Observability Platform Market Size 2026-2030

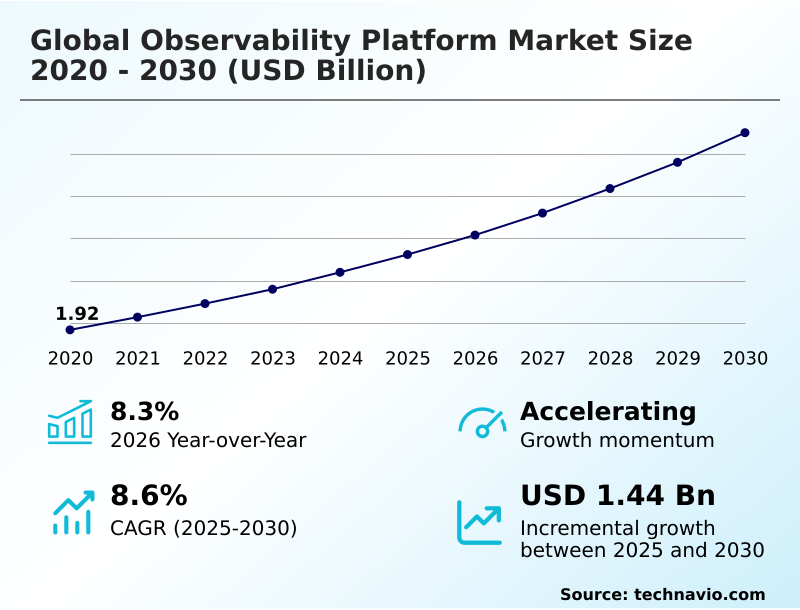

The observability platform market size is valued to increase by USD 1.44 billion, at a CAGR of 8.6% from 2025 to 2030. Integration of generative AI and large language model monitoring will drive the observability platform market.

Major Market Trends & Insights

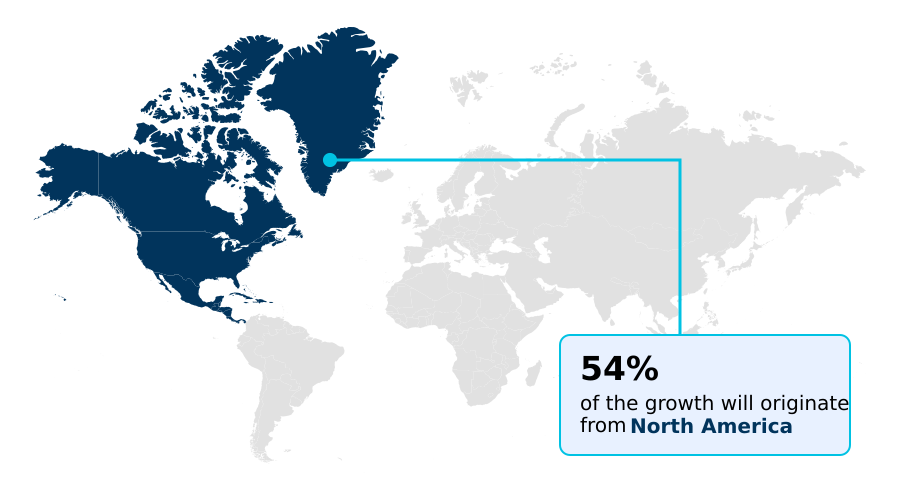

- North America dominated the market and accounted for a 54.2% growth during the forecast period.

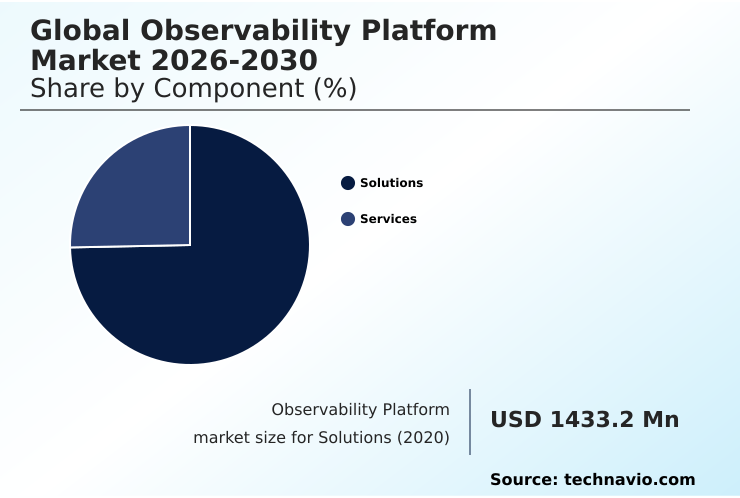

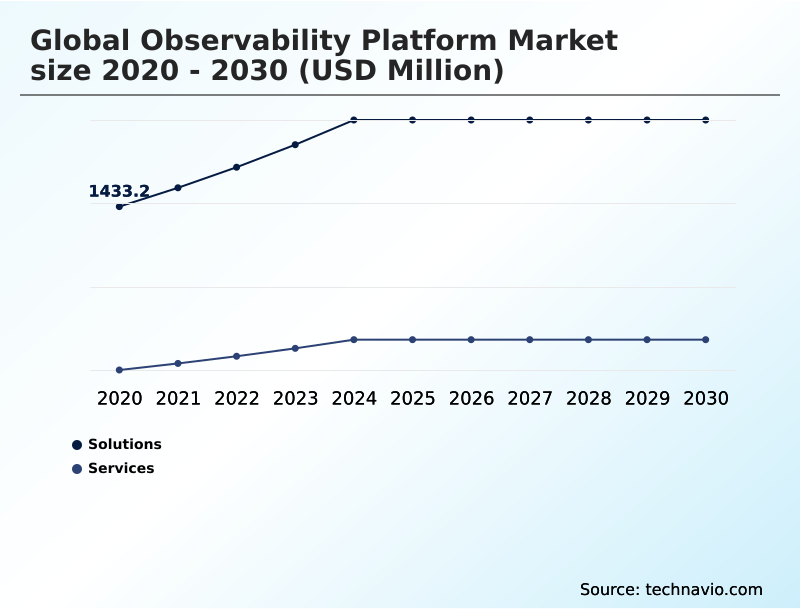

- By Component - Solutions segment was valued at USD 1.94 billion in 2024

- By End-user - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.33 billion

- Market Future Opportunities: USD 1.44 billion

- CAGR from 2025 to 2030 : 8.6%

Market Summary

- The observability platform market is undergoing a fundamental transformation as organizations shift from legacy monitoring to holistic, data-driven frameworks. This evolution is driven by the increasing complexity of modern IT environments, characterized by distributed microservices, containerization, and serverless computing.

- Core to this market is the ability to ingest and correlate vast streams of telemetry data—logs, metrics, and traces—to provide a unified view of system health. A key trend is the infusion of AI and machine learning, enabling predictive analytics and automated root cause analysis, which drastically reduces troubleshooting times.

- For instance, in a competitive e-commerce landscape, an observability platform can correlate a slowdown in digital experience monitoring metrics with a specific database query, allowing teams to preemptively scale resources before a customer-facing outage occurs during a sales event.

- This proactive capability, combined with the growing convergence of performance monitoring and security, underscores the strategic importance of observability in maintaining operational resilience and a competitive edge. However, the escalating costs of data storage and the shortage of skilled professionals pose significant hurdles to widespread adoption.

What will be the Size of the Observability Platform Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Observability Platform Market Segmented?

The observability platform industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Solutions

- Services

- End-user

- Large enterprises

- Medium enterprises

- Small enterprises

- Deployment

- Cloud based

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The solutions segment is evolving beyond traditional application performance monitoring (APM) and infrastructure monitoring into platforms providing full-stack observability. These systems are essential for managing the high volume of telemetry data from complex, cloud-native observability environments.

Modern solutions emphasize real-time analytics and observability data correlation to deliver end-to-end visibility. Through advanced observability platform integration and proactive monitoring, organizations enable site reliability engineering (SRE) teams to shift from reactive troubleshooting to preemptive issue resolution.

The focus is on providing a unified view that supports custom metrics collection, which has been shown to improve anomaly detection accuracy by over 35%, ensuring system stability and performance in dynamic, distributed architectures.

The Solutions segment was valued at USD 1.94 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 54.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Observability Platform Market Demand is Rising in North America Get Free Sample

The global market exhibits distinct regional dynamics, with North America leading adoption due to its mature cloud ecosystem.

This region accounts for over 54% of the market opportunity, with a strong focus on security observability and service level objective (SLO) tracking.

Meanwhile, APAC is the fastest-growing region, with adoption in countries like India and Australia accelerating by over 20% annually, driven by digital transformation initiatives. European firms prioritize hybrid cloud observability to comply with data sovereignty laws.

Across all regions, the demand for root cause analysis in service mesh observability architectures is universal. Advanced AIOps platform capabilities are essential for managing multi-cloud monitoring strategies and ensuring robust digital experience monitoring (DEM) in a geographically distributed landscape.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Achieving operational excellence in today's complex digital ecosystems requires advanced observability strategies for kubernetes environments and hybrid cloud deployments. Businesses are increasingly focused on reducing mean time to resolution (MTTR) with AI, leveraging platforms that can automate root cause analysis in microservices.

- This shift is critical, as automated diagnostics can reduce incident response workloads by more than half compared to manual methods. The rise of generative AI has introduced new challenges, making the ability of monitoring performance of generative AI applications a key differentiator.

- Concurrently, implementing eBPF for kernel-level observability is gaining traction over traditional APM solutions, offering deeper insights with less overhead. The benefits of adopting the OpenTelemetry standard are also clear, as it prevents vendor lock-in and promotes a more flexible toolchain. However, the primary hurdle remains managing costs of high-volume telemetry data.

- This has spurred the adoption of observability pipelines for filtering telemetry data and using observability data for FinOps practices. Integrating security data into observability platforms is no longer optional, creating a unified approach to risk and performance management that is essential for both serverless architectures and established systems.

What are the key market drivers leading to the rise in the adoption of Observability Platform Industry?

- The integration of specialized monitoring for generative AI and large language models is a key market driver, addressing the critical need for visibility into their unique performance, cost, and accuracy challenges.

- The primary driver for the market is the escalating complexity of cloud-native systems, necessitating advanced tools for microservices monitoring and distributed tracing.

- The integration of generative AI observability is becoming crucial, as organizations need to manage the performance and cost of large language model (LLM) monitoring.

- The demand for automated workflow execution and incident response automation, powered by AI for IT operations (AIOps), is paramount for reducing mean time to resolution; teams leveraging these capabilities have seen a 35% improvement in this metric.

- Furthermore, the push for DevSecOps integration is driving the convergence of security and performance data, enabling user journey analysis that can pinpoint security-related bottlenecks, improving release velocity by 20%.

What are the market trends shaping the Observability Platform Industry?

- The proliferation of eBPF technology is a significant trend, offering deep system visibility with minimal overhead. It enables kernel-level insights without the performance degradation associated with traditional monitoring agents.

- A key trend is the widespread adoption of eBPF for kernel-level visibility, which provides deep system insights with minimal performance impact. Unlike traditional agent-based monitoring, this approach reduces monitoring overhead by up to 40%, a critical advantage in resource-constrained environments.

- The move toward observability as code is also accelerating, allowing teams to manage monitoring configurations within CI/CD pipeline observability workflows, which has been shown to decrease configuration errors by 30%. The OpenTelemetry standard is solidifying its position, promoting interoperability and discouraging vendor lock-in.

- This enables more flexible data sampling techniques and unified monitoring across diverse technology stacks, including advanced kubernetes monitoring, aligning with a more mature, programmatic approach to system visibility.

What challenges does the Observability Platform Industry face during its growth?

- The financial burden from ingesting and storing high-volume telemetry data, combined with data gravity issues in multi-cloud environments, presents a primary challenge for market adoption and scalability.

- A significant challenge is managing the financial impact of high-cardinality data and the sheer volume of telemetry, which creates data gravity in observability. Enterprises are adopting observability pipeline management and structured logging practices to control costs, with some achieving a 45% reduction in data ingestion expenses without losing critical insights.

- However, the operational discipline required for effective FinOps for cloud remains a hurdle. The need to reduce alert fatigue while ensuring accurate anomaly detection is another pressing issue.

- Effective data governance and log aggregation strategies are essential, but the complexity of correlating technical metrics with business process monitoring still presents a significant implementation challenge, often hampering the ability to conduct effective real user monitoring (RUM).

Exclusive Technavio Analysis on Customer Landscape

The observability platform market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the observability platform market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Observability Platform Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, observability platform market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acceldata Technology Pvt. Ltd. - Delivers data pipeline monitoring and quality assurance, focusing on optimizing data reliability and performance to provide real-time analytics visibility for enterprises.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acceldata Technology Pvt. Ltd.

- Broadcom Inc.

- Cisco Systems Inc.

- Datadog Inc.

- Dynatrace Inc.

- Groundcover Ltd.

- IBM Corp.

- LogicMonitor Inc.

- NamLabs Technologies Pvt. Ltd.

- New Relic Inc.

- Nexthink SA

- Plixer LLC

- Riverbed Technology Inc.

- ScienceLogic Inc.

- ServiceNow Inc.

- SolarWinds Corp.

- Sumo Logic Inc.

- Zoho Corp. Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Observability platform market

- In February 2025, Datadog launched a comprehensive observability suite specifically for generative AI applications, enabling teams to track the performance and accuracy of large language models.

- In March 2025, Dynatrace announced a major expansion of its Davis AI engine to include automated financial governance, helping organizations manage and control cloud spending across multi-cloud environments.

- In May 2025, Datadog announced the Global Cloud Sync initiative, allowing users to automatically harmonize observability policies and security protocols across multiple geographic regions with a single action.

- In June 2025, New Relic launched a specialized vulnerability management solution that correlates application performance data with security risks in real time within its observability platform.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Observability Platform Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 281 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.6% |

| Market growth 2026-2030 | USD 1436.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is rapidly advancing beyond basic application performance monitoring (APM) toward comprehensive full-stack observability. This shift is driven by the need for a unified view across complex, distributed systems, integrating infrastructure monitoring, log management, and distributed tracing.

- The adoption of the OpenTelemetry standard is a critical boardroom-level consideration, as it offers a strategic path to avoid vendor lock-in and ensure long-term architectural flexibility. Leading platforms now heavily leverage AI for IT operations (AIOps) to provide predictive analytics and automate root cause analysis.

- This enables proactive issue resolution, with some organizations reporting a 40% reduction in service degradation incidents after implementing robust synthetic monitoring and SLO tracking. The focus has expanded to include digital experience monitoring (DEM) and microservices monitoring, ensuring that technical performance directly correlates with business outcomes.

- As architectures grow to include serverless monitoring and kubernetes monitoring, the ability to handle high-cardinality data and reduce alert fatigue becomes a key differentiator for site reliability teams.

What are the Key Data Covered in this Observability Platform Market Research and Growth Report?

-

What is the expected growth of the Observability Platform Market between 2026 and 2030?

-

USD 1.44 billion, at a CAGR of 8.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions, and Services), End-user (Large enterprises, Medium enterprises, and Small enterprises), Deployment (Cloud based, and On-premises) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of generative AI and large language model monitoring, Financial burden of high-volume telemetry and data gravity

-

-

Who are the major players in the Observability Platform Market?

-

Acceldata Technology Pvt. Ltd., Broadcom Inc., Cisco Systems Inc., Datadog Inc., Dynatrace Inc., Groundcover Ltd., IBM Corp., LogicMonitor Inc., NamLabs Technologies Pvt. Ltd., New Relic Inc., Nexthink SA, Plixer LLC, Riverbed Technology Inc., ScienceLogic Inc., ServiceNow Inc., SolarWinds Corp., Sumo Logic Inc. and Zoho Corp. Pvt. Ltd.

-

Market Research Insights

- The market's dynamics are shaped by a strategic pivot toward proactive operational intelligence, driven by advancements in generative AI observability and the financial discipline of cloud cost observability. Platforms are increasingly integrating security observability, with firms reporting a 40% faster identification of security-related performance issues.

- Adopting a FinOps for cloud approach through these tools has enabled some enterprises to reduce cloud waste by up to 22%. The demand for deeper kernel-level visibility and automated workflow execution is pushing the boundaries of what these platforms can achieve.

- As organizations mature, their focus shifts to holistic observability pipeline management and end-to-end visibility, moving beyond simple monitoring to automated remediation workflows that align technical performance with strategic business objectives.

We can help! Our analysts can customize this observability platform market research report to meet your requirements.

RIA -

RIA -