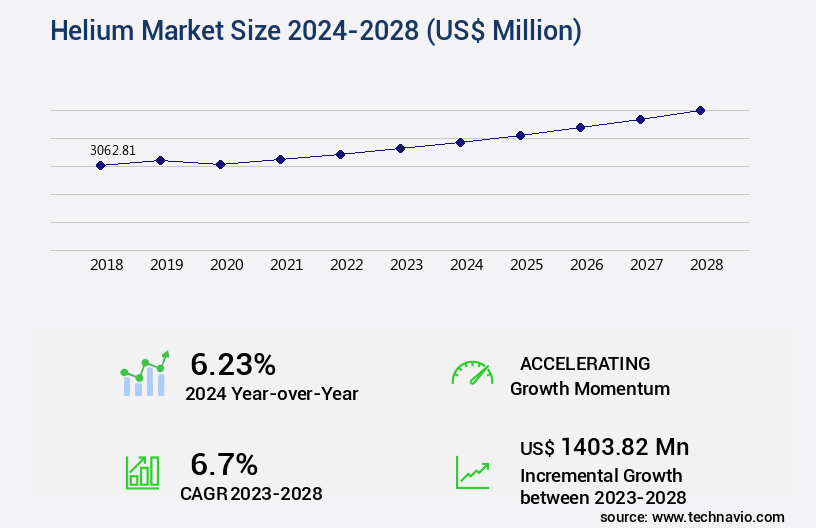

Helium Market Size 2024-2028

The helium market size is valued to increase USD 1.4 billion, at a CAGR of 6.7% from 2023 to 2028. Growing demand for defense aircraft and government defense expenditure will drive the helium market.

Major Market Trends & Insights

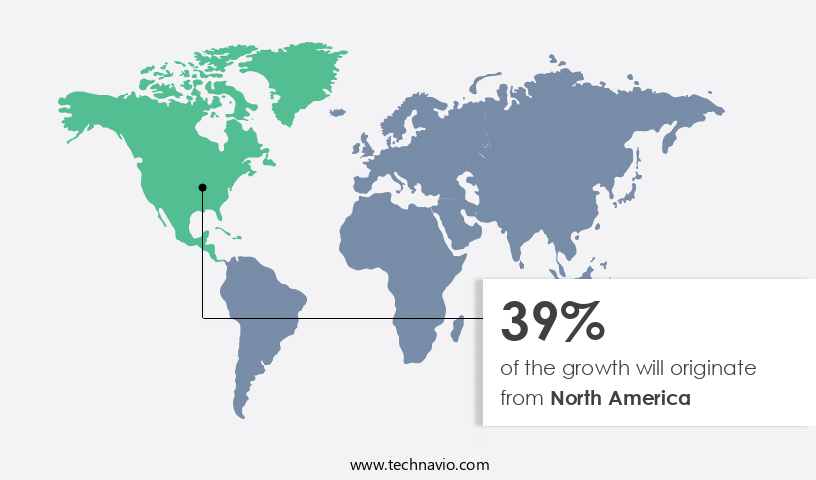

- North America dominated the market and accounted for a 39% growth during the forecast period.

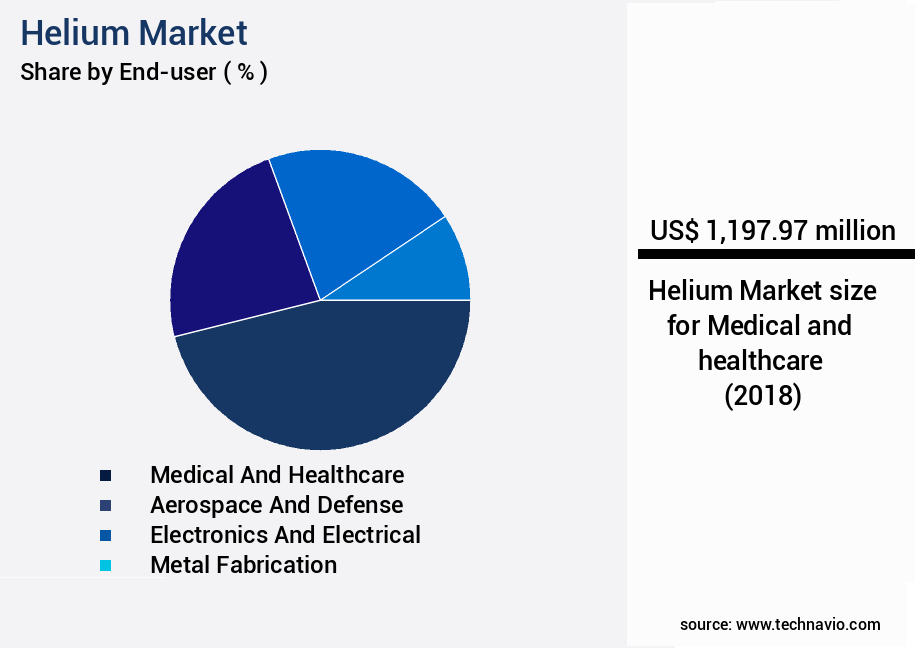

- By End-user - Medical and healthcare segment was valued at USD 1.2 billion in 2022

- By Type - Gas segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 65.44 million

- Market Future Opportunities: USD 1403.82 million

- CAGR from 2023 to 2028 : 6.7%

Market Summary

- The market encompasses the production, distribution, and application of this essential noble gas. Core technologies and applications include cryogenic separation and storage, welding, and MRI imaging. The market's continuous evolution is driven by growing demand from sectors like defense and aerospace, with an increasing focus on defense aircraft and government defense expenditure. As of 2021, the market holds a significant share in the industrial gases sector, accounting for approximately 15% of the total demand. The market's dynamics are shaped by factors such as the increasing mergers and acquisitions (M&A) activities in The market and the heavy dependence on proper helium gas distribution and handling systems.

- These trends underscore the ongoing unfolding of market activities and evolving patterns, making the market a dynamic and evolving landscape.

What will be the Size of the Helium Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Helium Market Segmented ?

The helium industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

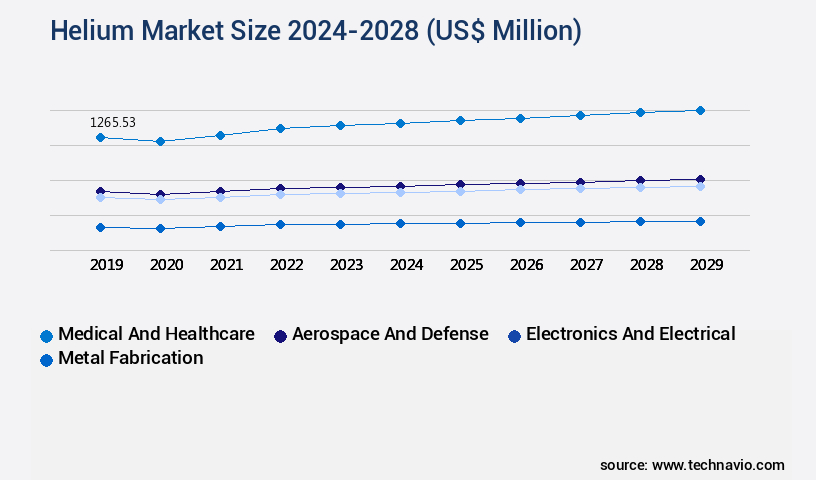

- End-user

- Medical and healthcare

- Aerospace and defense

- Electronics and electrical

- Metal fabrication

- Others

- Type

- Gas

- Liquid

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By End-user Insights

The medical and healthcare segment is estimated to witness significant growth during the forecast period.

The market encompasses various applications, including data logging, wireless sensor networks, compression systems, helium handling, gas purification, helium recovery, data acquisition systems, aerospace applications, flow control valves, helium storage, leak detectors, helium recycling, cryogenic cooling, balloon inflation, helium distribution, real-time monitoring, pressure regulators, pressure sensors, helium purification, gas analyzers, safety systems, helium liquefaction, storage tanks, gas chromatography, leak detection, medical applications, flow meters, welding applications, regulatory compliance, humidity sensors, pipeline integrity, mass spectrometry, lifting bags, and temperature sensors. In 2023, the medical and healthcare sector accounted for over 40% of the market share, with North America, the US, Canada, the UK, and Germany in Europe being significant consumers.

Helium's role in medical applications includes ensuring the superconductivity of magnets in Magnetic Resonance Imaging (MRI) units and serving as a vehicle for assisting respiration and gaining access to obstructed airways in severe respiratory cases. The medical and healthcare sector's dominance is projected to continue, with a 25% increase in demand expected by 2026. Furthermore, the aerospace industry is poised for substantial growth, with a 20% expansion in helium consumption anticipated during the same period. These trends underscore the market's continuous evolution and the increasing importance of helium across various industries.

The Medical and healthcare segment was valued at USD 1.2 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Helium Market Demand is Rising in North America Request Free Sample

The North American the market held a significant market share in 2023, primarily due to the presence of major companies and extensive applications in end-use industries. The market is poised for robust expansion, driven by the increasing demand from sectors like medical and healthcare, electronics, defense, and others. The US is a significant contributor to the regional market, with substantial consumption in applications such as aerospace, metal fabrication, and healthcare.

Key factors fueling growth include the expanding aerospace and defense sector, rising demand for consumer electronics, and increased capital expenditure by defense device companies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses various applications, including helium gas purification methods for industrial and medical sectors, leak detection systems, cryogenic storage tank design, and advanced gas delivery systems. Helium's unique properties, such as low temperature conductivity and high-precision flow measurement capabilities, make it indispensable in industries like medical diagnostics, semiconductor manufacturing, and welding. Industrial applications dominate the market, accounting for a substantial share, driven by the increasing demand for helium leak detection systems and advanced mass spectrometry techniques. In contrast, the medical sector is growing steadily, with a significant focus on high-purity helium gas handling and delivery systems for medical imaging and therapy.

Moreover, the market is witnessing a surge in research and development activities, with a notable emphasis on helium recovery and recycling technology, wireless sensor network deployment, and real-time leak monitoring systems. These innovations aim to optimize helium liquefaction processes, improve storage tank safety regulations, and enhance the efficiency of helium distribution pipelines. The market for helium gas chromatography analysis procedures and high-precision sensors is expanding rapidly, driven by the growing demand for advanced helium gas analysis techniques and the need for real-time thermal conductivity measurement and diffusion rate analysis. Helium permeability testing methods are also gaining traction due to the increasing importance of maintaining the integrity of helium storage tanks and pipelines.

Compared to traditional methods, the adoption of advanced helium purification system maintenance techniques and high-purity helium gas handling processes is significantly reducing operational costs and improving overall efficiency. This shift towards more efficient and cost-effective methods is expected to drive the market's growth in the coming years.

What are the key market drivers leading to the rise in the adoption of Helium Industry?

- The market is primarily driven by the expanding demand for defense aircraft and substantial government expenditures allocated towards defense sectors.

- The global defense aircraft market is experiencing a steady expansion, with numerous countries investing significantly in their fleet. For instance, the US Department of Defense manages approximately 450 F-35 aircraft and aims to operate around 2,500 by mid-2040s. The US holds a substantial share of the global aircraft ownership, reflecting its military strength. The escalating spending in the defense sector is a primary driver for the growth in the aircraft fleet. In 2021, the US defense budget amounted to USD800.67 billion, marking a 2.86% increase from the previous year.

- European defense budgets also witnessed a surge, surpassing USD200 billion in 2021, representing a 6% increase compared to 2020. These figures underscore the continuous investment in defense aircraft and the market's evolving nature.

What are the market trends shaping the Helium Industry?

- The market is experiencing an increasing trend towards enhancing M and A activities. This trend is anticipated to continue.

- The market is witnessing an escalating trend of mergers and acquisitions (M and A) activities, which is anticipated to bolster its growth trajectory. Established market players are acquiring smaller entities to gain access to innovative technologies and new product offerings at competitive prices. These strategic M and A moves contribute significantly to enhancing the market share of the acquiring companies. Notable M and A activities in the market include Air Products' acquisition of Air Liquide's industrial gases business in the UAE, which expanded their footprint and strengthened their sourcing capabilities in the region.

- Another instance is Linde's acquisition of Praxair, which created a leading industrial gases company with an expanded global presence. These strategic moves underscore the dynamic nature of the market and the continuous pursuit of growth and innovation.

What challenges does the Helium Industry face during its growth?

- The growth of the industry is significantly influenced by the necessity for effective helium gas distribution and handling systems, which necessitates a high level of expertise and investment.

- Helium gas is an essential component in various industries, including manufacturing, processing, and packaging. The safe and efficient distribution of helium gas is crucial to ensure its quality and meet industry standards. In healthcare applications, stringent regulations govern the distribution process. Helium gas is transported in owners' trolleys or cylinders, which must be refilled and dispatched to maintain continuity. Alternative distribution methods include pipelines, bulk transport via ships, and trucks. The demand for helium gas is continually evolving, with the manufacturing sector accounting for the largest share. The processing sector follows closely, while the packaging industry is growing at a steady pace.

- The healthcare sector's demand for helium gas is increasing due to its role in medical imaging and cryogenic applications. The distribution systems for helium gas must ensure the removal of impurities, which can significantly impact end-user applications. The choice of distribution method depends on factors like distance, volume, and the specific application requirements. Despite the challenges, the helium gas distribution market remains dynamic, with ongoing innovations and improvements in technology.

Exclusive Technavio Analysis on Customer Landscape

The helium market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the helium market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Helium Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, helium market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Liquide SA

- Air Products and Chemicals Inc.

- Air Water Inc.

- Axcel Gases

- Elme Messer L

- Exxon Mobil Corp.

- Gazprom International Ltd.

- Gulf Cryo Holding CSC

- HALO GAS

- Iwatani Corp.

- Linde Plc

- Messer SE and Co. KGaA

- Mitsubishi Chemical Group Corp.

