Micro Servers Market Size 2024-2028

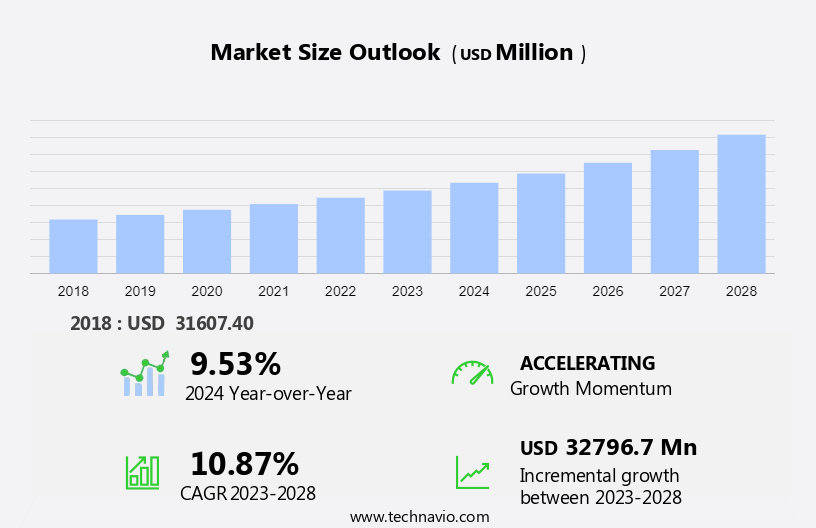

The micro servers market size is forecast to increase by USD 32.8 billion at a CAGR of 10.87% between 2023 and 2028.

- The micro servers market is experiencing significant growth due to the increasing demand for Internet services, smart devices, and social networks. With the wave in data generation from various sources, there is a rising need for high-density servers that offer low power consumption. Cloud services, including hybrid cloud solutions, are also driving market growth as businesses seek to store and process data more efficiently. The trend toward edge computing is another key factor, as organizations look to reduce latency and improve performance by processing data closer to the source. Additionally, increasing investments in data centers and data center consolidation are contributing to market expansion.

What will be the Size of the Market During the Forecast Period?

- Micro servers, also known as computing nodes, have gained significant attention in the technology industry due to their unique hardware configurations. These servers, which utilize low-power processors, RAM, and storage, offer several advantages for businesses seeking to optimize energy costs and physical space requirements. The microserver architecture is a scalable solution that allows organizations to add or remove servers as needed, ensuring system reliability and flexibility. This architecture contrasts with high-end servers, which may not offer the same level of flexibility and can consume more energy and physical space. Micro servers are particularly suitable for applications that require low power consumption, such as web hosting, cloud services, and social networks. One of the key benefits of micro servers is their redundancy. By deploying multiple micro servers, organizations can ensure that their systems remain available even if one server fails.

- Micro servers consume less power than traditional servers, making them an energy-efficient solution. Additionally, their compact size allows for high-density deployments, reducing the overall footprint of the data center. Micro servers can be used in various applications, from personal computers to enterprise-class rack servers and blade servers. They can also be integrated into hybrid cloud environments, where they can be used in conjunction with public cloud providers and private clouds. In conclusion, micro servers offer several advantages for businesses seeking to optimize their IT infrastructure. Their low power consumption, scalability, and redundancy make them an attractive option for applications that require high availability and efficient use of resources. When evaluating micro servers, it is essential to consider the specific requirements of your organization and choose a solution that aligns with your business goals and budget.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Large enterprises

- Small and medium enterprises

- Application

- Data center

- Cloud computing

- Media storage

- Data analytics

- Geography

- North America

- US

- APAC

- China

- Japan

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- North America

By End-user Insights

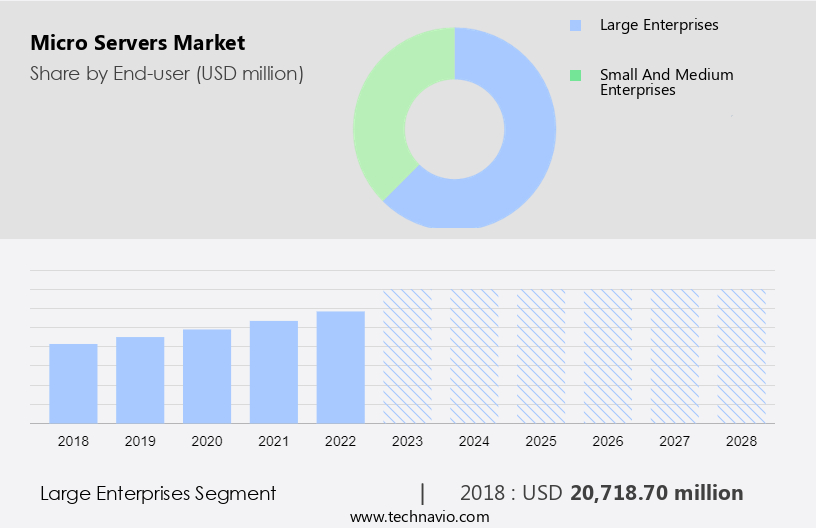

- The large enterprises segment is estimated to witness significant growth during the forecast period.

Micro server architecture has gained significant traction among large enterprises in the US and North America, particularly those with a widespread presence in various industries and geographical locations. Traditional monolithic servers can be costly and complex for organizations with multiple offices, stores, or plants, due to the high expense of hardware and the requirement for substantial physical space. In contrast, micro servers offer an efficient solution for data processing and management, reducing the need for extensive hardware and enabling easy data access and sharing between workplaces. The digital transformation trend, driven by economic development and the increasing importance of data, is fueling the adoption of micro servers.

Cloud-based services, which enable remote access to tools and information, are becoming increasingly popular. The demand for these services is projected to continue growing, leading to an increased reliance on micro servers for data processing and management during the forecast period. Micro servers provide system reliability and redundancy, ensuring that critical data is protected and accessible at all times. This is particularly important for organizations with mission-critical applications or those operating in regulated industries. The use of micro servers also enables organizations to scale their IT infrastructure as needed, making it a cost-effective solution for managing data and processing power.

Get a glance at the market report of share of various segments Request Free Sample

The large enterprises segment was valued at USD 20.72 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

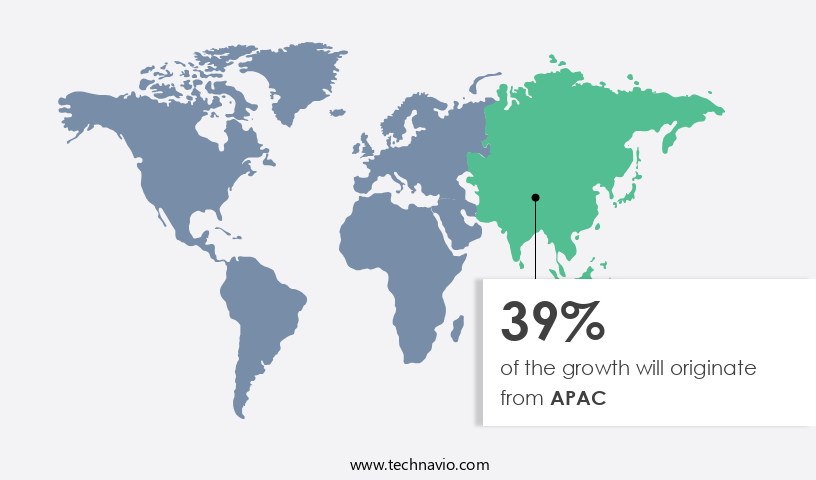

- APAC is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The micro servers market in North America is experiencing significant growth due to the increasing demand for cloud services among businesses in the United States and Canada. Enterprises are shifting towards cloud solutions to minimize their operational and capital expenses associated with on-premises data centers. Hyperscale cloud providers, such as Amazon Web Services (AWS), Microsoft, and Oracle, are popular choices for businesses due to their ability to offer scalable computing capacity at affordable prices. Moreover, investments in telecommunications network infrastructure in the region are on the rise, fueled by the proliferation of Internet of Things (IoT) devices and the emergence of big data analytics.

Further, the adoption of rack-mounted servers, powered by 64-bit processors and System-on-Chips (SoCs) from leading hardware manufacturers like Intel and ARM, is also gaining traction in the region. These servers offer high performance and energy efficiency, making them an ideal choice for data-intensive applications. In summary, the micro servers market in North America is witnessing growth due to the increasing adoption of cloud services, the rise in data traffic, and the demand for high-performance servers. The region's established data centers, such as Apple's six data centers, are contributing to the market's growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Micro Servers Market?

The shift toward edge computing is the key driver of the market.

- The market is experiencing significant growth due to the increasing adoption of edge computing in various sectors, including autonomous vehicles, smart manufacturing, and smart cities. Edge computing is a network architecture that enables data processing and storage near the source, reducing latency and enhancing server response. This architecture has gained popularity among small and medium-sized enterprises (SMEs) and large-scale enterprises alike, seeking efficient and secure data management solutions. Edge data centers are being established to accommodate the growing demand for compact servers, which are essential components of edge computing. The increasing use of smartphones, social platforms, and big data applications further fuels the demand for micro servers.

- Edge computing offers several advantages, such as faster data processing, improved security, and reduced bandwidth requirements, making it an attractive solution for various industries. Micro servers are compact and energy-efficient servers designed for edge computing applications. They offer high processing power and can be easily integrated into various systems, making them an ideal choice for enterprises looking to optimize their data management infrastructure. The enterprise end-user segment is expected to dominate the market due to the increasing demand for efficient and secure data management solutions. In conclusion, the market is poised for growth due to the rising adoption of edge computing and the increasing demand for efficient and secure data management solutions.

What are the market trends shaping the Micro Servers Market?

Increased investments in data centers and particularly hyper-scale data centers (HDCs) is the upcoming trend in the market.

- Micro servers, a more advanced iteration of conventional data centers, have gained significant traction due to the escalating demand for higher data storage capacity and enhanced computing speed. The market experienced notable growth in 2022, driven by substantial investments from public cloud providers, such as hyperscalers, in expanding and constructing new data centers. Over the past few years, these companies have collectively poured approximately USD 200 billion into capacity expansion and the establishment of new data centers. For instance, Google announced an investment of USD 13 billion to build new data centers. These investments from hyperscalers are fueling the expansion of The market.

- Public cloud providers, including hyperscalers, are increasingly turning to micro servers to support their Big Data analytics initiatives. Micro servers offer a greater number of physical servers and virtual machines compared to traditional servers, making them an ideal solution for handling the massive data processing requirements of Big Data analytics. As per the latest market research, The market is expected to continue its upward trajectory, with increasing adoption across various industries. The market is anticipated to grow at a steady pace, driven by the surging demand for cloud computing services and the need for high-performance computing solutions.

What challenges does Micro Servers Market face during the growth?

Increasing data center consolidation is a key challenge affecting market growth.

- The market is experiencing growth due to the increasing demand for Internet services and the proliferation of smart devices. With the generation of massive amounts of data from social networks and various devices, there is a rising need for efficient and low-power solutions for cloud services. High-density micro servers are gaining popularity as they offer a cost-effective and energy-efficient alternative to traditional servers. Data center consolidation is a significant trend driving the market's growth. Service providers are adopting hybrid cloud solutions to optimize their IT infrastructure and reduce costs. Hybrid cloud allows organizations to leverage both public and private cloud services, providing the benefits of both worlds.

- The consolidation of data centers leads to significant cost savings for service providers. By reducing the number of physical data centers, they can save on hardware and operational expenses. Additionally, micro servers' low power consumption makes them an attractive option for organizations seeking to minimize their carbon footprint. In conclusion, the US market is poised for growth due to the increasing demand for Internet services, the proliferation of smart devices, and the trend toward data center consolidation. High-density micro servers offer a cost-effective and energy-efficient solution for cloud services, making them an attractive option for organizations seeking to optimize their IT infrastructure.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acer Inc.

- Dawning Information Industry Co. Ltd.

- Dell Technologies Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise Co.

- Inspur Group.

- Intel Corp.

- IRON Global Inc.

- Lenovo Group Ltd.

- Plat Home Co. Ltd.

- Quanta Computer Inc.

- Super Micro Computer Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Micro servers, also known as computing nodes, are compact hardware configurations designed for data processing in various applications. These servers utilize low-power processors, RAM, and storage to minimize energy costs and physical space requirements. The microserver architecture offers scalability and redundancy, ensuring system reliability for digital transformation initiatives. Micro servers are increasingly popular in data centers due to their ability to process large volumes of data in real-time. They are essential for cloud computing, virtualization, containerization technologies, and edge computing. These servers cater to diverse industries, including data analytics, web hosting, network services, and IoT solutions. Micro servers are not limited to data centers alone.

Additionally, the enterprise end-user segment benefits from micro servers in various sectors such as smart manufacturing, smart cities, and 5G solutions. Micro servers enable economic development by reducing energy costs and physical space requirements, making them an attractive option for organizations seeking to optimize their IT infrastructure. With advancements in processors, including 64-bit processors and System-on-Chips (SoCs) from Intel and ARM, micro servers continue to evolve and offer enhanced performance and capabilities.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

157 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.87% |

|

Market growth 2024-2028 |

USD 32.80 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

9.53 |

|

Key countries |

US, China, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -