High Temperature 3D Printing Plastics Market Size 2025-2029

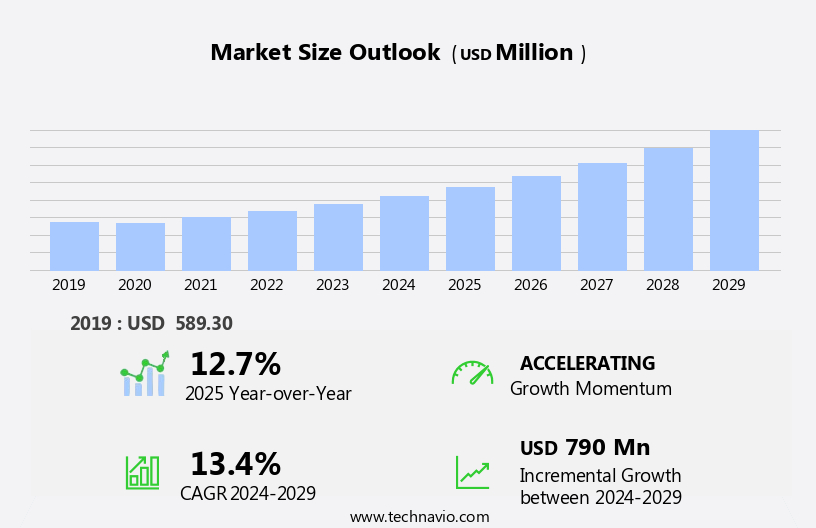

The high temperature 3d printing plastics market size is forecast to increase by USD 790 million, at a CAGR of 13.4% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by increasing applications in the automotive industry. This sector's adoption of high-temperature 3D printing plastics is escalating due to their ability to withstand extreme temperatures and enhance vehicle performance. Furthermore, product launches in this market continue to expand the technological frontier, introducing innovative solutions and materials. However, the high cost of materials poses a substantial challenge for market expansion. The use of high-performance polymers in high-temperature 3D printing results in a higher price point compared to traditional manufacturing methods.

- Companies must navigate this obstacle by exploring cost reduction strategies, such as optimizing material usage or developing more cost-effective alternatives. Effective management of these challenges and continued innovation will be crucial for market participants to capitalize on the burgeoning opportunities in the market.

What will be the Size of the High Temperature 3D Printing Plastics Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, driven by the ongoing development of advanced materials and technologies. This sector encompasses various additive manufacturing techniques, including Vat Polymerization, Material Extrusion, and Powder Bed Fusion, each with unique advantages and applications. High-performance thermoplastics, such as Polycarbonate (PC) and Polyetheretherketone (PEEK), are increasingly adopted for their excellent creep resistance, dimensional accuracy, and mechanical strength. These materials are finding widespread use in engineering applications, particularly in the aerospace and automotive industries. The market's dynamics are further shaped by the integration of smart manufacturing, circular economy principles, and digital manufacturing. These trends enable on-demand manufacturing, reduce material waste, and optimize production processes.

Polypropylene (PP) and other engineering plastics are gaining popularity due to their chemical resistance, thermal stability, and cost-effectiveness. The market's continuous growth is also fueled by advancements in material characterization, process monitoring, and printing resolution. The applications of high temperature 3D printing plastics span various sectors, including consumer products, functional prototypes, and product development. As the technology matures, it is increasingly adopted for the production of complex geometries, wear-resistant parts, and heat-resistant polymers. The market's future is marked by the integration of artificial intelligence (AI) and automation, enabling process optimization, part finishing, and the creation of jigs and fixtures.

The environmental impact of 3D printing plastics remains a critical concern, with ongoing efforts to minimize waste and improve sustainability. In summary, the market is characterized by continuous innovation and evolution, driven by the development of advanced materials, technologies, and manufacturing processes. The market's applications span various industries, with a focus on engineering applications and the production of complex geometries. The integration of smart manufacturing, circular economy principles, and digital manufacturing is shaping the market's future, enabling on-demand manufacturing, reducing material waste, and optimizing production processes.

How is this High Temperature 3D Printing Plastics Industry segmented?

The high temperature 3d printing plastics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Aerospace

- Healthcare

- Electrical and electronics

- Automotives

- Others

- Type

- Polyetherimide (PEI)

- Polyetheretherketone (PEEK)

- Polyphenylsulfone (PPSU)

- Polyetherketoneketone (PEKK)

- Geography

- North America

- US

- Europe

- France

- Germany

- Spain

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

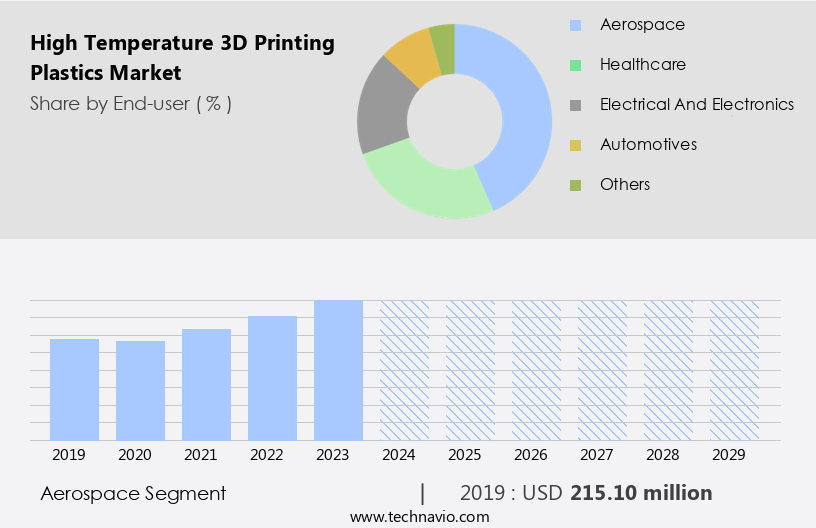

The aerospace segment is estimated to witness significant growth during the forecast period.

In the aerospace sector, high temperature 3D printing plastics play a pivotal role in manufacturing various components that endure extreme temperatures and mechanical stress. Materials such as Polyetheretherketone (PEEK) and Ultem are preferred for their high creep resistance, tensile strength, and thermal stability. These materials are utilized to produce intricate brackets, ducts, and other structural components, enabling improved performance and efficiency in aircraft production. Furthermore, high temperature 3D printing plastics are indispensable in the fabrication of engine parts. The technology's ability to create complex geometries that are challenging to achieve with conventional manufacturing methods significantly enhances the overall functionality of aerospace components.

Material extrusion and vat polymerization techniques are widely adopted for manufacturing these high-performance thermoplastics. The build platform and printing parameters are meticulously controlled to ensure dimensional accuracy and surface finish. Custom manufacturing and on-demand production enable rapid prototyping and application development, leading to cost savings and faster time-to-market. The integration of artificial intelligence and smart manufacturing technologies further optimizes the process, ensuring quality control and process monitoring. The circular economy principle is increasingly adopted in the industry, reducing waste and promoting sustainability. Heat-resistant polymers like polycarbonate (PC), polyamide (PA), and polypropylene (PP) are also utilized in the aerospace sector due to their excellent chemical resistance and impact strength.

Overall, the market is witnessing significant growth, driven by the aerospace industry's increasing adoption of advanced manufacturing technologies and the demand for lightweight, high-performance components.

The Aerospace segment was valued at USD 215.10 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

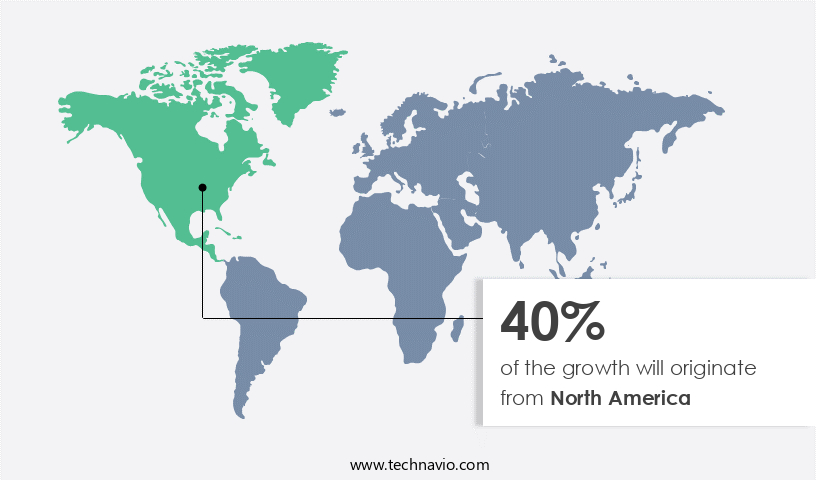

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is witnessing significant growth due to technological advancements in additive manufacturing and increasing demand from industries like aerospace, automotive, and healthcare. The region's robust industrial base, particularly in these sectors, is a major driver. The implementation of 3D printing technologies in these industries enhances production efficiency and facilitates the creation of intricate, high-performance components. Moreover, the healthcare sector's growing dependence on 3D printing for customized medical devices and implants is fueling market expansion. Advancements in material science, such as high-performance thermoplastics like polycarbonate (PC), polyetheretherketone (PEEK), and polyamide (PA), are revolutionizing the industry.

These materials offer superior creep resistance, dimensional accuracy, and mechanical strength, making them ideal for various applications. Moreover, the integration of artificial intelligence (AI) in 3D printing processes enhances design freedom, application development, and process optimization. The market's growth is also driven by the increasing adoption of on-demand manufacturing, which reduces inventory costs and leads to faster time-to-market. The circular economy trend is another factor contributing to market growth, as 3D printing enables the production of parts with minimal waste. Key players in the market focus on material characterization, process monitoring, and quality control to ensure the production of high-quality 3D printed parts.

The market's environmental impact is also a concern, and efforts are being made to develop sustainable material feedstocks and reduce energy consumption. The market's future lies in advanced manufacturing techniques like stereolithography (SLA), powder bed fusion, and material extrusion. These technologies enable the production of complex geometries, high-resolution prints, and large build volumes, making them suitable for various industries. In conclusion, the market in North America is experiencing significant growth due to technological advancements, increasing demand from key industries, and the adoption of sustainable manufacturing practices. The market's future lies in the development of advanced manufacturing techniques and the production of high-performance materials.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of High Temperature 3D Printing Plastics Industry?

- The automotive sector's growth serves as the primary catalyst for market expansion, given its significant influence on industry development.

- The market is experiencing significant growth, primarily driven by the automotive industry's expanding applications. High-performance thermoplastics, such as PEEK and Ultem, are increasingly integrated into automotive manufacturing for electric mobility solutions and advanced vehicle components due to their exceptional thermal stability and mechanical strength. In February 2024, a leading automotive supplier, Schaeffler, announced the opening of a new facility in the US dedicated to producing electric mobility solutions, highlighting the growing demand for high temperature 3D printing plastics in this sector. These materials are essential for the performance and safety of electric vehicle components, which must withstand rigorous conditions.

- The market's growth is further fueled by the increasing adoption of 3D printing technology in various industries, including aerospace, healthcare, and energy, where high-temperature plastics are used for complex geometries and immersive designs. The market's growth is harmonious and emphasizes the importance of innovative materials and technologies in addressing the evolving demands of diverse industries.

What are the market trends shaping the High Temperature 3D Printing Plastics Industry?

- Product launches have emerged as a significant market trend. It is essential for businesses to stay informed and prepared for these events to capitalize on new opportunities and maintain a competitive edge.

- The market is experiencing notable growth due to continuous product innovations and launches. One recent development came in February 2024, when Evonik introduced a new photopolymer resin for digital light processing (DLP) 3D printers. This flame-retardant and mechanically robust material, certified with a UL 94 flame retardancy rating of V-0 at a 3mm thickness, highlights the industry's focus on safety and durability. The resin's pourable nature at room temperature and post-processing capabilities enable the creation of parts with desired surface textures. The cured product boasts high elongation at break, offering flexibility and resilience similar to acrylonitrile butadiene styrene (ABS) plastics.

- Capital expenditures on high-performance thermoplastics for vat polymerization and material extrusion processes are driving market expansion. Printing parameters for these plastics are being optimized through the integration of artificial intelligence (AI) and machine learning algorithms, enhancing custom manufacturing capabilities. Functional prototypes and 3D printed parts are increasingly being used in various industries for application development and design freedom. The additive manufacturing and rapid prototyping sectors are benefiting significantly from these advancements.

What challenges does the High Temperature 3D Printing Plastics Industry face during its growth?

- The escalating costs of materials pose a significant challenge to the industry's growth trajectory.

- The market is driven by the unique properties of engineering plastics, such as creep resistance and high tensile strength, which are essential for various industries. However, the high cost of production is a significant challenge, as specialized techniques, including material characterization and controlled environments, are required to maintain these superior properties. For instance, high-performance polymers like polypropylene (PP) and polyetheretherketone (PEEK) have excellent chemical resistance and dimensional accuracy, making them ideal for aerospace, automotive, and medical applications. Yet, their production processes are complex and energy-intensive, leading to higher material costs. The cost of PP can range from USD1 to USD5 per kilogram, while PEEK can exceed USD200 per kilogram.

- This high cost poses a barrier to entry for smaller companies and startups, limiting market adoption. Moreover, the shift towards smart manufacturing and the circular economy is pushing the industry to explore more sustainable and cost-effective production methods, such as recycling and reusing waste materials, to reduce the environmental impact. Overall, the market's future growth depends on the balance between the demand for high-performance plastics and the ability to produce them cost-effectively.

Exclusive Customer Landscape

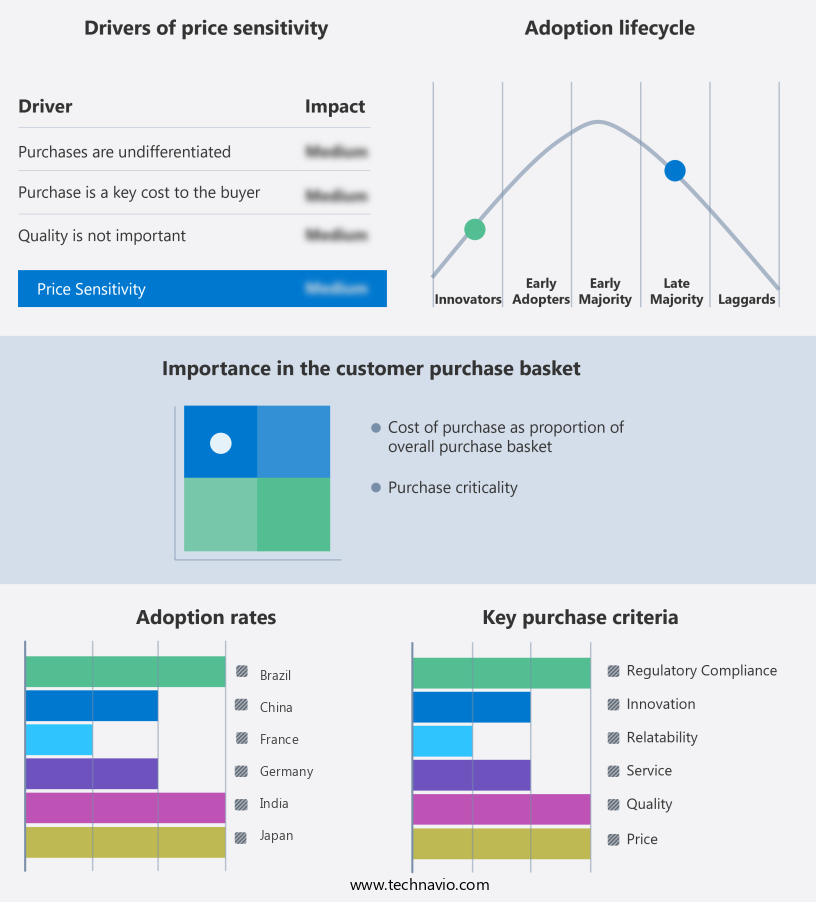

The high temperature 3d printing plastics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the high temperature 3d printing plastics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, high temperature 3d printing plastics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - This company specializes in 3D printing with high-temperature plastics, such as VisiJet® M2S-HT250. With a heat deflection temperature of up to 250 degrees Celsius, these materials enable the production of durable, heat-resistant parts. By utilizing advanced 3D printing technology, we create innovative solutions for various industries, ensuring superior product performance and functionality. Our commitment to research and development drives us to continually expand our material offerings and push the boundaries of additive manufacturing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- Arkema

- Avient Corp.

- BASF SE

- Covestro AG

- DSM-Firmenich AG

- Eastman Chemical Co.

- Ensinger

- ENVISIONTEC US LLC

- Evonik Industries AG

- Huntsman Corp.

- MATERIALISE NV

- Saudi Basic Industries Corp.

- Solvay SA

- Stratasys Ltd.

- Sumitomo Chemical Co. Ltd.

- Toray Industries Inc.

- Victrex Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in High Temperature 3D Printing Plastics Market

- In February 2023, BASF, a leading chemical producer, introduced Ultrafuse 3F, a new high-performance polyamide material for High Temperature Additive Manufacturing (HTAM) applications. This innovative material offers improved mechanical properties and is suitable for various industries, including aerospace and automotive (BASF press release, 2023).

- In May 2024, Stratasys, a leading 3D printing solutions provider, announced a strategic partnership with Siemens Energy to develop and commercialize high-temperature 3D printing solutions for the energy sector. This collaboration aims to accelerate the adoption of 3D printing in the production of components for gas turbines and power generation systems (Stratasys press release, 2024).

- In August 2024, GE Additive, a subsidiary of General Electric, raised USD200 million in a funding round to expand its additive manufacturing business, including the development and commercialization of high-temperature 3D printing technologies (GE Additive press release, 2024).

- In December 2025, Arkema, a global specialty materials company, launched PEKK-based high-performance materials for High Temperature Fused Deposition Modeling (HT FDM) applications. These materials offer excellent mechanical properties and high thermal stability, making them suitable for various industries, such as aerospace and automotive (Arkema press release, 2025).

Research Analyst Overview

- In the market, data acquisition plays a crucial role in optimizing part design and manufacturing process. Extreme environments, such as high temperatures, pose challenges in maintaining part integrity and heat distortion. Industry collaboration and university partnerships are essential for material testing and advancing technology in this field. High temperature applications, including medical devices like dental implants and aerospace components, require corrosion resistance and flame retardancy. Injection molding and CAD/CAM integration enable mass production with process control and regulatory compliance to ISO and ASTM standards. FEA analysis and thermal stress testing ensure safety standards in automotive parts and engine components.

- Government funding and research institutes contribute to the advancement of high temperature plastics, addressing the needs of industries like exhaust systems and turbine blades. Future trends include the development of new materials with enhanced heat resistance and improved thermal stress management, ensuring quality assurance and technological innovation in this dynamic market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled High Temperature 3D Printing Plastics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

223 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.4% |

|

Market growth 2025-2029 |

USD 790 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

12.7 |

|

Key countries |

US, China, Germany, UK, France, Spain, Japan, South Korea, India, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this High Temperature 3D Printing Plastics Market Research and Growth Report?

- CAGR of the High Temperature 3D Printing Plastics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the high temperature 3d printing plastics market growth of industry companies

We can help! Our analysts can customize this high temperature 3d printing plastics market research report to meet your requirements.

RIA -

RIA -