US Industrial Casting Market Size 2024-2028

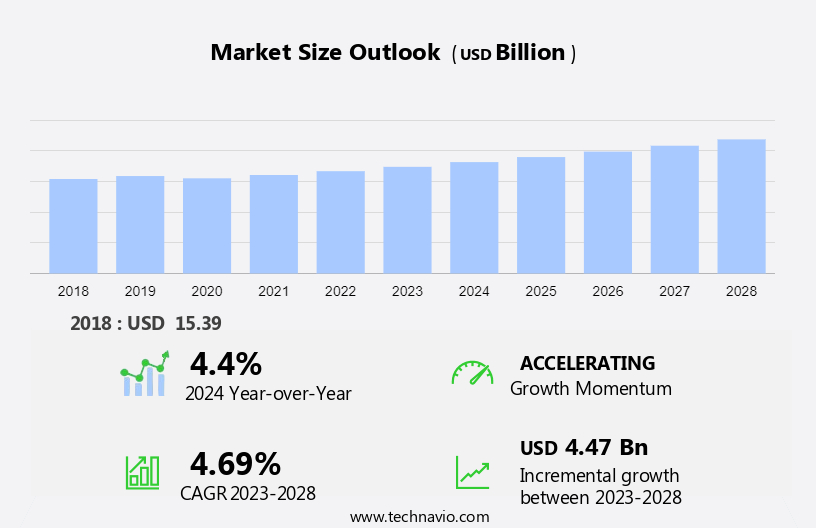

The US industrial casting market size is forecast to increase by USD 4.47 billion at a CAGR of 4.69% between 2023 and 2028.

- The industrial casting market in North America is experiencing significant growth due to increasing demand from the automotive industry. This sector's shift towards non-ferrous castings is another key trend, as these materials offer superior properties and increased energy efficiency. The high energy requirements In the industrial casting process present a challenge, as energy costs continue to rise. However, advancements in technology, such as the use of renewable energy sources and energy-efficient casting processes, are helping to mitigate this challenge. Additionally, the growing focus on sustainability and the adoption of green casting methods are expected to drive market growth In the coming years. Overall, the industrial casting market in North America is poised for steady expansion, driven by these market trends and the evolving needs of industries such as automotive and manufacturing.

What will be the size of the US Industrial Casting Market during the forecast period?

- The industrial casting market In the US is driven by various sectors, including automotive, construction, healthcare, telecom, and vehicle production. Metal casting continues to be a preferred choice for manufacturing precision metal parts due to its versatility and cost-effectiveness. Technologies such as die casting using sand molds and aluminum casting are gaining popularity for their energy efficiency and lightweight properties. The automotive sector, in particular, is a significant contributor to the market's growth, with increasing aluminum content in vehicles and the demand for high-performance, lightweight components. Stringent regulations in industries like automotive and construction are driving the adoption of recyclable materials and cast iron, such as grey iron, in place of traditional materials.

- Casting technologies continue to evolve, with a focus on automation and digitalization to improve productivity and reduce costs. The healthcare industry is also a growing market for industrial casting, with a demand for radiation protection tubes and other specialized components. In addition to automotive and construction, the industrial casting market serves various industries, including machine tools, heavy equipment, and telecom, where precision and durability are essential. Fuel efficiency and sustainability are key trends, with a growing focus on energy-efficient casting processes and the use of renewable energy sources. Overall, the industrial casting market In the US is expected to continue its growth trajectory, driven by advancements in casting technologies and the demand for lightweight, high-performance components in various industries.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Non ferrous

- Ferrous

- End-user

- Machinery

- Automotive

- Electrical and electronics

- Others

- Geography

- US

By Type Insights

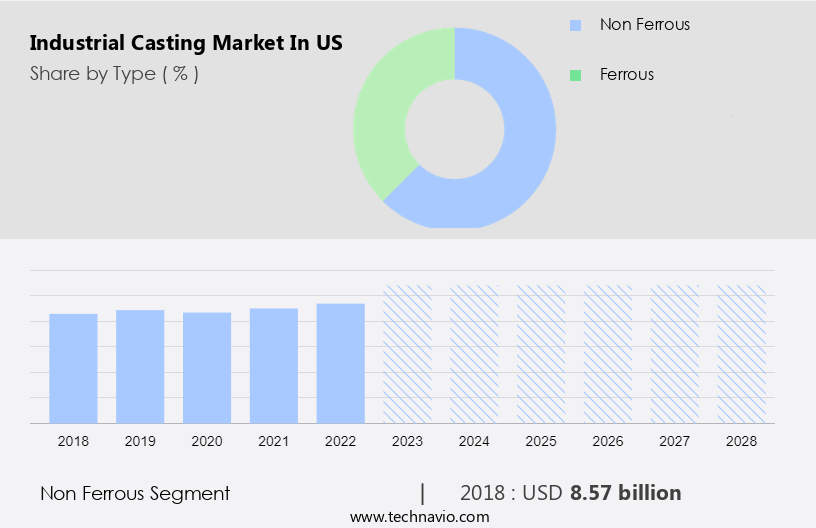

- The non ferrous segment is estimated to witness significant growth during the forecast period.

