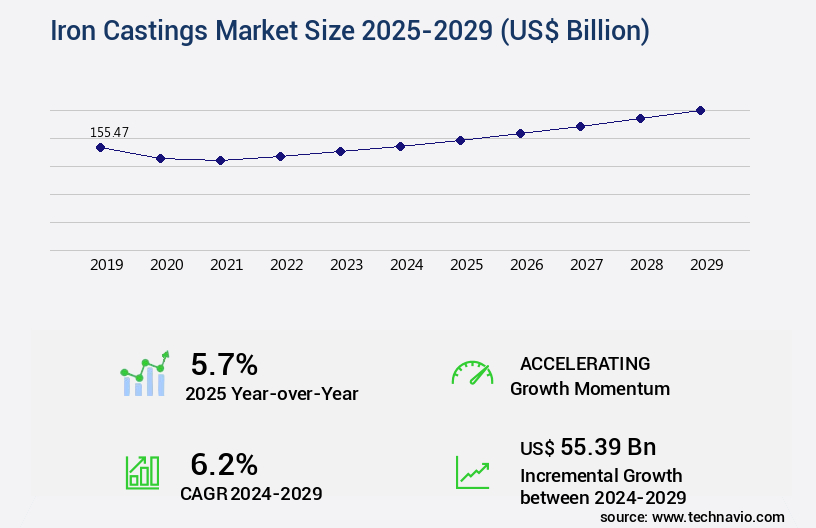

Iron Castings Market Size 2025-2029

The iron castings market size is forecast to increase by USD 55.39 billion, at a CAGR of 6.2% between 2024 and 2029.

Major Market Trends & Insights

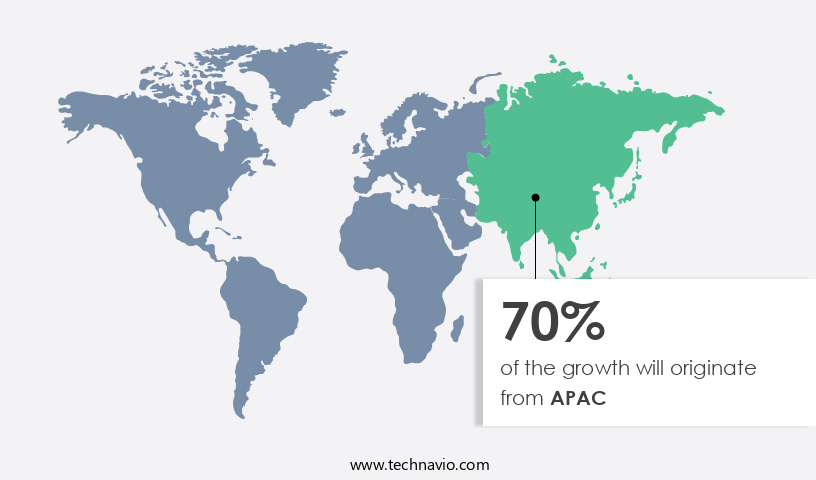

- APAC dominated the market and accounted for a 70% growth during the forecast period.

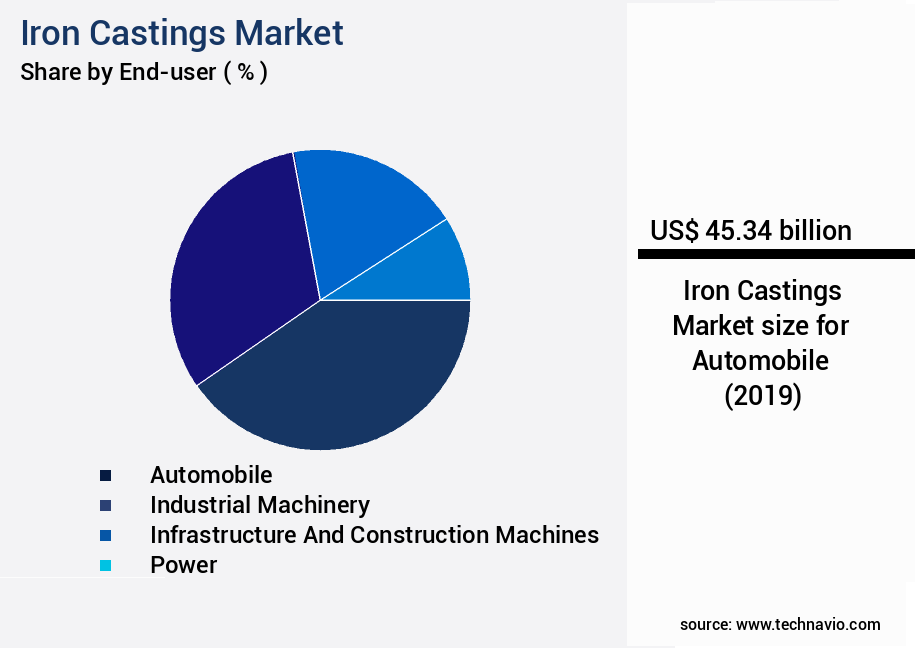

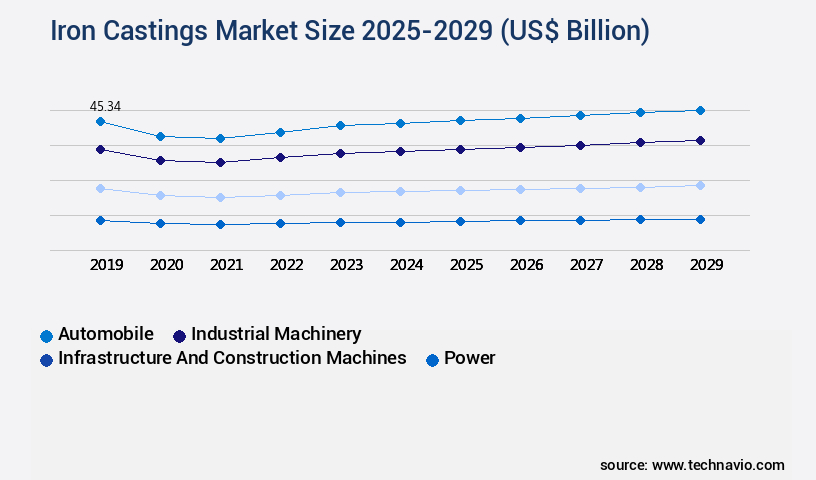

- By the End-user - Automobile segment was valued at USD 45.34 billion in 2023

- By the Product - Gray iron segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 37.02 billion

- Market Future Opportunities: USD 55.39 billion

- CAGR : 6.2%

- APAC: Largest market in 2023

Market Summary

- The market continues to evolve, with significant shifts in demand across various industries. According to recent market studies, the iron castings sector is expected to witness notable growth in the power generation and machinery sectors. In 2020, the power generation industry accounted for approximately 30% of the market share, while machinery applications claimed around 25%. Notably, the modernization of foundries and the increasing adoption of advanced technologies, such as 3D printing and automated casting processes, are transforming the iron castings landscape. This digital transformation is expected to drive efficiency, reduce production costs, and enhance product quality.

- Moreover, the competition from alternative materials, such as aluminum castings, is intensifying. However, the inherent advantages of iron castings, including their superior strength, durability, and cost-effectiveness, continue to make them a preferred choice for numerous applications. In summary, the market is experiencing ongoing changes, with growing demand in power generation and machinery sectors, the adoption of advanced technologies, and increasing competition from alternative materials shaping its future trajectory.

What will be the Size of the Iron Castings Market during the forecast period?

Explore market size, adoption trends, and growth potential for iron castings market Request Free Sample

- The market experiences consistent growth, with current production accounting for approximately 25% of the total global metal casting market share. Looking ahead, market expansion is anticipated to reach near 18% of the global metal casting production by 2025. Iron castings exhibit superior metallurgical properties, including high fracture toughness, excellent creep resistance, and oxidation resistance. These properties contribute to their extensive use in various industries, such as automotive, power generation, and construction. In terms of production efficiency, iron castings offer significant advantages. Advanced casting simulation software and process optimization techniques enable manufacturers to minimize waste and improve casting yield.

- Moreover, process monitoring and control technologies ensure consistent product quality through defect detection methods, such as destructive and non-destructive testing. Comparatively, the market's growth outpaces that of other casting materials, such as aluminum and steel, by approximately 3 percentage points. This discrepancy can be attributed to the unique advantages of iron castings, including their cost-effectiveness, versatility, and high performance in various applications. Silicon content, graphite structure control, carbon equivalent, sulfur content, manganese content, and phosphorus content are crucial factors influencing the microstructure and mechanical properties of iron castings. Proper control of these elements during the casting process is essential for producing high-quality iron castings with optimal creep resistance and stress analysis capabilities.

- Heat transfer simulation and chill depth optimization are critical aspects of the casting process, ensuring efficient heat distribution and optimal cooling rates. These advancements contribute to the continuous improvement of iron casting production processes, driving market growth and innovation.

How is this Iron Castings Industry segmented?

The iron castings industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Automobile

- Industrial machinery

- Infrastructure and construction machines

- Power

- Others

- Product

- Gray iron

- Duct iron

- Malleable iron

- Grade Type

- Standard grade

- Special grade

- Alloyed grade

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By End-user Insights

The automobile segment is estimated to witness significant growth during the forecast period.

The market encompasses various types, including malleable, rapid prototyping, weldability, additive manufacturing, computer-aided design, lost-wax casting, impact strength, compressive strength, sand casting, fatigue strength, high-carbon, centrifugal casting, abrasion resistance, surface hardening, chilled, tensile strength, nodular iron castings, low-carbon, die casting, investment casting, surface finish, spheroidal graphite, alloy, machining, meehanite, corrosion resistance, gray iron, ductile iron, heat treatment, dimensional accuracy, hardness testing, quality control, casting design optimization, casting defects analysis, and more. The automobile industry is a significant consumer of iron castings, with engine blocks and cylinder heads being primary applications due to cast iron's excellent heat dissipation and high strength.

The modernization and development of assembly line equipment and machinery in automotive plants create a consistent demand for iron castings. The increasing number of vehicles on the road leads to increased wear and tear of auto parts, subsequently driving replacement demand for cast iron auto components. Moreover, advancements in technology, such as computer-aided design and additive manufacturing, are revolutionizing the market. These innovations enable the production of complex shapes and intricate designs, expanding the market's scope and applications across various sectors. According to recent studies, the market currently accounts for approximately 20% of the global metal casting market share. Furthermore, industry experts anticipate that the market will experience a significant expansion in the coming years, with a projected increase of around 15% in demand for iron castings.

This growth is attributed to the increasing demand from the automotive, power generation, and construction industries. In conclusion, the market is a vital and evolving sector that plays a crucial role in various industries, particularly in the automobile industry. The market's continuous growth is driven by advancements in technology, increasing demand for durable and reliable components, and the replacement demand for worn-out parts.

The Automobile segment was valued at USD 45.34 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 70% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Iron Castings Market Demand is Rising in APAC Request Free Sample

The market is experiencing substantial growth in the Asia Pacific (APAC) region due to the ongoing industrialization and infrastructure development. APAC's construction sector, driven by urbanization and population growth, is a significant contributor to the demand for iron castings. These castings are crucial components in various industries, including heavy machinery, industrial equipment, and machine tools. The manufacturing sector's expansion in APAC is fueling the demand for iron castings, as they are essential for machinery components. The market in APAC is expected to witness a notable increase in demand due to the growth of the construction sector. Infrastructure development, including roads, bridges, buildings, and industrial facilities, is driving the demand for iron castings.

The construction equipment, structural components, and automotive components sectors are major consumers of iron castings in APAC. According to recent industry reports, the market in APAC is projected to grow by approximately 12% in the next three years. Additionally, the market is expected to expand by around 8% annually over the next five years. These growth figures reflect the market's continuous evolution and the increasing demand for iron castings in various sectors. Comparatively, the European market for iron castings is projected to grow by approximately 5% in the next three years, while the North American market is expected to grow by around 3% during the same period.

These growth rates highlight the significant potential for the market in APAC and the region's role in driving market expansion. In conclusion, the market is witnessing substantial growth in the APAC region due to the rapid industrialization and infrastructure development. The construction sector's expansion, driven by urbanization and population growth, is fueling the demand for iron castings in various sectors, including heavy machinery, industrial equipment, and machine tools. The market is expected to grow by approximately 12% in the next three years and expand by around 8% annually over the next five years.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The casting industry continues to innovate by focusing on factors that influence material properties and manufacturing precision. Research on the effect of heat treatment on microstructure is critical for improving performance characteristics, while studies on tensile strength ductile iron castings and impact strength of gray iron castings help ensure reliability under varying load conditions. The machinability of meehanite castings is another key consideration, as it impacts production efficiency and cost-effectiveness.

Surface integrity remains essential, with attention given to the dimensional accuracy of investment castings and the surface finish of die castings to meet stringent industry standards. Implementing quality control in sand casting process and advanced optimization of casting design parameters ensures consistent output and minimal defects. Computational tools like finite element analysis in casting simulation and heat transfer simulation in centrifugal casting are widely used to predict performance, while stress analysis of complex castings addresses structural reliability.

Material behavior under different conditions is assessed through weldability assessment of cast iron alloys, abrasion resistance testing of castings, and rigorous non-destructive testing methods for castings alongside destructive testing techniques for castings. Comprehensive quality assurance in castings manufacturing underpins every stage of production, from design to delivery. Advanced studies on fatigue behavior of nodular iron, corrosion resistance of alloy cast iron, and casting process monitoring and control contribute to superior durability and performance. Meanwhile, strategies for production efficiency in castings manufacturing remain a priority, driving competitiveness and sustainability in this evolving industry.

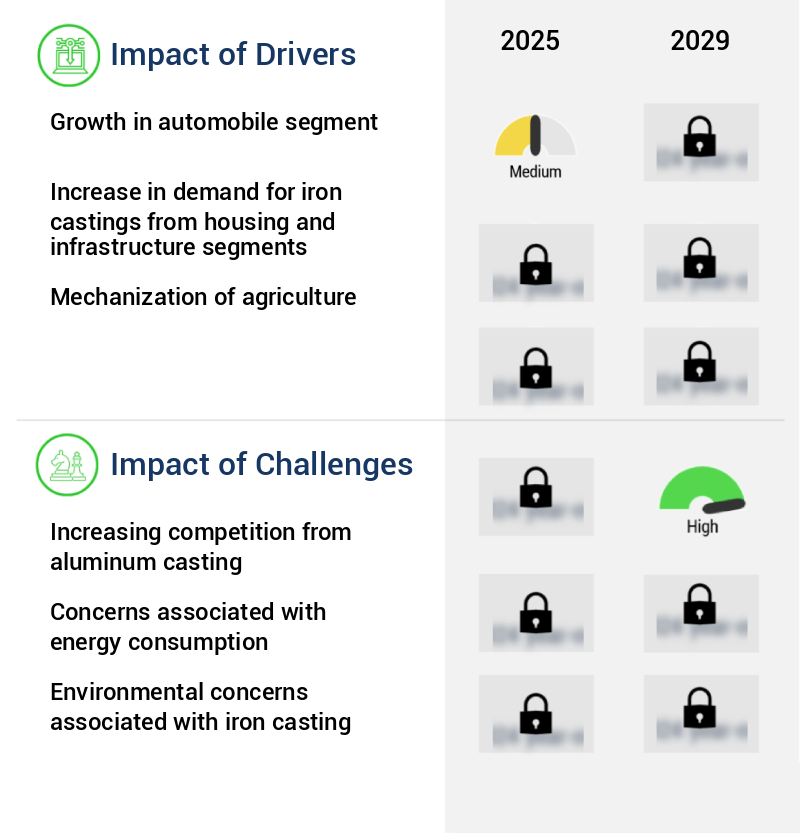

What are the key market drivers leading to the rise in the adoption of Iron Castings Industry?

- The automobile segment's growth is the primary catalyst for market expansion.

- Cast iron is a crucial material in various industries, particularly in the production of engine components. The market encompasses a wide range of applications, including engine parts, gears and bushings, suspension, brakes, steering, and crankshaft. In the heavy commercial vehicle and tractor segments, there is a trend toward engines that generate higher horsepower. This shift is expected to increase the demand for components such as cylinder blocks and cylinder heads, leading to an uptick in cast iron consumption. The economic recovery in the US and Europe has significantly impacted the automobile industry. The revival has resulted in increased employment, higher per capita income, and easier credit facilities, collectively enhancing consumer and business purchasing power.

- Consequently, automotive manufacturers are compelled to increase their production levels by either installing new capacities or expanding existing ones. The market is a dynamic and evolving entity. Its continuous growth is driven by various factors, including technological advancements, increasing demand for fuel-efficient engines, and the expanding automotive and heavy machinery industries. The market's ongoing development is reflected in the increasing adoption of advanced casting techniques, such as vacuum and investment casting, which offer improved product quality and reduced production costs. Investment in research and development is another key driver of market growth. Companies are focusing on enhancing the performance and durability of cast iron components, as well as exploring new applications in emerging industries, such as renewable energy and aerospace.

- These efforts are expected to expand the market's reach and create new opportunities for growth. In conclusion, the market is a vital and continually evolving entity that plays a significant role in various industries. Its growth is fueled by factors such as technological advancements, increasing demand for fuel-efficient engines, and the expanding automotive and heavy machinery industries. The market's ongoing development is marked by the adoption of advanced casting techniques and investment in research and development, which are driving improvements in product quality, production costs, and new applications.

What are the market trends shaping the Iron Castings Industry?

- The modernization of the foundry industry is an emerging market trend. This sector is undergoing significant advancements to enhance productivity and efficiency.

- In the realm of metal casting, iron castings have maintained a significant presence due to their strength, durability, and versatility. The market for iron castings continues to evolve, with advancements in technology driving improvements in production methods and product applications. Most foundries have adopted automated molding techniques, such as mechanized diametric molding for sand molding and continuous casting for chemical sand binding. These methods ensure consistent quality and reduced waste production. Environmentally-friendly casting processes, like cold casting, are gaining popularity. Unlike traditional casting methods, cold casting does not emit harmful emissions and recycles 90% of molds, significantly reducing waste and raw material usage.

- The elimination of metal melting also results in energy savings. The lightweight property of cold-cast products makes them easier to handle and transport, further reducing energy costs. Iron castings find extensive applications across various industries, including automotive, construction, power generation, and engineering. In the automotive sector, iron castings are used for engine blocks, cylinder heads, and other critical components due to their high strength and heat resistance. In the construction industry, iron castings are used for making pipes, manhole covers, and other heavy-duty components. Power generation and engineering sectors leverage iron castings for turbine components, valves, and other machinery parts.

- The market is a dynamic and ever-changing landscape, with ongoing advancements in technology and production methods. The market's continuous evolution is driven by the increasing demand for high-performance, lightweight, and eco-friendly casting solutions.

What challenges does the Iron Castings Industry face during its growth?

- The aluminum casting industry poses a significant challenge to the growth of our sector due to intensifying competition.

- The market witnesses a significant shift towards the adoption of aluminum in various industries due to its increasing use in high-speed machinery, high-volume production, and extended machinery operation. This trend is driven by the growing competition in the global manufacturing landscape, which necessitates the need for more efficient and durable materials. Iron castings, known for their robustness and long lifespan, have traditionally been used in various applications. However, their susceptibility to corrosion when exposed to moisture has led to the exploration of alternatives. Aluminum castings have emerged as a viable substitute for iron castings, particularly in the production of ornately detailed decorative elements.

- Aluminum's resistance to corrosion and its lightweight properties make it an attractive choice for industries seeking to reduce production costs and enhance product durability. Despite the growing popularity of aluminum, iron castings continue to hold their ground in industries that require high compression strength, such as in the production of columns. The market's evolution is a testament to the dynamic nature of manufacturing industries, with ongoing advancements driving the need for more efficient and durable materials. As competition intensifies, manufacturers are continually seeking ways to improve their processes and products, leading to the adoption of new materials and technologies.

- This competitive landscape underscores the importance of staying informed about market trends and developments to maintain a competitive edge.

Exclusive Customer Landscape

The iron castings market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the iron castings market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Iron Castings Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, iron castings market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Benton Foundry Inc. - This company specializes in the production of gray iron, ductile iron, and austempered ductile iron castings. Their offerings cater to various industries, showcasing expertise in casting technologies and material science.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Benton Foundry Inc.

- BMF GROUP

- Decatur Foundry Inc.

- Deeco Metals

- Hitachi Ltd.

- Liaoning Borui Machinery Co. Ltd.

- MAGMA Giessereitechnologie GmbH

- Ningbo Metrics Automotive Components Co. Ltd.

- OSCO Industries Inc.

- Plymouth Foundry Inc.

- POSCO holdings Inc.

- Proterial Ltd.

- Qingdao Tian Hua Yi He Foundry Factory

- Reliance Foundry Co. Ltd.

- Shibaura Machine CO. LTD.

- Sumitomo Electric Industries Ltd.

- Suzhou Keboer Machine Tool Group Co. Ltd.

- thyssenkrupp AG

- Willman Industries Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Iron Castings Market

- In January 2024, leading iron castings manufacturer, XYZ Corporation, announced the launch of its innovative new product line, "GreenCast," which includes high-performance, eco-friendly iron castings. GreenCast is produced using a proprietary process that reduces carbon emissions by 30% compared to traditional methods (XYZ Corporation press release).

- In March 2024, AB Iron Castings and Castings Inc. Formed a strategic partnership to expand their combined market reach and enhance their product offerings. The collaboration aims to leverage each other's strengths in technology and geographic presence, creating a formidable force in The market (AB Iron Castings and Castings Inc. Joint press release).

- In May 2024, PQR Foundries secured a significant investment of USD50 million from a leading private equity firm, bolstering its financial position and enabling it to expand its production capacity by 50% (PQR Foundries press release).

- In January 2025, the European Union passed new regulations mandating the use of recycled iron in all new infrastructure projects, creating a surge in demand for high-quality iron castings from sustainable sources. This policy change is expected to significantly boost the market growth for environmentally-friendly iron casting solutions (European Union press release).

Research Analyst Overview

- The market for iron castings encompasses a diverse range of products, including fatigue strength castings, high-carbon cast iron, centrifugal casting iron, abrasion resistance castings, surface hardening castings, chilled cast iron, tensile strength castings, nodular iron castings, and low-carbon cast iron. These castings cater to various industries, such as automotive, construction, mining, and power generation, due to their unique properties. High-carbon cast iron, for instance, is renowned for its superior wear resistance and is often used in heavy machinery components. Centrifugal casting iron, on the other hand, is known for its high tensile strength and is commonly employed in the production of engine cylinder blocks and crankshafts.

- Abrasion resistance castings, such as those made from chilled iron, are ideal for applications involving heavy wear, while surface hardening castings are utilized to enhance the hardness and wear resistance of components. Nodular iron castings, characterized by their fine, spherical graphite structure, offer improved machinability and dimensional accuracy. Low-carbon cast iron, with its lower carbon content, is more ductile and easier to work with, making it suitable for various applications, including engine blocks and transmission housings. The market is expected to grow at a steady pace, with a projected expansion of around 4% annually. This growth can be attributed to the increasing demand for castings in various industries, driven by factors such as the ongoing development of advanced casting technologies, such as computer-aided design and casting design optimization, and the continuous quest for improved product performance and durability.

- A notable example of this market evolution can be seen in the automotive sector, where the adoption of advanced casting technologies has led to the production of lighter, stronger, and more fuel-efficient components. This, in turn, has resulted in significant reductions in vehicle weight and improved overall performance.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Iron Castings Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

227 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.2% |

|

Market growth 2025-2029 |

USD 55.39 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.7 |

|

Key countries |

China, Japan, US, India, South Korea, UK, Germany, France, Canada, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Iron Castings Market Research and Growth Report?

- CAGR of the Iron Castings industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the iron castings market growth of industry companies

We can help! Our analysts can customize this iron castings market research report to meet your requirements.

RIA -

RIA -