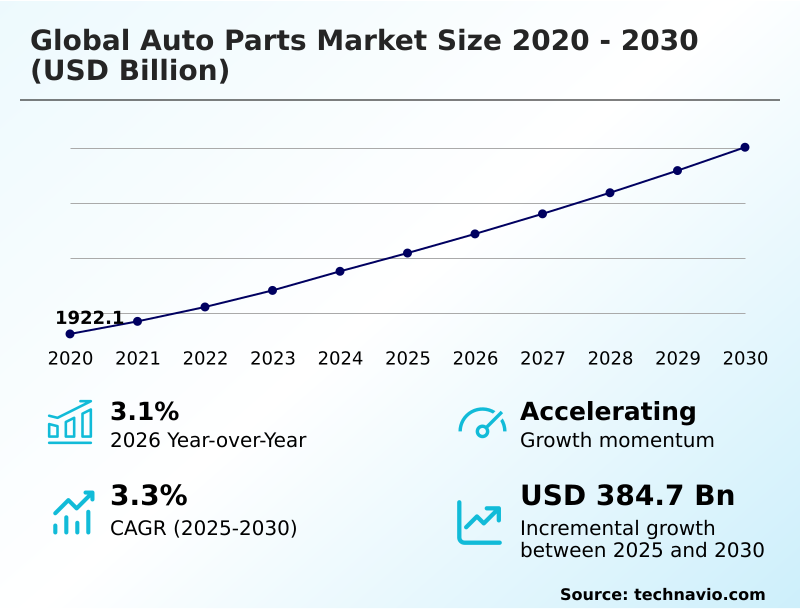

Auto Parts Market Size 2026-2030

The auto parts market size is valued to increase by USD 384.7 billion, at a CAGR of 3.3% from 2025 to 2030. Electrification and propulsion innovation will drive the auto parts market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 33.3% growth during the forecast period.

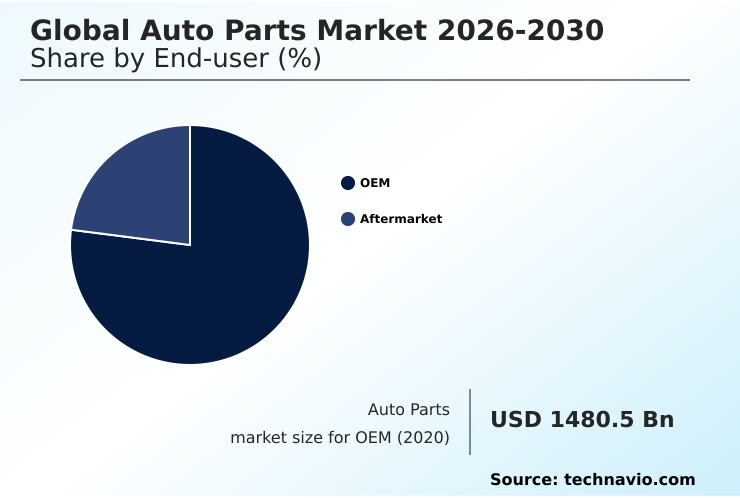

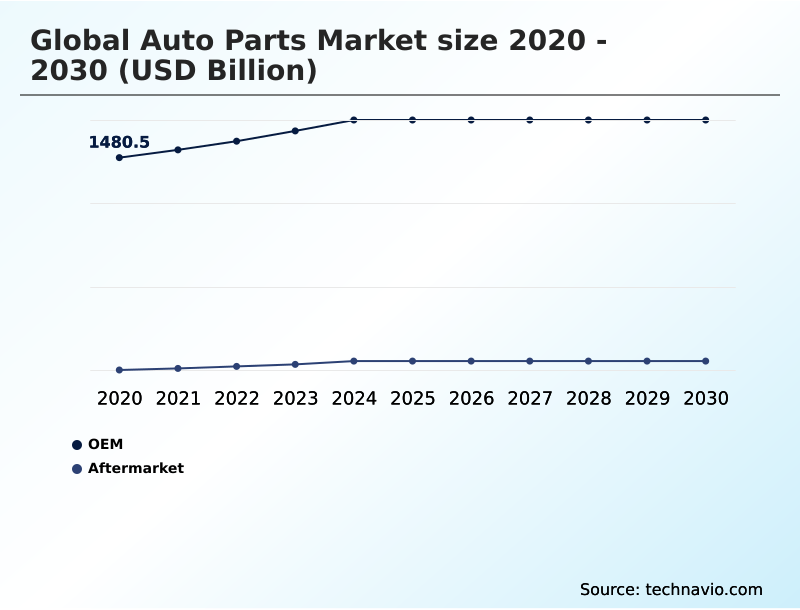

- By End-user - OEM segment was valued at USD 1664.6 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 678.8 billion

- Market Future Opportunities: USD 384.7 billion

- CAGR from 2025 to 2030 : 3.3%

Market Summary

- The auto parts market is navigating a period of profound technological change, driven by the dual trends of electrification and digitalization. The shift away from traditional internal combustion engines toward electric propulsion systems is fundamentally altering product portfolios, necessitating expertise in high-voltage battery chemistry, power electronics, and thermal management solutions.

- Simultaneously, the rise of software-defined vehicle architectures places a new emphasis on high-performance semiconductors, centralized electronic control units, and sophisticated sensor arrays, including high-resolution cameras and radar modules. This transition challenges legacy suppliers to adapt while creating opportunities for innovation in areas like modular vehicle electronics and over-the-air updates.

- A core business scenario involves manufacturers re-architecting supply chains to balance the production of legacy drivetrain systems with new investments in electric motor and battery management system manufacturing, a complex operational pivot essential for long-term market relevance and competitiveness in an evolving automotive landscape.

What will be the Size of the Auto Parts Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Auto Parts Market Segmented?

The auto parts industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- OEM

- Aftermarket

- Distribution channel

- Offline

- Online

- Type

- Electrical and electronics

- Driveline and powertrain

- Interior and exterior

- Body and chassis

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- North America

By End-user Insights

The oem segment is estimated to witness significant growth during the forecast period.

The OEM segment is undergoing a fundamental transformation, moving from legacy mechanical components to integrated digital systems.

This evolution is driven by the industry's pivot toward software-defined vehicle architectures, where components like drivetrain systems, advanced wiring systems, and braking systems are managed by centralized electronic control units.

Manufacturers are now prioritizing the development of modular vehicle electronics and high-speed data networks to support autonomous driving technologies and connected services. The integration of smart manufacturing, leveraging Industry 4.0 technologies, is critical for producing these complex parts.

For instance, the use of AI-driven digital twin simulations in production has led to a 15% reduction in micro-defects for certain structural components, enhancing both quality and efficiency.

The OEM segment was valued at USD 1664.6 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 33.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Auto Parts Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the market is diversifying, with distinct regional specializations influencing global supply chains. APAC leads in incremental growth, contributing over 33% of the market's expansion, largely driven by its dominance in lithium-ion battery and semiconductor component manufacturing.

In this region, the development of e-axle systems is a key focus.

Europe, which accounts for nearly 32% of growth opportunities, is concentrating on regulatory-driven innovation, including the production of silicon carbide chips to support its ambitious transition to electric mobility.

North America's strategy centers on reinforcing domestic supply chains and near-shoring, with significant investments in lightweight structural components and zonal architecture to support the production of next-generation electric trucks and SUVs.

This regionalization strategy aims to build resilience against geopolitical and logistical disruptions across the industry.

Market Dynamics

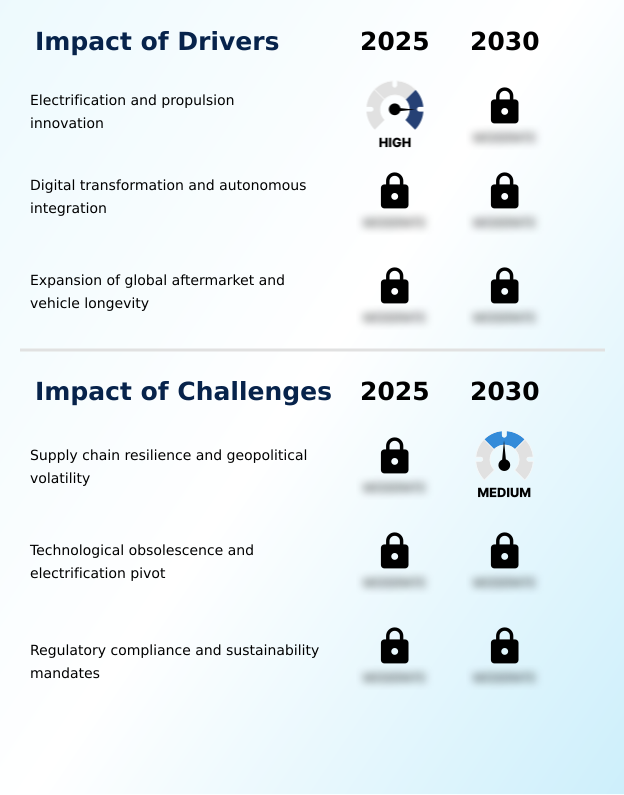

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the auto parts sector is increasingly influenced by long-term technological trajectories. The impact of electrification on powertrain components is forcing a complete re-evaluation of legacy manufacturing assets, with a clear pivot toward components for electric and hybrid systems. Simultaneously, the role of ADAS in automotive electronics growth is accelerating demand for high-performance computing and sensor fusion technologies.

- As this complexity grows, advancements in electric vehicle battery thermal management are becoming critical for ensuring safety and performance, creating a new sub-market for specialized cooling and monitoring systems. Businesses are also exploring the benefits of lightweight materials in chassis design to offset battery weight and improve vehicle efficiency.

- This is compounded by challenges in automotive semiconductor supply chains, which are pushing companies toward nearshoring strategies for automotive supply chain resilience to ensure production continuity.

- In the aftermarket, which has seen its share of the market grow by over 5% in some segments, the focus is on digital twin applications in auto parts production and the deployment of advanced diagnostics to service these technologically dense vehicles. Furthermore, the push for sustainability is driving innovation in sustainable materials for automotive interior manufacturing.

What are the key market drivers leading to the rise in the adoption of Auto Parts Industry?

- The primary market driver is the continuous innovation in vehicle electrification and advanced propulsion systems.

- Market growth is primarily propelled by the widespread adoption of electrification and advanced driver assistance systems (ADAS). The transition to electric propulsion systems fuels demand for innovative battery management systems, power inverters, and thermal management solutions.

- Concurrently, the integration of ADAS is becoming standard, requiring a complex array of high-resolution cameras, radar modules, and ultrasonic sensors.

- This shift has dramatically increased the electronic content in vehicles, with the number of electronic control units rising from fewer than 20 to over 100 in high-end models.

- The increasing average age of the global vehicle fleet also provides a steady tailwind for the aftermarket, where predictive maintenance analytics and digital diagnostic platforms are becoming essential tools for service.

What are the market trends shaping the Auto Parts Industry?

- The market is increasingly influenced by the proliferation of software-defined vehicle architectures. This trend is compelling a shift toward centralized computing and modular hardware components.

- Key trends are reshaping the auto parts market, emphasizing digitalization and sustainability. The proliferation of software-defined vehicle architectures is driving demand for high-speed data networks and modular vehicle electronics, enabling features like over-the-air (OTA) updates.

- This shift is turning vehicles into upgradable platforms, with one report indicating that 84% of vehicles in a major region are now out of warranty, creating a vast market for advanced aftermarket solutions. Concurrently, smart manufacturing and Industry 4.0 technologies are optimizing production lines.

- The adoption of circular economy principles is also gaining traction, with some companies successfully commercializing tires made from 65% sustainable materials, highlighting a significant move toward eco-friendly product lifecycles and recycled plastics.

What challenges does the Auto Parts Industry face during its growth?

- A key challenge facing the market is ensuring supply chain resilience amid persistent geopolitical volatility.

- The market faces significant challenges related to supply chain stability and rapid technological obsolescence. Geopolitical volatility has exposed the fragility of just-in-time logistics, forcing a strategic shift toward near-shoring supply chains and friend-shoring strategies to secure the availability of critical semiconductor components. This restructuring requires substantial capital investment.

- Simultaneously, the pivot to electrification is rendering decades of investment in internal combustion engine technology obsolete, requiring a massive re-allocation of resources toward mastering high-voltage battery chemistry and power electronics.

- The regulatory landscape adds another layer of complexity, as mandates for carbon capture technology and sustainable material sourcing increase compliance costs, often with a cost-to-benefit ratio that varies significantly across jurisdictions.

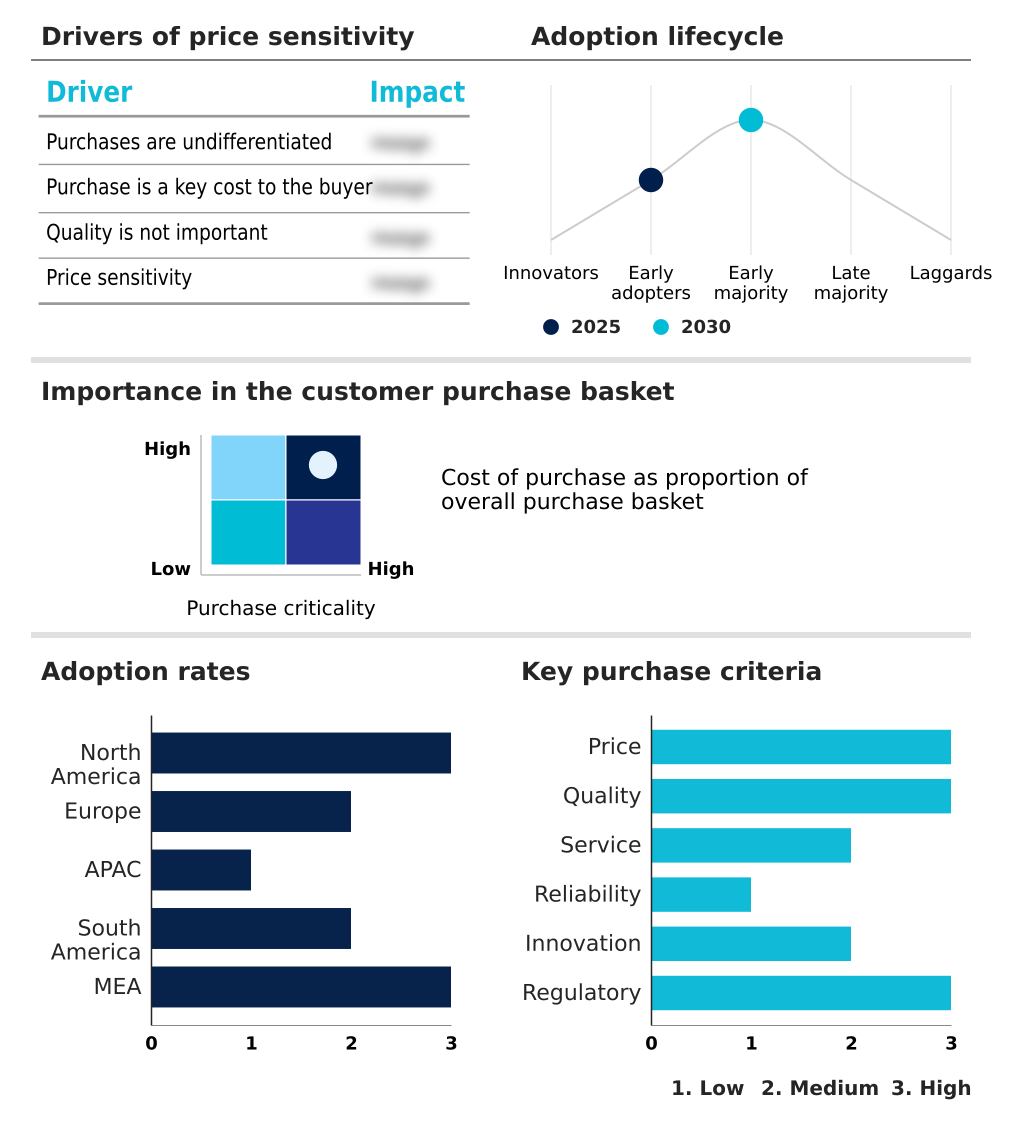

Exclusive Technavio Analysis on Customer Landscape

The auto parts market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the auto parts market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Auto Parts Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, auto parts market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AISIN Corp. - Analysis indicates a portfolio centered on advanced drivetrain systems and core automotive components, targeting vehicle performance and efficiency through integrated engineering solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN Corp.

- Aptiv PLC

- Autoliv Inc.

- BorgWarner Inc.

- Continental AG

- Dana Inc.

- DENSO Corp.

- Forvia SE

- Gestamp Automocion SA

- Lear Corp.

- Magna International Inc.

- MAHLE GmbH

- Marelli Holdings Co. Ltd.

- Robert Bosch GmbH

- Schaeffler AG

- Sumitomo Electric Industries

- Tenneco Inc.

- Valeo SA

- Yazaki Corp.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Auto parts market

- In August 2025, Bridgestone Corporation announced the commercialization of a new tire line incorporating 65% sustainable materials, including natural rubber from guayule shrubs and silica derived from rice husk waste.

- In May 2025, Siemens AG implemented an advanced AI-powered digital twin solution for a tier-one supplier, using real-time sensor data to adjust casting processes and reduce structural micro-defects by 15%.

- In April 2025, Toyota Motor Corporation initiated a decentralized micro-hub strategy in Southeast Asia to localize the sourcing of semiconductor components and mitigate the impact of global logistics disruptions.

- In February 2025, Robert Bosch GmbH launched a comprehensive reskilling program in Germany to transition thousands of mechanical engineers into roles focused on electric motor production and software-defined vehicle architecture.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Auto Parts Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.3% |

| Market growth 2026-2030 | USD 384.7 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.1% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, South Africa, UAE, Saudi Arabia, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The auto parts market is in a state of strategic realignment, where portfolio simplification and technological investment are paramount. The industry is moving beyond traditional mechanical components toward integrated systems defined by software and advanced electronics. This pivot requires substantial capital expenditure in new technologies, particularly in electric propulsion systems and autonomous driving technologies, areas where R&D spending is intensifying.

- Established players are focusing on core competencies like drivetrain systems, advanced wiring systems, braking systems, and automotive tires, while simultaneously building capabilities in next-generation fields such as high-performance semiconductors and battery management systems. The integration of high-resolution cameras, ultrasonic sensors, and radar modules is now standard, reflecting a market where vehicle intelligence is a primary differentiator.

- For instance, the adoption of advanced digital tools has enabled some manufacturers to improve defect detection by 15%, showcasing how operational efficiency is becoming a key competitive lever in this evolving landscape.

What are the Key Data Covered in this Auto Parts Market Research and Growth Report?

-

What is the expected growth of the Auto Parts Market between 2026 and 2030?

-

USD 384.7 billion, at a CAGR of 3.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (OEM, and Aftermarket), Distribution Channel (Offline, and Online), Type (Electrical and electronics, Driveline and powertrain, Interior and exterior, Body and chassis, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Electrification and propulsion innovation, Supply chain resilience and geopolitical volatility

-

-

Who are the major players in the Auto Parts Market?

-

AISIN Corp., Aptiv PLC, Autoliv Inc., BorgWarner Inc., Continental AG, Dana Inc., DENSO Corp., Forvia SE, Gestamp Automocion SA, Lear Corp., Magna International Inc., MAHLE GmbH, Marelli Holdings Co. Ltd., Robert Bosch GmbH, Schaeffler AG, Sumitomo Electric Industries, Tenneco Inc., Valeo SA, Yazaki Corp. and ZF Friedrichshafen AG

-

Market Research Insights

- Market dynamics are increasingly shaped by the convergence of sustainability and technology. The adoption of circular economy principles is evident, with some manufacturers now producing tires from over 65% sustainable materials, a significant shift from previous benchmarks.

- Concurrently, the aftermarket is supported by a large volume of out-of-warranty vehicles, with one major region reporting that such vehicles constitute 84% of the total fleet. This longevity drives consistent demand for remanufacturing processes and advanced diagnostic platforms.

- The move toward software-defined vehicle architectures is creating demand for new business models centered on over-the-air (OTA) updates and feature subscriptions, compelling suppliers to integrate advanced driver assistance systems (ADAS) and vehicle-to-everything (V2X) communication capabilities into their core offerings. This strategic pivot ensures relevance in an industry where digital features are becoming as critical as mechanical performance.

We can help! Our analysts can customize this auto parts market research report to meet your requirements.

RIA -

RIA -