Industrial Insulators Market Size 2024-2028

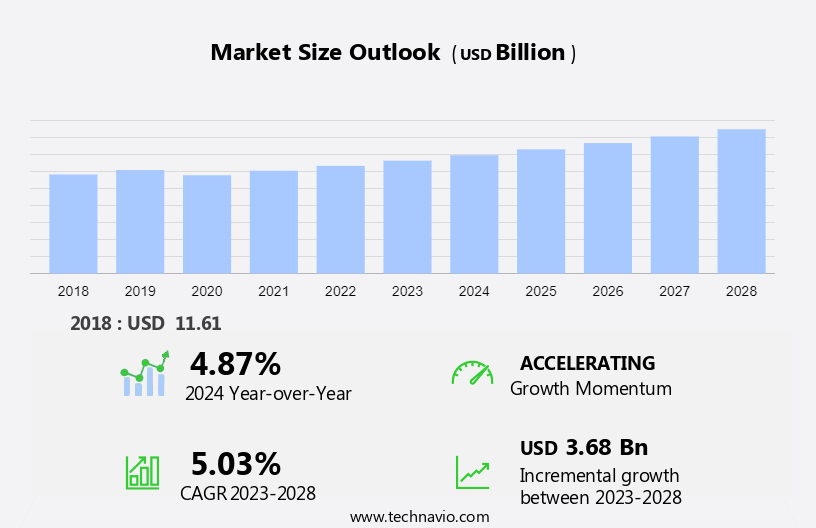

The industrial insulators market size is forecast to increase by USD 3.68 billion at a CAGR of 5.03% between 2023 and 2028.

- The market is driven by several key trends and challenges. One significant trend is the increasing focus on process efficiency in various industries, leading to the widespread adoption of insulation systems for energy savings and condensation control. Additionally, the integration of smart technologies and digitalization in insulation systems is gaining momentum, enabling real-time monitoring and optimization of insulation performance. Some of the commonly used insulation materials include aerogel, perlite, and dolomite. However, the market also faces challenges such as the need for technical expertise and installation complexities in industrial applications.

- Furthermore, concerns over environmental pollution and the rising awareness of the benefits of insulation for freeze protection and noise reduction are fueling market growth. Despite these opportunities, costs remain a critical factor, and the ongoing pandemic has added complexity to the market landscape. Overall, the market is poised for growth, with a focus on innovation and efficiency to meet the evolving needs of industries.

What will be the Size of the Market During the Forecast Period?

- The industrial insulation market is witnessing significant growth due to the increasing emphasis on energy efficiency and sustainability in various industries. Industrial insulation materials play a crucial role in maintaining optimal thermal performance, reducing energy consumption, and minimizing environmental pollution. Thermal performance optimization is a key focus area for industries seeking to improve their energy efficiency and reduce costs. Industrial insulation solutions are designed to maintain consistent temperatures, thereby reducing the energy required for heating or cooling processes. Sustainable insulation materials, such as natural fibers and recycled materials, are gaining popularity due to their environmental benefits and cost-effectiveness.

- Similarly, sustainable building practices are increasingly being adopted in the industrial sector to minimize energy consumption and reduce the carbon footprint. Low-energy building design and retrofit insulation solutions are becoming essential components of sustainable industrial facilities. Building envelope insulation is a critical aspect of energy-efficient industrial construction, ensuring that heat or cold does not escape, thereby reducing energy consumption and costs. Green building materials, including energy-saving technologies, are becoming an integral part of the industrial insulation market. These materials offer numerous benefits, such as noise reduction, condensation control, freeze protection, and improved process efficiency. Noise reduction is particularly important in industrial applications, where machinery and equipment can generate significant noise levels, leading to discomfort and productivity losses.

- Moreover, the industrial insulation market is witnessing rising awareness regarding the importance of energy performance analysis and cost savings. Industrial energy efficiency is a critical concern for industries, particularly in the current economic climate, where fiscal resources are under pressure. The pandemic and the volatility of crude oil prices have further emphasized the need for energy efficiency and cost savings. Industrial applications, such as machinery, boilers, pipes, storage tanks, and heat exchangers, require robust insulation solutions to maintain optimal operating temperatures and reduce energy consumption. Cooling towers are another critical application area, where insulation is essential for maintaining consistent water temperatures and reducing energy consumption.

- In conclusion, the benefits of insulation extend beyond energy efficiency and cost savings. Insulation also plays a crucial role in protecting industrial facilities from environmental pollution. By maintaining consistent temperatures and preventing the transfer of heat or cold, insulation helps to minimize the impact of external environmental conditions on industrial processes. In conclusion, the industrial insulation market is a dynamic and evolving market, driven by the need for energy efficiency, sustainability, and cost savings. Industrial insulation materials and solutions are essential components of industrial processes, providing numerous benefits, including thermal performance optimization, noise reduction, condensation control, freeze protection, and environmental pollution reduction. The market is expected to continue growing, driven by the increasing awareness of the importance of energy efficiency and sustainability in industrial applications.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

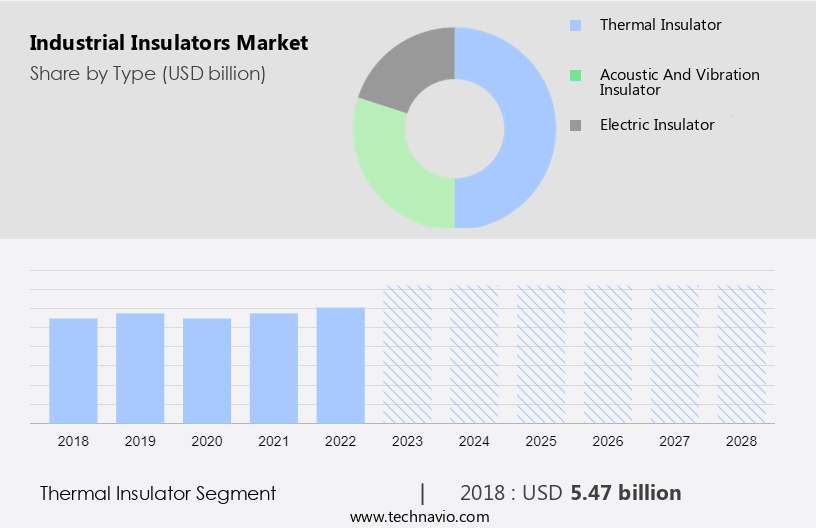

- Type

- Thermal insulator

- Acoustic and vibration insulator

- Electric insulator

- End-user

- Oil and gas

- Power generation

- Chemicals and petrochemicals

- Cement

- Others

- Geography

- APAC

- China

- India

- North America

- US

- Europe

- Germany

- France

- Middle East and Africa

- South America

- APAC

By Type Insights

- The thermal insulator segment is estimated to witness significant growth during the forecast period.

In the industrial sector, the thermal insulators market is projected to expand at a steady pace over the upcoming years. The expansion of this market can be linked to the growth of industries such as power generation, oil and gas, iron, and steel. Thermal insulators are extensively utilized in these industries due to their insulating properties, which help maintain optimal temperatures and improve energy efficiency. Additionally, the increasing industrialization and the burgeoning construction and manufacturing sectors are fueling the demand for insulation materials. The use of insulators in machinery, boilers, pipes, storage tanks, and heat exchangers is essential for maintaining the desired temperature levels and enhancing overall productivity.

Moreover, ongoing research and development (R&D) initiatives are underway worldwide to innovate and create advanced thermal insulator materials. These efforts are anticipated to drive the growth of the thermal insulators market, as the new materials are expected to offer superior insulation properties and increased energy savings. These materials provide excellent insulation properties and are widely adopted due to their cost-effectiveness and ease of application. The thermal insulators market encompasses various applications and end-use industries, making it a significant contributor to overall industrial growth.

Get a glance at the market report of share of various segments Request Free Sample

The thermal insulator segment was valued at USD 5.47 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

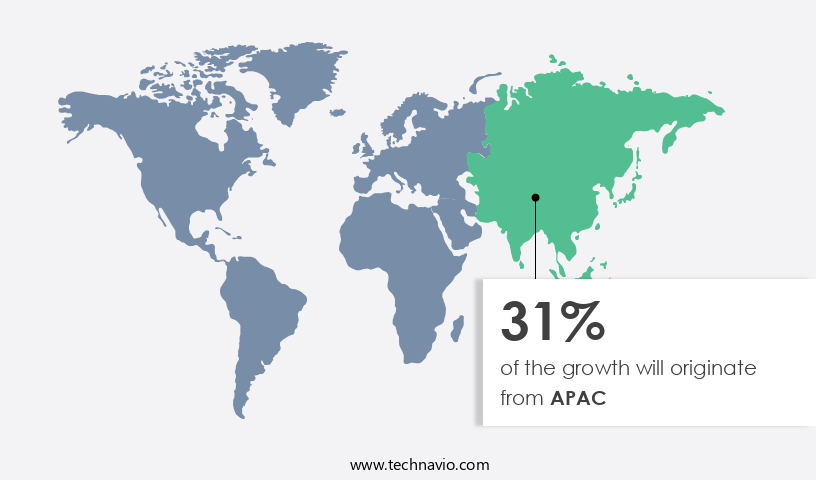

- APAC is estimated to contribute 31% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in APAC is projected to expand significantly during the forecast period. China, in particular, is a key player in this market due to its status as a major producer and consumer of insulation materials. The region's growing infrastructure development and the rise of China as a global manufacturing hub are driving the consumption of insulation products. This trend is further fueled by the increasing number of construction projects in the country, making it a major growth factor for the market. Heat transfer applications in industries such as petrochemical and cement are primary consumers of industrial insulators. Regulations mandating energy efficiency and cost-effective insulation solutions have led to an increase in insulation retrofitting activities.

Additionally, insulation standards, such as ASTM C518 and ASTM C1113, ensure thermal performance and prevent heat loss, thereby reducing energy consumption and improving overall efficiency. Thermal bridging, a common issue in insulation systems, can be mitigated through the use of advanced insulation materials and techniques. In conclusion, the market in APAC is poised for robust growth due to the increasing demand for insulation materials in infrastructure development and industrial applications. China's role as a major producer and consumer of insulation materials, coupled with regulatory requirements and the need for cost-effective insulation solutions, will continue to drive market growth during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Industrial Insulators Market?

The growing need for energy efficiency in buildings is the key driver of the market.

- The market is experiencing significant growth due to the increasing emphasis on energy efficiency in industrial buildings. Insulators play a crucial role in reducing energy leakage, thereby increasing the overall efficiency of industrial structures. With rising energy costs and growing environmental concerns, the demand for cost-effective insulation solutions is on the rise. New industrial facilities are incorporating advanced insulation technologies to minimize thermal loss, heat transfer, and condensation, which can lead to substantial energy savings. Governments and regulatory bodies are implementing policies and legislations to promote the use of insulation materials that meet energy efficiency and environmental standards. Insulation retrofitting of existing industrial infrastructure is also gaining popularity as a means to enhance energy efficiency and reduce heat loss.

- Additionally, the use of insulation materials, such as cement, perlite, dolomite, diabase, basalt, and elastomeric foam, can help minimize thermal bridging and improve dimensional stability. Insulation materials also offer benefits beyond energy efficiency, including corrosion protection, noise reduction, and freeze protection. However, the choice of insulation material depends on various factors, including the specific industrial application, temperature requirements, and environmental conditions. For instance, high-temperature piping may require specialized insulation materials, such as aerogel or CMS fibers, to ensure effective insulation and prevent energy losses. The market is expected to witness significant growth due to the increasing demand for insulation materials in various industrial sectors, including petrochemicals, machinery, boilers, pipes, storage tanks, and heat exchangers.

- Similarly, the market is also driven by the need for insulation materials that offer excellent fire barrier properties, as well as smoke and toxic gas resistance. The market is expected to grow further due to the increasing awareness of the benefits of insulation and the rising demand for sustainable insulation solutions. In conclusion, The market is poised for significant growth due to the increasing demand for energy-efficient insulation solutions, regulatory requirements, and the need to reduce energy costs and minimize environmental pollution. The market offers a wide range of insulation materials, each with unique properties that cater to specific industrial applications and environmental conditions. The use of insulation materials can help industrial facilities enhance their process efficiency, reduce energy losses, and comply with environmental regulations.

What are the market trends shaping the Industrial Insulators Market?

Integration of smart technologies and digitalization in insulation systems is the upcoming trend in the market.

- The market in the US is witnessing significant growth due to the integration of advanced technologies and digitalization in insulation systems. This innovation is aimed at enhancing energy efficiency, cost-effectiveness, and optimizing performance in industrial settings. For instance, the use of smart sensors in insulation systems allows real-time monitoring and data collection on temperature, humidity, and other relevant variables. Industrial facilities can utilize this data to gain insights into insulation system performance, enabling early detection of potential issues and preventing energy loss. Heat transfer is a critical aspect of industrial processes, particularly in petrochemical production and infrastructure expansion. Insulation plays a vital role in minimizing heat loss, thermal bridging, and energy consumption.

- In this regard, insulation retrofitting and adherence to insulation standards are essential for process efficiency and environmental sustainability. Regulations and policies, including energy efficiency standards and environmental regulations, are driving investments in cost-effective insulation solutions. These investments not only reduce energy costs but also provide corrosion protection and contribute to the overall sustainability of industrial facilities. Insulation materials such as cement, aerogel, perlite, dolomite, diabase, calcium silicate, and elastomeric foam offer various benefits, including high temperature resistance, moisture barrier properties, and dimensional stability.

- Additionally, the use of substitute materials like CMS fibers and asbestos alternatives addresses environmental concerns and reduces the risk of infrared radiation, smoke, and toxic gases. Industrial applications of insulation include machinery, boilers, pipes, storage tanks, and heat exchangers. The benefits of insulation, such as noise reduction, freeze protection, and condensation control, are essential for maintaining industrial-grade equipment and ensuring production facility efficiency. In conclusion, the US market is experiencing growth due to the integration of smart technologies, digitalization, and the adoption of cost-effective insulation solutions. These advancements contribute to energy efficiency, process efficiency, and environmental sustainability in various industrial applications, including petrochemicals and infrastructure expansion.

What challenges does Industrial Insulators Market face during the growth?

Technical expertise and installation challenges regarding industrial insulators is a key challenge affecting the market growth.

- The market in the US is experiencing challenges due to the lack of technical expertise and installation complexities. Inadequate insulation installations can lead to several issues, including reduced process efficiency, increased energy consumption, and safety concerns. Inefficient insulation can result in heat loss, thermal bridging, and condensation, leading to energy wastage and higher energy costs for industrial facilities. Moreover, subpar installations can pose fire hazards and fail to meet safety regulations, potentially endangering workers and industrial operations. Regulations and policies play a crucial role in driving the demand for industrial insulation. Environmental concerns and energy efficiency standards are key factors influencing the market.

- However, the need for cost-effective insulation solutions, insulation retrofitting, and infrastructure expansion are also significant market growth factors. Heat transfer applications in petrochemical industries, machinery, boilers, pipes, storage tanks, and heat exchangers require high-performance insulation materials. A range of insulation materials, including aerogel, perlite, dolomite, diabase, basalt, and calcium silicate, are used to address specific insulation requirements. These materials offer benefits such as fire barrier, smoke resistance, toxic gas protection, and noise reduction. The market dynamics are influenced by various factors, including production facilities' expansion, legislations, and investments. The pandemic and fiscal resources of oil-producing countries have also impacted the market.

- Insulation materials' costs, product demand, and the benefits of insulation in industrial applications continue to shape market trends. Industrial insulators play a critical role in maintaining energy efficiency and reducing environmental pollution. The rising awareness of sustainability and the need for eco-friendly insulation solutions are driving the demand for insulation materials with superior moisture barrier properties, dimensional stability, and condensation control. Elastomeric foam and plastic piping insulation are popular choices for their cost-effectiveness and ease of installation.

- In conclusion, the US the market is undergoing significant changes, driven by various factors such as regulations, energy efficiency standards, environmental concerns, and the need for cost-effective and sustainable insulation solutions. The market's growth is influenced by factors such as production facilities' expansion, legislations, and investments. Proper installation and technical expertise are essential to ensure the effectiveness and safety of industrial insulation systems.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- API Group Corp.

- Armacell International SA

- Aspen Aerogels Inc.

- Berkshire Hathaway Inc.

- Cabot Corp.

- Compagnie de Saint Gobain

- Etex NV

- Grasim Industries Ltd.

- Ibiden Co. Ltd.

- IPCOM NV

- Kingspan Group Plc

- Knauf Insulation

- Modern Insulators Ltd.

- Morgan Advanced Materials Plc

- Nichia Corp.

- Owens Corning

- Rath Aktiengesellschaft

- ROCKWOOL International AS

- TECHNONICOL Group of companies

- Yoshino Gypsum Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Industrial insulation plays a crucial role in the petrochemical industry, enhancing heat transfer efficiency and reducing energy losses. Cement-based insulation materials, such as calcium silicate and perlite, are commonly used due to their cost-effectiveness and insulation standards compliance. Regulations on energy efficiency and environmental concerns drive the demand for insulation retrofitting in infrastructure expansion projects. Heat loss and thermal bridging are significant concerns, leading to consumption of additional energy and increased production costs. Insulation standards and legislations ensure industrial facilities maintain process efficiency and adhere to energy efficiency and environmental regulations. Insulation materials like basalt, diabase, and aerogel offer high thermal performance for high-temperature piping and industrial-grade equipment.

Corrosion protection and noise reduction are additional benefits. Renovation projects focus on energy efficiency and sustainability, with investments in insulation being a critical component. Insulation materials, including elastomeric foam, offer moisture barrier properties and dimensional stability, reducing condensation and thermal loss. Fire barrier insulation protects against smoke and toxic gases. Substitute materials for asbestos, such as CMS fibers, are being increasingly used. Insulation's benefits extend beyond energy savings. It also offers freeze protection, condensation control, and noise reduction. The rising awareness of environmental pollution and the pandemic's impact on fiscal resources have further emphasized the importance of cost-effective insulation solutions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.03% |

|

Market growth 2024-2028 |

USD 3.68 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.87 |

|

Key countries |

US, China, India, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -