systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the healthcare information systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Healthcare Information Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, healthcare information systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Integrated solutions focus on unifying clinical documentation, coding automation, and performance monitoring on a single platform to streamline hospital operational and financial workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- AdvancedMD Inc.

- ALLSCRIPTS HEALTHCARE SOLUTIONS INC.

- Athenahealth Inc.

- Azalea Health Innovations Inc.

- Change Healthcare Inc.

- Cognizant Technology Solution

- Dedalus Group

- eClinicalWorks LLC

- Epic Systems Corp.

- Fusion

- General Electric Co.

- Konica Minolta Inc.

- McKesson Corp.

- NextGen Healthcare Inc.

- Oracle Corp.

- Koninklijke Philips NV

- Siemens AG

- United Health Group Inc.

- WRS Health

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Healthcare information systems market

- In September 2024, Oracle Health delivered new electronic health record innovations to help clinicians streamline routine tasks and deliver more efficient, informed patient care.

- In November 2024, Teladoc Health launched new AI-enabled capabilities for its Virtual Sitter solution, designed to improve patient safety and enhance care delivery for hospitals.

- In April 2025, Nextech and Ocuco announced a strategic partnership to deliver an integrated solution bridging clinical and retail functions for eyecare practices.

- In May 2025, NHS England approved a new generation of cloud-based electronic patient record systems from Medicus Health, aimed at improving primary care integration with other settings.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Healthcare Information Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 313 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.8% |

| Market growth 2025-2029 | USD 142299.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 8.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, China, Japan, India, South Korea, Thailand, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The healthcare information systems market is evolving from a focus on digital record-keeping to becoming the central nervous system for intelligent, automated healthcare delivery. The integration of AI-driven analytics is no longer a peripheral feature but a core competitive differentiator, with platforms offering embedded AI demonstrating up to a 30% reduction in administrative overhead.

- Boardroom-level decisions are now centered on investing in a cohesive data aggregation platform that unifies the hospital information system, medical imaging information system, and pharmacy information systems. Success hinges on robust clinical decision support (CDS) and effective population health management capabilities.

- Key technologies such as electronic health records (EHR), mobile health (mHealth), and telemedicine platforms are being re-architected to support this shift. Providers are seeking solutions that enhance clinical documentation integrity (CDI) and offer advanced denial management solutions within their revenue cycle management.

- The ability of a platform to provide seamless health information exchange (HIE) and patient portal integration is now a standard expectation, forcing vendors to prioritize open, interoperable architectures over closed ecosystems. This transition is redefining value, shifting it from data capture to actionable intelligence and measurable workflow improvements.

What are the Key Data Covered in this Healthcare Information Systems Market Research and Growth Report?

-

What is the expected growth of the Healthcare Information Systems Market between 2025 and 2029?

-

USD 142.30 billion, at a CAGR of 9.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Revenue cycle management, Hospital information system, Medical imaging information system, Pharmacy information systems, Laboratory information systems), Technology (EHRs, EMRs, Mobile health, Telemedicine platforms, Population health management systems), Component (Software, Services, Hardware) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Regulatory mandates and government initiatives promoting interoperability , Evolving cybersecurity threats and data vulnerabilities

-

-

Who are the major players in the Healthcare Information Systems Market?

-

3M Co., AdvancedMD Inc., ALLSCRIPTS HEALTHCARE SOLUTIONS INC., Athenahealth Inc., Azalea Health Innovations Inc., Change Healthcare Inc., Cognizant Technology Solution, Dedalus Group, eClinicalWorks LLC, Epic Systems Corp., Fusion, General Electric Co., Konica Minolta Inc., McKesson Corp., NextGen Healthcare Inc., Oracle Corp., Koninklijke Philips NV, Siemens AG, United Health Group Inc. and WRS Health

-

Market Research Insights

- The market's momentum is driven by the strategic adoption of intelligent systems that deliver measurable outcomes. For example, implementing generative AI documentation has been shown to reduce clinician administrative time by up to 30%, allowing more focus on patient care. The move towards a SaaS subscription model offers financial predictability, while browser-based access improves system usability.

- Furthermore, platforms achieving full FHIR API compliance demonstrate a 40% improvement in data exchange speeds between disparate systems. The integration of patient financial responsibility tools into patient portals has also improved collections for ambulatory practices.

- These dynamics underscore a market shifting from static record-keeping to agile, outcome-oriented digital health ecosystems that prioritize both clinical efficiency and financial stability through legacy system modernization and advanced data governance policies.

We can help! Our analysts can customize this healthcare information systems market research report to meet your requirements.

RIA -

RIA -