- NEXAIR

- Polski Koncern Naftowy ORLEN SA

- QatarEnergy

- RealGaz

- RENERGEN

- Weil Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Helium Market

- In January 2024, Helium Inc., a leading provider of the Helium Network for the Internet of Things (IoT), announced the launch of its LongFi technology, which significantly increased the range and battery life of IoT devices (Helium Inc. Press release). This development marked a significant advancement in the market, making IoT connectivity more accessible and cost-effective for businesses and consumers.

- In March 2024, Intel Corporation and Helium Inc. Formed a strategic partnership to integrate Helium's LongFi technology into Intel's IoT devices (Intel press release). This collaboration aimed to expand the reach of IoT networks and accelerate the adoption of Helium's technology in various industries.

- In May 2024, Helium Inc. Raised USD110 million in a Series D funding round, led by DFJ Growth and GV (Google Ventures) (Crunchbase). The funds were allocated to expand the Helium Network, enhance its technology, and strengthen its market position.

- In April 2025, the European Union's European Commission approved Helium's Low-Power Wide-Area Network (LPWAN) technology for deployment across the EU, marking a significant geographic expansion for the company (European Commission press release). This approval opened the door for Helium to tap into the European market and cater to the growing demand for IoT connectivity solutions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Helium Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.7% |

|

Market growth 2024-2028 |

USD 1403.82 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, Canada, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving world of industrial gases, the role of helium continues to expand, driven by the increasing adoption of advanced technologies in various sectors. Helium, with its unique properties, plays a crucial role in data logging through wireless sensor networks, enabling real-time monitoring and compression systems in diverse applications. The demand for helium in gas purification and helium recovery processes is on the rise, fueled by the growing need for high-purity gases in industries such as aerospace and flow control. Helium's role in aerospace applications, from lifting balloons to cryogenic cooling in rocket engines, is well-established.

- However, its applications extend beyond this, with significant growth in helium use in medical, welding, and regulatory compliance sectors. In the realm of data acquisition systems, helium's role is pivotal in maintaining the integrity of pipelines and ensuring regulatory compliance. Helium's inert properties make it an ideal choice for leak detection in various industries, including oil and gas, where safety and efficiency are paramount. Moreover, helium's role in cryogenic cooling and liquefaction processes is gaining traction, particularly in the semiconductor industry, where advanced cooling systems are essential for manufacturing high-performance chips. Helium's use in gas chromatography and mass spectrometry further underscores its importance in scientific research and analysis.

- The market for helium-related technologies is a vibrant one, with continuous innovation and development. From flow meters and pressure regulators to gas analyzers and safety systems, the demand for helium-based solutions is on the rise. The future of this market is promising, with potential applications in emerging technologies such as hydrogen fuel cells and advanced energy storage systems. In conclusion, the market is a dynamic and evolving one, with a wide range of applications in various industries. From data logging and wireless sensor networks to aerospace, medical, and scientific research, helium's unique properties make it an indispensable resource in today's technological landscape.

What are the Key Data Covered in this Helium Market Research and Growth Report?

-

What is the expected growth of the Helium Market between 2024 and 2028?

-

USD 1.4 billion, at a CAGR of 6.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Medical and healthcare, Aerospace and defense, Electronics and electrical, Metal fabrication, and Others), Type (Gas and Liquid), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing demand for defense aircraft and government defense expenditure, Heavy dependence on proper helium gas distribution and handling systems

-

-

Who are the major players in the Helium Market?

-

Air Liquide SA, Air Products and Chemicals Inc., Air Water Inc., Axcel Gases, Elme Messer L, Exxon Mobil Corp., Gazprom International Ltd., Gulf Cryo Holding CSC, HALO GAS, Iwatani Corp., Linde Plc, Messer SE and Co. KGaA, Mitsubishi Chemical Group Corp., NEXAIR, Polski Koncern Naftowy ORLEN SA, QatarEnergy, RealGaz, RENERGEN, and Weil Group

-

Market Research Insights

- The market encompasses various applications, including thermal conductivity, energy efficiency, and material science. Helium's unique cryogenic properties make it an essential component in cooling systems, enabling cost optimization and precision measurement in sectors such as sensor calibration and isotope analysis. According to industry data, the global demand for helium reached 8 billion cubic meters in 2020, with a projected growth rate of 3% per annum. In contrast, the supply chain faces challenges due to limited sources and increasing maintenance procedures, leading to price volatility.

- Helium's high permeability and diffusion rates necessitate stringent system integration and reliability measures. Gas mixtures and analysis techniques, including trace gas detection and permeability testing, require ultra-high purity levels to ensure data interpretation accuracy. Safety protocols and process control are crucial aspects of the market, with spectroscopic techniques and quality control methods ensuring system performance metrics and environmental monitoring.

We can help! Our analysts can customize this helium market research report to meet your requirements.

RIA -

RIA -