Medical Sensors Market Size 2026-2030

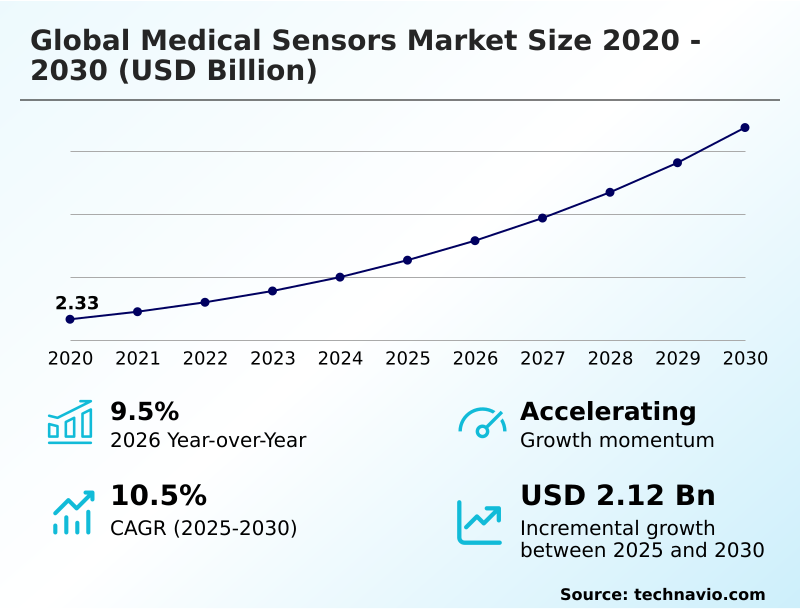

The Medical Sensors Market size was valued at USD 3.27 billion in 2025, growing at a CAGR of 10.5% during the forecast period 2026-2030.

Major Market Trends & Insights

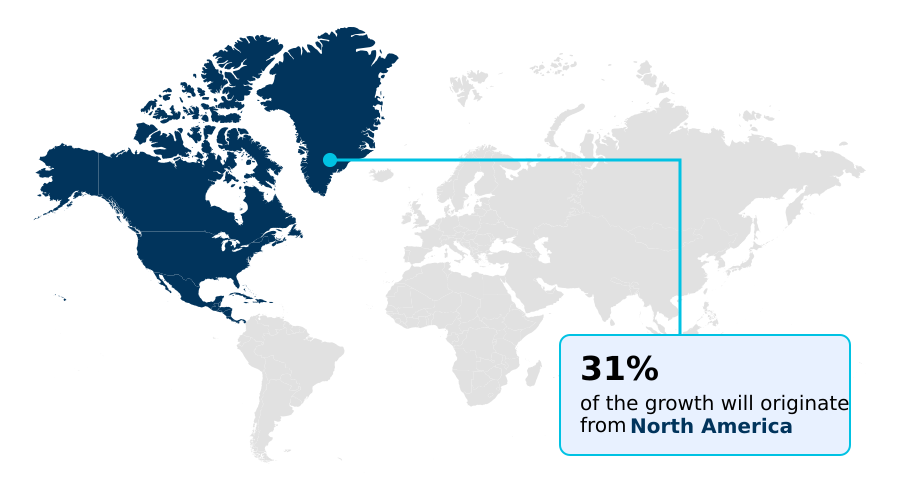

- North America dominated the market and accounted for a 30.8% growth during the forecast period.

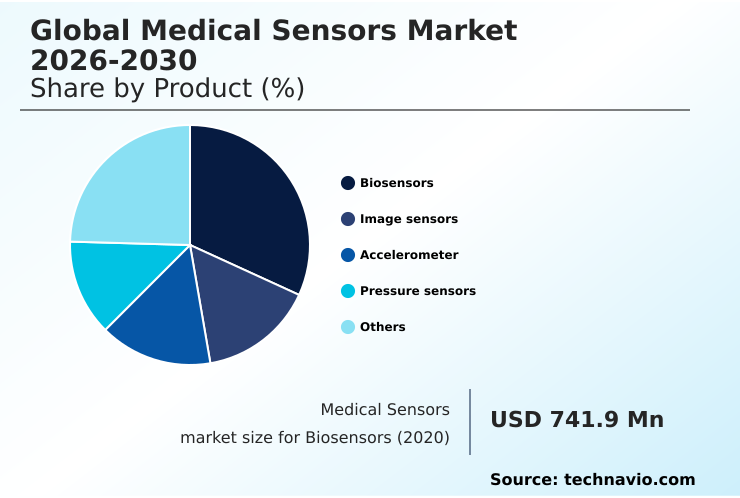

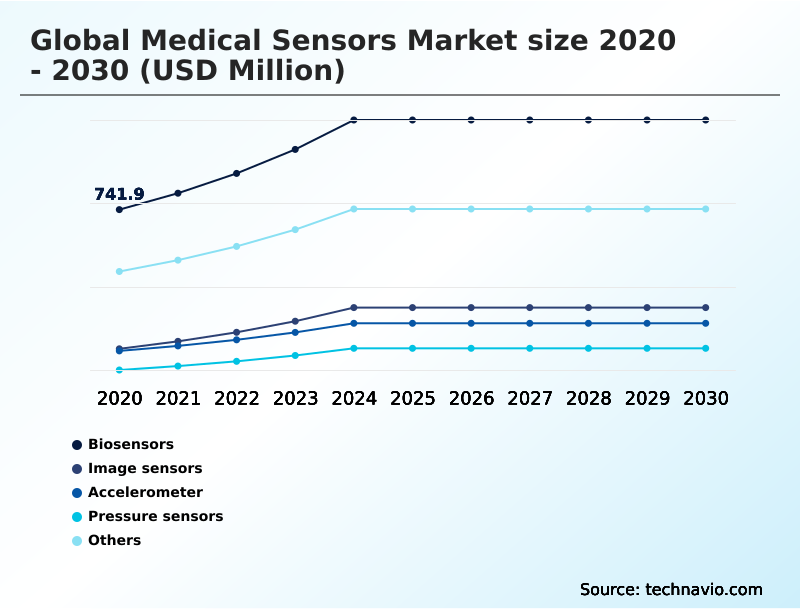

- By Product - Biosensors segment was valued at USD 987.7 million in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 3.05 billion

- Market Future Opportunities 2025-2030: USD 2.12 billion

- CAGR from 2025 to 2030 : 10.5%

Market Summary

- The medical sensors market is characterized by rapid innovation, where demand for continuous monitoring in home care settings now accounts for over 25% of the market.

- In a typical operational scenario, a manufacturer of wearable health technology must balance the high cost of R&D for miniaturization with the price sensitivity of the consumer market, a process where material selection can impact final device costs by up to 40%.

- A primary driver is the surging prevalence of chronic diseases, which necessitates the shift from episodic treatment to continuous, real-time management enabled by these sensors. The integration of sensors into remote patient monitoring (RPM) systems allows healthcare providers to track patient health outside of clinical settings, significantly reducing hospital readmissions.

- However, a significant challenge remains in the form of data security vulnerabilities and privacy concerns in connected healthcare, which can erode patient trust and slow adoption rates.

What will be the Size of the Medical Sensors Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Medical Sensors Market Segmented?

The medical sensors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Biosensors

- Image sensors

- Accelerometer

- Pressure sensors

- Others

- End-user

- Hospitals

- Clinics

- Home care settings

- Connectivity

- Wireless

- Wired

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

How is the Medical Sensors Market Segmented by Product?

The biosensors segment is estimated to witness significant growth during the forecast period.

Biosensors account for over 33% of the medical sensors market, primarily driven by innovations in electrochemical biosensors.

This segment's growth is largely due to the high demand for continuous glucose monitoring devices, which improve patient outcomes by over 25% compared to traditional testing methods.

These analytical devices leverage a biological component for biochemical reaction detection, enabling precise point-of-care diagnostics.

The operational shift toward real-time management of chronic conditions necessitates the use of these advanced sensors, which convert biological stimuli into actionable electrical signals for continuous health tracking and clinical decision support.

The Biosensors segment was valued at USD 987.7 million in 2024 and showed a gradual increase during the forecast period.

How demand for the Medical Sensors market is rising in the leading region?

North America is estimated to contribute 30.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Medical Sensors Market demand is rising in North America Request Free Sample

North America dominates the medical sensors market, contributing over 30% of global revenue, driven by high adoption rates in the US, which itself accounts for more than 80% of the regional market.

In contrast, Asia is the fastest-growing region, with a projected CAGR of 12.4%, significantly higher than North America's 9.4%. This growth is fueled by increasing healthcare expenditure and the expansion of private healthcare in countries like China and India.

The operational difference is stark: North America focuses on advanced remote patient monitoring and value-based care models with established reimbursement frameworks, whereas Asia prioritizes cost-effective, portable point-of-care diagnostics to serve a larger, more dispersed population.

This geographic divergence requires manufacturers to adapt their product strategies, balancing high-tech software-as-a-medical-device features for mature markets with robust, affordable hardware for emerging ones.

What are the key Drivers, Trends, and Challenges in the Medical Sensors Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Exploring the nuances of the global medical sensors market reveals a critical focus on specific applications and their associated challenges. Stakeholders frequently investigate biodegradable medical sensor applications to address issues of e-waste and the need for temporary, non-invasive monitoring, a segment poised for double-digit growth.

- The evaluation of medical sensor fusion accuracy benefits is paramount, as combining data from multiple sources can improve diagnostic reliability by over 20% compared to single-parameter systems. This is especially relevant in complex scenarios like gait analysis or multi-vital sign monitoring.

- However, significant challenges in medical sensor interoperability persist, often cited as a primary barrier to realizing the full potential of connected health ecosystems. Establishing universal standards could reduce integration costs by an estimated 30%.

- Concurrently, the rise of edge AI processing in wearable devices is a key trend, allowing for real-time analysis and alerts while minimizing data transmission and power consumption.

- Finally, a thorough cost-benefit of remote patient monitoring is essential for healthcare providers and payers to justify investment, with studies showing it can reduce hospital readmissions by up to 25%, demonstrating clear ROI and improved patient outcomes.

What are the key market drivers leading to the rise in the adoption of Medical Sensors Industry?

- The surging prevalence of chronic diseases and the concurrent expansion of remote patient monitoring are the primary drivers propelling market growth.

- The rapid advancement in micro-electro-mechanical systems and the Internet of Medical Things (IoMT) is a significant driver for the medical sensors market, enabling miniaturization that reduces device size by over 50% without compromising accuracy.

- This technological convergence has led to the development of highly effective wearable health technology and implantable devices with extended battery life. Favorable regulatory approval pathways for software-as-a-medical-device platforms are also accelerating market entry for innovative sensor technologies.

- The establishment of reimbursement frameworks for remote patient monitoring incentivizes healthcare providers to adopt these solutions, with some providers seeing a 25% reduction in hospital readmissions.

- This combination of technological capability and supportive policy is expanding the use of medical sensors from diagnostics into preventative care and personalized medicine.

What are the market trends shaping the Medical Sensors Industry?

- The emergence of biodegradable and transient electronics is a transformative trend, addressing the need for temporary monitoring solutions that eliminate secondary removal procedures.

- A transformative trend in the medical sensors market is the shift toward multi-parameter sensing and transient electronics, with sensor fusion algorithms improving diagnostic accuracy by up to 20% over single-metric devices.

- This move toward holistic patient assessment is driving the development of compact sensor modules that integrate optical, thermal, and electrochemical elements, allowing a single wearable patch to replace multiple discrete devices. The emergence of biodegradable and biocompatible materials addresses the challenge of medical waste, with transient electronics designed to dissolve in the body after their function is complete.

- This innovation is particularly relevant for post-surgical monitoring, where it can reduce infection risk by eliminating the need for secondary removal procedures by over 90%. This evolution towards more integrated and sustainable solutions is redefining patient monitoring and data acquisition.

What challenges does the Medical Sensors Industry face during its growth?

- Data security vulnerabilities and privacy concerns inherent in connected healthcare ecosystems represent a key challenge affecting industry growth and patient trust.

- The most significant challenge for the medical sensors market is ensuring data security, as the proliferation of connected devices has increased the number of potential cyberattack vectors by over 300% in the last five years.

- Manufacturers face the high cost of implementing robust cybersecurity protocols and data encryption methods to comply with regulations like HIPAA and GDPR, which can add up to 20% to development costs. Another critical hurdle is the lack of interoperability standards across the fragmented market.

- This creates data silos, preventing physicians from getting a unified view of patient-generated health data and limiting the effectiveness of clinical decision support systems. Until universal standards for data exchange are established, the full potential of medical sensors to improve systemic healthcare efficiency will remain constrained.

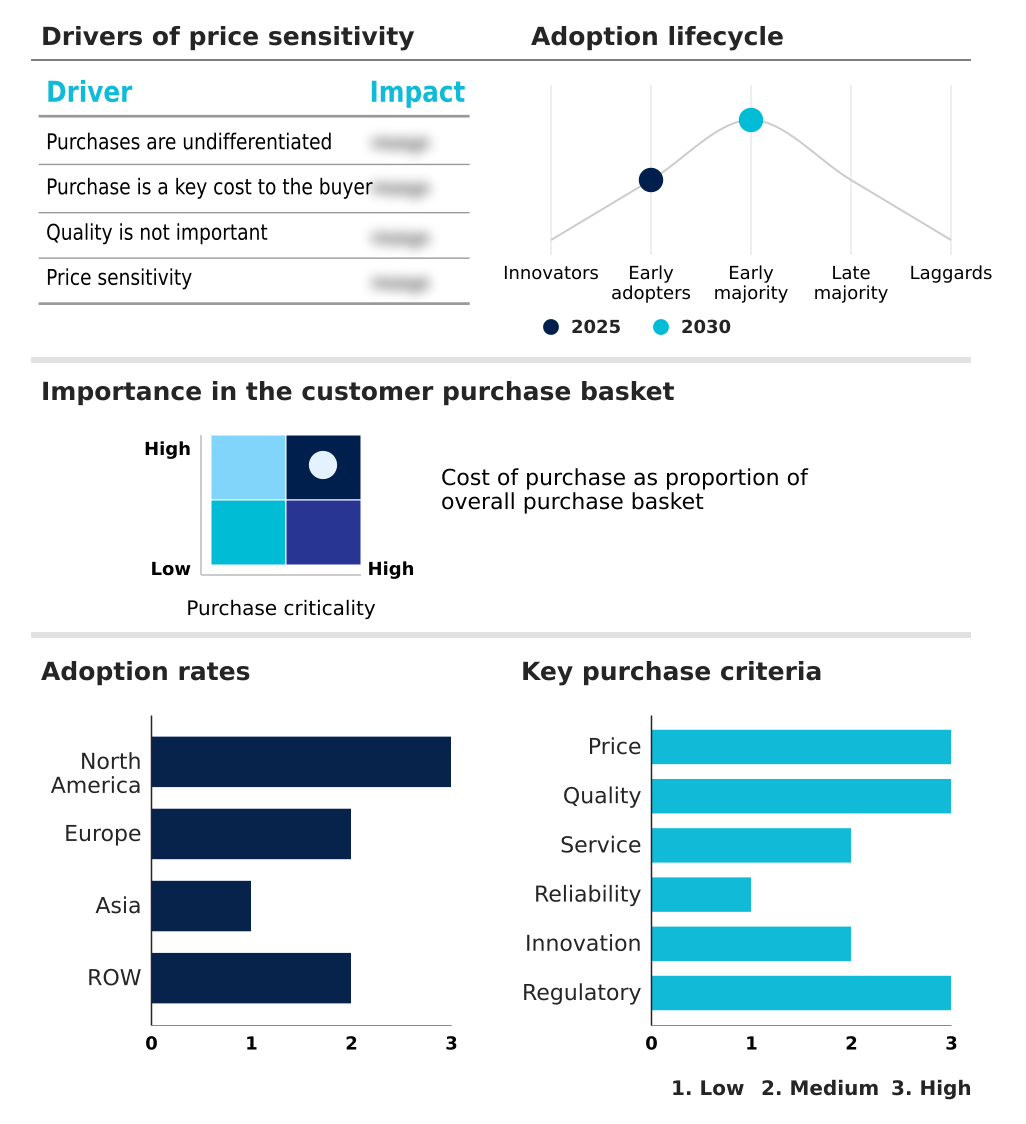

Exclusive Technavio Analysis on Customer Landscape

The medical sensors market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical sensors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Medical Sensors Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, medical sensors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Key offerings include advanced sensor technologies for continuous physiological monitoring, diagnostic imaging, and therapeutic interventions, enabling real-time data acquisition for improved patient outcomes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Amphenol Corp.

- Analog Devices Inc.

- Becton Dickinson and Co.

- Boston Scientific Corp.

- Dexcom Inc.

- Edwards Lifesciences Corp.

- GE HealthCare Technologies

- Honeywell International Inc.

- Koninklijke Philips NV

- Masimo Corp.

- Medtronic Plc

- Nonin Medical Inc.

- NXP Semiconductors NV

- Sensirion AG

- Siemens Healthineers AG

- STMicroelectronics NV

- Stryker Corp.

- TE Connectivity plc

- Texas Instruments Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Life Sciences Tools and Services industry, increasing R&D spending by pharmaceutical companies has expanded the use of medical sensors in clinical trials for more accurate physiological data acquisition, with some trials seeing a 15% improvement in data fidelity.

- A consolidation trend through mergers and acquisitions within the parent market is enabling larger entities to offer more comprehensive medical sensors portfolios, integrating advanced sensor fusion algorithms to create more powerful diagnostic platforms.

- The implementation of stricter regulatory frameworks, such as the Unique Device Identification (UDI) system, is compelling medical sensors manufacturers to enhance traceability and post-market surveillance, impacting supply chain risks and compliance costs.

- Growing demand for contract research organizations is driving the adoption of standardized, high-throughput medical sensors to ensure consistency and reliability across multi-site research projects and value-based care models.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Sensors Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.5% |

| Market growth 2026-2030 | USD 2115.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, Russia, China, India, Japan, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, South Africa, UAE, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The medical sensors market ecosystem involves a complex value chain, where raw material and component suppliers, such as semiconductor firms providing MEMS technology, form the foundational layer, accounting for approximately 15% of the final device cost. Manufacturers like Abbott Laboratories and Medtronic Plc then integrate these components into finished products, ranging from CGMs to implantable devices.

- These products are subject to stringent oversight by regulatory bodies like the FDA and EMA, which can delay market entry by 12 to 18 months. Distribution channels include direct sales to large hospital networks and partnerships with distributors for clinics and home care settings, with the hospital segment representing over 45% of end-user demand.

- The entire ecosystem is supported by contract research organizations that validate sensor efficacy and academic institutions that drive foundational research into new biocompatible materials and sensing modalities.

What are the Key Data Covered in this Medical Sensors Market Research and Growth Report?

-

What is the expected growth of the Medical Sensors Market between 2026 and 2030?

-

The Medical Sensors Market is expected to grow by USD 2.12 billion during 2026-2030, registering a CAGR of 10.5%. Year-over-year growth in 2026 is estimated at 9.5%%. This acceleration is shaped by surging prevalence of chronic diseases and expansion of remote patient monitoring, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Biosensors, Image sensors, Accelerometer, Pressure sensors, and Others), End-user (Hospitals, Clinics, and Home care settings), Connectivity (Wireless, and Wired) and Geography (North America, Europe, Asia, Rest of World (ROW)). Among these, the Biosensors segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, Asia and Rest of World (ROW). North America is estimated to contribute 30.8% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, Russia, China, India, Japan, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, South Africa, UAE, Saudi Arabia and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is surging prevalence of chronic diseases and expansion of remote patient monitoring, which is accelerating investment and industry demand. The main challenge is data security vulnerabilities and privacy concerns in connected healthcare, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Medical Sensors Market?

-

Key vendors include Abbott Laboratories, Amphenol Corp., Analog Devices Inc., Becton Dickinson and Co., Boston Scientific Corp., Dexcom Inc., Edwards Lifesciences Corp., GE HealthCare Technologies, Honeywell International Inc., Koninklijke Philips NV, Masimo Corp., Medtronic Plc, Nonin Medical Inc., NXP Semiconductors NV, Sensirion AG, Siemens Healthineers AG, STMicroelectronics NV, Stryker Corp., TE Connectivity plc and Texas Instruments Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for medical sensors is moderately fragmented, with the top ten vendors accounting for less than 50% of the total market share. Key players such as Medtronic Plc and Abbott Laboratories are aggressively investing in R&D, with some firms increasing their budgets by over 15% to develop next-generation devices like AI-powered continuous glucose monitors and patch-based ambulatory blood pressure monitoring systems.

- This innovation is a direct response to the industry's shift toward value-based care models, which demand more precise and real-time physiological data acquisition. These developments focus on enhancing patient outcomes through remote patient monitoring and early detection.

- However, all vendors face the persistent challenge of ensuring interoperability, as proprietary data formats create silos that can limit the clinical utility of the advanced data these sensors generate.

We can help! Our analysts can customize this medical sensors market research report to meet your requirements.

RIA -

RIA -