ITSM Market in Latin America Size 2024-2028

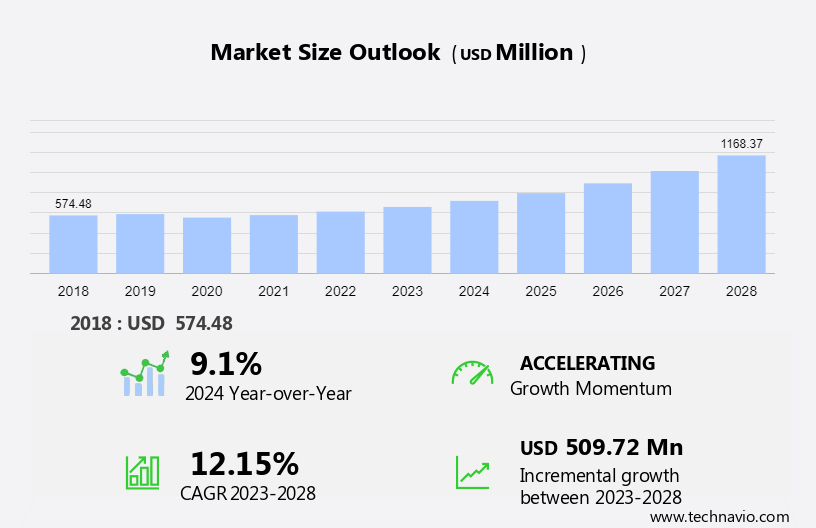

The ITSM market in Latin America size is forecast to increase by USD 509.72 million at a CAGR of 12.15% between 2023 and 2028. The market is experiencing significant growth due to the increasing demand for effective enterprise IT service incident and problem management. Advanced technologies, such as artificial intelligence and automation, are gaining popularity, revolutionizing the way IT services are delivered. Additionally, the accessibility of high-quality data is driving the market, enabling organizations to make informed decisions and improve their IT service management capabilities. These trends are expected to continue, with the market expected to grow at a steady pace in the coming years. Effective IT service management is crucial for businesses to maintain productivity and competitiveness in today's digital landscape. The adoption of advanced technologies and access to high-quality data are key enablers, enabling organizations to streamline their IT operations and deliver superior services to their customers.

The Latin American market is experiencing significant growth due to the increasing adoption of cloud solutions and automation in IT organizations. Cloud-based ITSM tools are becoming increasingly popular as they offer cost reduction, data gathering, and flexibility to enterprises. The recession and procurement strategies have led IT teams to prioritize cloud computing and IT services, resulting in a rise in demand for ITSM software. Cybersecurity concerns are also driving the market, as IT infrastructure becomes more complex and remote working becomes the new norm in the digital transformation era. ITSM tools help IT organizations maintain reliability concerns and adhere to quality standards, ensuring service level agreements are met.

Furthermore, the hybrid workplace model further highlights the need for efficient ITSM software to support internal IT support and applications. IT industry dynamics continue to shape the ITSM market, with enterprises seeking cost-effective solutions to manage their IT services and applications. ITSM tools play a crucial role in addressing cybersecurity concerns and ensuring business continuity in a rapidly evolving technological landscape.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Deployment

- Cloud

- On-premises

- Application

- Configuration management

- IT asset management and IT service desk

- Availability and performance management

- Network management

- Others

- Geography

- Latin America

By Deployment Insights

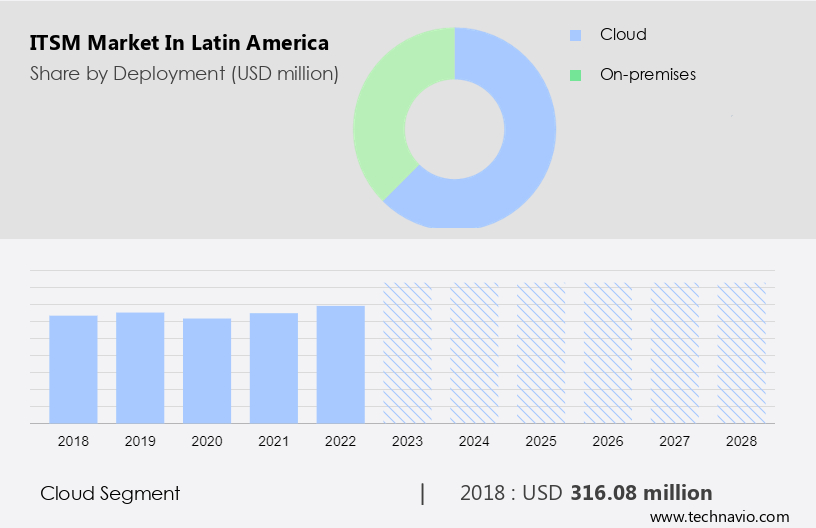

The Cloud segment is estimated to witness significant growth during the forecast period. The IT service management (ITSM) market in Latin America is experiencing notable growth in the cloud segment. ITSM is a process-driven approach to delivering, managing, and supporting IT services for enterprises. The adoption of cloud computing technologies and the demand for advanced IT service management capabilities are driving the popularity of cloud-based ITSM solutions in the region. Cost reduction and operational efficiency are key factors motivating organizations to migrate from traditional on-premises ITSM implementations to cloud-based alternatives. Cloud solutions offer flexibility, eliminating the need for significant upfront investments in IT infrastructure and maintenance costs. Moreover, the current economic recession has intensified the focus on cost savings and efficiency in IT procurement strategies.

Furthermore, cybersecurity concerns and reliability are essential considerations for IT organizations in the Latin American market. Cloud-based ITSM solutions provide enhanced security features and unified visibility, addressing these concerns. The hybrid workplace model and remote working have become increasingly common due to digital transformation initiatives. ITSM tools enable IT teams to provide internal support and manage applications effectively, ensuring service level agreements are met. Telecom businesses are significant contributors to the Latin American ITSM market, with infrastructure setup, human resources, and content mobilization being key areas of focus. Cloud-based ecosystems, including social media, smart devices, and 5G subscriptions, are transforming the IT industry dynamics. ITSM software plays a crucial role in managing these complexities and ensuring data capture for informed decision-making.

Get a glance at the market share of various segments Request Free Sample

The cloud segment was valued at USD 316.08 million in 2018 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Latin America ITSM Market Driver

Effective enterprise IT service incident and problem management is the key driver of the market. In the dynamic IT industry landscape of Latin America, ITSM tools play a pivotal role in enhancing operational efficiency and ensuring reliability for IT organizations. Amidst the ongoing digital transformation and the shift towards remote working, cloud-based ITSM solutions have gained significant traction. These solutions offer automation capabilities, enabling cost reduction through data gathering and streamlined procurement strategies. Cybersecurity concerns remain a top priority, necessitating stringent quality standards and service-level agreements. Telecom businesses and other enterprises are increasingly adopting cloud computing and hybrid workplace models, requiring unified visibility into IT infrastructure and applications. ITSM software facilitates this need, providing internal IT support with intelligent incident routing and escalation triggers.

Furthermore, the integration of cloud solutions, social media, smart devices, and 5G subscriptions further enhances the capabilities of ITSM tools. Human resources and infrastructure setups also benefit from the data capture and content mobilization features of these systems. Amidst the economic uncertainties brought about by the recession and the evolving IT industry dynamics, ITSM market growth in Latin America remains strong.

Latin America ITSM Market Trends

The advent of advanced technologies is the upcoming trend in the market. In Latin America, the ITSM market is experiencing significant growth due to the increasing adoption of cloud solutions and automation in IT services. Cloud-based ITSM tools are becoming increasingly popular among enterprises as they offer cost reduction, reliability, and quality standards that meet service level agreements. The region's IT industry dynamics are being influenced by cybersecurity concerns, procurement strategies, and the shift towards cloud computing. The COVID-19 recession has accelerated the digital transformation trend, leading to an increase in remote working and the adoption of hybrid workplace models. IT teams are relying on ITSM software to ensure internal IT support and operational efficiency.

Furthermore, telecom businesses are also investing in infrastructure setup and unified visibility to cater to the growing demand for 5G subscriptions, smart devices, and content mobilization. Cloud-based ecosystems, social media, and AI-powered technologies are transforming the way IT services are delivered. ITSM tools are being integrated with ML, predictive analytics, blockchain, Big Data, IoT, AR, and VR to provide advanced features such as automatic task and request categorization, intelligent incident routing, proactive incident detection, and performance optimization. Human resources are also leveraging these tools to ensure operational efficiency and maintain unified visibility across IT infrastructure. Despite these advancements, there are challenges such as data capture and security concerns that need to be addressed.

Moreover, enterprises must ensure that their ITSM tools are compatible with on-premise systems and can provide reliable and secure data transfer. Telecommunication giants and other enterprises must also prioritize cybersecurity measures to protect their IT infrastructure and applications from potential threats. Overall, the market is poised for growth as enterprises continue to adopt advanced technologies to streamline their IT services and improve operational efficiency.

Latin America ITSM Market Challenge

The accessibility of high-quality data is a key challenge affecting market growth. In the IT industry dynamics of Latin America, the adoption of ITSM tools is gaining momentum due to the increasing need for operational efficiency, reliability concerns, and quality standards in IT services. Cloud solutions have become a preferred choice for IT organizations due to cost reduction and flexibility benefits. However, the deployment of Cloud based ITSM solutions faces challenges such as cybersecurity concerns, procurement strategies, and data gathering. With the rise of remote working and digital transformation, IT teams require unified visibility into IT infrastructure, applications, and internal IT support. The large volume of data generated by businesses and the disparate nature of data across departments pose significant challenges.

Furthermore, relevant data supporting ITSM tools are often distributed across databases, repositories, systems, and processes, making it difficult for ITSM software to access them. Cloud computing and hybrid workplace models have further complicated data access, as data may be spread across on-premise and cloud-based ecosystems. Moreover, the increasing use of social media, smart devices, and 5G subscriptions have led to an exponential increase in data generation. Telecom businesses, in particular, face unique challenges in setting up infrastructure and managing human resources to capture and analyze this data. ITSM market growth is also influenced by the need to meet service level agreements and address cybersecurity concerns in the context of cloud computing and automation.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Bitrix Inc.: The company offers ITSM that includes change management, configuration management, and incident management.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BMC Software Inc.

- Broadcom Inc.

- Citrix Systems Inc.

- Freshworks Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise Co.

- IFS World Operations AB

- International Business Machines Corp.

- InvGate

- Ivanti Software Inc.

- Microsoft Corp.

- Oracle Corp.

- SAP SE

- ServiceNow Inc.

- SolarWinds Corp.

- SysAid Technologies Ltd

- Tata Consultancy Services Ltd.

- Zoho Corp. Pvt. Ltd.

- Zendesk Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The Latin America market is experiencing significant growth, driven by the increasing adoption of cloud solutions and IT organizations' shift towards cloud-based ITSM tools for automation and operational efficiency. The recession and procurement strategies have led IT teams in enterprises to prioritize cost reduction and data gathering, making cloud computing an attractive option. Cybersecurity concerns remain a top priority, and ITSM tools are essential for ensuring reliability, quality standards, and adherence to service level agreements. The IT industry dynamics in Latin America are influenced by the hybrid workplace model, with remote working becoming increasingly common.

Furthermore, digital transformation initiatives have led to the implementation of ITSM software for internal IT support, enabling unified visibility across cloud-based ecosystems. Telecom businesses are also investing in ITSM tools to manage their IT services, applications, and infrastructure setup, addressing human resources challenges and enhancing customer experience. Cloud-based ITSM solutions offer advantages such as data capture, content mobilization, and integration with smart devices, social media, and 5G subscriptions. Telecommunication giants are leading the way in adopting these solutions to provide reliable and efficient IT services, meeting the demands of their customers in the digital age.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 12.15% |

|

Market growth 2024-2028 |

USD 509.72 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.1 |

|

Key companies profiled |

Bitrix Inc., BMC Software Inc., Broadcom Inc., Citrix Systems Inc., Freshworks Inc., Fujitsu Ltd., Hewlett Packard Enterprise Co., IFS World Operations AB, International Business Machines Corp., InvGate, Ivanti Software Inc., Microsoft Corp., Oracle Corp., SAP SE, ServiceNow Inc., SolarWinds Corp., SysAid Technologies Ltd, Tata Consultancy Services Ltd., Zoho Corp. Pvt. Ltd., and Zendesk Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Latin America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -