Last Mile Delivery Market Size 2026-2030

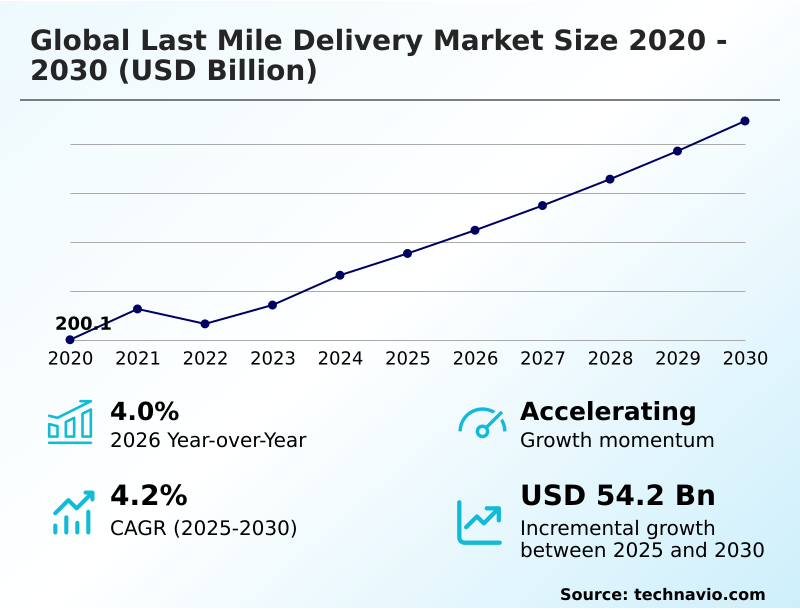

The Last Mile Delivery Market size was valued at USD 235.4 billion in 2025, growing at a CAGR of 4.2% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 43.2% growth during the forecast period.

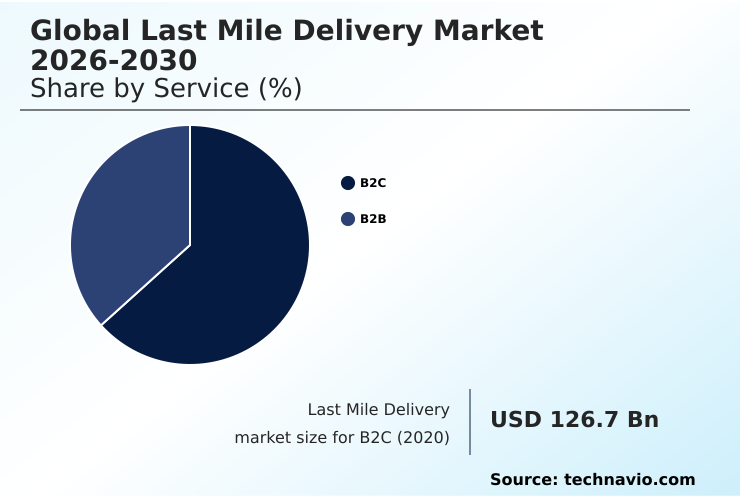

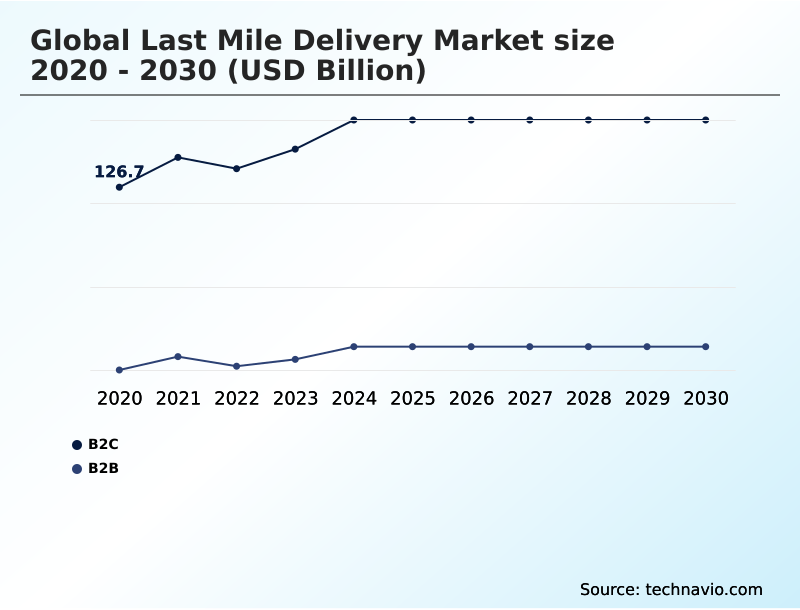

- By Service - B2C segment was valued at USD 146.3 billion in 2024

- By Application - FMCG segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 89.5 billion

- Market Future Opportunities 2025-2030: USD 54.2 billion

- CAGR from 2025 to 2030 : 4.2%

Market Summary

- The last mile delivery market is defined by a relentless focus on optimizing the final, most expensive leg of the supply chain, which can account for over 50% of total shipping costs. A primary driver is the explosive growth of e-commerce, compelling logistics providers to meet consumer demands for faster, more transparent service.

- For example, a large retailer implementing a network of micro-fulfillment centers can reduce average delivery times by 30% and cut associated transportation costs by 15% by positioning inventory closer to urban customers. However, the industry faces significant operational challenges.

- Urban congestion slows down deliveries, while labor shortages during peak seasons can increase wage costs by up to 20%, directly impacting profitability. Success in this market requires a delicate balance of speed, cost-efficiency, and technological innovation to manage complex urban logistics and fluctuating consumer demand.

What will be the Size of the Last Mile Delivery Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Last Mile Delivery Market Segmented?

The last mile delivery industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Service

- B2C

- B2B

- Application

- FMCG

- E-commerce

- Retails

- Others

- Vehicle type

- Vans and trucks

- Two-wheelers

- Drones

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

How is the Last Mile Delivery Market Segmented by Service?

The b2c segment is estimated to witness significant growth during the forecast period.

The business-to-consumer segment accounts for over 65% of last mile delivery activity, driven by evolving e-commerce fulfillment demands.

This sector is characterized by a high volume of small, individual shipments where the customer experience is paramount, directly impacting brand loyalty and repeat purchases.

In contrast to B2B, which prioritizes scheduled, bulk deliveries, B2C success hinges on offering flexible delivery windows and real-time tracking.

Logistics firms find that implementing predictive analytics in this segment improves on-time delivery rates by up to 18%, a significant enhancement over the B2B sector's typical performance.

This focus on individual consumer satisfaction requires sophisticated delivery management software and a resilient logistics network design to handle demand fluctuations and returns management efficiently.

The B2C segment was valued at USD 146.3 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Last Mile Delivery market is rising in the leading region?

APAC is estimated to contribute 43.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Last Mile Delivery Market demand is rising in APAC Request Free Sample

The geographic landscape of the last mile delivery market is characterized by significant regional disparities in growth and technological adoption.

APAC is the fastest-growing region, with a projected CAGR of 4.8%, contributing over 43% of the market's incremental growth, substantially outpacing Europe's 3.8% CAGR.

This surge is led by China and India, where high population density and rapid e-commerce penetration create immense parcel volumes.

In contrast, North America, led by the US with a market value over three times that of China's, is a more mature market focused on technological innovation like autonomous delivery and predictive analytics.

European markets prioritize sustainable logistics and urban logistics solutions, with a higher adoption of electric vehicles and cargo bikes, reflecting stricter environmental regulations compared to other regions.

What are the key Drivers, Trends, and Challenges in the Last Mile Delivery Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Optimizing the final stage of the supply chain requires a multi-faceted approach, where last mile delivery cost optimization is a primary objective. Companies are finding that the implementation of advanced last mile delivery software for e-commerce can reduce operational expenses by up to 15% through better route planning and resource allocation.

- However, significant challenges in urban last mile delivery persist, including traffic congestion and regulatory hurdles, which can inflate costs per delivery by over 20% compared to suburban areas.

- To counteract this, there is a growing investment in sustainable last mile delivery solutions, such as electric vehicle fleets, which not only reduce carbon emissions but can also lower fuel and maintenance costs over their lifecycle.

- The deployment of autonomous robots in last mile delivery is also gaining traction in controlled environments, with pilot programs demonstrating the potential to handle up to 30% of deliveries in dense residential complexes, further addressing labor shortages and enhancing efficiency.

What are the key market drivers leading to the rise in the adoption of Last Mile Delivery Industry?

- The rapid growth of the global e-commerce industry is a primary driver for the last mile delivery market.

- The continued expansion of the global e-commerce industry, which now represents over 20% of total retail spending, is the principal driver for the last mile delivery market.

- This structural shift has created a sustained increase in demand for rapid and reliable e-commerce fulfillment networks. Consumers increasingly expect same-day delivery and seamless returns management, which intensifies pressure on logistics network design.

- This demand is amplified by the premiumization of delivery services, where specialized handling for high-value goods can support profit margins up to 15% higher than standard deliveries.

- Consequently, companies are heavily investing in hyperlocal delivery infrastructure, including micro-fulfillment centers, to position inventory closer to consumers and meet heightened service level agreements.

What are the market trends shaping the Last Mile Delivery Industry?

- A strong focus on technological advances is a key trend shaping the market. This includes the adoption of AI for route optimization and automation in delivery services.

- Technological advancement is fundamentally reshaping last mile delivery, with firms adopting AI-driven route optimization to reduce driven miles by 10% and achieve 98% on-time delivery accuracy. This trend extends to warehouse automation, where automated sorting and picking systems are increasing throughput by over 30% compared to manual processes.

- The integration of delivery drones and autonomous robots, while nascent, shows promise in reducing labor costs and delivery times in controlled environments. For instance, commercial autonomous robots are now serving over 1.6 million residents in select urban areas.

- Furthermore, data analytics and machine learning are enabling predictive analytics for demand forecasting, allowing for smarter resource allocation and enhanced supply chain visibility, ultimately improving the overall customer experience through greater transparency and reliability.

What challenges does the Last Mile Delivery Industry face during its growth?

- Operational challenges, including urban congestion and labor shortages, represent a significant constraint on the growth of last mile delivery companies.

- Operational inefficiencies present a primary challenge, with urban congestion and limited parking increasing delivery times by as much as 25% in metropolitan centers. This directly impacts fleet management and route optimization, elevating fuel and labor costs.

- Last mile carriers also face significant risks from package theft and damage, which can account for up to 5% of total delivery costs due to replacements and claims processing. These issues erode profitability and customer trust. The introduction of alternative models like parcel lockers and crowdsourced delivery adds competitive pressure, forcing traditional providers to innovate.

- Failure to adopt efficient delivery management software and sustainable logistics practices can lead to a 10% decrease in operational margins compared to more agile competitors.

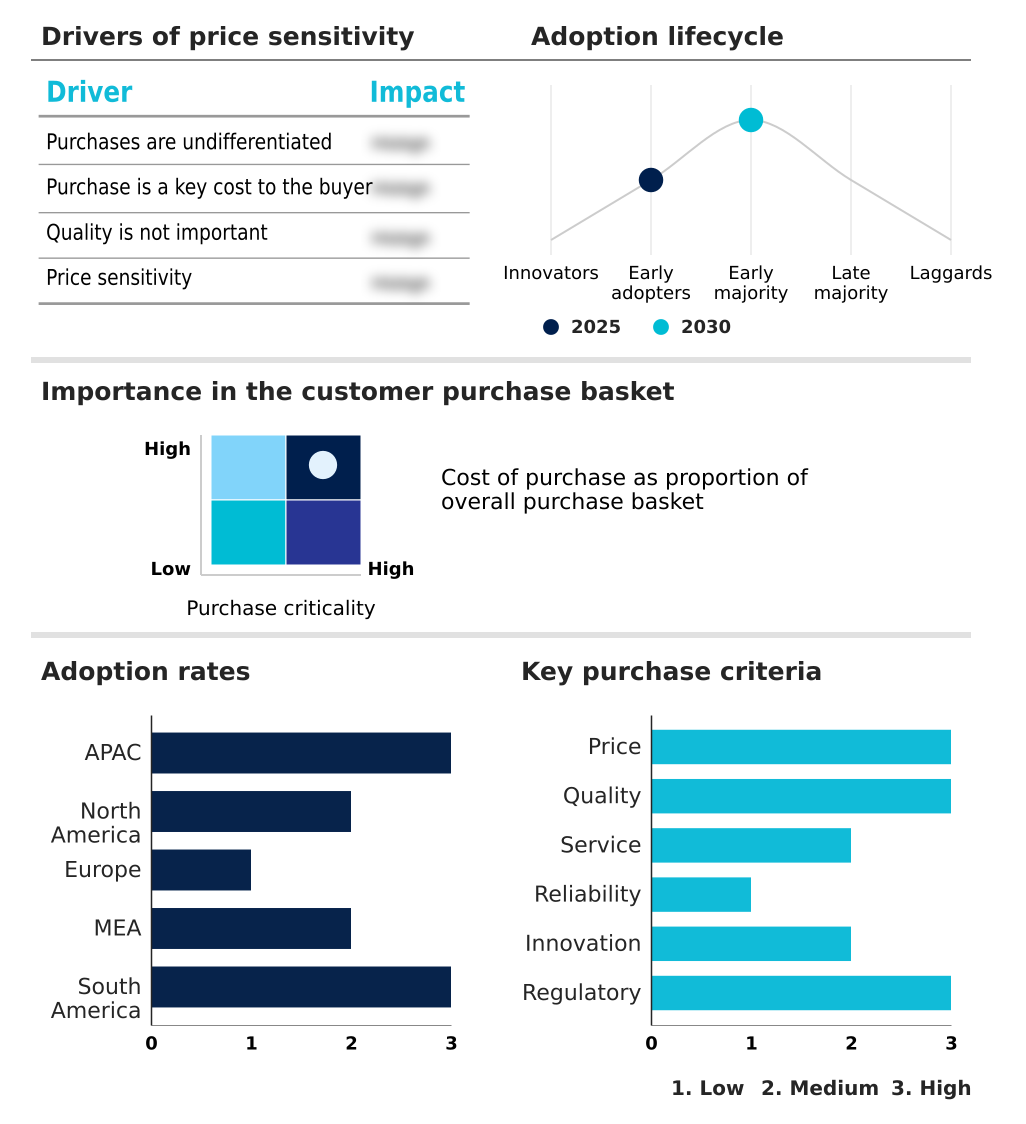

Exclusive Technavio Analysis on Customer Landscape

The last mile delivery market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the last mile delivery market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Last Mile Delivery Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, last mile delivery market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

CMA CGM Group - Analyst viewpoint: Provides end-to-end logistics solutions, focusing on parcel delivery, e-commerce fulfillment, and specialized courier services to meet diverse residential and commercial needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CMA CGM Group

- Deutsche Bahn AG

- Deutsche Post AG

- DSV AS

- FarEye Technologies Pvt. Ltd.

- FedEx Corp.

- FM Logistic

- Honeywell International Inc.

- Infosys Ltd.

- JB Hunt Transport Services

- Kuehne Nagel Management AG

- Nippon Express Holdings Inc.

- Royal Mail Group Ltd.

- Schneider Electric SE

- SNCF Group

- United Parcel Service Inc.

- Werner Enterprises Inc.

- XPO Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Air Freight and Logistics industry, the sustained expansion of cross-border e-commerce has increased parcel volumes by over 15%, creating a heightened demand for sophisticated last mile carrier networks capable of handling complex customs and delivery window requirements.

- Stringent environmental regulations, mandating a 20% reduction in urban transport emissions in key economic zones, are compelling the adoption of electric vehicles and cargo bikes within last mile delivery fleets to ensure compliance and market access.

- The proliferation of third-party logistics (3PL) integration and outsourcing models allows retailers to improve supply chain visibility by up to 25%, driving partnerships with specialized last mile delivery providers to manage final-leg fulfillment and enhance the customer experience.

- Modernization of airport terminals and cargo handling facilities, which has increased ground processing speed by approximately 10%, necessitates corresponding efficiency gains in the final delivery stage, fueling investment in automated sorting and dynamic routing for last mile operations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Last Mile Delivery Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.2% |

| Market growth 2026-2030 | USD 54.2 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The last mile delivery ecosystem is a complex interplay of stakeholders, with technology providers offering route optimization and delivery management software that improves efficiency by up to 25%. Logistics carriers, from global giants to hyperlocal delivery services, utilize this technology to execute deliveries.

- These carriers interact with a flexible workforce, including gig economy drivers, who now handle an estimated 30% of on-demand deliveries in urban areas. E-commerce platforms and omnichannel retail businesses are the primary customers, driving demand and shaping service level agreements. Supporting this are infrastructure players providing parcel lockers and dark stores.

- The entire system is governed by evolving regulations on emissions and labor, influencing fleet management and operational models.

What are the Key Data Covered in this Last Mile Delivery Market Research and Growth Report?

-

What is the expected growth of the Last Mile Delivery Market between 2026 and 2030?

-

The Last Mile Delivery Market is expected to grow by USD 54.2 billion during 2026-2030, registering a CAGR of 4.2%. Year-over-year growth in 2026 is estimated at 4.0%%. This acceleration is shaped by growing global e-commerce industry, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Service (B2C, and B2B), Application (FMCG, E-commerce, Retails, and Others), Vehicle Type (Vans and trucks, Two-wheelers, and Drones) and Geography (APAC, North America, Europe, Middle East and Africa, South America). Among these, the B2C segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, Middle East and Africa and South America. APAC is estimated to contribute 43.2% to market growth during the forecast period. Country-level analysis includes China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is growing global e-commerce industry, which is accelerating investment and industry demand. The main challenge is operational challenges for last mile delivery companies, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Last Mile Delivery Market?

-

Key vendors include CMA CGM Group, Deutsche Bahn AG, Deutsche Post AG, DSV AS, FarEye Technologies Pvt. Ltd., FedEx Corp., FM Logistic, Honeywell International Inc., Infosys Ltd., JB Hunt Transport Services, Kuehne Nagel Management AG, Nippon Express Holdings Inc., Royal Mail Group Ltd., Schneider Electric SE, SNCF Group, United Parcel Service Inc., Werner Enterprises Inc. and XPO Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the last mile delivery market features intense rivalry, with global incumbents like Deutsche Post AG, FedEx Corp., and United Parcel Service Inc. commanding significant share but facing pressure from agile tech-driven startups. These established players leverage dense logistics network design and scale to handle massive parcel volumes, yet the market's overall fragmentation allows for niche competition.

- Vendor focus is increasingly on technology, with investments in delivery management software and autonomous delivery leading to a 10-15% improvement in operational efficiency. The market is projected to see a year-over-year growth of 4.0%, primarily fueled by the e-commerce boom in APAC, which accounts for 43.2% of the incremental growth.

- This dynamic forces all players to innovate continuously to manage costs and meet rising customer expectations for speed and sustainability.

We can help! Our analysts can customize this last mile delivery market research report to meet your requirements.

RIA -

RIA -