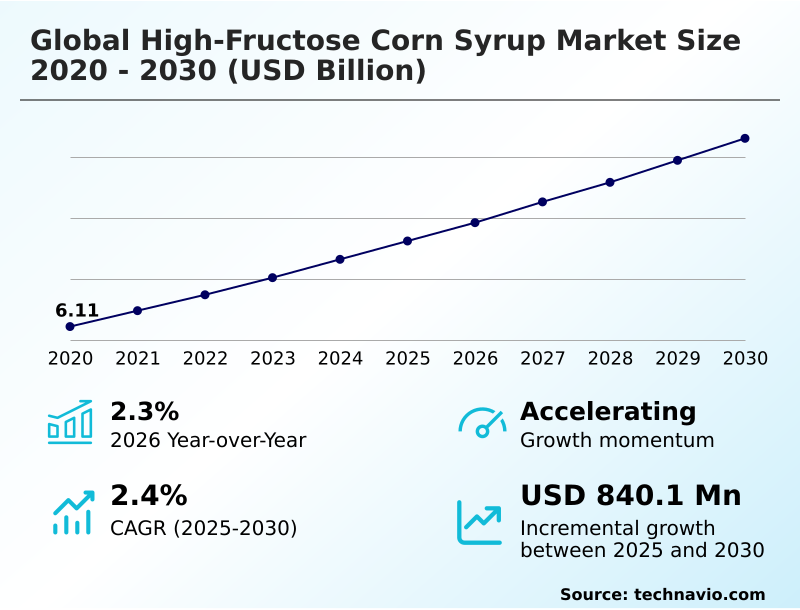

High-fructose Corn Syrup Market Size 2026-2030

The high-fructose corn syrup market size is valued to increase by USD 840.1 million, at a CAGR of 2.4% from 2025 to 2030. Strategic requirement for cost efficiency amid sugar price volatility will drive the high-fructose corn syrup market.

Major Market Trends & Insights

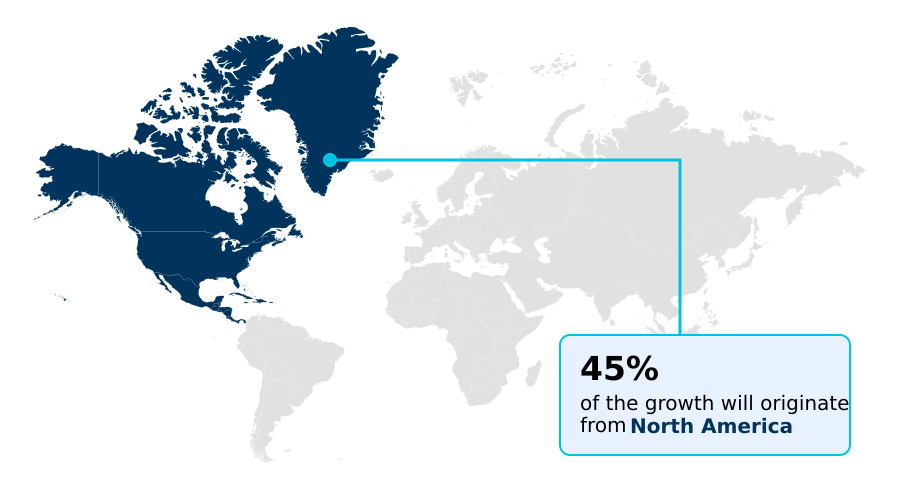

- North America dominated the market and accounted for a 44.6% growth during the forecast period.

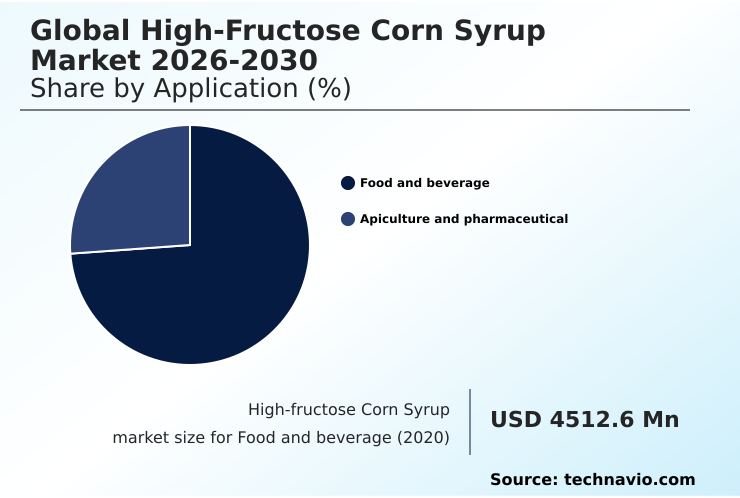

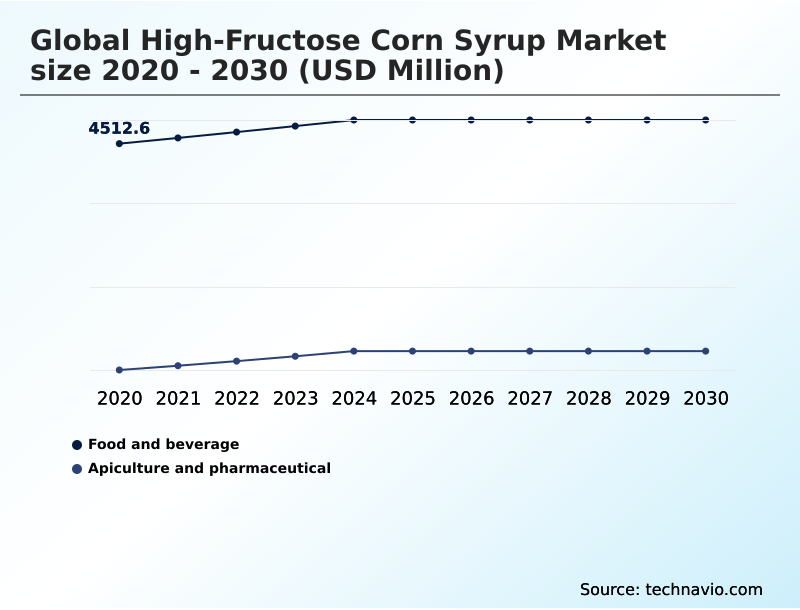

- By Application - Food and beverage segment was valued at USD 4.82 billion in 2024

- By Product Type - HFCS-55 segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.54 billion

- Market Future Opportunities: USD 840.1 million

- CAGR from 2025 to 2030 : 2.4%

Market Summary

- The high-fructose corn syrup market is defined by its critical role as a caloric sweetener in global food and beverage manufacturing. The core of the market revolves around the enzymatic isomerization of corn starch derivatives to produce a liquid sweetener formulation with a specific fructose-to-glucose ratio, such as HFCS-42 and HFCS-55.

- This process delivers significant functional benefits, including humectant properties for shelf-life extension and superior stability in acidic solutions, making it indispensable for carbonated soft drinks and processed foods. A key business scenario involves beverage producers using automated blending systems to manage raw material volatility.

- By dynamically adjusting the mix of high-fructose corn syrup and other sweeteners based on real-time commodity prices, companies can achieve a cost-optimization strategy that protects margins without altering the established sensory profile. This operational agility, combined with the sweetener's functional versatility, underscores its persistent value despite challenges from clean label alternatives and evolving consumer health perceptions.

What will be the Size of the High-fructose Corn Syrup Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the High-fructose Corn Syrup Market Segmented?

The high-fructose corn syrup industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Food and beverage

- Apiculture and pharmaceutical

- Product type

- HFCS-55

- HFCS-42

- Others

- Distribution channel

- Offline

- Online

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Application Insights

The food and beverage segment is estimated to witness significant growth during the forecast period.

The food and beverage segment is foundational, driven by the industrial requirement for a high-solubility sweetener. The sector's reliance on high-fructose corn syrup is pronounced in ready-to-drink formulation, where its properties as a beverage stabilizer are critical.

This liquid carbohydrate source is also integral to confectionery production and as a processed bakery ingredient, valued for its humectant effects in baked goods.

Manufacturers leverage its functional texturizer capabilities and cost-optimization strategy, with data indicating that optimizing sweetener blending systems can reduce raw material expenditure by over 12% compared to using single-source sweeteners alone.

This industrial sweetener economics makes it a staple in high-volume food processing, especially as a condiment formulation agent and dairy product stabilizer.

The Food and beverage segment was valued at USD 4.82 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How High-fructose Corn Syrup Market Demand is Rising in North America Get Free Sample

The geographic landscape is shifting, with mature markets focusing on efficiency and emerging regions driving volume. In North America, the focus is on optimizing isoglucose production and developing advanced liquid handling systems to manage costs.

Europe is navigating stringent regulations, promoting biocatalytic optimization in its processing plants. The APAC region is a major growth driver, where the ingredient is a key component in everything from a non-alcoholic beverage sweetener to a savory snack ingredient.

In these regions, the use of a liquid carbohydrate source is essential for scaling up production of shelf-stable food additives.

The industry's ability to provide a volatility-resistant sweetener has been crucial, with firms reporting that integrated supply chains have reduced logistics-related disruptions by up to 25% compared to non-integrated models.

This resilience is vital as the product expands into roles like a processed meat binder and soup base thickener.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A critical analysis of the market reveals nuanced decision-making based on specific applications. The high-fructose corn syrup vs sucrose cost debate remains central to procurement, with industrial users frequently choosing corn sweeteners due to the cost efficiency of liquid sweeteners.

- The use of hfcs-55 in carbonated soft drinks is standard due to the functional benefits of hfcs in beverages, particularly the stability of hfcs in acidic solutions. Conversely, hfcs-42 for bakery moisture retention is selected for its superior humectant effects in baked goods and for maillard reaction enhancement with hfcs.

- The impact of hfcs on food texture is a key consideration for formulators. In pharmaceuticals, the selection of pharmaceutical grade hfcs as an excipient is driven by purity requirements. Beyond food, high-fructose corn syrup in apiculture serves as a reliable honeybee feed supplement.

- The industry grapples with challenges such as replacing hfcs with clean label alternatives and navigating regulatory challenges for hfcs labeling. These factors, combined with the hfcs supply chain and corn prices, highlight the complexity of the market.

- Firms that master the enzymatic isomerization of corn starch through efficient processing of corn wet-milling showcase a distinct competitive advantage, which is more than twice as effective in cost reduction than simple raw material substitution.

What are the key market drivers leading to the rise in the adoption of High-fructose Corn Syrup Industry?

- A primary driver shaping the market is the strategic requirement for cost efficiency in the face of ongoing sugar price volatility.

- Market growth is primarily driven by economic and functional advantages in large-scale food manufacturing. The sweetener cost advantage over sucrose remains a powerful incentive, especially given persistent raw material volatility, making high-fructose corn syrup a cornerstone of cost-optimization strategy.

- Functionally, its role as a moisture retention agent and its humectant properties are indispensable in the processed bakery ingredient sector.

- For beverage applications, its high solubility and stability as an acid-stable sweetener make it ideal for automated blending systems used in carbonated soft drink formulation.

- The transition to liquid sweetener formulation has streamlined production lines, with adoption rates in new beverage plants exceeding 80%. This combination of economic drivers and superior functional performance in high-volume food processing ensures its continued relevance.

What are the market trends shaping the High-fructose Corn Syrup Industry?

- The market is observing a significant trend toward the expansion of precision fermentation. This is complemented by the adoption of enzyme-enhanced processing to improve manufacturing efficiency.

- Key market trends revolve around enhancing production efficiency and expanding application scope. The adoption of precision fermentation efficiency is enabling the creation of highly specialized enzyme cocktails for enzymatic conversion technology, improving yields from the saccharification process. This move toward biocatalytic optimization reduces the energy and chemical inputs required in traditional isoglucose production.

- This trend allows for more precise control over the final liquid carbohydrate source, with some advanced facilities achieving a 5% greater consistency in fructose-to-glucose ratio. Concurrently, there is growing demand for the ingredient as a non-food humectant use and a shelf-stable food additive, pushing the boundaries beyond its traditional role as a caloric sweetener.

- The ongoing refinement of these technologies is critical for maintaining a competitive edge.

What challenges does the High-fructose Corn Syrup Industry face during its growth?

- A key challenge for the industry stems from the intensification of regulatory scrutiny, particularly regarding the classification of products as ultra-processed foods.

- The market confronts significant challenges from regulatory pressures and evolving consumer preferences. Intensifying regulatory scrutiny and the negative connotations of ultra-processed food classification are impacting consumer health perception, creating demand for clean label alternatives.

- The technical difficulty of functional ingredient replacement poses a substantial hurdle, as few alternatives can match the sensory characteristic impact of high-fructose corn syrup at a comparable price. This is compounded by agricultural input costs and supply chain fragility, which can erode the ingredient's price advantage.

- Manufacturers report that reformulating a single product line to remove corn syrup can increase R&D costs by up to 20%. Navigating these challenges requires a strategic focus on demonstrating functional necessity and managing supply chain risks effectively.

Exclusive Technavio Analysis on Customer Landscape

The high-fructose corn syrup market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the high-fructose corn syrup market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of High-fructose Corn Syrup Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, high-fructose corn syrup market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGRANA Beteiligungs AG - Offers glucose-fructose syrups with customized fructose ratios, engineered for large-scale industrial food and beverage applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGRANA Beteiligungs AG

- Archer Daniels Midland Co.

- Cargill Inc.

- Dacheng Corn Group Co. Ltd

- Daesang Corp.

- FoodChem International Corp.

- Ingredion Inc.

- Luzhou Bio-Chem Technology

- Prinova Group LLC

- Qinhuangdao Lihua Starch Co.

- Roquette Freres SA

- Samyang Corp.

- Sedamyl

- Shandong Dongxiao Biotechnology

- Sweetener Supply Corp.

- Tate and Lyle Plc

- Tereos SCA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in High-fructose corn syrup market

- In October 2024, Cargill Inc. announced a strategic investment to upgrade its corn wet-milling facilities, focusing on enhancing enzyme-enhanced processing to improve the efficiency and yield of its liquid sweetener formulation, aiming for a 10% reduction in energy consumption.

- In December 2024, Ingredion Inc. launched a new portfolio of specialty HFCS blends, designed as a functional texturizer and moisture retention agent for clean label bakery alternatives, addressing the technical friction of replacing traditional ingredients.

- In March 2025, Archer Daniels Midland Co. entered a partnership with a leading beverage manufacturer to implement advanced sweetener blending systems, enabling dynamic switching between HFCS-55 and other sweeteners to mitigate raw material volatility.

- In May 2025, Tate and Lyle Plc received new regulatory approval for its pharmaceutical grade excipient line of high-fructose corn syrup, expanding its use as a liquid medication vehicle in pediatric formulations due to its effective taste-masking properties.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled High-fructose Corn Syrup Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.4% |

| Market growth 2026-2030 | USD 840.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The high-fructose corn syrup market is underpinned by advanced industrial biotechnology, where processes like enzymatic isomerization and biocatalytic optimization are pivotal. The industry relies on glucose isomerase within corn wet-milling facilities to execute a saccharification process that creates a corn starch derivative with a specific fructose-to-glucose ratio.

- This liquid sweetener formulation, whether HFCS-42 or HFCS-55, serves as a foundational caloric sweetener. Its utility extends beyond sweetness; its humectant properties and function as a moisture retention agent are critical for shelf-life extension. In baking, it aids Maillard reaction browning, while its non-crystallizing syrup nature makes it an ideal beverage stabilizer and functional texturizer.

- The use of automated blending systems and liquid handling systems allows for a cost-optimization strategy, making it a volatility-resistant sweetener. For boardroom decisions, the choice to invest in enzyme-enhanced processing technology directly impacts operational expenditure, with some operators reporting a 15% reduction in processing costs.

- This high brix syrup is also crucial in cold-fill beverage systems and ready-to-drink formulation, acting as an acid-stable sweetener. Its role as a microbial growth inhibitor through osmotic pressure control has also led to its use as a pharmaceutical grade excipient.

What are the Key Data Covered in this High-fructose Corn Syrup Market Research and Growth Report?

-

What is the expected growth of the High-fructose Corn Syrup Market between 2026 and 2030?

-

USD 840.1 million, at a CAGR of 2.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Food and beverage, and Apiculture and pharmaceutical), Product Type (HFCS-55, HFCS-42, and Others), Distribution Channel (Offline, and Online) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Strategic requirement for cost efficiency amid sugar price volatility, Intensification of regulatory scrutiny and ultra-processed food classification

-

-

Who are the major players in the High-fructose Corn Syrup Market?

-

AGRANA Beteiligungs AG, Archer Daniels Midland Co., Cargill Inc., Dacheng Corn Group Co. Ltd, Daesang Corp., FoodChem International Corp., Ingredion Inc., Luzhou Bio-Chem Technology, Prinova Group LLC, Qinhuangdao Lihua Starch Co., Roquette Freres SA, Samyang Corp., Sedamyl, Shandong Dongxiao Biotechnology, Sweetener Supply Corp., Tate and Lyle Plc and Tereos SCA

-

Market Research Insights

- Market dynamics are shaped by a complex interplay of economic and technical factors. The persistent sweetener cost advantage is a primary consideration, though it is frequently tested by raw material volatility and agricultural input costs.

- A major pressure point is the consumer-driven push for clean label alternatives, which creates friction for manufacturers concerned about sensory characteristic impact and functional ingredient replacement costs. The industry also navigates intense regulatory scrutiny and the ultra-processed food classification debate, which influences consumer health perception. Simultaneously, opportunities are emerging in non-food humectant use and apiculture feed supplements.

- The efficiency of enzymatic conversion technology remains a competitive differentiator, especially for high-volume food processing in applications ranging from non-alcoholic beverage sweeteners and processed bakery ingredients to condiment formulation. The stability of the ingredient in products like fruit preparation sweeteners and as a savory snack ingredient continues to reinforce its position against supply chain fragility.

We can help! Our analysts can customize this high-fructose corn syrup market research report to meet your requirements.

RIA -

RIA -