The non-ferrous casting market In the US is driven primarily by the increasing demand for lightweight materials, particularly aluminum, in various industries. Aluminum castings are extensively used In the automotive sector due to their high strength-to-weight ratio, making them an ideal choice for weight reduction strategies adopted by automobile OEMs. The construction industry also contributes significantly to the market growth due to the use of aluminum and other non-ferrous metals In the production of machine tools, heavy equipment, and building components. Stringent regulations regarding safety and energy efficiency are also driving the adoption of non-ferrous castings in industries such as healthcare, telecom, and automotive production.

The market is further expected to grow due to the increasing use of recyclable materials, including aluminum, in casting processes. Casting techniques continue to evolve, with a focus on automation and digitalization, fuel efficiency, and safety standards. Key industries such as automotive and transportation, equipment and machine, building and construction, aerospace and military, and alloy wheels continue to be major consumers of non-ferrous castings. The market is expected to grow further due to the increasing demand for fuel efficiency and the adoption of casting technologies that minimize environmental concerns. Raw materials, including recycled metals, play a crucial role In the market's growth, with aluminum being the most commonly used non-ferrous metal in casting applications.

Get a glance at the market share of various segments Request Free Sample

The Non ferrous segment was valued at USD 8.57 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of US Industrial Casting Market?

Growing demand from automotive industry is the key driver of the market.

- The Industrial Casting Market In the US is primarily driven by the automotive sector, with metal casting being a key technology for manufacturing automotive components such as engine parts, like bushings, differential shells, cylinder blocks, suspensions, and steering components. The demand for cast iron, specifically grey iron and ductile iron, is increasing due to its high strength and durability. The construction market also contributes significantly to the market growth, with the use of castings In the production of machine tools, heavy equipment, and building structures. Stringent regulations in various industries, including healthcare, telecom, and automotive production, are driving the need for energy efficiency and the use of recyclable materials in casting processes.

- Aluminum casting is gaining popularity due to its lightweight properties and high recyclability, making it an ideal choice for the automotive and transportation industries. The automotive and transportation sector is witnessing a shift towards fuel efficiency and automation and digitalization, leading to an increase In the use of casting techniques for manufacturing precision metal parts such as Decanters, Metal valves, gaskets, flanges, air injection tubes, coal throw pipes, radiation protection tubes, and other components. Fuel efficiency requirements and safety standards are major factors influencing the market dynamics. Manufacturing processes are becoming more efficient, with an increasing focus on the use of raw materials, including recycled metals such as aluminum, zinc, magnesium, and steel.

- The aerospace and military industries also contribute to the market growth, with the production of alloy wheels, clutch casings, cylinder heads, cross car beams, crank cases, battery housings, and other components. The market for industrial casting is expected to grow significantly In the coming years, driven by the increasing demand for castings in various industries, including passenger cars, light commercial vehicles, heavy commercial vehicles, hybrid electric vehicles, and battery electric vehicles. The market is also expected to benefit from the increasing use of casting technologies and the focus on fuel efficiency and environmental concerns.

What are the market trends shaping the US Industrial Casting Market?

Shift from ferrous to non ferrous castings is the upcoming trend In the market.

- The US metal castings market has witnessed a significant trend towards the utilization of non-ferrous metals, particularly aluminum, in various industries. This shift is driven by the desirable characteristics of non-ferrous castings, including resistance to rusting and corrosion, and their lighter weight compared to ferrous castings. The automotive sector, telecommunications industry, and industrial machinery are leading the charge in this transition. For instance, automotive manufacturers are replacing iron and steel components with lighter and more corrosion-resistant alternatives, such as aluminum, zinc, and magnesium, to enhance product quality and efficiency. These lightweight materials are also beneficial for the construction market, as they reduce the overall weight of buildings and infrastructure.

- In the automotive production process, components like alloy wheels, clutch casings, cylinder heads, cross car beams, crank cases, battery housings, passenger cars, light commercial vehicles, heavy commercial vehicles, hybrid electric vehicles, and battery electric vehicles are increasingly being manufactured using non-ferrous casting techniques. Additionally, the energy efficiency and fuel efficiency requirements in various industries are driving the demand for lightweight and recyclable materials, further boosting the market for non-ferrous metal castings. The casting technologies used In the production of these parts include sand casting, gravity casting, and various precision metal casting techniques. The market for industrial castings, including decanters, metal valves, gaskets, flanges, air injection tubes, coal throw pipes, radiation protection tubes, and precision metal parts, is also experiencing growth due to the increasing demand for fuel efficiency, automation, and digitalization, as well as safety standards in various industries.

- The market for castings is expected to continue growing, as industries seek to improve efficiency, reduce environmental concerns, and meet the demands of consumers for lighter, more durable, and more sustainable products.

What challenges does US Industrial Casting Market face during the growth?

High energy requirements in industrial casting process is a key challenge affecting the market growth.

- The industrial casting market In the US utilizes various casting techniques, including sand casting and gravity casting, to produce metal components for various sectors. Key industries such as automotive, construction, healthcare, telecom, and automobile manufacturing rely heavily on casting technologies for the production of precision metal parts, decanters, metal valves, gaskets, flanges, air injection tubes, coal throw pipes, radiation protection tubes, and other components. Metals used in casting include cast iron, grey iron, aluminum, steel, zinc, and magnesium. The automotive sector is a significant consumer of aluminum casting due to the increasing demand for lightweight materials in vehicle production.

- The construction market also utilizes cast iron and steel for the manufacturing of heavy equipment and machine tools. Stringent regulations regarding safety standards and fuel efficiency requirements In the automotive and transportation industries are driving the adoption of casting technologies that ensure fuel efficiency and environmental concerns. The use of recyclable materials, such as recycled aluminum, is also gaining popularity In the industry. The casting process is energy-intensive, with most energy requirements going towards metal melting. Natural gas and electricity are the primary energy sources used In the casting industry, and their usage is expected to increase with the growth of the market.

- Energy efficiency and the exploration of alternative energy sources are crucial for the industry's future growth. The industrial casting market caters to various sectors, including automotive production, equipment and machine manufacturing, building and construction, aerospace and military, alloy wheels, clutch casing, cylinder head, cross car beam, crank case, battery housing, passenger cars, light commercial vehicles, heavy commercial vehicles, hybrid electric vehicles, and battery electric vehicles. The market is expected to grow significantly due to the increasing demand for precision metal parts and the need for fuel efficiency and automation and digitalization in manufacturing processes.

Exclusive US Industrial Casting Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alcoa Corp.

- Aludyne Inc.

- Andritz AG

- Charlotte Pipe and Foundry Co.

- D.W. Clark

- EJ Group Inc.

- Georg Fischer Ltd.

- Great Lakes Castings LLC

- Grupo Industrial Saltillo SAB de CV

- Impro Precision Industries Ltd.

- KSB SE and Co. KGaA

- Meridian Lightweight Technologies Inc.

- MetalTek International

- Neenah Enterprises Inc.

- OSCO Industries Inc.

- Pace Industries

- Precision Castparts Corp.

- Sivyer Steel Castings LLC

- Sujan Industries

- The Weir Group Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The industrial casting market In the US is a significant sector that caters to various industries, including automotive, construction, healthcare, telecom, and more. This market encompasses the production of metal parts through different casting techniques, such as sand mold and gravity casting, using metals like cast iron, grey iron, aluminum, steel, zinc, magnesium, and others. The automotive sector is a major consumer of cast parts In the US market. The increasing demand for lightweight materials in vehicle production, particularly In the automobile market, has led to a growth in aluminum casting. The use of aluminum in automotive components, such as engine blocks, cylinder heads, and suspension parts, contributes to fuel efficiency and reduced emissions.

The construction market is another significant consumer of cast parts. Cast iron and grey iron are commonly used In the production of decanters, metal valves, gaskets, flanges, air injection tubes, coal throw pipes, radiation protection tubes, and other precision metal parts. These components are essential in various applications, including water and wastewater treatment, power generation, and heavy machinery. The industrial segment also includes the manufacturing of cast parts for industries like aerospace and military, equipment and machine, and building and construction. In these industries, cast parts are used to produce critical components, such as alloy wheels, clutch casings, cylinder heads, cross car beams, crank cases, battery housings, and various other parts for passenger cars, light commercial vehicles, heavy commercial vehicles, hybrid electric vehicles, and battery electric vehicles.

The use of recycled metals in casting processes is a growing trend In the US market. This approach not only reduces the environmental impact but also contributes to cost savings. The availability of recycled aluminum, steel, zinc, and magnesium has led to the development of new casting technologies that prioritize energy efficiency and automation and digitalization. Safety standards and fuel efficiency requirements are crucial factors driving the industrial casting market In the US. Stringent regulations in various industries necessitate the production of cast parts that meet specific safety and performance standards. Additionally, the focus on fuel efficiency and reducing emissions has led to the adoption of lightweight materials and casting techniques that minimize energy consumption.

The industrial casting market In the US is a dynamic and evolving sector that caters to various industries and applications. The use of advanced casting techniques, raw materials, and recycled metals, along with the emphasis on energy efficiency, automation, and safety standards, are key factors driving the growth of this market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

130 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.69% |

|

Market growth 2024-2028 |

USD 4.47 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.4 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -