Maritime AI Market Size 2025-2029

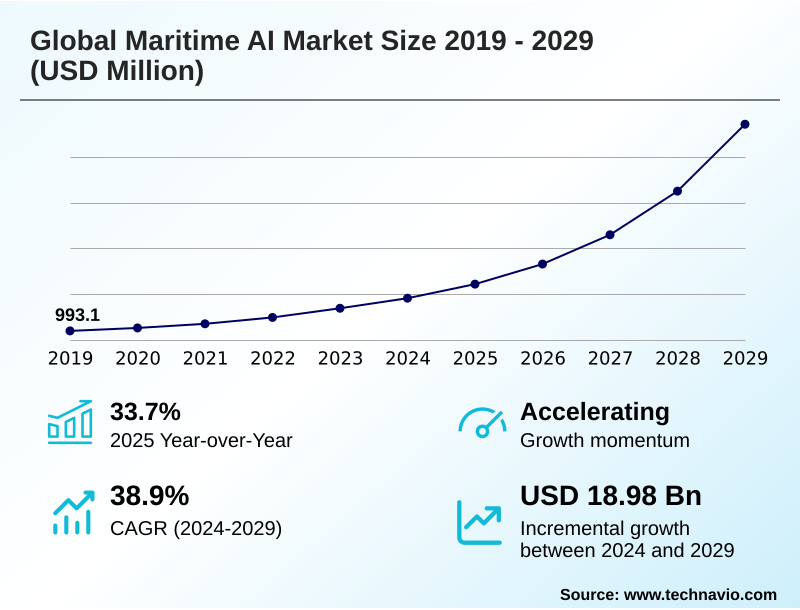

The maritime ai market size is valued to increase by USD 18.98 billion, at a CAGR of 38.9% from 2024 to 2029. Imperative for operational efficiency and cost reduction will drive the maritime ai market.

Major Market Trends & Insights

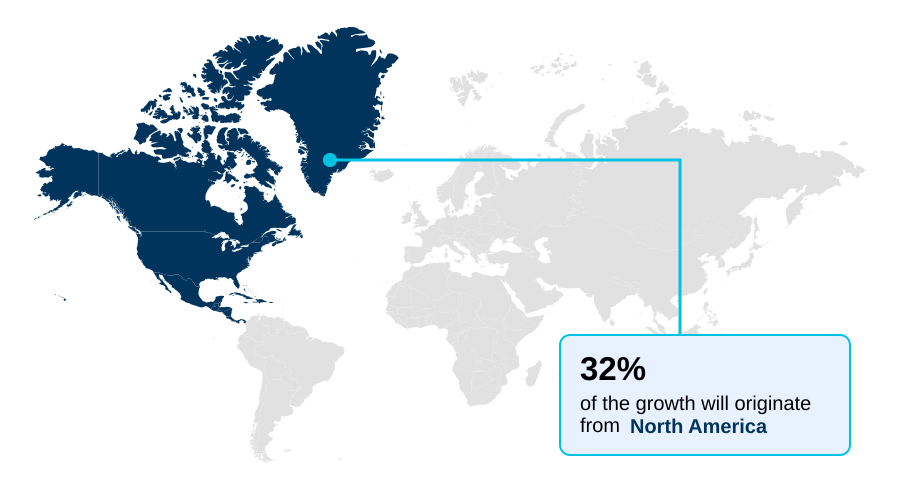

- North America dominated the market and accounted for a 32.2% growth during the forecast period.

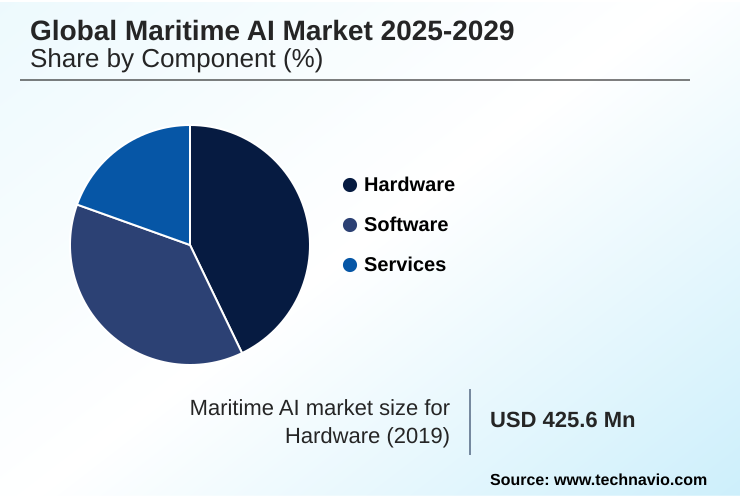

- By Component - Hardware segment was valued at USD 1.46 billion in 2023

- By Technology - Machine learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 22.54 billion

- Market Future Opportunities: USD 18.98 billion

- CAGR from 2024 to 2029 : 38.9%

Market Summary

- The maritime AI market is undergoing a significant transformation, driven by the convergence of economic pressures and technological advancements. A primary catalyst is the relentless pursuit of operational efficiency, compelling operators to adopt AI-powered vessel performance tools and predictive maintenance models to reduce expenditures and enhance asset reliability.

- This shift is further accelerated by stringent environmental mandates like the Carbon Intensity Indicator (CII) compliance, which necessitates the use of sophisticated AI-driven route optimization and machine learning fuel management to minimize emissions.

- For instance, a fleet operator can leverage a voyage optimization platform that synthesizes real-time weather data, vessel hydrodynamics, and port schedules to chart the most fuel-efficient course, thereby cutting costs and improving its environmental rating.

- Concurrently, trends such as the development of maritime digital twin simulation and the move toward edge computing for vessels are enabling higher levels of automation and real-time decision-making. However, the industry grapples with challenges related to maritime data standardization and the high initial capital required for systems built on ruggedized onboard computing and high-fidelity sensor integration.

- Overcoming these hurdles is essential for realizing the full potential of AI-powered fleet management and moving closer to widespread autonomous shipping.

What will be the Size of the Maritime AI Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Maritime AI Market Segmented?

The maritime ai industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

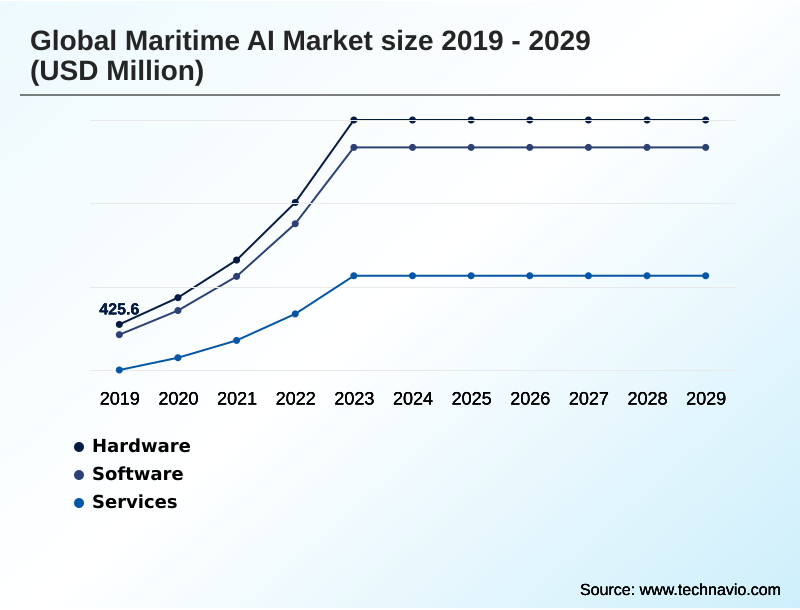

- Component

- Hardware

- Software

- Services

- Technology

- Machine learning

- Computer vision

- Robotics and autonomous systems

- Data analytics

- Others

- Application

- Navigation and route optimization

- Predictive maintenance

- Port operations and management

- Autonomous shipping

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- The Netherlands

- UK

- APAC

- China

- Japan

- South Korea

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The market is segmented by several core components, with hardware forming the essential physical layer for most maritime AI applications. This segment, crucial for enabling autonomous shipping solutions, includes a diverse array of sensors, onboard computers, and networking equipment.

A key area of development is edge computing for vessels, which supports real-time data processing for an autonomous navigation system. The adoption of smart port technologies also drives demand for hardware that facilitates maritime supply chain optimization.

The trend towards developing a comprehensive maritime digital twin simulation, supported by sophisticated hardware, is a testament to the industry's investment in AI for maritime safety.

These systems, often managed from a remote operation center (ROC), leverage computer vision collision avoidance and vessel performance analytics.

Effective deployment of a voyage optimization platform can lead to emission reductions of up to 15%, highlighting the tangible benefits of these decarbonization AI tools and predictive maintenance model integrations.

The Hardware segment was valued at USD 1.46 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Maritime AI Market Demand is Rising in North America Get Free Sample

The geographic landscape is characterized by varied adoption rates, with North America leading in investment, contributing over 32% of the market's incremental growth. The region's focus is on enhancing fleet operational efficiency and deploying advanced maritime surveillance AI.

In contrast, Europe emphasizes regulatory compliance, driving demand for machine learning fuel management and AI-based fuel optimization tools. APAC is a hub for shipbuilding and smart port development, focusing on data analytics for port logistics and AI in port management.

These advanced applications rely on ruggedized onboard computing and high-fidelity sensor integration.

Innovations in sensor fusion for situational awareness and LiDAR object detection are critical across all regions, underpinning remote vessel operations and improvements in AI-powered vessel performance, with some ports achieving a 20% increase in container handling speed.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of artificial intelligence is fundamentally reshaping maritime operations, with a strong focus on tangible outcomes. A key application is using AI to reduce maritime emissions, where advanced algorithms for machine learning for ship fuel optimization are becoming essential tools for both cost savings and regulatory adherence.

- The benefits of AI for predictive maintenance on ships are equally compelling, shifting asset management from a reactive to a proactive model and significantly reducing costly unscheduled downtime. In terms of safety, the development of systems for autonomous navigation in congested waterways and computer vision for maritime object detection directly addresses the challenge of human error.

- Companies are increasingly asking about the ROI of AI in the shipping industry, and evidence shows that integrated platforms deliver compounding value. For instance, combining AI-powered port operations management with AI solutions for IMO CII compliance can improve a vessel’s charterability rating by more than a full grade compared to vessels using only basic routing software.

- The creation of a digital twin for vessel lifecycle management represents a holistic approach, enabling simulation and optimization from design to decommissioning. The architectural debate over edge computing vs cloud for ships continues, with hybrid models emerging as a practical solution. The establishment of remote operation centers for autonomous ships marks a significant step toward the future of uncrewed vessels.

- Furthermore, AI for maritime surveillance and security is enhancing maritime situational awareness, while the broader AI role in decarbonizing maritime sector is driving innovation across the entire value chain.

What are the key market drivers leading to the rise in the adoption of Maritime AI Industry?

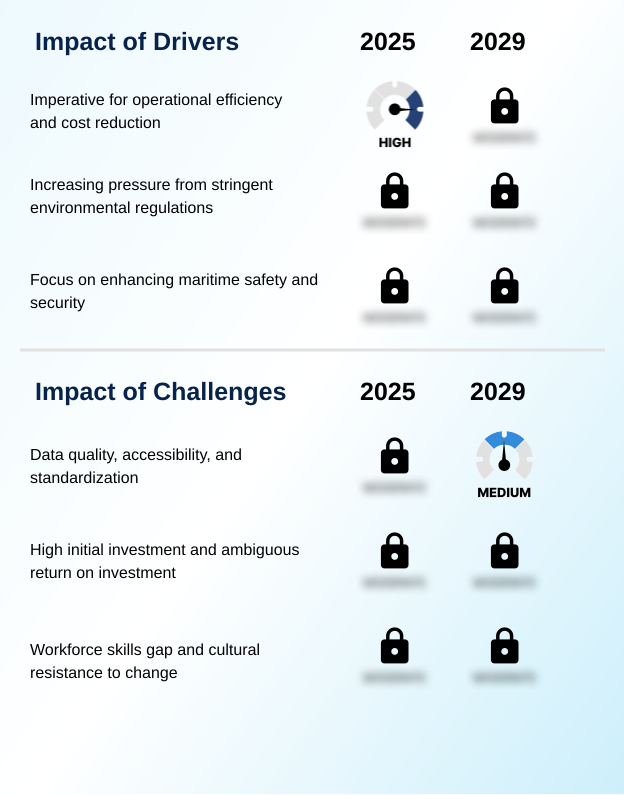

- The imperative for enhancing operational efficiency and achieving significant cost reductions serves as a primary driver for the maritime AI market.

- The imperative for operational efficiency and stringent environmental regulations are primary market drivers.

- The pursuit of cost reduction fuels demand for smart shipping technology and digital fleet management, with AI-powered fleet management platforms showing a capacity to improve fuel efficiency by up to 10%.

- Enhanced safety and security needs also propel growth, spurring development in autonomous cargo ship technology and automated vessel tracking.

- This has led to advancements in deep learning for object classification and the use of unmanned surface vessels (USVs) for maritime domain awareness. AI for marine surveying, utilizing autonomous underwater vehicles (AUVs), is another growth area.

- Furthermore, the push for automated port call optimization and the use of natural language processing (NLP) to streamline documentation are becoming crucial. However, realizing these benefits at scale hinges on achieving maritime data standardization and robust maritime cybersecurity AI.

What are the market trends shaping the Maritime AI Industry?

- The increasing adoption of digital twin technology for holistic asset lifecycle management is emerging as a significant market trend. This approach facilitates a sophisticated evolution from simple data monitoring to comprehensive simulation and predictive optimization.

- A transformative trend is the increasing adoption of digital twins and intelligent vessel systems for holistic asset lifecycle management. This approach integrates maritime data analytics and AI predictive maintenance, allowing operators to simulate performance and diagnose issues virtually. Real-time condition monitoring improves asset reliability, with some systems reducing unexpected equipment failures by over 30%.

- The shift toward edge computing enhances onboard autonomy, supporting AI-assisted navigation with technologies like thermal imaging for navigation and GNSS-denied navigation solutions. The establishment of remote operation centers is also a key trend, centralizing expertise for fleet management.

- These trends are critical for AI-driven route optimization, ensuring both Carbon Intensity Indicator (CII) compliance and EEXI adherence while improving outcomes in maritime risk management AI and port congestion prediction through automated cargo handling at advanced AI for container terminals.

What challenges does the Maritime AI Industry face during its growth?

- Persistent issues related to data quality, accessibility, and the lack of standardization present a key challenge affecting industry growth.

- Significant challenges restrain widespread market adoption, primarily related to data quality, accessibility, and standardization. The fragmented nature of the maritime logistics chain hinders the creation of unified datasets essential for training a robust AI-driven analytics platform. This data fragmentation can undermine the effectiveness of connected ship solutions and intelligent traffic management systems.

- Another challenge is the high initial investment and ambiguous ROI, as retrofitting vessels for maritime process automation requires substantial capital. For example, implementing systems for real-time collision avoidance or predictive analytics for route optimization can represent a major expenditure for smaller operators. A pervasive skills gap and cultural resistance to change also pose hurdles.

- Integrating intelligent crew support systems requires extensive training and a shift in mindset, which is a systemic challenge for an industry built on traditional expertise, impacting applications from autonomous ferry navigation to inland waterway automation.

Exclusive Technavio Analysis on Customer Landscape

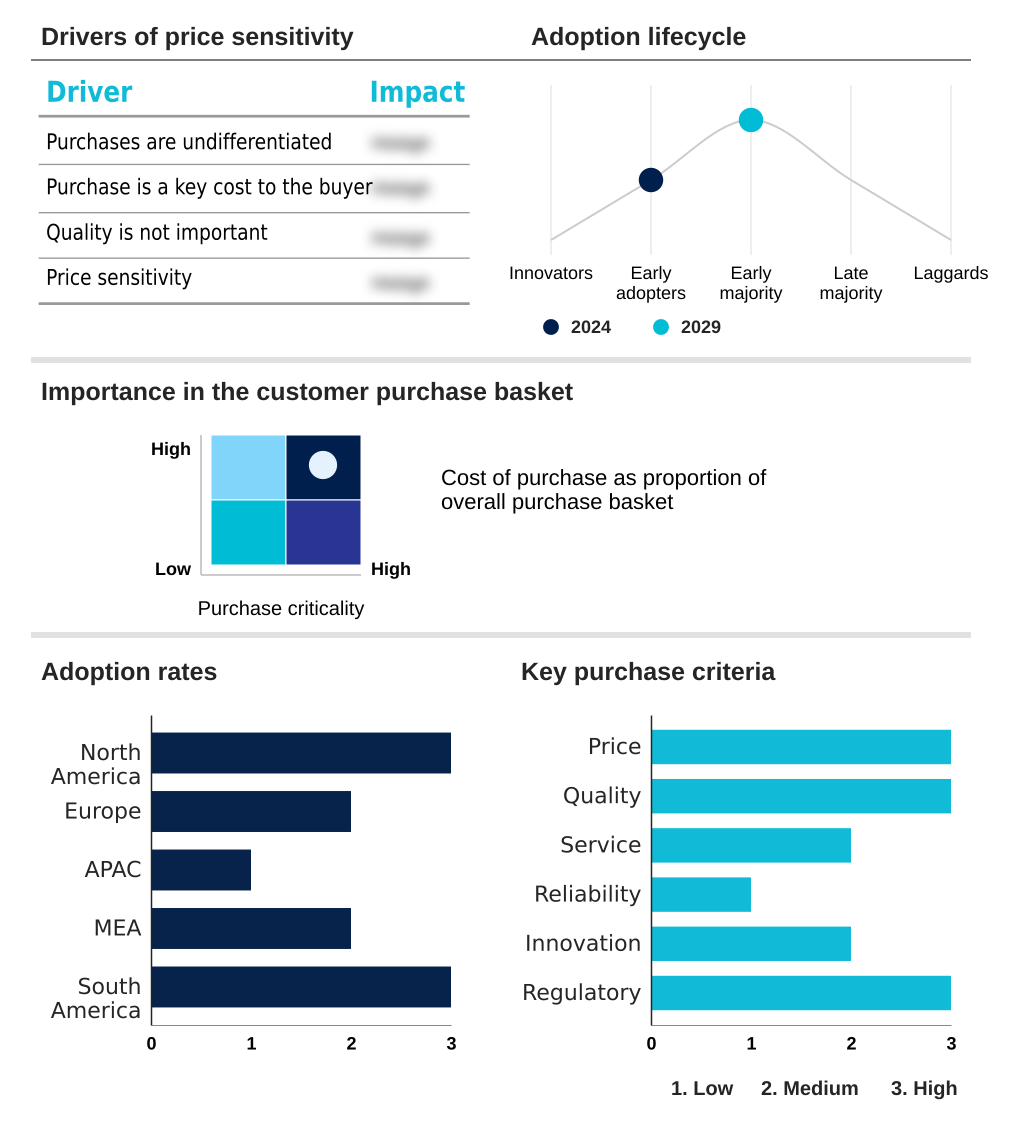

The maritime ai market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the maritime ai market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Maritime AI Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, maritime ai market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Provides autonomous vessel control and predictive maintenance solutions, focusing on enhancing the operational efficiency and safety of maritime assets through advanced AI integration and process automation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Anemo Robotics ApS

- BAE Systems

- Bedrock Ocean Exploration

- Blue Visby Services Ltd.

- Buffalo Automation

- Hefring ehf.

- ladonrobotics

- MARINE WEATHER

- Massterly

- Ocean Revive

- Oracle Corp.

- Rolls Royce Holdings Plc

- Sea Machines Robotics Inc

- Seamo AI

- SentiSystems

- Silo AI

- Stream Ocean

- Zeabuz

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Maritime ai market

- In August 2024, ADNOC Logistics and Services successfully rolled out AIQ's SMARTi intelligent operational safety monitoring solution across 86 of its vessels.

- In September 2024, Shipping Technology secured a strategic investment to advance its AI solutions, including its ST BRAIN integrated platform, for the inland shipping industry.

- In January 2025, Ecopetrol signed a strategic collaboration with AIQ to deploy advanced AI solutions for intelligent safety monitoring and operational support within its maritime activities.

- In March 2025, Lloyds Register announced a partnership with Microsoft to utilize generative AI for advancing the application and licensing of nuclear technology in the maritime sector.

- In May 2025, Orca AI announced a Series B funding round of USD54.2 million to develop its autonomous platform and expand its capabilities into defense and security.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Maritime AI Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 38.9% |

| Market growth 2025-2029 | USD 18978.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 33.7% |

| Key countries | US, Canada, Mexico, Germany, The Netherlands, UK, Spain, Italy, France, China, Japan, South Korea, India, Australia, Indonesia, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is advancing through the integration of sophisticated systems designed to optimize maritime operations. At the core is the autonomous navigation system, which relies on computer vision collision avoidance and sensor fusion for situational awareness to enhance safety.

- This is enabled by high-fidelity sensor integration with LiDAR object detection and thermal imaging for navigation, all processed on ruggedized onboard computing hardware. Operationally, a voyage optimization platform using machine learning for ship fuel optimization and predictive analytics for route optimization is critical for Carbon Intensity Indicator (CII) compliance.

- A robust predictive maintenance model based on real-time condition monitoring has been shown to decrease unexpected downtime by over 25%. The concept of a digital twin for vessel lifecycle management, often running via edge computing for vessels, is gaining traction.

- The development of remote operation centers for autonomous ships is a precursor to managing unmanned surface vessels (USVs) and autonomous underwater vehicles (AUVs) used for tasks like seabed mapping AI. These advancements, from an AI-driven analytics platform to intelligent crew support systems, are reshaping the maritime logistics chain.

What are the Key Data Covered in this Maritime AI Market Research and Growth Report?

-

What is the expected growth of the Maritime AI Market between 2025 and 2029?

-

USD 18.98 billion, at a CAGR of 38.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, Services), Technology (Machine learning, Computer vision, Robotics and autonomous systems, Data analytics, Others), Application (Navigation and route optimization, Predictive maintenance, Port operations and management, Autonomous shipping, Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Imperative for operational efficiency and cost reduction, Data quality, accessibility, and standardization

-

-

Who are the major players in the Maritime AI Market?

-

ABB Ltd., Anemo Robotics ApS, BAE Systems, Bedrock Ocean Exploration, Blue Visby Services Ltd., Buffalo Automation, Hefring ehf., ladonrobotics, MARINE WEATHER, Massterly, Ocean Revive, Oracle Corp., Rolls Royce Holdings Plc, Sea Machines Robotics Inc, Seamo AI, SentiSystems, Silo AI, Stream Ocean and Zeabuz

-

Market Research Insights

- The market dynamics are defined by a strategic push toward smart shipping technology and maritime supply chain optimization. The adoption of AI for maritime safety is a critical factor, with AI-assisted navigation platforms demonstrating an ability to reduce close-quarter incidents by over 40% in trials.

- Concurrently, the drive for decarbonization AI tools is reshaping fleet operational efficiency, as AI-based fuel optimization systems enable fuel savings that contribute to an emissions reduction of up to 15%. This focus on intelligent vessel systems is evident in the rise of remote vessel operations and AI in port management.

- While the ROI for AI predictive maintenance can be ambiguous initially, leading operators report that such systems can decrease unscheduled machinery downtime by more than 25%, significantly boosting vessel availability and profitability. This evidences a clear trend towards leveraging maritime data analytics for tangible performance gains.

We can help! Our analysts can customize this maritime ai market research report to meet your requirements.

RIA -

RIA -