Industrial Air Compressor Market Size 2024-2028

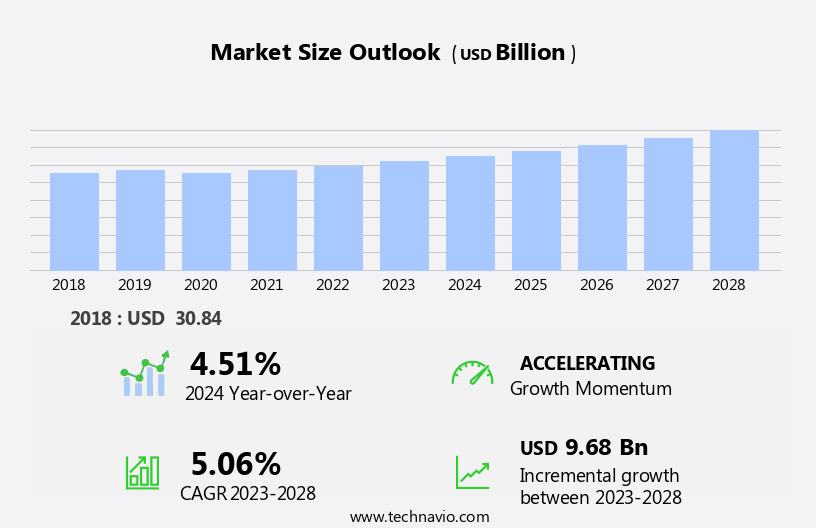

The industrial air compressor market size is forecast to increase by USD 9.68 billion at a CAGR of 5.06% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing adoption of these systems in various industries. The demand for energy-efficient solutions is driving the market, as industries seek to reduce their carbon footprint and lower operating costs. Additionally, fluctuating prices of raw materials for air compressors are influencing the market dynamics.

- Energy-efficient industrial air compressors are becoming increasingly popular as companies strive to minimize their energy consumption and reduce production costs. The market is expected to continue its growth trajectory in the coming years, as the need for reliable and efficient compressed air solutions, including portable air compressors, persists across industries.

What will be the Size of the Industrial Air Compressor Market During the Forecast Period?

- The market in the United States is experiencing significant growth, driven by the increasing industrialization in various sectors such as the oil & gas industry, food & beverage, and pharmaceuticals. Asia Pacific countries are also key contributors to market expansion due to their rapid industrial development.

- Sustainability and environmental concerns are increasingly influencing market dynamics, with strict regulations promoting the adoption of sustainable technology and energy-efficient products. High-quality air is essential in industries like oil and gas and steel, leading to a focus on advanced product innovation, including oil-filled and oil-free air compressors with varying operating modes and power ranges.

- The market is moderately concentrated, with key players investing in research and development to meet evolving customer needs and expectations. Lubrication systems are also a critical consideration in the selection and operation of industrial air compressors. Prices of crude oil and economic conditions can impact demand, but overall, the market is expected to continue its robust growth trajectory.

How is this Industrial Air Compressor Industry segmented and which is the largest segment?

The industrial air compressor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Chemicals and petrochemicals

- Food and beverages

- Pharmaceuticals

- Construction

- Others

- Type

- Stationary

- Portable

- Geography

- APAC

- China

- Japan

- North America

- US

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- APAC

By End-user Insights

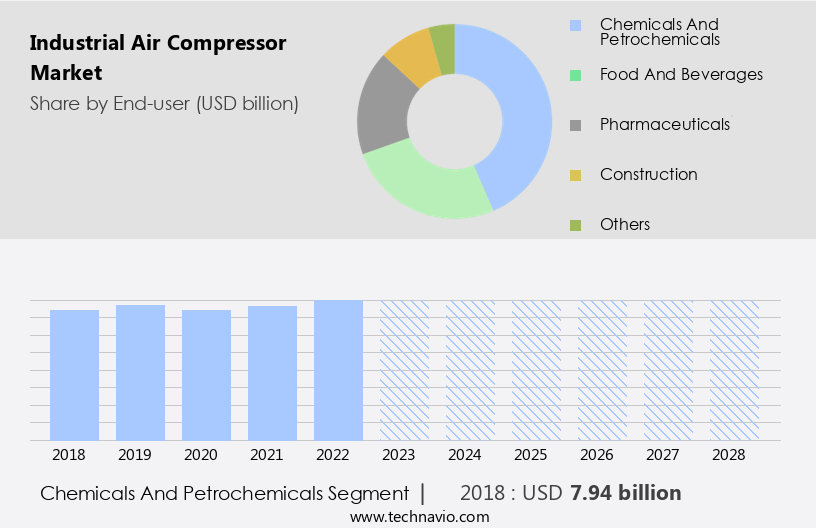

- The chemicals and petrochemicals segment is estimated to witness significant growth during the forecast period.

Industrial air compressors are essential equipment in various industries, including food and beverage and pharmaceuticals, for powering pneumatic tools and processes. Stationary industrial air compressors, in particular, are preferred due to their larger capacities and ability to store a greater volume of compressed air. These compressors, which are designed for fixed installation, are typically larger in size and require a continuous power supply from the AC main. They are commonly used in applications that demand high cubic meters of compressed air and uninterrupted supply. The steel industry and crude oil production are significant consumers of stationary industrial air compressors due to their energy-intensive processes. Product innovation and advancements in technology continue to drive the market, with manufacturers focusing on energy efficiency and reducing maintenance costs.

Get a glance at the Industrial Air Compressor Industry report of share of various segments Request Free Sample

The Chemicals and petrochemicals segment was valued at USD 7.94 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

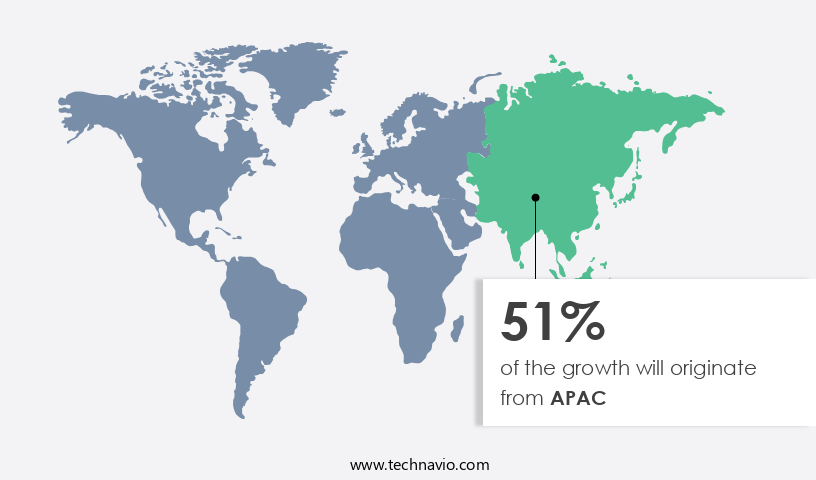

- APAC is estimated to contribute 51% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in the Asia Pacific (APAC) region is driven by the significant growth of key end-users, including the automobile, food and beverage, construction, and chemical industries. In the automotive sector, industrial air compressors are utilized for various applications such as tire inflation, air-operated robots, product finishing, plasma cutting, welding, and painting. APAC's automotive industry is experiencing a strong expansion, with rising production and sales, leading to increased demand for industrial air compressors. Additionally, the oil and gas industry's demand for industrial air compressors is anticipated to increase due to the high energy demand in developing countries like China and India. The APAC market is poised for robust growth during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Industrial Air Compressor Industry?

Increasing adoption of industrial air compressors in various industries is the key driver of the market.

- The market in the US has experienced substantial growth in various sectors, including oil and gas, food and beverage, pharmaceuticals, steel, and semiconductors. The adoption of industrial air compressors is driven by their ability to enhance productivity and efficiency in industrial processes. These compressors play a vital role in compressing gases and air, powering pneumatic tools and machinery, and supplying energy for various applications. For instance, in the oil and gas industry, industrial air compressors are used for drilling operations and natural gas processing. In the food and beverage industry, they ensure the supply of high-quality, hygienic air for food processing, packaging, and storage.

- The pharmaceuticals industry relies on industrial air compressors for their role in the production of medications and maintaining clean environments. In the steel industry, they are used for various applications, such as powering pneumatic tools and machinery, and supplying energy for heating processes. The increasing focus on sustainability and environmental concerns has led to the development of sustainable technology and energy-efficient products. Oil-free air compressors, rotary compressors, centrifugal compressors, and reciprocating compressors are some of the popular compressor types used in industrial applications. The market for industrial air compressors is also witnessing the adoption of innovative technologies such as Industry 4.0,

- IoT, cloud technology, and big data analytics, which enhance energy efficiency and reduce maintenance costs. The market dynamics of industrial air compressors are influenced by factors such as crude oil prices, operating mode, power range, and lubrication requirements. The use of hybrid fuel and sustainable technology in industrial air compressors is gaining popularity due to the increasing focus on reducing energy costs and minimizing the carbon footprint. Overall, the market in the US is expected to continue its growth trajectory due to the increasing demand for high-quality air and the need for efficient and sustainable industrial processes.

What are the market trends shaping the Industrial Air Compressor Industry?

Increasing need for energy-efficient industrial air compressor systems is the upcoming market trend.

- The market is witnessing significant growth due to the increasing focus on sustainability and energy efficiency in various industries, particularly in the oil & gas sector. With environmental concerns at the forefront, there is a rising need for industrial equipment, including air compressors, to conform to regional regulations on carbon emissions. This trend is most prominent in Europe and North America, where government authorities are taking initiatives to ensure industrial compliance. Energy efficiency is another driving factor in the adoption of new air compressors. Industrial end-users are seeking air compressors with efficient and reliable controls to lower electricity consumption and reduce overall energy usage.

- Two types of air compressors that are gaining popularity for their energy efficiency are oil-free air compressors and sustainable technology-driven compressors. The food & beverage and pharmaceuticals industries are also adopting energy-efficient air compressors to maintain high-quality air for their processes. The steel industry, which is a significant consumer of compressed air, is also transitioning to energy-efficient compressors to reduce operating costs and improve productivity. Product innovation is another key factor driving the market growth. Manufacturers are developing energy-efficient products, such as rotary/screw compressors, reciprocating air compressors, rotary compressors, centrifugal compressors, and stationary compressors, to cater to the evolving needs of various industries.

- The semiconductor industry is also embracing energy-efficient air compressors to power their pneumatic equipment. The use of hydrogen as a fuel source and the integration of Industry 4.0 technologies, such as IoT, cloud technology, Big Data analytics, and lubrication systems, are further enhancing the energy efficiency and overall performance of industrial air compressors. In conclusion, the market is expected to continue its growth trajectory, driven by the need for energy efficiency, sustainability, and product innovation. The adoption of energy-efficient technologies, such as oil-free air compressors and sustainable technology-driven compressors, is a key trend that is gaining momentum in various industries.

What challenges does the Industrial Air Compressor Industry face during its growth?

Fluctuating prices of raw materials is a key challenge affecting the industry growth.

- The market is significantly influenced by sustainability concerns and the need for high-quality air in various industries, including oil & gas, food & beverage, pharmaceuticals, steel, and semiconductor. Sustainable technology and energy efficiency are key trends driving product innovation in this market. Oil & gas industry's environmental concerns and the increasing demand for oil-free air compressors are significant factors. In the food & beverage and pharmaceuticals industries, the requirement for clean and oil-free air is crucial for product quality and safety. The industrialization process and the growing demand for pneumatic equipment in commercial manufacturing further boost the market's growth.

- Crude oil prices and the availability of raw materials, such as stainless steel, iron, bronze, and copper, impact the market's cost structure. The energy cost and the adoption of energy-efficient products, such as rotary/screw compressors, reciprocating air compressors, rotary compressors, centrifugal compressors, and stationary compressors, are crucial factors. The semiconductor industry's growing demand for hydrogen and the implementation of Industry 4.0, IoT, cloud technology, and big data analytics, are expected to provide new opportunities. Maintenance costs, lubrication, and the adoption of hybrid fuel are essential considerations for market participants. The operating mode and power range of industrial air compressors also influence the market dynamics.

- Overall, the market's growth is subject to various factors, including raw material prices, energy efficiency, and market trends.

Exclusive Customer Landscape

The industrial air compressor market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial air compressor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, industrial air compressor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Atlas Copco AB - The company provides a range of industrial-grade air compressors for businesses. These include the ZR and ZT oil-free screw compressors, the oil-free air centrifugal compressors ZH and ZH Plus, and Atlas Copco's high-pressure PET bottle blowing compressor.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atlas Copco AB

- Baker Hughes Co.

- BOGE KOMPRESSOREN GmbH and Co. KG

- Chart Industries Inc.

- Coaire Inc.

- Danfoss AS

- Doosan Corp.

- Elgi Equipments Ltd

- EMAX Compressor

- Fusheng Precision Co. Ltd.

- Hitachi Ltd.

- Ingersoll Rand Inc.

- KAESER KOMPRESSOREN SE

- Kirloskar Pneumatic Co. Ltd.

- Kobe Steel Ltd.

- MAT Holdings Inc.

- Mitsubishi Heavy Industries Ltd.

- NICE COMPRESSORS CO.

- Siemens AG

- Sulzer Management Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth, driven by the increasing demand for high-quality air in various industries. The importance of compressed air in commercial manufacturing processes cannot be overstated, as it is a vital component in numerous applications, from powering pneumatic tools to maintaining clean environments in the food and beverage industry. Industrialization and the expansion of various sectors, such as oil & gas, pharmaceuticals, and steel, have led to an increased focus on energy efficiency and sustainable technology in the market. Environmental concerns have also come to the forefront, with companies striving to minimize their carbon footprint and adopt more eco-friendly practices.

In the oil & gas industry, the focus on oil-free air compressors has gained significant traction due to their ability to eliminate the risk of oil contamination in applications where purity is crucial. These compressors operate in oil-free modes, using advanced technology to ensure the production of clean, oil-free air. The power range of industrial air compressors varies widely, with rotary and screw compressors being popular choices for medium to large-scale applications. Rotary compressors, which use rotors to compress air, offer high efficiency and low maintenance requirements, making them a popular choice in industries such as semiconductors and hydrogen production.

Reciprocating air compressors, on the other hand, are commonly used in smaller applications due to their affordability and ease of maintenance. These compressors use pistons to compress air and are often used in applications where oil contamination is not a concern. Stationary compressors are another important segment of the market, providing a reliable and consistent source of compressed air for commercial manufacturing processes. These compressors can be powered by various fuels, including electricity, natural gas, and hybrid fuels, allowing for flexibility in energy sourcing. The adoption of sustainable technology and energy efficiency measures is a major trend in the market.

Energy-efficient products, such as oil-filled compressors, are gaining popularity due to their ability to reduce energy costs and minimize environmental impact. The integration of IoT, cloud technology, and big data analytics is also transforming the market, enabling predictive maintenance and optimizing compressor performance. The pharmaceuticals industry, in particular, is driving innovation in the market, with a focus on producing high-purity air for critical applications. The semiconductor industry is also investing heavily in advanced compressor technology to meet the demands of its highly specialized applications. The crude oil prices have an impact on the market, as they influence the cost of producing and transporting various fuels used to power compressors.

However, the market is resilient, with companies continuing to invest in advanced technology and sustainable practices to improve efficiency and reduce costs. In conclusion, the market is a dynamic and evolving landscape, driven by the increasing demand for high-quality air in various industries and the adoption of sustainable technology and energy efficiency measures. The market is expected to continue growing, with innovation and advancements in compressor technology playing a crucial role in shaping its future.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.06% |

|

Market growth 2024-2028 |

USD 9.68 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.51 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Industrial Air Compressor Market Research and Growth Report?

- CAGR of the Industrial Air Compressor industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the industrial air compressor market growth of industry companies

We can help! Our analysts can customize this industrial air compressor market research report to meet your requirements.

RIA -

RIA -