North America Automotive Camera Market Size 2024-2028

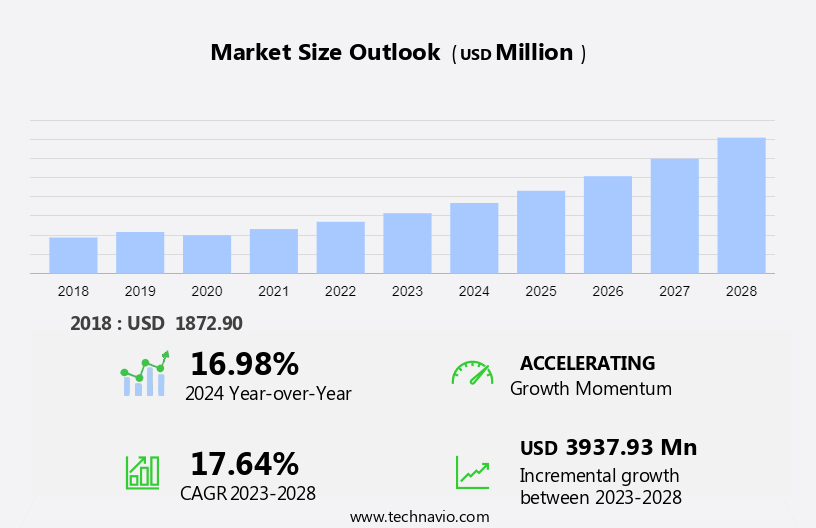

The North America automotive camera market size is forecast to increase by USD 3.94 billion at a CAGR of 17.64% between 2023 and 2028.

- In North America, the market is witnessing significant growth due to the increasing prioritization of automotive active safety systems among consumers. The use of advanced camera technologies, such as rear-view, driver monitoring, 360-degree, top-view, and bird's-eye cameras, is becoming increasingly common in new vehicles. These cameras provide real-time views of congested areas, crowded parking spaces, and obstacles, reducing the risk of accidents. However, the high installation cost and integration challenges are limiting the adoption of these advanced safety features in older models.

- Additionally, the limited space in vehicles and the need for calibration can pose challenges in the implementation of these systems. High-definition (HD) digital cameras are increasingly being adopted to enhance image quality and improve safety. The market is expected to continue its growth trajectory, driven by the increasing demand for advanced safety features and the development of more cost-effective camera technologies.

What will be the size of the market during the forecast period?

- The market is witnessing significant growth due to the increasing demand for advanced safety features and convenient driving experiences in both passenger cars and commercial vehicles. These cameras play a crucial role in enhancing vehicle safety by providing real-time images of the vehicle's surroundings, enabling features such as traffic sign recognition, pedestrian detection systems, and park assist. Digital and infrared cameras are the primary types of automotive cameras used in the industry. Digital cameras capture visible light, while infrared cameras detect heat signatures, making them suitable for low-light conditions and nighttime driving.

- Additionally, these cameras are integrated into various safety systems, such as lane departure warnings, blind spot detection, and collision avoidance systems. Auto manufacturers are focusing on integrating these cameras into entry-level vehicles to cater to the growing demand for affordable safety features. The integration of automotive cameras is not limited to passenger cars alone; commercial vehicles, including buses and trucks, are also adopting these technologies to improve safety and operational efficiency. The market is driven by the increasing focus on vehicle safety and the need for convenient driving experiences. Pedestrian detection systems, for instance, help prevent accidents by alerting the vehicle's driver of pedestrians in the vicinity.

- Similarly, park assist systems make it easier for drivers to maneuver their vehicles into tight parking spaces. Moreover, traffic sign recognition systems help drivers stay informed of speed limits, no passing zones, and other road signs, ensuring a safer driving experience. These systems use advanced imaging technology to identify and display the relevant sign information to the driver in real-time. The integration of automotive cameras also enhances the overall safety of vehicle occupants. Seatbelts and airbags are no longer the only safety features that automakers focus on; real-time imaging of the vehicle's surroundings is becoming an essential safety feature.

- In the event of an accident, these cameras can provide valuable evidence to aid in insurance claims and investigations. In conclusion, the market is expected to continue growing as auto manufacturers focus on enhancing vehicle safety and providing convenient driving experiences. The integration of these cameras into various safety systems is revolutionizing the automotive industry, making roads safer for all road users.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Digital

- Infrared

- Thermal

- Type

- Front view camera

- Rear view camera

- Surround view camera

- Geography

- North America

- Canada

- Mexico

- US

- North America

By Technology Insights

- The digital segment is estimated to witness significant growth during the forecast period.

In North America, the automotive camera market is witnessing significant growth as auto manufacturers integrate advanced digital camera technology into vehicles for enhanced safety features and convenient driving experiences. Digital cameras, including those with high megapixel sensors and sophisticated image processing capabilities, are being used to capture clearer visual information for traffic signs, pedestrians, and other vehicles. DENSO Corp. And Continental AG are among the companies leading this innovation. Surround-view systems, which rely on digital cameras for a 360-degree view, are increasingly popular for parking assistance and improving overall situational awareness.

Additionally, digital rearview mirrors, which replace traditional mirrors with camera-based displays, are gaining traction due to their wider field of view and integration with safety features like blind-spot monitoring and cross-traffic alerts. Infrared and thermal cameras are also being adopted for advanced safety applications, such as pedestrian detection systems. These cameras help vehicles identify potential hazards, contributing to overall vehicle safety. As the demand for safer and more technologically advanced vehicles continues to rise, the market is poised for continued growth. The market will grow at a steady pace, driven by the increasing adoption of safety devices and the integration of cameras into various vehicle systems. This trend is expected to continue as consumers prioritize safety and convenience in their purchasing decisions.

Get a glance at the market share of various segments Request Free Sample

The digital segment was valued at USD 926.49 million in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of North America Automotive Camera Market?

The priority of automotive safety among customers is the key driver of the market.

- The market has witnessed expansion due to the rising consumer preference for improved vehicle safety and regulatory mandates promoting the implementation of advanced driver assistance systems (ADAS) in vehicles. North American consumers are increasingly conscious of safety features in automobiles, with easily accessible information about crash test ratings and safety technologies shaping their purchasing decisions. Regulatory organizations in North America, such as the National Highway Traffic Safety Administration (NHTSA), have established safety standards and initiatives, making it essential for manufacturers like Robert Bosch GmbH to comply. These onboard cameras play a crucial role in providing real-time images of the vehicle's surroundings, aiding the driver in executing vehicle maneuvers safely.

- Furthermore, insurance companies are increasingly considering the presence of such safety features when assessing accident claims, adding to the market's growth. The integration of AI-based cameras in entry-level vehicles and the development of self-driving cars are additional factors contributing to the market's expansion. The market is expected to continue growing, driven by the increasing consumer disposable income, stable automobile sales, and decreasing commodity prices. In-car safety features remain a priority for consumers, ensuring the market's sustained growth.

What are the market trends shaping the North America Automotive Camera Market?

Increased use of wide-angle camera technology is the upcoming trend in the market.

- In the North American automotive industry, there is a rising preference for advanced driver assistance systems (ADAS) that utilize wide-angle cameras. These cameras, including UHD, stereo, monocular, and thermal types, contribute significantly to features such as park assist systems, road sign assistance, and intelligent headlight control. Wide-angle cameras are essential for 360-degree surround-view camera systems, which have gained popularity in the US, Canada, and Mexico due to their benefits in parking assistance and maneuvering in confined areas.

- Additionally, these systems employ multiple wide-angle cameras strategically placed around the vehicle to offer a comprehensive view, facilitating parking, maneuvering, and obstacle detection. Additionally, digital dash cams with GPS tracking, parking mode, motion detection, and connected software with online dashboards are gaining traction in security applications, including blind spots, cargo holds, and night vision using infrared thermography.

What challenges does North America Automotive Camera Market face during the growth?

High replacement costs associated with camera modules is a key challenge affecting the market growth.

- Advanced camera systems, including rear-view, driver monitoring, 360-degree, top-view, and bird's-eye cameras, are increasingly being integrated into vehicles in North America to enhance safety and convenience. However, the high replacement costs of these camera modules act as a significant barrier to their widespread adoption by automakers in the US, Canada, and Mexico. The integration of these advanced camera technologies, such as high-definition (HD) cameras, into vehicles comes with a high installation cost, which can deter automakers from incorporating them into their offerings.

- For consumers, the replacement costs of these camera modules contribute to the total cost of ownership for a vehicle, potentially influencing purchasing decisions, particularly in price-sensitive markets. Moreover, the perceived high replacement costs may also impact the resale value of vehicles equipped with advanced camera systems. Despite these challenges, the demand for advanced safety features continues to grow, and car manufacturers are exploring ways to reduce the cost of these systems while maintaining their effectiveness.

Exclusive North America Automotive Camera Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Autoliv Inc.

- BorgWarner Inc.

- Continental AG

- DENSO Corp.

- Fluke Corp.

- Garmin Ltd.

- Gentex Corp.

- HELLA GmbH and Co. KGaA

- Hitachi Ltd.

- Intel Corp.

- LG Electronics Inc.

- Magna International Inc.

- NVIDIA Corp.

- Panasonic Holdings Corp.

- Ricoh Co. Ltd.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Teledyne Technologies Inc.

- Valeo SA

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth due to the increasing integration of advanced safety devices in passenger cars and commercial vehicles. These safety features include traffic sign recognition, pedestrian detection systems, and cross-traffic alert, among others. Digital and infrared cameras, as well as thermal cameras, are commonly used in these systems. Auto manufacturers are focusing on providing convenient driving experiences and enhancing vehicle safety through the use of cameras. Advanced camera technologies such as intelligent cameras, smart cameras, and automated emergency braking (AEB) systems are becoming increasingly popular. These systems help in detecting objects, motion paths, and distances in real-time, providing the vehicle's driver with crucial information about the surroundings.

Additionally, the adoption of these camera-based systems is driven by various factors, including consumer awareness, supporting legislation, and increased demand for safety and comfort in vehicles. The premium segment vehicles and automotive OEMs are leading the market, with tie-ups and active safety systems becoming more common. However, high installation cost and integration challenges remain key challenges for the market. The market is also witnessing the emergence of self-driving cars and AI-based cameras, which are expected to revolutionize the automotive industry. These technologies are enabling advanced safety features such as lane departure warning (LDW) systems, adaptive cruise control, and blind spot detection.

Moreover, the market is witnessing the adoption of 5G, network connectivity, and cloud data, which are enabling V2V and V2X communications and vehicular infrastructure. The market is also witnessing the growth of electric vehicles (EVs), and battery manufacturers are playing a crucial role in the market's growth. However, the market is also facing challenges such as complex connections, increased wiring, and limited space in older models. Calibration and standardization are also key challenges for the market, particularly for multi-camera systems.

In conclusion, the market is witnessing significant growth due to the increasing adoption of advanced safety features, consumer awareness, and supporting legislation. The market is also witnessing the emergence of self-driving cars and AI-based cameras, which are expected to revolutionize the automotive industry. However, challenges such as high installation cost, integration, and calibration remain key challenges for the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

159 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 17.64% |

|

Market growth 2024-2028 |

USD 3.94 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

16.98 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -