Industrial Water Treatment Equipment Market Size 2024-2028

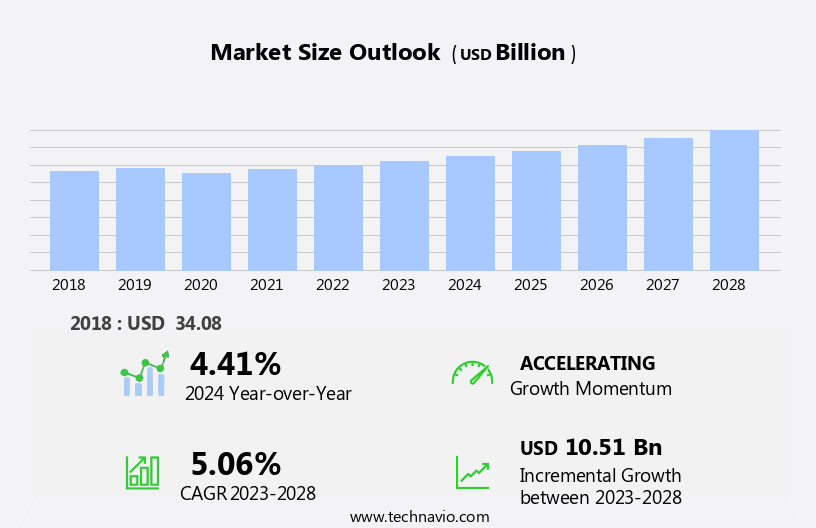

The industrial water treatment equipment market size is forecast to increase by USD 10.51 billion, at a CAGR of 5.06% between 2023 and 2028.

- The market is driven by the scarcity of water and escalating environmental concerns, necessitating the adoption of advanced water treatment solutions. The depletion of freshwater resources and increasing industrialization have led to the extensive use of recycled water, necessitating robust water treatment systems. Furthermore, stringent regulations governing industrial water discharge have intensified the need for efficient water treatment technologies. Innovation in water treatment technologies represents a significant trend in the market, with companies investing heavily in research and development to create more effective and sustainable solutions. Technological advancements, such as membrane filtration, ion exchange, and reverse osmosis, are revolutionizing the industrial water treatment landscape.

- However, the market faces challenges, including the impact of hardwater on water treatment equipment. Hardwater, which contains high mineral content, can cause scaling and corrosion, reducing the efficiency and lifespan of water treatment equipment. Addressing this challenge through the development of corrosion-resistant materials and advanced descaling techniques is crucial for market participants to remain competitive. Companies seeking to capitalize on market opportunities and navigate challenges effectively must stay abreast of technological advancements and regulatory requirements while addressing the impact of hardwater on their equipment.

What will be the Size of the Industrial Water Treatment Equipment Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market is characterized by continuous evolution and dynamism, driven by the diverse needs of various sectors and stringent regulatory requirements. Cooling water treatment remains a significant application, with ongoing advancements in energy efficiency and corrosion control. Simultaneously, membrane technology, including reverse osmosis and nanofiltration, gains prominence in water reuse and industrial wastewater treatment. Membrane fouling mitigation and filtration media optimization are crucial areas of focus, ensuring optimal process performance and environmental compliance. Membrane technology's integration with cleaning and maintenance services enhances system longevity and efficiency. Process water treatment applications, such as boiler water treatment, water demineralization, and pH control, require constant attention to maintain water quality and energy efficiency.

Ozone disinfection and UV disinfection are increasingly adopted for advanced disinfection and microbiological control. Environmental compliance, water conservation, and water quality monitoring are essential aspects of the industrial water treatment landscape. Spare parts and remote monitoring services ensure uninterrupted operations and minimize downtime. Ion exchange resins, scale prevention, and dissolved oxygen measurement are integral components of comprehensive water treatment strategies. Biofouling control, conductivity measurement, and turbidity measurement are essential for maintaining system performance and ensuring water reuse feasibility. The market's ongoing development reflects the interconnected nature of water treatment technologies and their role in industrial processes and sustainability.

How is this Industrial Water Treatment Equipment Industry segmented?

The industrial water treatment equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Energy and power

- Manufacturing

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

.

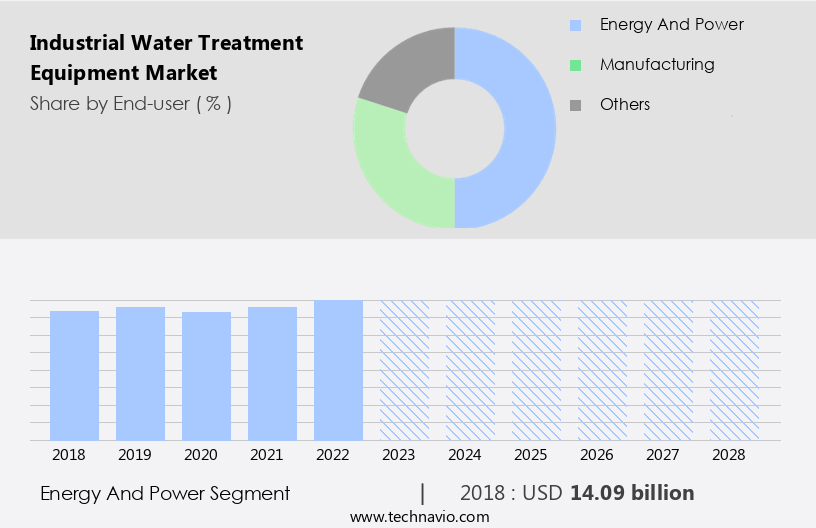

By End-user Insights

The energy and power segment is estimated to witness significant growth during the forecast period.

In the energy sector, water treatment plays a crucial role in power generation, oil and gas production, and refining and petrochemical processes. The International Energy Agency anticipates that water consumption in energy production will double over the next quarter-century. This water is utilized for power generation, cooling, condensing, and oil extraction. According to our analysis, the market will experience moderate growth during the forecast period. Water treatment technologies are integral to the energy industry, as water functions as the working fluid in thermal power plants. These technologies include intake screening, pre-treatment solutions, boiler feedwater treatment, condensate polishing, cooling tower makeup, flue gas desulfurization wastewater treatment, and energy-efficient reverse osmosis systems.

Moreover, water conservation is a significant concern in the energy sector due to increasing discharge standards and environmental compliance regulations. Scale prevention, water demineralization, and corrosion control are essential water treatment processes to maintain equipment efficiency and prolong asset life. Chemical dosing, pH control, dissolved oxygen measurement, and remote monitoring systems enable process optimization and reduce operational costs. Ozone disinfection and UV disinfection are essential for water reuse and water quality monitoring. Membrane technology, filtration media, and membrane fouling mitigation are crucial for process water treatment. Spare parts, cleaning, and maintenance services ensure the continuous operation of water treatment systems.

Energy efficiency and cooling water treatment are essential for reducing water usage and minimizing environmental impact. Biofouling control and water reuse are emerging trends in the industry, as they help conserve water resources and reduce operational costs. Installation services are vital for ensuring the successful implementation of water treatment systems in energy applications.

The Energy and power segment was valued at USD 14.09 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

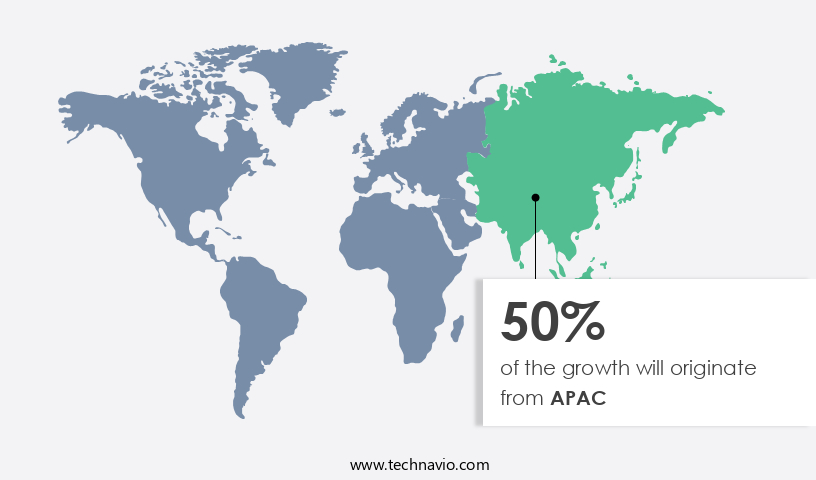

APAC is estimated to contribute 50% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The industrial water treatment market in the Asia-Pacific (APAC) region is experiencing significant growth, with China and India leading the charge. APAC is projected to have a faster growth rate than other regions due to the accelerating infrastructure development in countries such as Australia, South Korea, Taiwan, Singapore, and Japan. This development will increase both the number of industries and their power consumption, positively impacting the market. China is the largest market for industrial water treatment equipment in the region, driven by rapid industrialization, urbanization, and construction. The increasing generation of heavy metal waste necessitates effective water treatment solutions.

In addition, stringent wastewater discharge standards require industries to implement advanced water treatment technologies, such as scale prevention, water demineralization, and water conservation. Chemical dosing, boiler water treatment, municipal wastewater treatment, potable water treatment, process optimization, ozone disinfection, and environmental compliance are essential components of the industrial water treatment market. Spare parts, turbidity measurement, industrial wastewater treatment, ion exchange resins, corrosion control, pH control, dissolved oxygen measurement, remote monitoring, reverse osmosis, water quality monitoring, conductivity measurement, biofouling control, water reuse, energy efficiency, UV disinfection, water softening, cooling water treatment, cleaning and maintenance, membrane technology, filtration media, process water treatment, membrane fouling, and installation services are integral to the market's offerings.

Energy efficiency and water reuse are crucial trends in the market, as industries strive to minimize their environmental footprint and reduce costs. Technologies such as membrane technology and filtration media are gaining popularity due to their ability to provide high-quality water while minimizing energy consumption. In conclusion, the industrial water treatment market in APAC is poised for robust growth, driven by infrastructure development, increasing industrialization, and stringent regulations. The market offers a range of solutions to address various water treatment needs, with a focus on energy efficiency and water reuse.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Industrial Water Treatment Equipment Industry?

- The scarcity of water and escalating environmental concerns serve as the primary drivers in shaping the market dynamics.

- The global water scarcity issue is a pressing concern, with freshwater resources dwindling due to excessive extraction from underground sources. Approximately two-fifths of the global population currently faces water shortages, and regions such as the Middle East, North Africa, and Southeast Asia are projected to experience severe water scarcity in the coming decade. Population growth, increasing per capita water consumption, and urbanization are primary drivers of this issue. In response, the water treatment industry is gaining significance to address the depletion of freshwater resources. Advancements in water treatment technology are addressing these challenges through various methods, including remote monitoring, energy efficiency, water reuse, and biofouling control.

- Reverse osmosis, conductivity measurement, UV disinfection, and water softening are essential water treatment techniques. Remote monitoring enables real-time monitoring and analysis of water quality, ensuring efficient and effective treatment. Energy efficiency is another crucial factor, as water treatment accounts for a substantial portion of global energy consumption. Water reuse is a sustainable solution to address water scarcity, and biofouling control prevents the growth of microorganisms in water systems. UV disinfection and water softening are essential techniques for ensuring water quality and preventing corrosion and scaling, respectively. The integration of these technologies in water treatment systems is vital to meet the growing demand for clean water while minimizing energy consumption and reducing the environmental impact.

- In conclusion, the water treatment industry is essential in addressing water scarcity and ensuring sustainable water management. The adoption of advanced technologies such as remote monitoring, energy efficiency, and water reuse will play a significant role in mitigating the effects of water scarcity and ensuring a reliable water supply for future generations.

What are the market trends shaping the Industrial Water Treatment Equipment Industry?

- Water treatment technologies are experiencing significant innovation, which is currently a prominent trend in the market. This advancement is crucial for addressing water scarcity and ensuring the delivery of clean and safe water to communities.

- Industrial water treatment is a critical process that ensures the efficient use and maintenance of water in various industries. Two primary areas of focus are cooling water treatment and process water treatment. Cooling water treatment is essential for thermal power plants and other industries that rely on cooling systems to operate efficiently. Process water treatment is necessary for industries that use water in their manufacturing processes. Membrane technology, including reverse osmosis (RO) and nanofiltration, plays a significant role in industrial water treatment. Membrane fouling, however, is a common challenge in membrane filtration systems, which can be mitigated through the use of filtration media and cleaning and maintenance practices.

- Advanced technologies such as biomimetic membrane technology, membrane technology, and automatic variable filtration (AVF) technology are gaining popularity in the industrial water treatment market. For instance, Aquaporin Inside technology, developed by the Danish company Aquaporin, uses biomimetic membranes based on cell membranes for water treatment. This technology, which is used in both industrial and household water filtration systems, employs RO technology to filter out salts and larger solution components, providing clean water. Installation services are also crucial in the industrial water treatment market, ensuring the proper implementation and maintenance of water treatment systems. Overall, the innovation of new water treatment methods is essential to improve efficiency and address the challenges of the industrial water treatment process.

What challenges does the Industrial Water Treatment Equipment Industry face during its growth?

- The growth of the water treatment industry is significantly influenced by the challenges posed by the impact of hardwater on water treatment equipment. This issue necessitates continuous research and development to mitigate its effects and ensure the longevity and efficiency of the equipment used in the industry.

- Industrial water treatment is essential to maintain optimal water quality for various applications, including municipal wastewater treatment, potable water treatment, and industrial processes. One of the primary challenges in water treatment is the presence of calcium and magnesium ions, which can lead to scaling in water purification systems and industrial equipment. Scaling occurs when these ions accumulate and form mineral deposits on surfaces, reducing the efficiency of the equipment and increasing operational costs. Water conservation is a significant concern in industrial water treatment, as the backwashing of membranes in RO systems to prevent scaling results in the wastage of large quantities of water.

- Additionally, the discharge of wastewater containing high mineral concentrations can lead to the formation of scales in boilers, cooling towers, and other industrial equipment. Water demineralization and scale prevention are crucial aspects of industrial water treatment. Chemical dosing is an effective method for controlling the concentration of minerals and chemicals in water. Boiler water treatment is essential to maintain the efficiency and longevity of boilers by preventing the formation of scales and corrosion. Process optimization is another critical factor in industrial water treatment, as it helps minimize water usage and reduce operational costs. In conclusion, the importance of industrial water treatment lies in ensuring compliance with wastewater discharge standards, maintaining the efficiency and longevity of industrial equipment, and promoting water conservation.

- Effective water treatment strategies include water demineralization, scale prevention, and chemical dosing, among others. By implementing these strategies, industries can reduce operational costs, minimize water usage, and promote sustainable water management practices. Recent research indicates that advanced technologies, such as membrane filtration and ion exchange, are becoming increasingly popular in industrial water treatment due to their high efficiency and low water usage.

Exclusive Customer Landscape

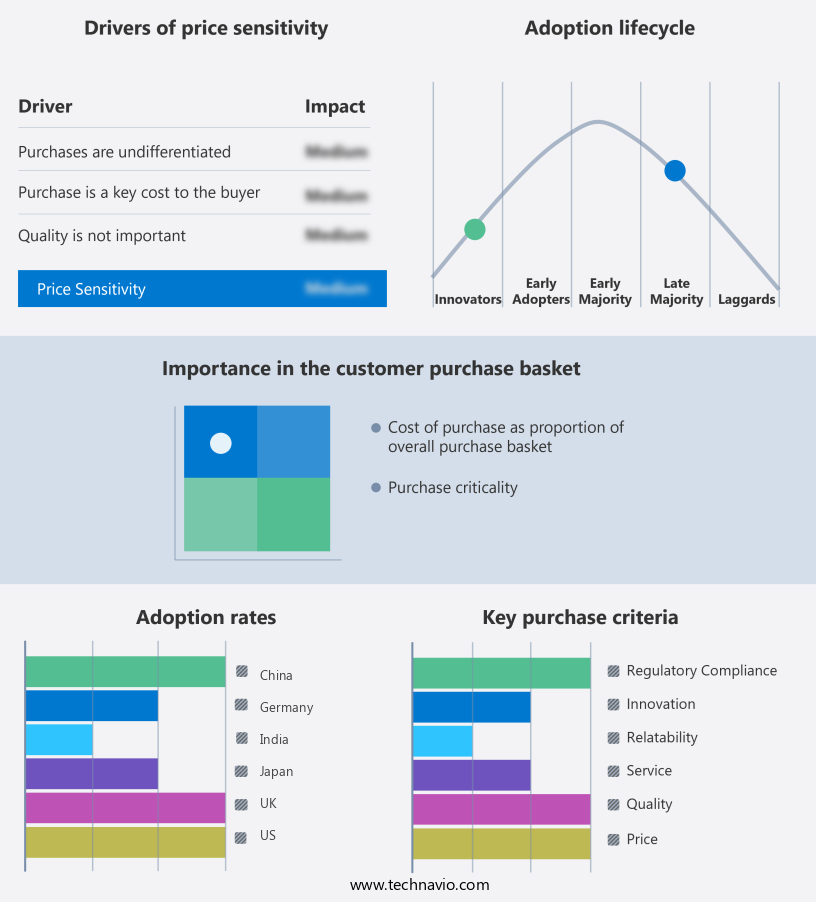

The industrial water treatment equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial water treatment equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, industrial water treatment equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - The company provides advanced water treatment solutions through the 3M Liqui Flux W Series Ultrafiltration system, specifically designed for multifiber polyethylene terephthalate (p.E.T.) technology and engineered for controlled hydrodynamics. This cutting-edge equipment delivers enhanced water purification capabilities, ensuring superior filtration efficiency and consistent performance. The system's innovative design caters to various industries, contributing to sustainable water management and resource conservation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Aquatech International LLC

- Calgon Carbon Corp.

- Culligan International Co.

- Danaher Corp.

- DuPont de Nemours Inc.

- Ecolab Inc.

- Evoqua Water Technologies LLC

- General Electric Co.

- Kurita Water Industries Ltd

- Lamor Corp. Plc.

- Lenntech BV

- Organo Corp.

- Pentair Plc

- Robert B. Hill Co.

- Samco Technologies Inc.

- SUEZ WTS USA Inc.

- Terex Corp.

- Veolia Environnement SA

- Xylem Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial Water Treatment Equipment Market

- In February 2023, Evoqua Water Technologies LLC, a leading provider of water and wastewater treatment solutions, announced the launch of their new AQUAvantage MBR (Membrane Bioreactor) system. This innovative product is designed to deliver superior performance in industrial water treatment applications, with a focus on energy efficiency and ease of operation (Evoqua Water Technologies LLC, 2023).

- In April 2024, Veolia Water Technologies, a global leader in water solutions and services, entered into a strategic partnership with Siemens Energy to jointly develop and commercialize membrane technologies for industrial water treatment. This collaboration aims to combine Veolia's expertise in water treatment with Siemens Energy's membrane technology to create advanced solutions for various industries (Veolia Water Technologies, 2024).

- In June 2024, Kemira Oyj, a global chemicals company, completed the acquisition of the water treatment business of QuÃmica Suiza S.A. This acquisition significantly expanded Kemira's presence in the Latin American market and strengthened its position as a leading provider of water treatment chemicals and services (Kemira Oyj, 2024).

Research Analyst Overview

- The market encompasses various technologies, including membrane filtration, trickling filters, thermal treatment, zero liquid discharge, and sand filtration. Membrane filtration and membrane bioreactors are gaining traction due to their ability to provide high-quality water and reduce water footprint. Digital twins and the Internet of Things facilitate data-driven decisions, enhancing the efficiency of water treatment processes. Advanced oxidation processes, such as electrochemical treatment and ultraviolet disinfection, offer effective solutions for water contaminants. Biological treatment methods, including activated sludge process and anaerobic digestion, contribute to the circular economy by transforming wastewater into valuable resources. Cloud computing and big data analytics enable machine learning algorithms to optimize water treatment processes, reducing costs and improving performance.

- Thermal treatment and air stripping are essential for industrial applications requiring high temperature and pressure conditions. Green chemistry and circular economy principles are driving the adoption of water recovery and sludge treatment technologies. Artificial intelligence and chemical oxidation methods are also gaining popularity for their ability to address complex water treatment challenges. Zero liquid discharge systems and advanced biological treatment processes are essential for industries striving to minimize their environmental impact. The integration of data-driven decisions, artificial intelligence, and the circular economy is transforming the industrial water treatment landscape.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Water Treatment Equipment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.06% |

|

Market growth 2024-2028 |

USD 10.51 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.41 |

|

Key countries |

China, US, Germany, Japan, UK, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Industrial Water Treatment Equipment Market Research and Growth Report?

- CAGR of the Industrial Water Treatment Equipment industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the industrial water treatment equipment market growth of industry companies

We can help! Our analysts can customize this industrial water treatment equipment market research report to meet your requirements.

RIA -

RIA -