In-vehicle Computer System Market Size 2026-2030

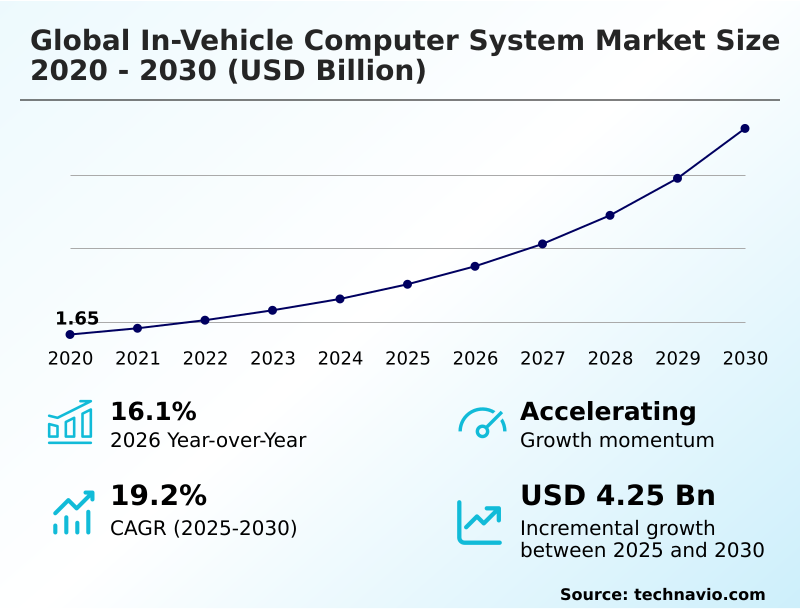

The in-vehicle computer system market size is valued to increase by USD 4.25 billion, at a CAGR of 19.2% from 2025 to 2030. Inexorable rise of advanced driver assistance systems and pursuit of vehicle autonomy will drive the in-vehicle computer system market.

Major Market Trends & Insights

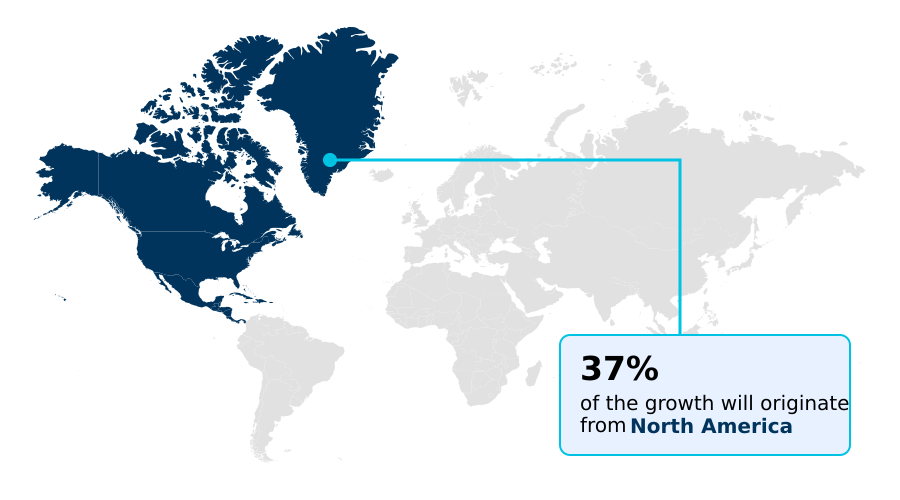

- North America dominated the market and accounted for a 36.8% growth during the forecast period.

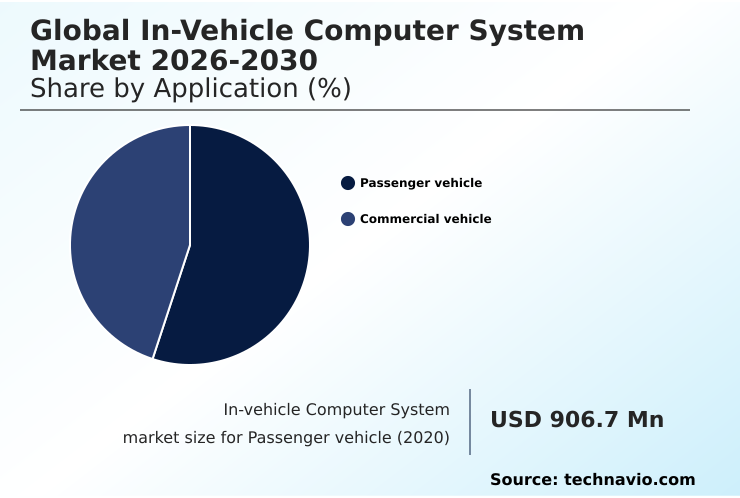

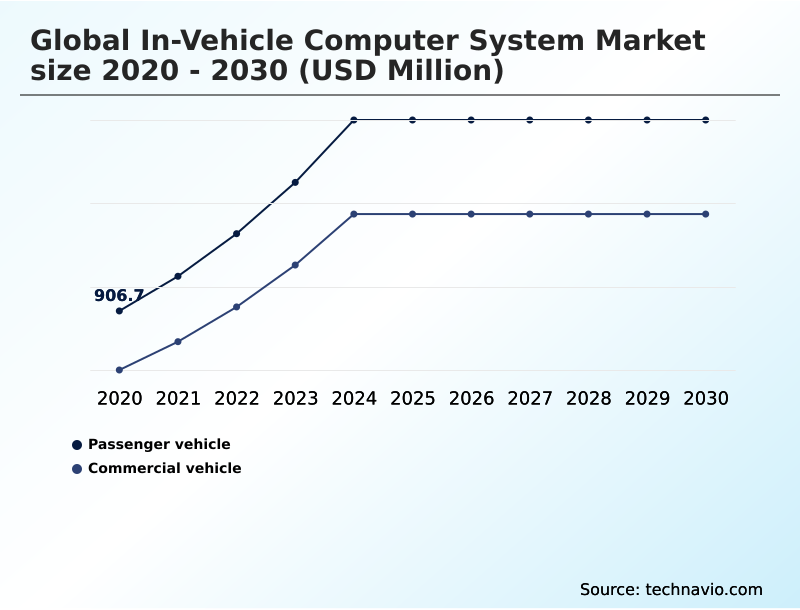

- By Application - Passenger vehicle segment was valued at USD 1.44 billion in 2024

- By Component - Hardware segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.62 billion

- Market Future Opportunities: USD 4.25 billion

- CAGR from 2025 to 2030 : 19.2%

Market Summary

- The in-vehicle computer system market is undergoing a foundational transformation, shifting from being a set of discrete components to the central nervous system of modern automobiles. This evolution is driven by the industry-wide adoption of the software-defined vehicle (SDV) concept, where vehicle functionality and performance are increasingly determined by software.

- This paradigm necessitates powerful, centralized high-performance computing (HPC) platforms capable of managing everything from safety-critical advanced driver-assistance systems (ADAS) to immersive in-cabin experiences. For instance, fleet management operators now leverage these systems to process telematics data in real time, optimizing route efficiency and performing predictive maintenance, thereby reducing operational downtime.

- The underlying hardware, often a complex system-on-a-chip (SoC), must support a mixed-criticality environment, running multiple operating systems simultaneously while ensuring absolute security and functional safety. This requirement for consolidated, powerful, and secure computing is reshaping the entire automotive supply chain, creating new dependencies on semiconductor and software expertise.

- The market's trajectory is defined by this pursuit of greater vehicle intelligence, connectivity, and autonomy, making the in-vehicle computer the core enabler of future automotive innovation.

What will be the Size of the In-vehicle Computer System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the In-vehicle Computer System Market Segmented?

The in-vehicle computer system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Passenger vehicle

- Commercial vehicle

- Component

- Hardware

- Software

- Os

- QNX

- Android automotive OS

- Linux-based systems

- Custom OS

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Application Insights

The passenger vehicle segment is estimated to witness significant growth during the forecast period.

The passenger vehicle segment is driven by the integration of sophisticated electronic systems. The shift towards heterogeneous computing architectures enables platforms to handle diverse workloads, from powertrain management to advanced infotainment.

Automakers are leveraging over-the-air (OTA) updates to deploy new features and security patches, a process reliant on robust embedded computing platforms and a central vehicle control unit. The deployment of vehicle-to-everything (V2X) communication is further increasing data processing demands.

This requires powerful in-vehicle server capabilities and edge AI processing for real-time decision-making, with some automakers reporting a 15% improvement in network-assisted collision avoidance through such systems. This evolution depends on the successful integration of the automotive domain controller.

The Passenger vehicle segment was valued at USD 1.44 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How In-vehicle Computer System Market Demand is Rising in North America Request Free Sample

The geographic landscape is led by North America, which is poised to capture over 36% of incremental growth, driven by high consumer demand for a premium in-cabin experience and a robust technology ecosystem.

Europe follows, with its strong automotive manufacturing base enforcing strict integration of digital cockpit solutions and telematics control unit standards.

In these regions, the transition to modern architectures has resulted in up to a 20% reduction in controller area network (CAN bus) related wiring.

Meanwhile, APAC is an emerging hub where the demand for affordable connected mobility is fueling the adoption of automotive-grade linux (AGL) and custom in-vehicle HMI systems in rugged in-vehicle computers.

This creates distinct regional requirements for both hardware, including V2X chipset integration, and the supporting infotainment head unit.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the automotive sector increasingly revolve around the centralized vs distributed vehicle architecture debate. The benefits of a software defined vehicle architecture are compelling, particularly for electric vehicles, where a zonal architecture for electric vehicles can optimize power distribution and thermal management.

- The choice of an automotive ethernet for data backbone is becoming standard for the bandwidth required by a high performance computer for autonomous driving. A critical software element is the role of hypervisor in vehicle computing, which enables mixed-criticality workload consolidation in vehicles by isolating different operating systems.

- This leads to the open source vs proprietary in-vehicle OS discussion, comparing options like QNX vs linux for automotive applications. An ISO 26262 compliant computing platform is non-negotiable for safety systems, dictating robust design from the silicon level, including thermal management for automotive SoC, up to the application layer.

- The impact of SDV on automotive hardware is profound, pushing for upgradable hardware for future ADAS features. Real-time processing for sensor fusion and low latency networking for vehicle control are essential performance metrics.

- For specific applications, a rugged computer for commercial vehicle telematics or an in-vehicle computer for fleet management must provide reliable connectivity, often through V2X communication module integration, and support for edge AI inference in automotive systems. Effective cybersecurity for connected car systems is paramount, protecting the entire architecture from threats and ensuring data integrity.

What are the key market drivers leading to the rise in the adoption of In-vehicle Computer System Industry?

- The inexorable rise of advanced driver assistance systems and the industry's pursuit of vehicle autonomy are the primary drivers propelling market growth.

- The primary market driver is the escalating computational demand from advanced driver-assistance systems (ADAS) and the pursuit of full autonomy.

- These systems require the real-time processing of immense data volumes for sensor fusion, a task managed by a dedicated ADAS domain controller.

- This necessitates powerful hardware, including a specialized graphics processing unit (GPU) and neural processing unit (NPU) integrated into an autonomous driving computer.

- The in-vehicle AI accelerator is critical for executing complex algorithms with low latency, with some systems achieving a 50% faster response time in critical scenarios.

- This push for greater intelligence and fail-operational capabilities fuels investment in advanced automotive sensor integration and robust vehicle data processing platforms, directly driving the need for more capable in-vehicle computers.

What are the market trends shaping the In-vehicle Computer System Industry?

- The market is undergoing a definitive architectural shift away from legacy distributed models. This transition favors the adoption of centralized and zonal computing paradigms to handle increasing system complexity.

- A dominant trend is the architectural shift toward a software-defined vehicle (SDV), which relies on a centralized high-performance computing (HPC) platform. This move to a zonal architecture, away from distributed ECUs, is enabled by a high-speed automotive ethernet backbone connecting a central compute cluster to zonal gateway controllers.

- This consolidation streamlines the automotive software stack and simplifies in-vehicle networking, with some engineering teams reporting up to a 40% reduction in software integration conflicts. A sophisticated automotive hypervisor or hypervisor software layer is essential to manage and isolate different functions.

- The successful implementation of this new paradigm is critical for delivering advanced features and maintaining a competitive edge in the evolving automotive landscape.

What challenges does the In-vehicle Computer System Industry face during its growth?

- Intensifying system complexity and significant software integration hurdles present a key challenge to industry growth.

- A formidable challenge is managing the escalating complexity of a mixed-criticality environment on a single system-on-a-chip (SoC). Ensuring functional safety (ISO 26262) in a consolidated architecture requires a robust real-time operating system (RTOS) and secure automotive middleware. Effective automotive thermal management becomes critical, as concentrating processing power in one location can lead to a 30% increase in localized heat generation.

- Furthermore, the entire system, including all automotive processing hardware, must be protected by stringent cybersecurity protocols to prevent threats. Integrating these complex hardware and software components from multiple vendors into rugged embedded systems poses significant validation hurdles for automotive cybersecurity solutions, potentially delaying vehicle development timelines by several months.

Exclusive Technavio Analysis on Customer Landscape

The in-vehicle computer system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the in-vehicle computer system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of In-vehicle Computer System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, in-vehicle computer system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AAEON Technology Inc. - Delivers rugged, fanless embedded computing platforms engineered for reliability in transportation and industrial mobile environments, supporting diverse vehicle applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AAEON Technology Inc.

- Acrosser Technology Co. Ltd.

- ADLINK Technology Inc.

- American Portwell Technology

- Avalue Technology Inc.

- Axiomtek Co. Ltd.

- IBASE Technology Inc.

- IEI Integration Corp.

- JLT Mobile Computers AB

- Kontron AG

- Neousys Technology Inc.

- OnLogic Inc.

- Premio Inc.

- roda computer GmbH

- SD OMEGA Hong Kong Co. Ltd.

- SINTRONES Technology Corp.

- WINSONIC ELECTRONICS CO. LTD.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in In-vehicle computer system market

- In September 2024, a leading semiconductor firm announced a partnership with a major European automaker to supply its next-generation compute platform for their 2028 vehicle lineup, focusing on centralizing autonomous driving and infotainment functions.

- In November 2024, the US Department of Transportation issued new proposed cybersecurity guidelines for software-defined vehicles, mandating stringent real-time threat detection capabilities within central compute units.

- In January 2025, a major mobile technology company unveiled its next-generation automotive SoC at a consumer electronics show, demonstrating the consolidation of digital cockpit, ADAS, and cloud-native services on a single chip, reducing hardware complexity by up to 30%.

- In April 2025, a Japanese electronics corporation launched its new family of automotive SoCs, featuring enhanced AI acceleration and low-power performance for next-generation zonal E/E architectures and entry-to-mid-level ADAS applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled In-vehicle Computer System Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 285 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 19.2% |

| Market growth 2026-2030 | USD 4249.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The in-vehicle computer system market is pivoting toward a centralized, software-centric future, where the vehicle's value is defined by its computational power and upgradability. The adoption of the software-defined vehicle (SDV) model is compelling automakers to rethink their core architecture, moving toward high-performance computing (HPC) platforms.

- These platforms are built around a complex system-on-a-chip (SoC) featuring heterogeneous computing capabilities, including a CPU, graphics processing unit (GPU), and a dedicated neural processing unit (NPU). This transition enables critical functionalities such as real-time sensor fusion for advanced driver-assistance systems (ADAS) and allows for continuous over-the-air (OTA) updates.

- Boardroom decisions now center on managing this complexity, particularly in a mixed-criticality environment where a hypervisor software layer must isolate safety functions. Adherence to cybersecurity protocols and functional safety (ISO 26262) standards is paramount, demanding fail-operational capabilities.

- The shift to a zonal architecture, connected by an automotive ethernet backbone, is a key enabler, with early adopters reporting a 15% reduction in integration testing time.

- This evolution impacts everything from the telematics control unit (TCU) and controller area network (CAN bus) to the digital cockpit solutions and overall in-cabin experience, also driving demand for automotive-grade linux (AGL) and edge AI processing for vehicle-to-everything (V2X) communication.

What are the Key Data Covered in this In-vehicle Computer System Market Research and Growth Report?

-

What is the expected growth of the In-vehicle Computer System Market between 2026 and 2030?

-

USD 4.25 billion, at a CAGR of 19.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger vehicle, and Commercial vehicle), Component (Hardware, and Software), OS (QNX, Android automotive OS, Linux-based systems, and Custom OS) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Inexorable rise of advanced driver assistance systems and pursuit of vehicle autonomy, Intensifying system complexity and software integration hurdles

-

-

Who are the major players in the In-vehicle Computer System Market?

-

AAEON Technology Inc., Acrosser Technology Co. Ltd., ADLINK Technology Inc., American Portwell Technology, Avalue Technology Inc., Axiomtek Co. Ltd., IBASE Technology Inc., IEI Integration Corp., JLT Mobile Computers AB, Kontron AG, Neousys Technology Inc., OnLogic Inc., Premio Inc., roda computer GmbH, SD OMEGA Hong Kong Co. Ltd., SINTRONES Technology Corp., WINSONIC ELECTRONICS CO. LTD. and ZF Friedrichshafen AG

-

Market Research Insights

- The transition to a software-defined model is reshaping automotive value chains, with platforms now achieving over-the-air update success rates exceeding 98%. This paradigm is built upon the automotive domain controller and central compute cluster, which consolidate functions previously managed by dozens of discrete ECUs.

- Adopting an automotive ethernet backbone has been shown to reduce in-vehicle networking latency by up to 40% compared to legacy bus systems. This efficiency allows for the deployment of sophisticated in-vehicle AI accelerator technology and connected car platform services, directly impacting the in-cabin experience and enabling new revenue models based on feature subscriptions.

- The integration of a capable infotainment head unit is now a key differentiator.

We can help! Our analysts can customize this in-vehicle computer system market research report to meet your requirements.