Naval Combat Systems Market Size 2024-2028

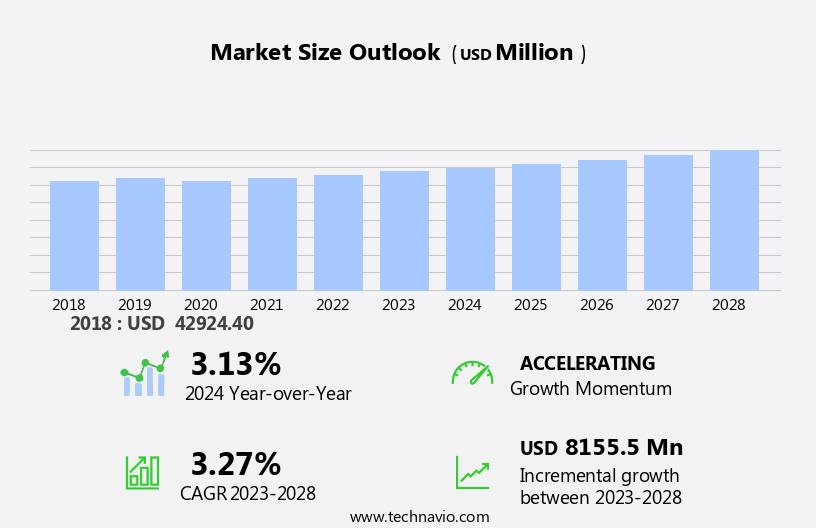

The naval combat systems market size is forecast to increase by USD 8.16 billion at a CAGR of 3.27% between 2023 and 2028.

- The market is experiencing significant growth due to several key trends. One major factor driving market expansion is the increasing focus on Intelligence, Surveillance, and Reconnaissance (ISR) operations. With heightened geopolitical tensions and the need for enhanced security, defense spending is on the rise. This trend is further fueled by the technological complexity and integration issues that come with advanced naval combat systems. As nations seek to modernize their naval fleets, the demand for sophisticated combat systems is increasing. Emerging technologies, such as directed energy weapons and laser weapon systems, are revolutionizing naval warfare. Supply chain constraints, engineering, logistics, and after-sales services are crucial considerations for market participants. However, the integration of these systems into existing fleets presents challenges, requiring significant resources and expertise. Despite these challenges, the market is expected to continue growing, as nations prioritize their defense capabilities to ensure national security.

What will be the Size of the Naval Combat Systems Market During the Forecast Period?

- The market is experiencing significant growth due to ongoing fleet modernization programs and the integration of advanced technologies. Shipyard workers are in high demand as international navies invest in upgrading their vessels with state-of-the-art systems. The C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) segment is a key driver, with increasing demand for system integration, safety, and automation. Navies are also focusing on system safety, cyber security solutions, and configuration control to ensure the reliability and effectiveness of their combat systems.

- The integration of AI-based vehicles, navigation sensors, and a bridge integration platform further enhances operational capabilities. Key players In the market include Fincantieri, Ultra Electronics, and SAAB, among others. System safety, system integration, and navigation sensors are critical focus areas for these companies.

How is this Naval Combat Systems Industry segmented and which is the largest segment?

The naval combat systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

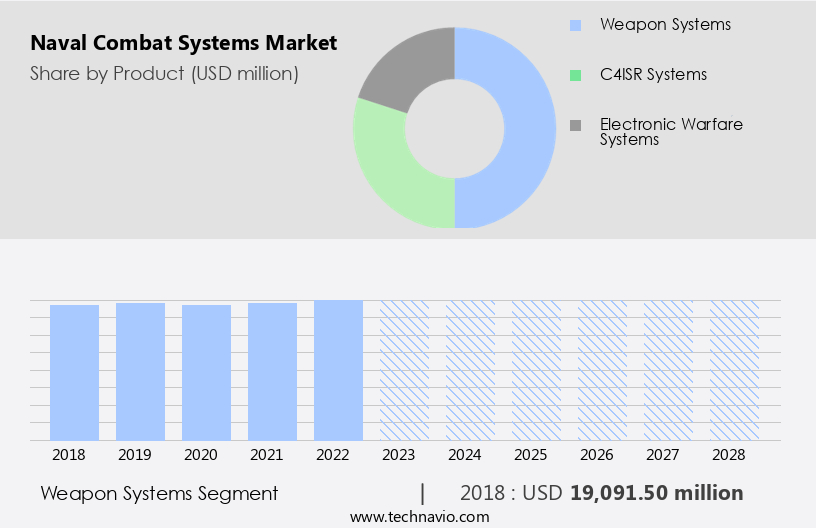

- Product

- Weapon systems

- C4ISR systems

- Electronic warfare systems

- Geography

- North America

- US

- APAC

- China

- Japan

- Europe

- Germany

- UK

- Middle East and Africa

- South America

- North America

By Product Insights

- The weapon systems segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth due to the increasing demand for advanced weapon systems on naval surface combatants. The integration of directed energy weapons, such as laser weapon systems, and the modernization of fleet programs are key drivers. For instance, Fincantieri, a leading shipbuilder, is investing in engineering, logistics, and after-sales services to meet the needs of international navies. The integration of subsystems, such as gyros, radars, situational awareness displays, C2 systems, visual surveillance systems, automation, unmanned operation missions, AI-based vehicles, and combat management systems, is essential for enhancing the capabilities of naval vessels. Additionally, the integration of cyber security solutions and configuration control is crucial for maintaining system safety and program management.

Key players, including Ultra Electronics and Saab, are focusing on the development of electronic warfare, weapon systems, and small patrol boats, as well as large aircraft carriers, submarines, and frigates. The integration of friend nation systems and crew training is also important for effective intelligence, situational awareness, planning, decision-making, and enemy target detection. Radar detection and ship type-specific combat boats and patrol boats are also significant areas of investment.

Get a glance at the market report of share of various segments Request Free Sample

The Weapon systems segment was valued at USD 19.09 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

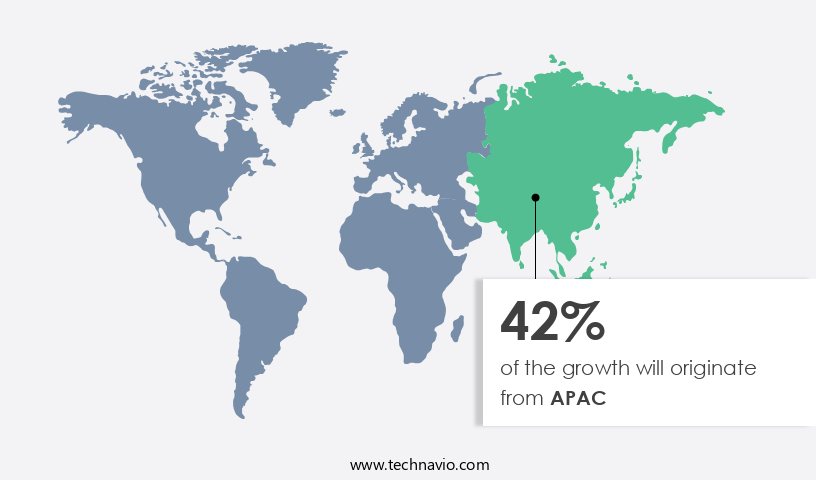

- APAC is estimated to contribute 42% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The North American market is a significant and evolving sector, fueled by technological innovations and strategic defense requirements. The United States, as the market leader In the region, prioritizes naval modernization and expansion, driving the demand for advanced combat systems. Key components of naval combat systems consist of radar and sonar systems, electronic warfare equipment, command and control systems, and missile defense systems. These technologies ensure superior situational awareness, precise targeting, and effective threat neutralization, vital for contemporary naval operations. Fleet modernization programs, including those for naval surface combatants, submarines, and aircraft carriers, are integral to the market's growth.

Additionally, the integration of directed energy weapons, such as laser weapon systems, and unmanned operation missions, including AI-based vehicles, further enhance naval capabilities. International navies' demand for advanced systems, focusing on surveillance, system integration, system safety, program management, and crew training, also contributes to the market expansion. Key players In the sector include Fincantieri, Ultra Electronics, Saab, and Electronic Warfare, providing engineering, logistics, after sales services, and cyber security solutions. Key components of naval combat systems include gyros, radars, situational awareness displays, C2 systems, visual surveillance systems, automation, and navigation sensors. The market encompasses various naval assets, including combat boats, patrol boats, frigates, and large aircraft carriers, as well as friend nation subsystems, intelligence, planning, decision making, enemy target radar detection, and ship type-specific systems.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Naval Combat Systems Industry?

Increasing focus on ISR operations is the key driver of the market.

- The market encompasses advanced technologies and systems designed for Intelligence, Surveillance, and Reconnaissance (ISR) operations in naval warfare. ISR plays a crucial role in military missions by providing commanders with real-time information for effective decision-making in high-risk situations. Surveillance employs sensors to generate imagery or videos of the battlefield, while reconnaissance is the process of obtaining information about enemy troops or terrain features. These operations have seen significant advancements due to their strategic importance. The market is witnessing rapid developments in areas such as system integration, configuration control, and cyber security solutions. Shipyard workers and international navies are investing in fleet modernization programs, integrating advanced technologies like directed energy weapons, laser weapon systems, and AI-based vehicles.

- Naval surface combatants, including frigates, destroyers, and large aircraft carriers, are being equipped with advanced C2 systems, gyros, radars, situational awareness displays, and visual surveillance systems. Submarines and small patrol boats also benefit from these advancements, enhancing their capabilities for unmanned operation missions. Key players In the market include Fincantieri, Saab, Ultra Electronics, and others. They provide engineering, logistics, after sales services, and electronic warfare systems. The market is characterized by program management, system safety, and navigation sensors, all contributing to the overall effectiveness of naval combat systems. The market is experiencing significant growth due to the increasing importance of ISR operations in naval warfare.

- The market is driven by advancements in technology, fleet modernization programs, and the need for enhanced situational awareness and decision-making capabilities.

What are the market trends shaping the Naval Combat Systems Industry?

Increasing geopolitical tensions and increased defense spending is the upcoming market trend.

- The market encompasses various technologies and systems used in naval warfare, including supply chain constraints, shipyard workers, fleet modernization programs, and advanced systems such as directed energy weapons and laser weapon systems. Firms like Fincantieri, Ultra Electronics, Saab, and Electronic Warfare provide engineering, logistics, after sales services, and system integration for international navies. Open architecture combat systems, such as those offered by Raytheon Technologies, enable easy integration of new interfaces and modes of interaction, reducing costs and minimally impacting existing components. In 2016, the US Navy awarded Lockheed Martin a five-year COMbat System Components-Based Total-Ship System (COMBATSS-21) contract worth USD 795 million for system safety, program management, and configuration control of naval surface combatants.

- Naval systems also include gyros, radars, situational awareness displays, C2 systems, visual surveillance systems, automation, unmanned operation missions, AI-based vehicles, and combat management systems. Key components include navigation sensors, cyber security solutions, and bridge integration platforms. The market comprises various ship types, including combat boats, patrol boats, frigates, aircraft carriers, and submarines, as well as friend nation subsystems, crew, intelligence, situational awareness, planning, decision making, enemy target radar detection, and ship type-specific systems.

What challenges does the Naval Combat Systems Industry face during its growth?

Technological complexity and integration issues is a key challenge affecting the industry growth.

- The market encompasses the supply of advanced technologies for naval combat, including sensors, fire control, ordnance, and control systems. Effective Combat System Integration (CSI) is crucial for the successful coordination of these components, sourced from various companies, in warships. CSI involves the integration of gyros, radars, situational awareness displays, C2 systems, visual surveillance systems, automation, unmanned operation missions, AI-based vehicles, combat management systems, navigation sensors, cyber security solutions, and more. Navies face challenges in CSI due to the unique requirements of each component and the complexity of integrating them. Delays and costs associated with improper integration can ground valuable warships, hindering naval missions.

- Despite the importance of CSI, it is a common issue In the international naval community, with many nations experiencing lengthy deployment timelines for combat systems. Shipyard workers play a significant role In the market, as they are responsible for the engineering, logistics, after-sales services, and program management aspects of fleet modernization programs. Companies like Fincantieri, Ultra Electronics, Saab, and Electronic Warfare provide subsystems for various ship types, including Small Patrol Boats, Large Aircraft Carriers, Submarines, and Combat Boats. Naval surface combatants, such as Frigates and Destroyers, require sophisticated systems for intelligence, situational awareness, planning, decision making, and enemy target detection.

- Radar detection systems, for instance, are essential for detecting and tracking enemy targets at a distance. The integration of these systems, along with crew training and cyber security solutions, is vital for maintaining fleet readiness and ensuring mission success.

Exclusive Customer Landscape

The naval combat systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the naval combat systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, naval combat systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASELSAN AS

- ATLAS ELEKTRONIK GmbH

- BAE Systems Plc

- Elbit Systems Ltd.

- General Dynamics Mission Systems Inc.

- HAVELSAN Inc.

- L3Harris Technologies Inc.

- Leonardo Spa

- Lockheed Martin Corp.

- Naval Group

- Northrop Grumman Corp.

- QinetiQ Ltd.

- RTX Corp.

- Saab AB

- Safran SA

- Terma AS

- Thales Group

- Ultra Electronics Holdings Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of technologies and applications designed to enhance the capabilities of naval forces. This market is driven by several factors, including the need for fleet modernization, advancements in technology, and the evolving threat landscape. Fleet modernization programs are a significant driver for the market. Shipyards around the world are constantly working to upgrade existing vessels and build new ones, incorporating the latest technologies to improve their combat capabilities. This includes the integration of advanced sensors, communication systems, and weapon systems. One area of focus in naval combat systems is the development of directed energy weapons and laser weapon systems.

These technologies offer the potential for non-kinetic engagement of enemy targets, reducing the need for traditional munitions and minimizing collateral damage. Firms are investing heavily in research and development to bring these systems to market. Another key area of growth In the market is system integration. With the increasing complexity of naval platforms, there is a growing need for seamless integration of various subsystems to ensure optimal performance and interoperability. This includes the integration of gyros, radars, situational awareness displays, C2 systems, visual surveillance systems, automation, and unmanned operation missions. Logistics and after-sales services are also crucial components of the market.

International navies require ongoing support to maintain their fleets, including the provision of spare parts, training, and maintenance services. Firms are responding to this demand by offering integrated logistics support and developing advanced configuration control systems to ensure the timely delivery of parts and services. Safety and program management are critical considerations In the market. With the high stakes involved in naval operations, there is a strong focus on ensuring the safety and reliability of combat systems. This includes rigorous testing and certification processes, as well as the implementation of program management practices to ensure projects are delivered on time and on budget.

The market is diverse, encompassing a range of naval surface combatants, from small patrol boats to large aircraft carriers and submarines. Each type of vessel presents unique challenges and requirements, driving innovation and investment in technologies such as electronic warfare, weapon systems, and intelligence gathering. Naval combat systems also play a critical role in enhancing situational awareness and decision-making capabilities. This includes the use of advanced sensors and data processing technologies to detect and identify enemy targets, as well as the integration of AI-based vehicles and cyber security solutions to improve situational awareness and planning. The market is a dynamic and complex industry, driven by the need for fleet modernization, technological advancements, and the evolving threat landscape.

Firms operating in this market must stay abreast of the latest trends and developments to remain competitive, while also ensuring the safety, reliability, and interoperability of their systems. Whether it's the integration of advanced sensors and communication systems, the development of directed energy weapons, or the provision of logistics and after-sales services, the market is a critical enabler of naval power and capability.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

149 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.27% |

|

Market growth 2024-2028 |

USD 8.15 Billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.13 |

|

Key countries |

US, China, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Naval Combat Systems Market Research and Growth Report?

- CAGR of the Naval Combat Systems industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the naval combat systems market growth of industry companies

We can help! Our analysts can customize this naval combat systems market research report to meet your requirements.

RIA -

RIA -