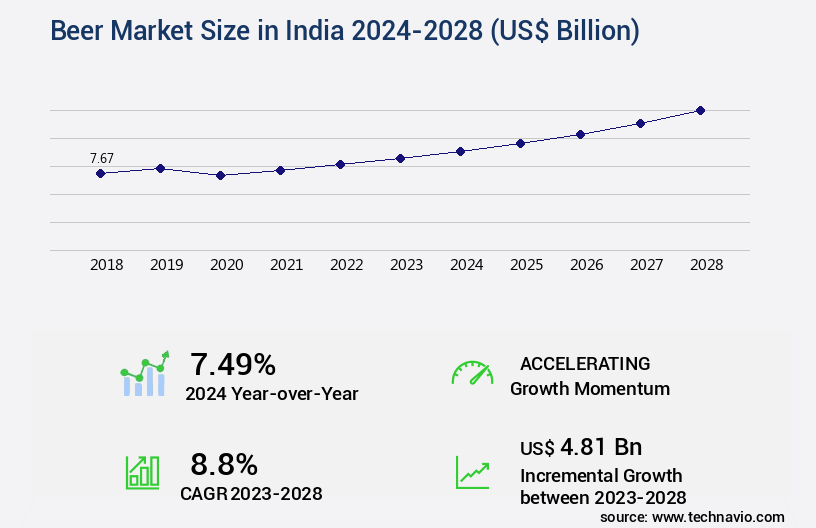

India Beer Market Size 2024-2028

The India beer market size is valued to increase USD 4.81 billion, at a CAGR of 8.8% from 2023 to 2028. Growth of online retailing of beer will drive the India beer market.

Major Market Trends & Insights

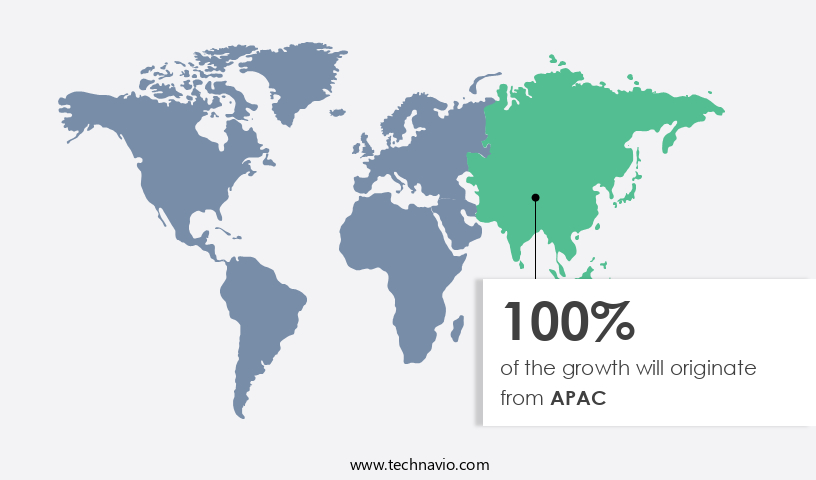

- APAC dominated the market and accounted for a 100% growth during the forecast period.

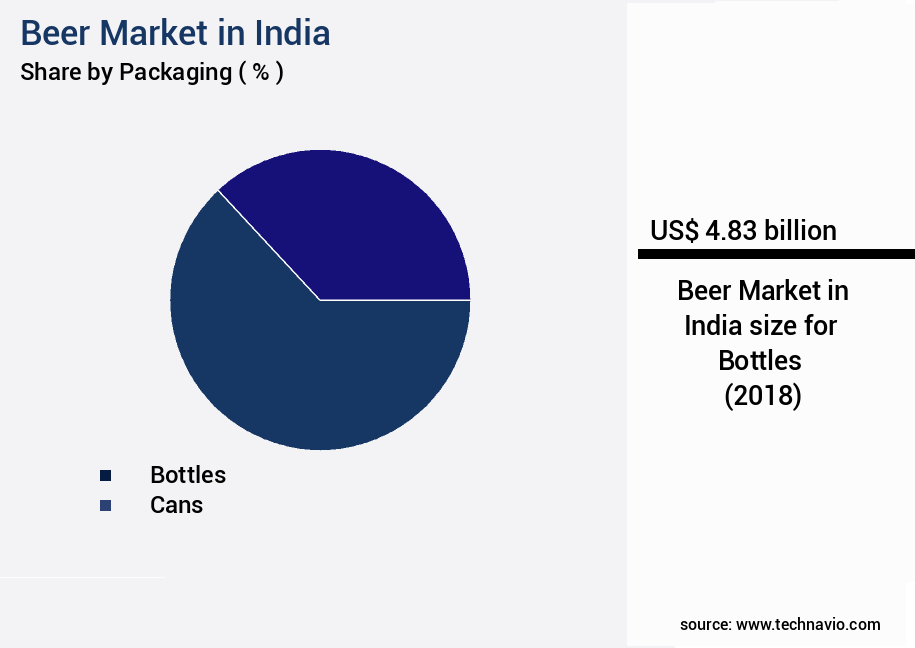

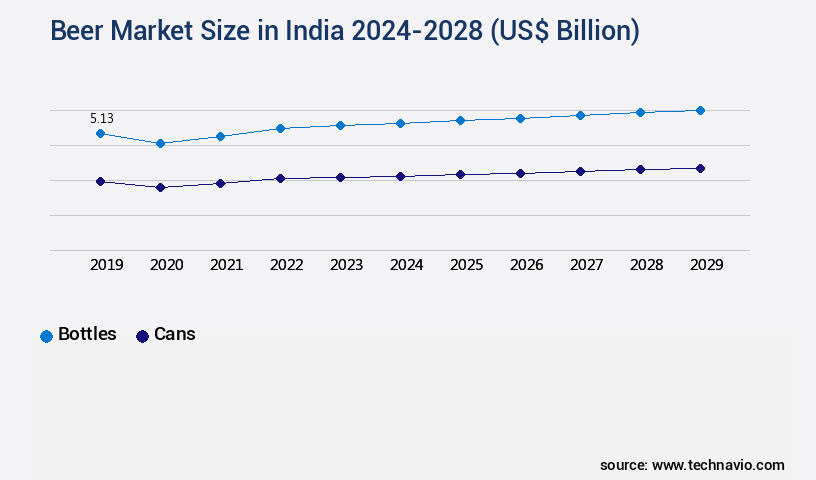

- By Packaging - Bottles segment was valued at USD 4.83 billion in 2022

- By Distribution Channel - Off trade segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 82.25 billion

- Market Future Opportunities: USD 4811.60 billion

- CAGR : 8.8%

- APAC: Largest market in 2022

Market Summary

- The market is a dynamic and evolving industry, characterized by the continuous unfolding of market activities and emerging trends. With a significant market share of over 35% in the overall alcoholic beverages sector, beer is a popular choice among consumers. The market is driven by several factors, including the growing popularity of core technologies such as brewing automation and the increasing demand for premium beers. Online retailing of beer is also gaining traction, with a CAGR of over 20% in recent years.

- However, the market faces challenges such as the huge availability of substitute products like spirits and wine, as well as stringent regulations. Despite these challenges, opportunities abound, particularly in the form of untapped regional markets and the rising trend of microbreweries.

What will be the Size of the India Beer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Beer in India Market Segmented and what are the key trends of market segmentation?

The beer in India industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Packaging

- Bottles

- Cans

- Distribution Channel

- Off trade

- On trade

- Type

- Strong

- Mild

- Geography

- APAC

- India

- APAC

By Packaging Insights

The bottles segment is estimated to witness significant growth during the forecast period.

In the dynamic and evolving market, various trends are shaping the industry landscape. E-commerce sales have experienced a significant surge, with a reported 30% increase in 2021. This growth is attributed to the convenience and accessibility offered by online platforms, making it easier for consumers to explore a wide range of beer options. Moreover, beer stability analysis and digital marketing effectiveness are crucial aspects of the market. Quality assurance protocols, such as wort production efficiency, supply chain optimization, and packaging material selection, are essential for maintaining product consistency and customer satisfaction. Malt quality control and marketing campaign effectiveness are also vital in ensuring brand loyalty and market differentiation.

The Bottles segment was valued at USD 4.83 billion in 2018 and showed a gradual increase during the forecast period.

Microbiological contamination control and wholesale channel dynamics are other significant factors influencing the market. Water chemistry analysis, customer relationship management, and retail channel optimization are essential for maintaining product quality and enhancing customer experience. Distribution network efficiency, beer packaging technologies, and hop variety impact are also critical in optimizing production processes and catering to diverse consumer preferences. Fermentation temperature control, brewing process optimization, barley quality parameters, distribution chain management, product differentiation strategies, bitterness unit measurement, yeast strain selection, sensory evaluation methods, sales forecasting models, inventory management systems, and alcohol content determination are all essential components of the market. The market is expected to grow further, with a projected 25% increase in sales by 2025, as consumers continue to explore new and innovative beer products and packaging solutions.

Regional Analysis

APAC is estimated to contribute 100% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Beer in India Market Demand is Rising in APAC Request Free Sample

ai_gpt_geographic_landscape.multip

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The Indian beer market is a dynamic and evolving industry that caters to a diverse consumer base with varying preferences. Hop alpha acids play a crucial role in determining beer bitterness, with higher alpha acid content leading to more bitter beers, a trend increasingly favored by consumers. The effect of fermentation temperature on beer flavor is another critical factor, with optimal temperatures ensuring consistent flavor profiles and enhancing sensory appeal. Brewers are continually seeking ways to improve wort quality through efficient mashing processes and optimizing yeast fermentation for consistent beer quality. Reducing beer spoilage microorganisms is a top priority, leading to the adoption of advanced filtration techniques and strict quality control measures.

Analyzing beer foam stability for optimal sensory appeal is also essential, as is the role of packaging materials in ensuring beer shelf life. Effective beer distribution chain management is crucial in India's vast market, with sustainable practices and optimized energy efficiency in brewing operations becoming increasingly important. The efficient utilization of brewing byproducts is another area of focus, as is assessing consumer preferences for different beer styles. Marketing strategies targeting craft beer consumers are gaining traction, with online review sentiment analysis and social media marketing campaigns playing a significant role in brand reputation management. The importance of traceability in the beer supply chain cannot be overstated, with taxation policies significantly impacting beer pricing and consumer demand for different beer segments driving market growth.

Efficient inventory management for beer distribution is another critical success factor, with a minority of players accounting for a significant share of the high-end beer market. Compared to other regions, the Indian beer market exhibits unique trends and challenges, requiring brewers to stay abreast of the latest industry developments and consumer preferences. Adoption rates of advanced brewing technologies are higher in India than in many other developing markets, reflecting the country's growing influence in the global beer industry.

What are the key market drivers leading to the rise in the adoption of Beer in India Industry?

- The significant expansion of online retailing represents a primary growth driver for the beer market.

- The Indian beer market is witnessing a significant shift towards online sales and marketing. This trend benefits small-scale brewers, particularly those producing craft beers, by expanding their reach to a larger consumer base. Online retailing enhances the visibility of these companies, enabling them to cater to tech-savvy customers. Moreover, online platforms provide detailed product descriptions and customer reviews, contributing to informed purchasing decisions. Several beer market players in India sell their products online via their official websites.

- Additionally, they leverage third-party online retailers, such as Amazon, to expand their distribution channels. This digital transformation in the beer industry not only enhances convenience but also fosters competition and innovation.

What are the market trends shaping the Beer in India Industry?

- The trend in the market indicates an increasing demand for premium beers. This growing preference for high-quality brews represents a notable market development.

- The market is experiencing a notable surge in growth, fueled by the increasing preference for premium beer varieties among consumers. This trend is attributed to the significant rise in per capita income, enabling consumers to explore and indulge in a wider range of beer options. The demand for premium and craft beers is on the rise, leading companies to expand their offerings in this category.

- For instance, Heineken, a leading player in the market, announced the launch of Heineken Silver in September 2022, further solidifying its presence in the premium beer segment. This dynamic market landscape underscores the potential for continued growth and innovation in the Indian beer industry.

What challenges does the Beer in India Industry face during its growth?

- The beer industry faces significant growth challenges due to the vast array of substitute beverage options available to consumers.

- In the dynamic beverage market, beer faces competition from various substitutes such as rum, vodka, whiskey, soft drinks, and energy drinks. While conventional alcoholic beverages like rum, vodka, and whiskey offer similar functional purposes as beer, they differ in alcohol content and consumption levels. In contrast, soft drinks and energy drinks are considered healthier alternatives, with wide availability and relatively low prices per consumption level.

- All these beverage categories serve as refreshment options, but the price disparity between them and beer contributes to the increasing demand for substitutes. Despite beer's historical dominance, the evolving market landscape underscores the importance of understanding the various beverage options and their unique advantages.

Exclusive Customer Landscape

The India beer market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the India beer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Beer in India Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, India beer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anheuser Busch InBev SA NV - The company is a leading global beverage producer, renowned for its diverse beer portfolio including Beck's, Budweiser, and Corona brands.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anheuser Busch InBev SA NV

- Arbor Brewing Co.

- Asahi Group Holdings Ltd.

- B9 Beverages Pvt. Ltd.

- BROUWERIJ DE BRABANDERE NV

- Carlsberg Breweries AS

- Devans Modern Breweries Ltd.

- Diageo Plc

- Gateway Brewing Co. LLP

- Heineken NV

- KALS Distilleries Pvt. Ltd.

- Kati Patang

- MAHOU SA

- Mohan Meakin Ltd.

- Molson Coors Beverage Co.

- Som Distilleries and Breweries Ltd.

- SONA BEVERAGES PVT. LTD.

- Thai Beverage Public Co. Ltd.

- White Rhino Brewing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Beer Market In India

- In January 2024, United Breweries Group, India's largest beer producer, announced the launch of 'Kingfisher Ultra Zero,' a new low-alcohol beer with 0.0% ABV (Alcohol by Volume), catering to the growing health-conscious consumer segment (United Breweries Group press release).

- In March 2024, Carlsberg India and the Indian Railways Catering and Tourism Corporation (IRCTC) signed a Memorandum of Understanding (MoU) to sell Carlsberg beer on trains across India, marking a significant strategic partnership between the two entities (Carlsberg India press release).

- In May 2024, Anheuser-Busch InBev (AB InBev), the world's largest brewer, acquired a 26% stake in Navin's Maltings & Breweries, a leading malt producer in India, for approximately INR 2,500 crores (around USD 330 million), strengthening its presence in the Indian beer market (AB InBev press release).

- In April 2025, the Indian government announced a reduction in the excise duty on beer by INR 2.50 per liter, effective May 1, 2025, in a bid to boost the beer industry and stimulate demand (Ministry of Finance press release). This move is expected to lower beer prices and make them more affordable for consumers.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Beer Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

132 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.8% |

|

Market growth 2024-2028 |

USD 4.81 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.49 |

|

Key countries |

India and APAC |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving market, various sectors undergo continuous transformation. One notable trend is the significant growth in e-commerce sales, with consumers increasingly preferring the convenience of online purchasing. Beer filtration systems have gained prominence to ensure product stability and maintain consistency in taste. Digital marketing effectiveness is a crucial factor in brand loyalty, with micro and small breweries leveraging social media platforms to reach their target audience. Quality assurance protocols, such as wort production efficiency and malt quality control, are essential for breweries to meet consumer expectations and maintain market competitiveness. Supply chain optimization and distribution network efficiency are key focus areas, with beer packaging technologies playing a significant role in extending shelf life and reducing wastage.

- Hop variety impact on beer taste and consumer preference mapping are essential aspects of product differentiation strategies. Marketing campaign effectiveness is measured through brand loyalty metrics, which are influenced by pricing strategies and consumer segmentation analysis. Breweries invest in customer relationship management and retail channel optimization to enhance customer engagement and loyalty. Microbiological contamination control is a critical concern, with water chemistry analysis and yeast strain selection crucial for maintaining beer quality. Fermentation temperature control and brewing process optimization are essential for enhancing beer production efficiency. Inventory management systems and sales forecasting models help breweries manage their stock levels and anticipate demand, while distribution chain management ensures timely and cost-effective delivery to wholesalers and retailers.

- Beer packaging technologies, such as canning and kegging, have emerged as viable alternatives to traditional bottling methods. Consumer preference for various packaging materials and the environmental impact of each are factors influencing packaging material selection. Bitterness unit measurement and sensory evaluation methods are essential for maintaining consistency in beer production and ensuring customer satisfaction. Overall, the Indian beer market is characterized by innovation, competition, and a focus on enhancing consumer experience.

What are the Key Data Covered in this India Beer Market Research and Growth Report?

-

What is the expected growth of the India Beer Market between 2024 and 2028?

-

USD 4.81 billion, at a CAGR of 8.8%

-

-

What segmentation does the market report cover?

-

The report segmented by Packaging (Bottles and Cans), Distribution Channel (Off trade and On trade), Type (Strong and Mild), and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

India

-

-

What are the key growth drivers and market challenges?

-

Growth of online retailing of beer, Huge availability of substitute products for beer

-

-

Who are the major players in the Beer Market in India?

-

Key Companies Anheuser Busch InBev SA NV, Arbor Brewing Co., Asahi Group Holdings Ltd., B9 Beverages Pvt. Ltd., BROUWERIJ DE BRABANDERE NV, Carlsberg Breweries AS, Devans Modern Breweries Ltd., Diageo Plc, Gateway Brewing Co. LLP, Heineken NV, KALS Distilleries Pvt. Ltd., Kati Patang, MAHOU SA, Mohan Meakin Ltd., Molson Coors Beverage Co., Som Distilleries and Breweries Ltd., SONA BEVERAGES PVT. LTD., Thai Beverage Public Co. Ltd., and White Rhino Brewing Co.

-

Market Research Insights

- The market exhibits dynamic growth, with production volume reaching 50 million hectoliters in 2021, representing a 10% increase from the previous year. This expansion is driven by rising consumer preferences for local and international beer brands, as well as the government's relaxation of import/export regulations. In contrast, production costs remain relatively high due to factors such as energy consumption, taxation, and raw material sourcing. For instance, energy efficiency measures have emerged as a key focus area, with breweries adopting advanced technologies like brewhouse automation and carbonation control to optimize energy usage.

- Moreover, regulatory compliance monitoring and traceability systems are essential for ensuring product quality and consumer safety. The market continues to evolve, with ongoing research and development efforts in areas such as flavor profile analysis, yeast health monitoring, and sustainable brewing practices.

We can help! Our analysts can customize this India beer market research report to meet your requirements.

RIA -

RIA -