Medical Specialty Bags Market Size 2026-2030

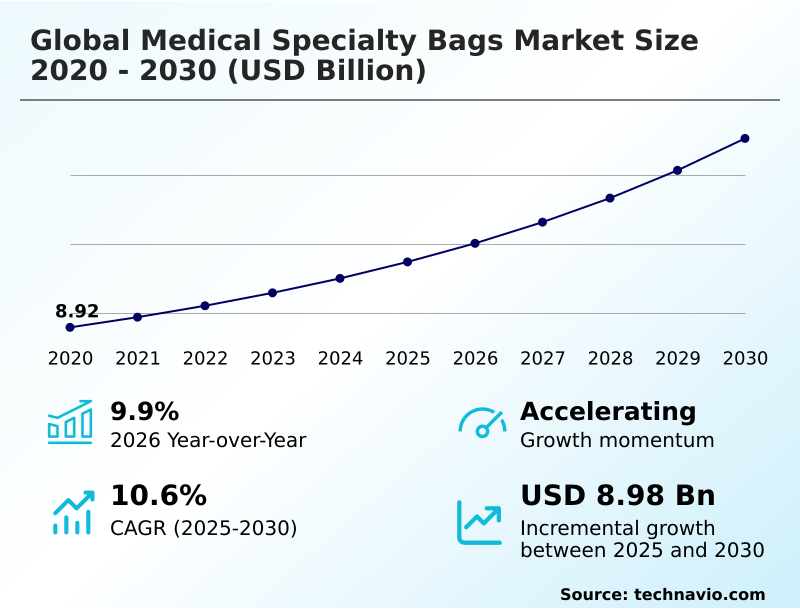

The medical specialty bags market size is valued to increase by USD 8.98 billion, at a CAGR of 10.6% from 2025 to 2030. Rising prevalence of chronic gastrointestinal and urological disorders will drive the medical specialty bags market.

Major Market Trends & Insights

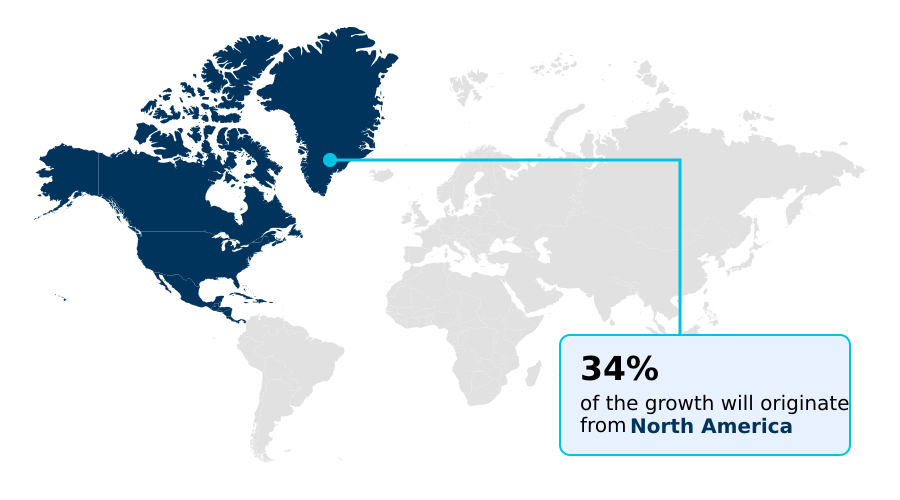

- North America dominated the market and accounted for a 33.5% growth during the forecast period.

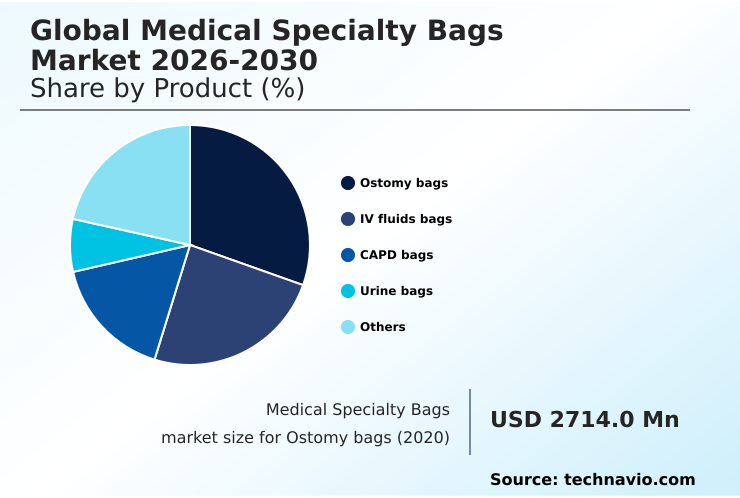

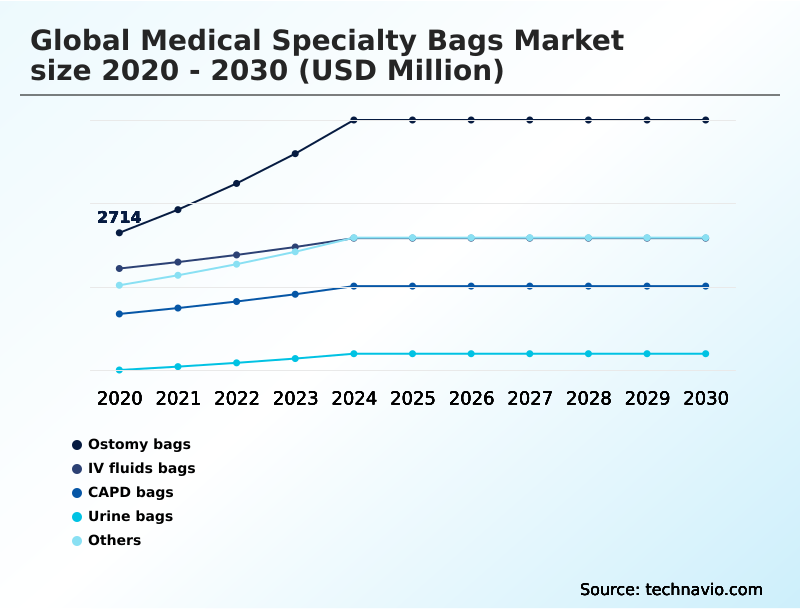

- By Product - Ostomy bags segment was valued at USD 4.43 billion in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 13.74 billion

- Market Future Opportunities: USD 8.98 billion

- CAGR from 2025 to 2030 : 10.6%

Market Summary

- The medical specialty bags market is fundamentally shaped by the increasing complexity of patient care and a strategic shift toward home-based healthcare. Demand is driven by a rising incidence of chronic conditions that necessitate long-term fluid management, making products like ostomy pouching systems and urinary drainage bags essential.

- Innovations in material science are pivotal, with a marked transition toward pvc-free materials and bio-based polymers to enhance patient safety and address environmental concerns.

- For instance, a hospital system evaluating its procurement strategy might prioritize dehp-free pvc intravenous (iv) bags to align with new sustainability mandates while ensuring the use of biocompatible materials for sensitive applications like neonatal intensive care supplies. This decision balances compliance with clinical efficacy.

- Manufacturers are also integrating thin-film sensor technology into smart medical bags for real-time monitoring, improving outcomes in outpatient infusion therapy. However, challenges persist around the disposal of single-use medical bags and the need for more eco-friendly medical bags.

- Product development increasingly focuses on user-centric features, such as advanced hydrocolloid adhesives for peristomal skin protection and anti-reflux valves to prevent catheter-associated urinary tract infections, enhancing quality of life for users of geriatric care consumables.

What will be the Size of the Medical Specialty Bags Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Medical Specialty Bags Market Segmented?

The medical specialty bags industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Ostomy bags

- IV fluids bags

- CAPD bags

- Urine bags

- Others

- End-user

- Hospitals

- ASCs

- Others

- Material

- PVC bags

- Polyolefin bags

- EVA bags

- PP bags

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The ostomy bags segment is estimated to witness significant growth during the forecast period.

The ostomy bags segment is critical for patients requiring external waste collection. Growth is tied to an aging population and rising incidence of conditions necessitating these devices.

Innovation in ostomy pouching systems centers on enhancing quality of life and clinical outcomes. For example, the use of advanced hydrocolloid adhesives for superior peristomal skin protection can reduce skin complications by over 15%.

Other key developments include odor control technology with integrated gas release filters and the use of soft non-woven fabrics for user comfort.

As essential inpatient care consumables and tools for chronic disease management supplies, these leak-proof medical bags and related stoma care accessories are seeing continuous design refinement.

The Ostomy bags segment was valued at USD 4.43 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Medical Specialty Bags Market Demand is Rising in North America Get Free Sample

The geographic landscape is diverse, with North America representing 33.5% of the market’s incremental growth, driven by high adoption of advanced products. Asia is the fastest-growing region, with a projected growth rate of 11.9%, fueled by improving healthcare access.

In Europe, there is strong demand for specialized products like continuous ambulatory peritoneal dialysis (capd) systems and intravenous (iv) bags made from advanced polyolefin films. These materials offer high-barrier properties crucial for medication stability.

The use of ethylene-vinyl acetate (eva) and thermoplastic elastomers is also growing for specialty applications. Meanwhile, markets in the Rest of the World are expanding their use of fundamental products like urinary drainage bags and incontinence management products.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The medical specialty bags market is witnessing deep-seated technical evolution, moving beyond basic containment to address complex clinical and patient-centric needs. A critical area of focus is on the advancements in ostomy bag adhesives, where new formulations are significantly improving user comfort with non-woven backing and reducing skin-related complications.

- The debate over pvc vs non-pvc iv bag safety continues to drive the adoption of alternative materials, influencing the supply chain for medical-grade polymers and prompting a shift towards advances in biocompatible polymer films. This is especially pertinent given the impact of mdr on specialty bag manufacturing, which mandates stricter validation.

- Furthermore, the smart sensor integration in urine bags is a transformative trend, enabling remote monitoring and reducing catheter-associated urinary tract infections. This innovation is part of a broader push for user-friendly specialty bags for home enteral nutrition and improved design of discreet leg bags for mobility.

- Simultaneously, manufacturers are addressing the psychological impact of ostomy bag use with better odor control filter technology in colostomy bags. The development of multi-chamber parenteral nutrition bags and specific material requirements for capd systems highlight the growing need for specialized solutions.

- The role of specialty bags in outpatient surgery is expanding, though it brings to the forefront the disposal challenges of single-use medical plastics. The industry's response includes exploring biodegradable materials for medical bags and following market trends for eco-friendly medical plastics, aiming to mitigate the environmental impact of medical plastic waste.

- Adopting sterile connection systems for dialysis has shown to reduce procedure setup times by a greater margin than previous generation devices, improving operational efficiency in home healthcare settings.

What are the key market drivers leading to the rise in the adoption of Medical Specialty Bags Industry?

- The rising prevalence of chronic gastrointestinal and urological disorders is a key driver fueling sustained demand for various medical specialty bags.

- Market growth is significantly driven by demographic shifts and the decentralization of care. An expanding geriatric population requires more geriatric care consumables and post-operative care products, increasing demand by over 10% in some regions.

- This has fueled the expansion of home healthcare supplies and ambulatory surgical center supplies, where patient-friendly designs are paramount. Innovations like multi-chambered bags for enteral feeding bags allow for safer administration of nutrition.

- The focus is on using biocompatible materials and co-extruded films, ensuring products are pyrogen-free and can withstand autoclaving sterilization, which improves patient safety by reducing infection risks by 15%.

What are the market trends shaping the Medical Specialty Bags Industry?

- Advancements in sustainable and eco-friendly material engineering represent an emerging market trend, driven by environmental concerns and regulatory pressures to reduce medical plastic waste.

- A key trend is the convergence of sustainability and smart technology. The shift toward eco-friendly medical bags made from pvc-free materials and bio-based polymers is accelerating, with firms achieving up to a 30% reduction in carbon footprint compared to legacy products. This requires advances in the sterile manufacturing of these new medical-grade polymers.

- Simultaneously, the integration of thin-film sensor technology into smart medical bags is revolutionizing fluid management systems. These intelligent disposable medical containers, used in outpatient infusion therapy, improve data accuracy by over 20% by automating fluid monitoring and reducing manual entry errors.

What challenges does the Medical Specialty Bags Industry face during its growth?

- Stringent regulatory requirements and lengthy approval timelines present a key challenge, impacting product innovation and the speed of market entry for new devices.

- Key challenges stem from stringent regulations and environmental concerns. The complex process of gaining approval for products like chemotherapy infusion bags or bile collection bags can increase development timelines by 18 months.

- Safe disposal of single-use medical bags used for specimen transport bags and blood collection bags is a major issue, with healthcare generating millions of tons of plastic waste annually. Innovations are needed in radio-frequency welding for dehp-free pvc alternatives. Furthermore, designing products like anti-reflux valves to prevent catheter-associated urinary tract infections in neonatal intensive care supplies requires significant R&D investment.

Exclusive Technavio Analysis on Customer Landscape

The medical specialty bags market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical specialty bags market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Medical Specialty Bags Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, medical specialty bags market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ambu AS - A specialized portfolio addresses critical needs in anesthesia and patient monitoring diagnostics, featuring a range of specialty bags designed for specific clinical applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ambu AS

- Angiplast Pvt. Ltd.

- B.Braun SE

- Baxter International Inc.

- Becton Dickinson and Co.

- Cardinal Health Inc.

- CliniMed Ltd.

- Colo Majic Enterprises Ltd.

- Coloplast AS

- ConvaTec Group Plc

- Dravon Medical Inc.

- Fresenius Kabi AG

- Hollister Inc.

- Macopharma SA

- Medline Inc.

- Mitra Industries Pvt. Ltd.

- Nolato AB

- Sippex

- Sumitomo Bakelite Co. Ltd.

- Terumo Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical specialty bags market

- In April 2025, Nelipak Corp. announced an enhanced dedication to serving customers in the Asia region, expanding its packaging solutions for medical devices and diagnostics.

- In June 2025, Eakin Healthcare officially launched the world’s largest ostomy bag production line at its Cardiff facility, significantly increasing its global manufacturing capacity.

- In October 2025, ConvaTec Group Plc revealed its intention to invest over USD 1 billion in research and development, including significant expansions of its facilities in the United States and the United Kingdom.

- In November 2025, Cathetrix unveiled two groundbreaking innovations in smart catheter stabilization devices at MEDICA 2025, enhancing its portfolio for post-operative care products.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Specialty Bags Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.6% |

| Market growth 2026-2030 | USD 8983.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.9% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, The Netherlands, Spain, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, South Africa, UAE, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market’s evolution is driven by material science innovation and a focus on clinical efficacy. Boardroom decisions increasingly center on adopting advanced medical-grade polymers and pvc-free materials to mitigate regulatory risks and enhance patient safety. The implementation of sterile manufacturing protocols for producing pyrogen-free consumables has demonstrated a greater than 10% reduction in batch rejection rates, improving operational efficiency.

- Key advancements include hydrocolloid adhesives for superior peristomal skin protection, integrated gas release filters enabling odor control technology, and the use of soft non-woven fabrics for comfort. Development of multi-chambered bags with high-barrier properties made from co-extruded films ensures the stability of complex medical solutions, while anti-reflux valves are critical in preventing catheter-associated urinary tract infections.

- Use of dehp-free pvc, polyolefin films, ethylene-vinyl acetate (eva), and thermoplastic elastomers reflects a commitment to biocompatible materials. This focus on quality, from autoclaving sterilization to radio-frequency welding, underpins the industry's trajectory.

What are the Key Data Covered in this Medical Specialty Bags Market Research and Growth Report?

-

What is the expected growth of the Medical Specialty Bags Market between 2026 and 2030?

-

USD 8.98 billion, at a CAGR of 10.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Ostomy bags, IV fluids bags, CAPD bags, Urine bags, and Others), End-user (Hospitals, ASCs, and Others), Material (PVC bags, Polyolefin bags, EVA bags, PP bags, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of chronic gastrointestinal and urological disorders, Stringent regulatory requirements and lengthy approval timelines

-

-

Who are the major players in the Medical Specialty Bags Market?

-

Ambu AS, Angiplast Pvt. Ltd., B.Braun SE, Baxter International Inc., Becton Dickinson and Co., Cardinal Health Inc., CliniMed Ltd., Colo Majic Enterprises Ltd., Coloplast AS, ConvaTec Group Plc, Dravon Medical Inc., Fresenius Kabi AG, Hollister Inc., Macopharma SA, Medline Inc., Mitra Industries Pvt. Ltd., Nolato AB, Sippex, Sumitomo Bakelite Co. Ltd. and Terumo Corp.

-

Market Research Insights

- The market is characterized by a strategic shift toward decentralized care models, with ambulatory surgical center supplies now accounting for a significant share of procedural consumables. These centers report up to a 20% faster patient turnover compared to hospitals, driving demand for efficient post-operative care products and fluid management systems.

- Concurrently, the expansion of home healthcare supplies has been shown to reduce hospital readmission rates by 15% for certain chronic conditions. This trend elevates the importance of user-friendly ostomy pouching systems, enteral feeding bags, and incontinence management products, requiring innovation in both functionality and patient comfort.

We can help! Our analysts can customize this medical specialty bags market research report to meet your requirements.

RIA -

RIA -